One of the biggest draws of the Citi Prestige card is the 4th Night Free benefit, which allows cardholders to stay four nights at a hotel for the cost of three. Depending on how frequently you travel and the types of accommodation you stay in, the value from this benefit can more than cover the card’s S$535 annual fee.

As great as that sounds, there have been some disconcerting developments abroad. The 4th Night Free benefit has been capped at five uses per calendar year on the Indonesia version and two on the US/India versions. The Thailand version is going to cap the benefit at two uses per calendar year from April 2020.

Thanks to all this, there’s been a kind of looming dread that it’s only a matter of time before a similar devaluation happens in Singapore.

Changes are coming to the Citi Prestige’s 4th Night Free benefit

Well, Citibank has unveiled some changes to the Citi Prestige’s 4th Night Free benefit that take effect from 1 March 2020.

The good news is the changes aren’t what everyone’s fearing. The benefit’s not getting capped, at least not yet.

The bad news is that Citi is adding restrictions in terms of the types of properties that qualify, and a requirement that the stay be fully prepaid. Also, depending on how cynical you feel, there might be a hint that a cap is in the works (more on that later).

New restrictions on qualifying stays

The 4th Night Free benefit currently excludes full board rates and any hotels that come as part of a package rate (e.g those including airfare and car rental).

From 1 March 2020, the following restrictions will be added:

| The following stays will not qualify for this benefit: ◦ Full and Half board room stays ◦ Single and multi-room suites ◦ Home & Farm Stays ◦ Serviced apartments ◦ Villas ◦ Packaged stay and member rates, such as air and hotel, hotel and car rental, hotel and meals bundled promotions |

Now, it’s Citi’s prerogative to tweak the 4th Night Free benefit as business needs dictate, but I do have issues with is how nebulously-defined these terms are.

I mean, OK, it’s pretty straightforward to determine if a rate is full or half-board, but what about the restrictions regarding suites? I get that the spirit of the rule is to for people to book the base-category room, but things are much more complicated in practice.

For example, at the St Regis Bali the entry-level rooms are called “suites”. Does that mean all stays at the St Regis Bali will be ineligible for the 4th Night Free benefit?

Or consider the “all suite property” tag that some hotels like to give themselves to sound exclusive. Are all such properties going to be excluded from the 4th Night Free benefit too?

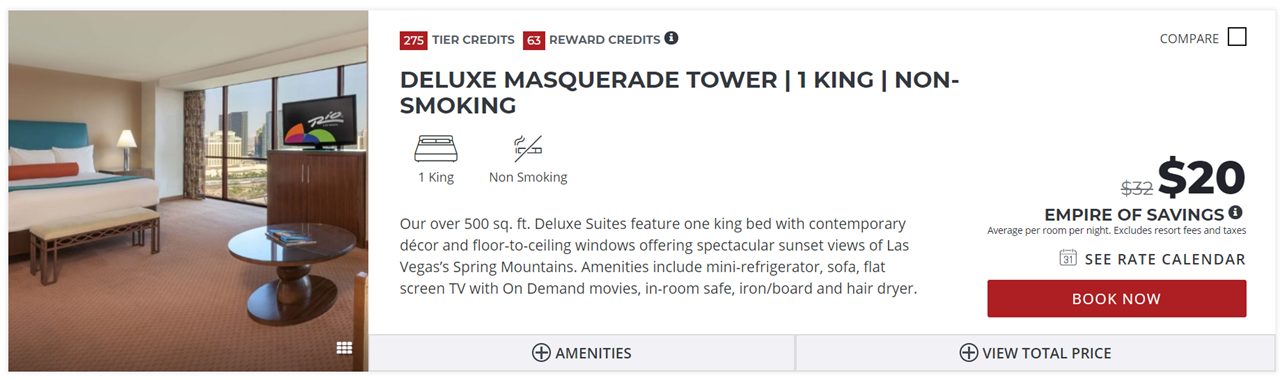

It’d be weird if that happens, because in many cases, the “all suite” tag is more marketing than reality. Some so-called “all suite” properties are actually pretty cheap and dumpy- the Rio All-Suite Las Vegas is a great case in point. When a “Deluxe Suite” is going for US$20 a night…

It’d be weird if that happens, because in many cases, the “all suite” tag is more marketing than reality. Some so-called “all suite” properties are actually pretty cheap and dumpy- the Rio All-Suite Las Vegas is a great case in point. When a “Deluxe Suite” is going for US$20 a night…

And what about villas? Presumably this refers to the holiday villas you see in places like Bali which come with multiple bedrooms, private pools, waitstaff and chefs, but many resort hotels may adopt the “villa” nomenclature to describe even base rooms.

For example, one of my favourite non-chain properties is the Maca Villas & Spa in Seminyak, Bali. The base level rooms are villas in the sense that they’re free-standing buildings with their own pools and backyards. But in all other ways, the property functions like a hotel with communal facilities like restaurants and a main pool. So does this run afoul of the “no villa” rule?

