One common objection I hear to playing the miles game goes something like this:

Applying for multiple credit cards will hurt my credit score, which will impact my ability to apply for a housing, renovation or car loan

That’s certainly a legitimate concern. Your credit score affects the willingness of banks to lend money, and if you sign up for a whole bunch of cards while not paying your bills on time, you’re going to be in a world of hurt.

But is playing the miles game incompatible with a good credit score, and does holding a higher-than-average number of cards necessarily tarnish your record?

My experience says no.

What is a credit score?

Consumer credit scores in Singapore are issued by two companies:

While every major lender in Singapore is part of CBS, Experian only has three members (BOC, Diners Club and UOB, all of whom are also part of CBS). This makes its reports less useful for consumers, and I’d recommend ignoring them altogether and relying solely on CBS.

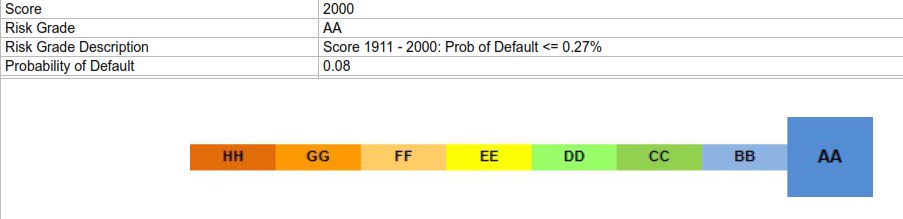

CBS assigns individuals a four-digit credit score which indicates how likely they are to default. Scores range between 1000 and 2000; the higher the score, the lower your odds of defaulting.

| Probability of Default | ||

| Score | Min | Max |

| 1911-2000 (AA) | 0.00% | 0.27% |

| 1844-1910 (BB) | 0.27% | 0.67% |

| 1825-1843 (CC) | 0.67% | 0.88% |

| 1813-1824 (DD) | 0.88% | 1.03% |

| 1782-1812 (EE) | 1.03% | 1.58% |

| 1755-1781 (FF) | 1.58% | 2.28% |

| 1724-1754 (GG) | 2.28% | 3.46% |

| 1000-1723 (HH) | 3.46% | 100% |

Each score is assigned a two-letter band ranging from AA to HH. An AA individual has less than a 0.27% chance of defaulting; a HH individual more than 3.46%.

| ❓ How do I get a credit report? |

|

There are three ways you can obtain a credit report from CBS.

|

According to CBS, your credit score is affected by the following factors:

(1) Utilisation Pattern

This refers to the amount of credit an individual owns and utilises, e.g. carrying a balance on a credit card or having an outstanding housing loan.

(2) Recent Credit

This refers to the number of new credit facilities acquired in the recent past.

(3) Account Delinquency Data

This refers to whether you currently have any delinquent (i.e. late) payments on your credit facilities.

(4) Credit Account History

This refers to the length of your credit history, as well as your track record of making prompt payments. The past 12 months of account repayment conduct is used for score calculation.

(5) Available Credit

This refers to the total number of active credit accounts you have.

(6) Enquiry Activity

This refers to the enquiries that banks or financial institutions make every time you apply for a new credit product, and is therefore linked to (2). Too many enquiries may harm an individual’s score, to the extent they suggest that he/she is trying to take on more debt.

Banks or financial institutions will also periodically review your credit score as part of their ongoing checks. Such routine reviews have no impact on your credit score.

What happens when you play the miles game?

CBS does not disclose the exact weightage of each component, but it’s quite clear that (2) Recent Credit and (6) Enquiry Activity will take a hit if you apply for multiple cards in a short period of time.

However, if you build up a track record of paying off your bill in full and on time, your scores for (3) Account Delinquency Data and (4) Credit Account History will improve.

It’s also important to remember that while credit scores are important, they are just one factor used in the application process. Credit providers will also look at other factors such as:

