Citibank made a big announcement this morning that’s going to really shake up the miles game in Singapore. The bank is launching own payment service called PayAll, allowing customers to pay bills with Citibank cards and earn rewards while doing so.

If this sounds familiar, that’s because it’s what Cardup and iPaymy are already doing. The difference is the fees- Citi is pricing PayAll at a rate that significantly undercuts both of them in certain circumstances.

Who can use Citi PayAll and what does it cover?

For now, Citi PayAll is a targeted service: only people who received an email or SMS are able to register for the service. I imagine that Citi is going to beta test the service with a smaller group of customers before rolling it out to everyone later on. If you received the email/SMS, you have 30 days to set up the service.

PayAll currently supports only rental and education payments, but the publicity materials say they will soon add taxes and condo management fees. One has to imagine that insurance and loan payments can’t be far behind.

There is a cap of $10,000 for all PayAll transactions within a month, or 95% of your credit limit, whichever is lower. You can read the T&C for PayAll here.

Setting up Citi PayAll

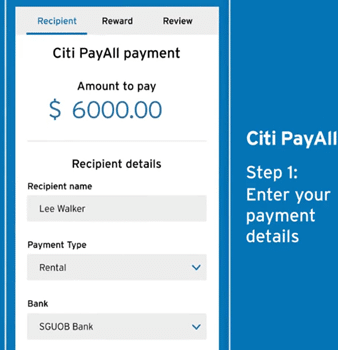

Once you register for PayAll, you’ll be directed to the following screen. First, you enter the recipient’s name, payment type, bank details and payment date…

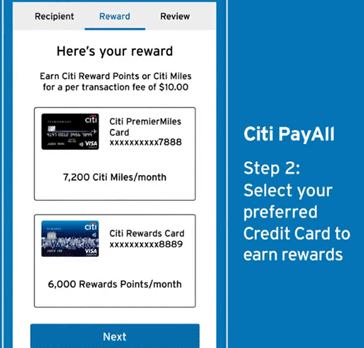

…then you select which credit card you want to charge the transaction to.

Two things to note. First, the transaction fee in the diagram above is incorrect- based on the data points I’ve gathered, a $6,000 payment would attract a fee of $120, not the $10 shown above.

Second, you earn points according to the base earn rate of your card, which means this hypothetical $6,000 payment earns either 7,200 Citi Miles if you charge it to your Citi PremierMiles Visa Card, or 6,000 Thank You Points (2,400 miles) if you charge it to your Citi Rewards Visa Card. No prizes for guessing which one you should pick.

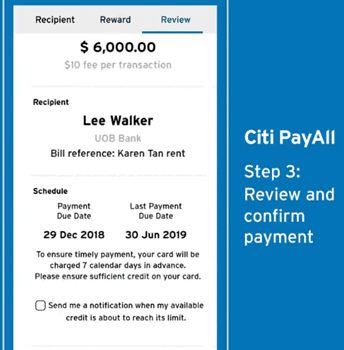

In the final step you review the details and confirm your payment.

Your card will be charged 7 calendar days in advance of payment and your recipient will be paid via bank transfer. There is no need for the counterparty to be registered with PayAll.

Buy miles as low as 0.75 cents per mile, but…

Citibank never explicitly says what the fees are for using PayAll, but based on crowdsourced data the fee structure looks something like this:

| Payment Amount | Fee |

| $2,000 or less | $24 |

| $2,001-5,000 | $60 |

| $5,001-$10,000 | $120 |

Based on the various base earn rates of different Citibank cards, we can derive the following table for a hypothetical $5,000 payment:

| Card | Base Earn Rate | Total Miles | Cost Per Mile with PayAll |

| Citi Rewards Visa or Citi Rewards Mastercard | 0.4 | 2,000 | 3 |

| Citi PremierMiles Visa | 1.2 | 6,000 | 1 |

| Citi PremierMiles AMEX | 1.3 | 6,500 | 0.92 |

| Citi Prestige* | 1.3 | 6,500 | 0.92 |

| Citi Ultima | 1.6 | 8,000 | 0.75 |

*The deal with the Citi Prestige is potentially even better when one considers the end-of-year relationship bonus. Assuming that payments made to PayAll count towards this calculation, you’re potentially paying as low as 0.85 cpm with a 1.42 post-relationship earning rate.

Assuming you spend $5,000 and hold a regular Citi PremierMiles Visa card (income requirement: $30,000 per year), you’re able to buy miles at a mere 1 cent each, which is an excellent price to pay.