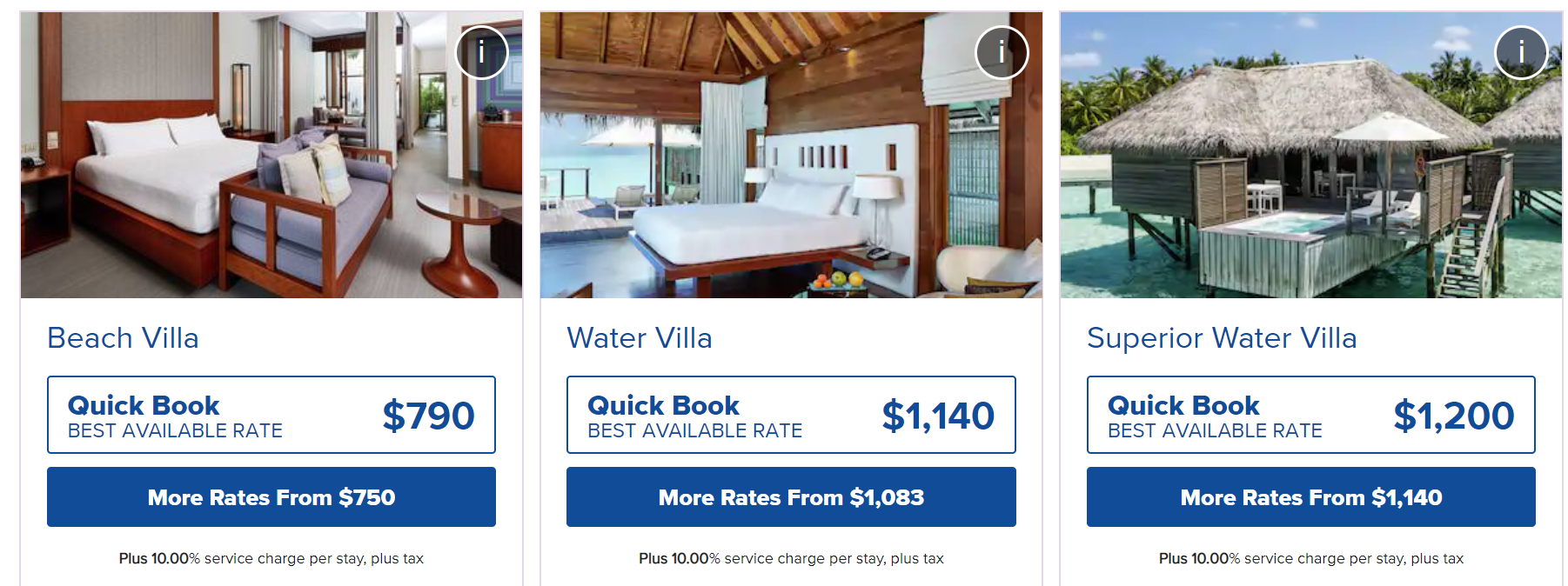

Or consider hotels in the Maldives, where it’s common for the entry-level room to be called a villa. The screenshot below is from the Conrad Maldives, where the cheapest room available is a Beach Villa.

I’m guessing this isn’t what the T&C intends to exclude, but without concrete definitions, I fear people may run into by-the-book CSOs who spy the trigger word “villa” or “suite” and refuse to make the booking.

All 4th Night Free bookings must be prepaid

The current verbiage says that to receive a complimentary night stay, the reservation must be paid in full with a Citi Prestige card. Rates can either be prepaid, or paid at time of checkout.

From 1 March 2020, it gets a lot stricter. Cardholders will need to:

| Fully pay (100% Prepaid) for the entire stay (minimum of 4 nights) with the primary cardholder’s Citi Prestige Card at the time of booking |

My reading of this is that only prepaid rates will be eligible for the 4th Night Free benefit going forward. That’s a significant devaluation if true, because there may be many instances where you’d want to book a refundable rate. Maybe your plans haven’t firmed up yet. Maybe the flexible rate is just a few dollars more than the prepaid rate. Maybe there’s a special package including spa credits or breakfast that’s part of an overall refundable rate. Maybe you’re booking hotels for work travel and need to keep your flexibility. Maybe prepaid rates simply aren’t available at the property you wish to stay at.

| Note: As per a couple of people who have called the Citi Prestige concierge, you can still book refundable rates, but you’ll need to prepay them at the time of booking. I’m not quite sure how that works in practice though- does Citi make arrangements with the hotel to take the payment in advance? What happens if you need to cancel? |

So the loss of the ability to use the 4th Night Free benefit on refundable rates would be a major nerf.

Is Citi preparing to cap the 4th Night Free benefit?

Those are the main changes, but there’s something else in the new T&Cs that has me jittery too.

A new section called C. Amendment and Cancellation has been added, under which you’ll find three particularly concerning bullet points:

|

On first glance, this is confusing. Why does it matter if the reservation is considered part of 2019 or 2020’s benefit usage?

But think about it for a minute, and a disturbing possibility comes to mind. Is this being pre-emptively put in place for a future capping of the benefit? After all, there’s similar wording in the Indonesian version of the Citi Prestige, which as mentioned, caps the 4th Night Free benefit at five uses per calendar year.

|

This same clause also appears in the Thailand version of the Citi Prestige, which will be capping the 4th Night Free benefit to two uses per year from April 2020.

|

It’s just speculation on my part for now, but why else would they put this term in? If the benefit is unlimited, it doesn’t matter which year the usage belongs to.