- Annual salary

- Length of employment

- Bankruptcy/litigation information

My experience with credit scores

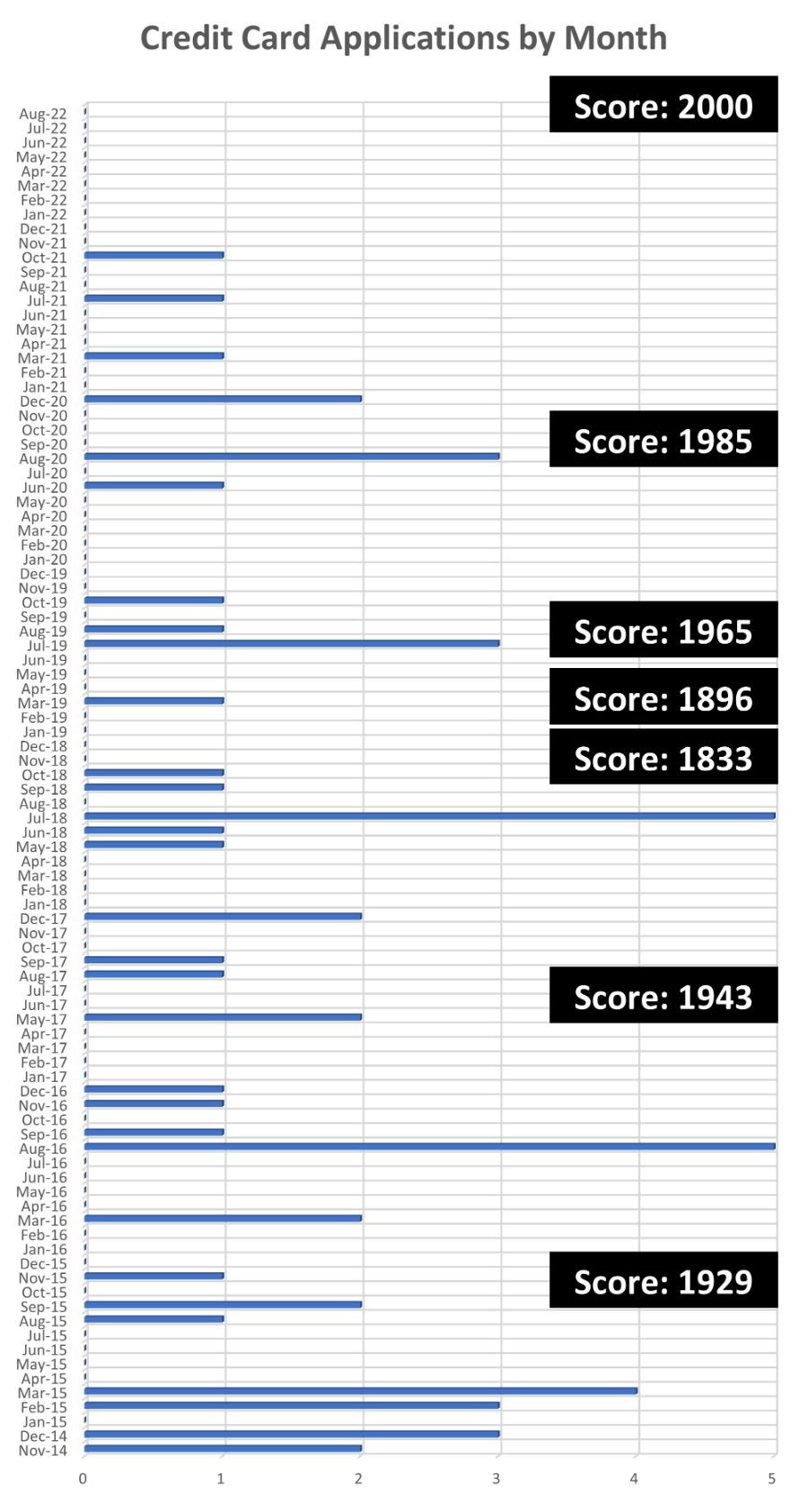

Here’s how my credit score has evolved ever since I started playing the miles game in November 2014.

| Report Date | Credit Score |

| Nov 2015 | 1929 (AA) |

| Jul 2017 | 1943 (AA) |

| Oct 2018 | 1833 (CC) |

| Feb 2019 | 1896 (BB) |

| Aug 2019 | 1965 (AA) |

| Aug 2020 | 1985 (AA) |

| Aug 2022 | 2000 (AA) |

To provide more context to the figures, what I’ve done is plot the number of credit card applications by month against my credit score, from the day I got my first miles card till today.

The objective of this chart is to show two things:

- Whether recent card applications cause your credit score to deteriorate in the short-term

- Whether on-time payments cause your credit score to improve in the long run, regardless of the total number of cards you hold

I think the data bears out both.