But here’s an important caveat: if your payment falls in between one of those ranges, your cents per mile cost goes up. That’s very interesting, because it explains how Citibank is able to offer such a compelling rate for this service.

If you hold a Citibank PremerMiles Visa card, here’s what your math looks like depending on the amount you pay:

| PayAll Amount | Fee | Total Miles | Cost Per Mile (Cents) |

| $1 | $24 | 1 | 2400 |

| $2,000 | $24 | 2400 | 1 |

| $2,001 | $60 | 2401 | 2.5 |

| $5,000 | $60 | 6000 | 1 |

| $5,001 | $120 | 6001 | 2 |

| $10,000 | $120 | 12000 | 1 |

If you hold 2 cents per mile to be your threshold price for buying miles, then the “minimum efficient scale” for a Citibank PremerMiles Visa cardholder to use PayAll is:

- $1,000 for transactions $2,000 or less

- $2,500 for transactions $2,001 to $5,000

- Any amount for transactions $5,001 to $10,000

Anything below this “minimum efficient scale”, and the flat fee penalizes you too much for PayAll to be useful. That explains how Citibank is able to offer this service- not everyone’s rent or education payments will fall nicely into those $2,000, $5,000 or $10,000 fee breaks. In practice, therefore, you’re going to to be paying between 1-2.5 cents per mile.

For the sake of benchmarking, here’s how the other options for buying miles in Singapore currently stack up:

| Method | Income Required | CPM |

|---|---|---|

| DBS Insignia + RentHero | $500K | 1.07 |

| SCB Visa Infinite Tax Payment | $150K | 1.14-1.6 |

| HSBC Visa Infinite Tax Payment | $120K | 1.2-1.5 |

| HSBC Premier MC Tax Payment | AUM: $200K | 1.25 |

| Citi ULTIMA + PayAll | $500K | 1.25 |

| HSBC Visa Infinite Welcome Gift | $120K | 1.39-1.86 |

| SCB Visa Infinite + EasyBill | $150K | 1.43-2.0 |

| DBS Altitude + RentHero | $30K | 1.43 |

| Citi Prestige + PayAll | $120K | 1.54 |

| UOB PRVI Miles + CardUp (GET225) | $30K | 1.57 |

| Citi PremierMiles + PayAll | $30K | 1.67 |

| HSBC Visa Plat/Revolution Tax Payment | $30K | 1.75 |

| DBS Altitude/Citibank PremierMiles + CardUp (GET225) | $30K | 1.83 |

| OCBC VOYAGE Tax Payment | $120K | 1.9 |

| UOB Reserve VI Payment Facility | Invitation | 1.9 |

| OCBC VOYAGE Payment Facility | $120K | 1.9-1.95 |

| Citibank PremierMiles, DBS Altitude, KrisFlyer UOB Card, OCBC 90N Annual Fee | $30K | 1.93 |

| UOB PRVI Pay Facility | $30K | 2.0 |

| UOB VI Metal Payment Facility | $150K | 2.0 |

| OCBC VOYAGE Annual Fee- Option 2 | $120K | 2.14 |

| Citi Prestige Annual Fee | $120K | 2.14 |

| DBS Altitude Tax Payment | $30K | 2.5 |

| OCBC VOYAGE Annual Fee- Option 1 | $120K | 3.25 |

What about Cardup/iPaymy?

I imagine the two companies which are going to lose the most sleep about PayAll will be Cardup and iPaymy, given this represents an encroachment on their turf. Cardup and iPaymy charge 2.6% and 2.25% respectively on Visa/Mastercard payments (over the past few months I’ve been getting promo codes offering iPaymy payments for 1.99% fees).

Assuming you used a UOB PRVI Miles card for 1.4 mpd, your equation would be:

| Provider | Fee | Cents Per Mile |

| Cardup | 2.6% | 1.81 |

| iPaymy | 2.25% | 1.57 |

| iPaymy | 1.99% | 1.39 |

You can see how PayAll can potentially be much cheaper than either Cardup or iPaymy*, depending on the amount you pay.

*Want to complicate it even further? Some people in the Telegram Group report they’ve received 10X with the Citi Rewards Visa card and iPaymy. Assuming that’s true, then your cost per mile goes down even further to 0.49 with a 1.99% promo code (although one does wonder if Citibank will continue to allow that given the launch of PayAll).