So the 4th Night Free benefit continues to be unlimited for now, but I’d certainly keep a very close eye on this in the months to come.

Conclusion

I gave up my Citi Prestige card in 2019 in favor of the AMEX Platinum Charge, and I have to say, I haven’t missed it at all. That said, I have friends who swear by the Citi Prestige, because the 4th Night Free benefit is a good fit for their travel patterns. And it’s true, if you do a lot of stays each year, you can easily earn back your annual fee, and then some.

I understand the benefit must be costing Citi quite a bit to provide (keep in mind they’re probably subsidizing this from the commission they earns from hotels, which can be about 15-30%), but if they continue to chip away at it without adding new perks, it’s surely only a matter of time before people start giving other $120K cards a second look.

Time to get rid of this card as well – do you have an updated analysis / view on the best > $120k card in the market today?

will probably do something later this year. i hear there are some product changes afoot for some of the cards

Seriously can’t wait for this one Prestige and SCB VI have been winners for the last two editions Now one is disconned and the other is fast becoming a shadow of its former self Reread the prestige articles and was counting the benefits that got nerfed vs new benefits added: 3-0 And that’s not including the 1for1 dining offers which seem rather blah for the last year or so I really hope the x comes up with some winners but will it be included given its income requirements (It really should since its annual fees are already higher than all… Read more »

Not sure if I interpret ‘prepaid’ as not covering refundable rates. I believe I have prepaid refundable bookings before.

yes, there are refundable rates that require you to put a deposit, but it’s usually not a 100% deposit. if it’s not 100%, those rates wont be allowed under the revised rules either.

AF due in a couple months, am considering not renewing unless they agree to waive

have a decent stash like 500k miles, where will u recommend to transfer other than KF or AM?

most likely i’d want to put them to use in redeeming long haul premium to europe but with no certain itineraries in place it’s difficult to decide which as well as how much to transfer.

BA or TK seems good for sweet spots but what about etihad or qatar?

i fly north asia mostly so EVA will be a good backup if no other options

Do your own research.

yes I have, many people may have thoughts which did not cross my mind

simply starting discussion for more options, others reading can benefit from q&a, after all isn’t this what this is for? To learn and share?

for all the 5sec added up for u to post these kind of replies u may actually have put to use to doing something helpful for someone else other than yourself instead

Sod off mate – this blog is exactly what these kinds of questions are for

Avoid qatar’s FFP like the plague. etihad has a very unique set of partners and is good for things like 7.5/10k y/j trips to USM. if you want to go long haul premium to europe, TK is your best bet (but watch that YQ)

thanks Tom and Aaron having followed milelion I have gathered an acceptable understanding of value (thanks again Aaron!) but given citi’s transfer partners i’m inclined to use them on something KF/AM or the usual star alliance/one world has no/less access to, more towards an experience standpoint rather than maximizing value especially for a family trip hence the question from asking friends and reading trip reports, my take is that TK is good getting u there for lower miles but hard and soft quality of their products cannot exactly be compared with other premium cabins apple to apple the ME3 intrigues… Read more »

I have the same issues as you. I have about 700,000 miles in prestige and would finally not renew this year. I was only using it for Payall.

i wanted to go other alliance but in the end SQ still. Ha ha.

Some time ago (2 years ago and I tried again about a year ago), I tried to claim the 4th night rebate for a half board room booked through the Citi prestige Concierge but I was told that the rebate does not apply to half board bookings.

I recently tried to use the 4th Night free benefit and was told that I could only book using the rates on Expedia (which were considerably more than booking direct once all the direct inclusions were priced in). I asked where this was in the T&Cs and in the end was told they would give me a one time exemption that allows them to book direct with the hotel. This is the first time I came across this, but this time it just felt it was a lot harder to use the benefit, with the CSO seemingly having less power.

Am not sure if limiting the 4NF benefit to 5 times a year is really a deal-breaker. Many readers of this site are hoping to be smarter and savvier travelers, and looking to make the most of their hard earned $ or miles. And that is a good thing.

Availing 4NF 5 times a year easily allows you to get back your annual fee, and some. Unlimited 4NF is asking for a lot, and 2 x 4NF is a dead on arrival.

5x is decent, more than enough for the common traveler unless u’re a biz traveler milking 4nf for all its worth

2x is just sad and putting citi in the leagues of uob

So to me capping at 5x isn’t a deal breaker but the way citi is making it restrictive is

Like the limo changes, as though they’re implying the benefits are there but practically, it isn’t

Agree, I’d rather have a 5x cap than all those restrictions. I’ve used the 4NF benefit over 5 times in 2019 but would be ok if there’s a cap. But these sneaky little restrictions really turn me off, I want to be able to book direct and benefit from my status (e.g. Hilton or Accor Gold). Seems that’s not an option anymore if I am forced to book a prepaid Expedia rate (even if it’s refundable).