Assuming CBS uses a six-month period when they refer to (2) Recent Credit and (6) Enquiry Activity, we can observe the following:

- November 2015: 1929 (AA) with four recent applications

- July 2017: 1943 (AA) with two recent application

- October 2018: 1833 (CC) with nine recent applications

- February 2019: 1896 (BB) with two recent applications

- August 2019: 1965 (AA) with five recent applications

- August 2020: 1985 (AA) with four recent applications

- August 2022: 2000 (AA) with no recent applications

Notice how my score initially held steady at AA, until it deteriorated to 1833 (CC) in October 2018 with nine recent applications.

I took my foot off the pedal a bit, and by February 2019 it improved to 1896 (BB) with two recent applications, and in August 2019, 1965 (AA) with five recent applications. Keep in mind, between February and August 2019 I also took out a substantial housing loan.

In August 2020, I had 1985 (AA) with four recent applications, and in August 2022, 2000 (AA) with no recent applications.

Therefore, the data does seem to suggest that a flurry of recent applications can cause your short term credit score to deteriorate (more than five could be the magic number, but that’s speculation on my part)

However, zooming the camera out and looking at the bigger picture would suggest that holding multiple cards does not damage your credit score, in and of itself. Case in point: I currently hold a score of 2000 (AA) with 24 active credit cards and an outstanding housing loan.

| 😱 24 credit cards?! |

|

While I have 24 credit cards on paper, I don’t use all of them. Some were obtained for sign-up gifts or bonuses and then promptly sock drawered, others fell out of favour because of changes in the T&Cs or CVP (farewell, UOB Preferred Platinum AMEX). I’d say my regular rotation features perhaps 6-7 cards at most. |

I’ve always paid my card bills and housing loan instalments in full and on time via GIRO. I never roll over my card balance, and while I have missed the odd payment here and there due to GIRO snafus, I’ve always resolved the matter within a few days, with the late fees and interest waived.

So even though I took a short-term hit to my score in October 2018, it quickly recovered in the following months because of prompt payments. This leads me to conclude that in the long run (2) Recent Credit and (6) Enquiry Activity are not as important as (3) Account Delinquency Data and (4) Credit Account History in determining one’s score.

That belief is corroborated by friends who work in the industry, who tell me that defaults and late payments are bigger black marks than new credit lines per se, and that’s what you really need to watch out for.

So in short, my advice would be this: if you’re planning to apply for a loan in the near future, now might not be the best time to go on a credit card sign-up binge. A couple of cards should be OK, but nothing more than that- and space out your applications where possible.

Once your loan is approved, you can proceed to apply for the rest of the cards you want. Pay everything on time, and your score will naturally improve.

Playing the miles game responsibly

At the risk of sounding like a broken record, I’ll say that if you have impulse control issues or lack the discipline to organise your financial affairs, then the miles game isn’t right for you.

But playing the miles game is not mutually exclusive with the responsible use of credit. Here’s three pointers I’d offer to anyone getting started.

Build credit history with credit cards

I know a couple of people who have philosophical objections to credit cards, because their friends or family members have wound up in bad places after misusing them.

That’s unfortunate to be sure, but the solution isn’t to avoid cards altogether. If you avoid taking on any kind of credit, your score won’t be AA, it’ll more likely be CX. CX means that CBS has insufficient information to assign a score, and banks may not be willing to extend loans because they have no idea as to whether you’re a responsible credit user.

Even if you don’t see yourself getting into the miles game, it still makes sense to get one or two cards and pay them off on time to build up your credit score.

Set up GIRO for all your cards

The first thing you should do upon getting a new card is to sign up for GIRO. This ensures you’ll never miss a payment- unless of course you’re spending more than you have in your bank account, in which case you shouldn’t be getting a card in the first place.

I’ve heard the most absurd excuses for not setting up GIRO. “Oh, it takes too much time” / “Oh, I want to keep track on how much I’m spending” / “Oh, the pain of paying the bill manually each month will remind me not to overspend”.

Please. Now that we have eGIRO, the hassle of setting up an arrangement has been minimised. Moreover, using GIRO doesn’t stop you from reviewing your consolidated bills each month to know how much you’re spending. That should be a standard practice, regardless of your payment method.

Missed payments are very, very bad for your score, and very, very avoidable. A responsible miles chaser will always have GIRO arrangements in place.

Treat credit cards as debit cards with rewards

Oxymoron though it may be, you should never view credit cards as sources of credit. If you’re short on funds, there are much cheaper options to borrow money.

Instead, view credit cards as debit cards with rewards, in the sense that you never spend more than you have. See it as earning rebates on spending that you’d need to make anyway; earning miles should never be a justification for spending more than you otherwise should.