There’s an important nuance to this, however: will your rental or education payments fall nicely into those $2,000, $5,000 and $10,000 bands? If it doesn’t, then Cardup/iPaymy could still make sense for you depending on your exact amount. The smart miles chaser would probably tell his or her landlord to expect two different payments- one from Citi Payall of $2,000, and the rest via regular bank transfer or Cardup/iPaymy.

Conclusion

PayAll is still very much a beta service from Citibank’s point of view, and I won’t be surprised if over the next few months we see a tweaking of

- the fee structure

- the monthly maximum PayAll transaction amount

based on take up rates and usage patterns. The T&C make it abundantly clear that fees may be amended from time to time, and the bank reserves the right to offer promotional fees to selected cardmembers at their discretion.

My guess is the current structure was predicated on the fact that most people would prefer the convenience of making one payment, instead of splitting their payment in a way that yields the lowest cent per mile scenario. If it turns out us miles fanatics are greater in number than Citi thought, then I’m pretty sure there’ll be an adjustment to make the program economically viable for Citi.

Of all the banks in Singapore, it really seems like Citi has done the most to shake up the miles game (recent greatest hits: the opportunity to buy miles at 0.76 cents each, or earn 8 mpd without cap on Apple Pay).

Received and signing up. My targeted offer is rather opt-in for recurring payment (with a checkbox – “Make this payment recurring”)

interesting…the FAQs say it’s monthly recurring only. maybe they’re doing a/b testing

Hi Aaron.. From reach outs to both Citiphone as well as RM, apparently he ‘fees’ are not as straight forward as it seems, per your tables.. From what we’ve been told, ‘the fee’ depends on a few factors.. including relationship with bank, and even who payee is.. the only way to know what the fee will be, according to bank, is to fill up the spaces and see what figure comes out.. quite strange indeed..!

I think that’s the party line- but for now everyone who I’ve asked sees the same offer. They will probably fine tune this further and then yes we will probably see more variance

I think it directly competes with UOB PRIV Pay. Citi need to be bold to allow to credit to one’s own account like UOB.

Anyway, it does not ask for proof of payment. However, the TnCs don’t allow payment to oneself and illegitimate payment.

(unless expressly allowed by us);

This statement in the TnC is interesting.

It’s a better way to run credit card balance transfer than traditional way. The cost to Citi is lower than offer 6-month 2% fee.

Think about it. Citi charges more than 1.2% fee for less than 2 month balance transfer.

The miles awarded is additional cost, but that’s probably from other sources.

Citi premier miles Amex pays 1.3 miles per dollar bringing down the MPD to below 1 🙂

I was wandering since it was Citi provding this service through its own credit card, maybe the transaction will not through Visa/MasterCard/AMEX,

If this is the case, Citi will not earn the portion as an issuer of intercharge fee for normal credit card transaction fee. Instead, Citi will got the ‘admin’ fee charged to us.

Anyway, it’s good for us as consumer…

What’s stopping me to pay “rent” to myself?

I tried to key in my own bank account. It seems to be ok. But I didnt click through. They didnt ask for documentation like Cardup. Or maybe they’ll ask for it later via other means (eg separate email?).

I was thinking the same thing. How does Citi know the receiving party is your education provider (eg private tutor)

Will we get miles for the admin fee charged to a Citi card? We do get the miles for the full payment of rent+Admin fee on Cardup

I got the email yesterday, tried to sign up, complete all the steps and then I get an error message saying We apologize, It seems that something went wrong, we are having some trouble processing your request. Called Citibank and they said they would look into this. Anyone else having this problem?

I had this problem too

I have this problem too and the CSOs have yet to give me an answer. It’s been 2 days already

Called Citibank for the same problem,they confirmed that payall has stopped working as Citibank is going to release this within the Citibank app

Can someone confirm if they would ask for verification documents?

They haven’t asked me

my rental is only 4000/month..and still have to pay 60 flat fees for that..not great…

Why not just split it into 2x $2000 payments for $48 in fees instead?

Thanks Aaron for sharing, otherwise I would never have realised the PayAll email from citi. I just set up my monthly rent payment using Citi PremierMiles Visa and it works out to a 1.3 cent per mile, not bad I must say.

Nicely done! You *can* get lower prices than that, but 1.3 is still an excellent cost per mile

PremrMiles Visa latest service fee for PayAll is 1.5%.

$1=1.2miles (advertised)

$1.015 = 1.2miles (+fee)