Remember: the miles game is a way of not leaving money on the table, not putting extra money down!

Conclusion

Playing the miles game may involve holding more credit cards than the average person, but it need not be harmful to your credit score provided you use them responsibly. This means paying off your bill in full and on time, never carrying a balance, and living within your means.

Just remember: credit cards can be your best friend if you use them well, or your worst nightmare if not.

How has your credit score changed since you started playing the miles game?

Dunno whats their criteria for approving tho..

u seem to have 100% approval even with CC..

im AA with 0%

I’m curious, out of the 24 credit cards, how many annual fees do you pay?

Only one: amex platinum charge. For the rest: no waiver, cancel

Citi Prestige?

Don’t most of the credit cards offering miles as sign up bonus require you to pay the full annual fees?

sure. but i signed up a long time back.

Great article! Yes be careful. I applied for 4-5 cards within 2 months and my score plunged from AA to HH without any missed payments, housing loans etc.

CBS is such a scam. Every time I apply for a card I try to check afterwards and the free report never works. Now I did the HSBC signup and yet again no redirect or free report. What a shambolic company.

I have exactly the same issue. Never got a proper report from them.

Not sure if it’s related to being here on EP.

That might be it – thanks! I ended up getting a proper score, in which I was AA, but I still kept getting randomly declined. After many many months of calls I found 2 main reasons: 1) hyphenated name; 2) expiry of Passport / EP within 1 year / 6months. Still better than trying for Japanese cards 20+ years back. Generally always declined because you don’t have a credit history locally in Japan – how do you get one? Well easy: get a credit card! … There was one work-around: get one of those terrible department store cards and hold… Read more »

as someone with a hyphenated name, i fully empathise. so many messed up FFP transfers…

It is indeed quite poorly run. There was a motor accident claim against me for a 2014 minor fender bender (4-digit quantum) for which the other party only filed suit in 2017. Motor insurer settled the matter promptly and yet CBS kept listing me as a HX rating, saying there were pending court cases against me. I duly waited the 3 years until 2020, since CBS claimed HX ratings remain in place for 3 years after a case is closed. 2020 came and went – still listed as pending court case against me. I ran my own eLitigation and QuestNet… Read more »

Wow that’s terrible to hear Spoon. Glad it finally got fixed, but the power and lack of oversight that these orgs enjoy is just staggering. Sadly this seems to be par for the course with these type of orgs worldwide, whether in the US, or the Schufa in Germany. They all have horror stories of mistaken identities, etc pp, but they live of a comfortable monopoly/duopoly and don’t really do any work.

Does eGIRO even work? I had the pain of going through paper GIRO forms – 2 months on and not all my GIRO applications have been processed..

think it’s coming to credit cards soon.

The 13 pilot billing organisations span across five different business segments including public services, insurance, wealth management, and payment services.

They comprise the CPF Board, HDB, GrabPay, Singtel Dash, FWD Insurance, Etiqa Insurance, Singlife, iFast Corporation, YouTrip, Singapore E-Business, Bank of China credit cards, ICBC credit cards, and Diner’s Club.

https://abs.org.sg/docs/library/egiro-participating-billing-organisations-as-on-31-july-2022.pdf

Surprisingly, the credit cards can be paid are from BOC and ICBC only !

Not sure why the other banks are all not onboarded ZZZ.

this can’t get rolled out fast enough.

Is your credit score also a function of your credit limit for each card? E.g. For cards which don’t offer bonus points beyond the first $1k or spending, I’ll opt for a much lower credit limit on these cards.

I’m newbie to the miles game. Just for my guide, how many miles is required for a Tokyo ticket? How much to spend roughly to earn this required miles? Can miles earned from different cards be combined into one? Thanks

Hey buddy, the short answer to all (yes, all) your queries is – it depends. It absolutely depends. Your queries are too broad. Since you’re already on the right site, I recommend you take the time to read the articles within.

Hello there, are you looking for me?

I happened to just make a video on how to retrieve your free Credit Report on CBS 😄

Here’s the link:

https://youtu.be/x6XbN65r3Jg

I hope it’s useful!

For Amex is there a way to giro pay as well?

Does cancelling credit cards affect (improve or lower) our credit score in any way? I heard cancelling cards can improve credit score bcos it reduces our credit limit. But I also heard that it can have the opposite effect & degrade credit score instead, bcos cancelling cards is deemed as inability to handle such given credit limit. Not sure which one is true.

Does getting secured cards lower credit rating?