If you use AXS to make bill payments, you may have noticed the Pay+Earn and Pay Any Bills banners on the m-Station app.

These are basically a clone of CardUp/Citi PayAll, allowing cardholders to pay bills with their credit cards and earn rewards, in exchange for a fee.

| Pay+Earn | Pay Any Bills | |

| Launched | March 2020 | June 2021 |

| Availability | m-Station | m-Station |

| Coverage |

|

|

| Admin Fee | 2.5% | 2.6% |

| Processed By | Unclear | SGeBIZ |

| Payment Methods | Visa & MC | Visa & MC |

That’s the theory, at least.

Having received a few complaints from readers that these services don’t actually do what they say on the tin, I decided to dig deeper into the matter.

What’s the official position on rewards?

At the risk of stating the obvious, the whole purpose of Pay+Earn or Pay Any Bills is to earn rewards. I mean, if you can’t, then what’s the admin fee for?

So it felt a bit silly to be asking “hey, I know your website says that AXS Pay+Earn/Pay Any Bills transactions earn rewards, but do they really earn rewards?”

But I suppose that’s my job.

AXS

AXS is pretty emphatic that transactions made through its Pay+Earn and Pay Any Bills service will earn credit card rewards.

From its Pay Any Bills landing page:

|

Pay Any Bills is a newly launched service on AXS m-Station (mobile app) that allows you to make payments to any corporate organization for goods and services using the company’s UEN (Unique Entity Number) or rental payments using UEN or NRIC No/FIN. When you make a payment with your preferred credit card, you will earn rewards such as credit card points, miles, or cash back with every successful payment transaction. |

| Maximise your credit card rewards – Pay Any Bills benefits users who value rewards gain from credit card transactions. With Pay Any Bills, you will earn credit card rewards by using your preferred card for payments on AXS mobile app. |

This message is also reinforced in its various marketing collaterals:

Just to be thorough, I reached out to AXS to ask whether I’d earn credit card rewards for these payments.

I did this twice. The first CSO who followed up said that all credit cards except Citibank, CIMB, and UOB One would earn rewards with Pay Any Bills.

The second CSO told me that “it depends on the bank’s T&Cs”. However, she also provided a valuable data point:

- AXS Pay+Earn codes as MCC 7399 Business Services Not Elsewhere Classified

- AXS Pay Any Bills codes as MCC 6513 Real Estate Agents and Managers- Rentals

These MCCs apply regardless of what sort of payment is made.

MCC 7399 is generally kosher, but MCC 6513 should send up a big red flag, since it’s a common rewards exclusion.

| Bank | MCC 7399 | MCC 6513 |

| ✓ | ✕ |

|

| ✓ | ✕ | |

| ✓ | ✓ | |

| ✓ | ✕ | |

| ✓ | ✓ |

|

| ✓ | ✕ |

|

| ✓ | ✕ |

|

|

✓ | ✕ |

But could it be that AXS has negotiated some kind of behind-the-scenes deal with banks to ensure that Pay Any Bill transactions do indeed earn points, MCC notwithstanding? After all, they wouldn’t be promoting the rewards aspect so heavily if the vast majority of card issuers excluded rewards, right?

Hold that thought.

SGeBiz

![]()

I also reached out to SGeBIZ, who process payments for the Pay Any Bills service.

|

Please take note that the eligibility to earn rewards and/or if there were any exclusions are purely at the discretion of the Credit Card Issuing Bank. All pricings are quoted with full transparency on AXS Pay Any Bills service. For any further clarification on pricing and/or product, kindly reach out directly to AXS. |

Their response basically punted the question over to the bank- rather unhelpful, since you’d think it’d be in their interest to provide something more concrete.

Field testing

Since MCC 7399 is generally not excluded while MCC 6513 is, I decided it was less important to test AXS Pay+Earn and more important to test AXS Pay Any Bills.

So I made a S$300 rent payment transaction via AXS Pay Any Bills with each of the following cards, paying a total of S$305.10 under the current promotional 1.7% admin fee.

- DBS Altitude Visa

- HSBC TravelOne Card

- OCBC 90°N Card

- StanChart Journey Card (formerly known as the StanChart X Card)

In addition to this, I received a few data points from readers who had used Pay Any Bills with the UOB PRVI Miles Card and UOB Visa Infinite Metal Card.

| ❓ What about Citi? |

| I tried to test this with my Citi PremierMiles Card too, but got an error message saying “your payment card is not accepted”. This ties back to what the first AXS CSO said about Citi, CIMB and UOB One Cards not being accepted. |

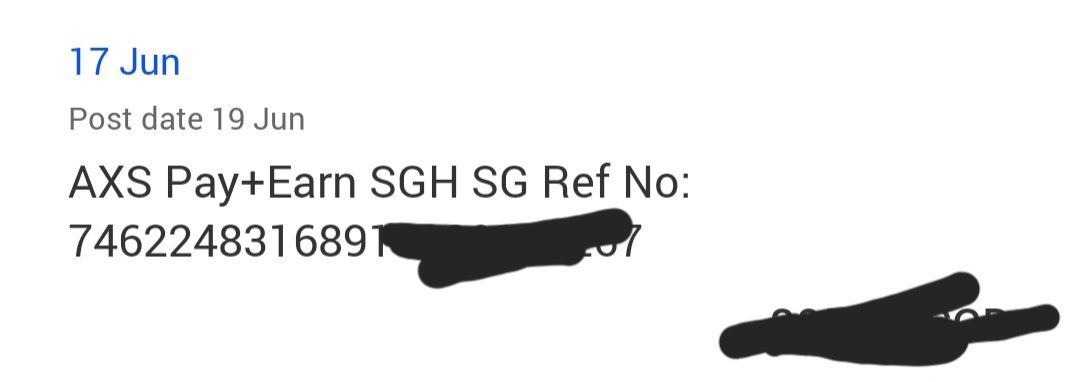

Interestingly enough, Pay Any Bill transactions code as AXS Pay+Earn, which may cause some confusion when going through your statement.

However, the MCC was exactly what the CSO said it would be: MCC 6513.

As for points, the record was hit and miss- with some surprising results.

| Bank | “Should it” earn points?* | Did it earn points? |

| DBS | Yes | Yes |

| HSBC | No | Yes |

| OCBC | No | No |

| Standard Chartered | No | No |

| UOB | No | No |

| *Based on MCC 6513 | ||

DBS

DBS explicitly carves out an exception for Pay+Earn transactions in its T&Cs, and does not exclude MCC 6513.

2.6 DBS Points will not be awarded for:

|

I therefore expected to earn rewards with my DBS Altitude Visa, and indeed I did, at an effective rate of 1.2 mpd.

HSBC

The HSBC TravelOne Card’s T&Cs explicitly exclude MCC 6513, with no exception carved out for AXS Pay+Earn/Pay Any Bills.

So I was surprised that my Pay Any Bills transaction did earn points on the HSBC TravelOne Card, at an effective rate of 1.2 mpd.

OCBC

While the OCBC 90°N Card’s T&Cs exclude MCC 6513, they carve out an exception for AXS Pay+Earn transactions, awarding a reduced rate of 1 mpd instead of the usual 1.2 mpd.

|

1.1 As a reward for incurring spend on their OCBC 90°N Mastercard / Visa Card, all

|

However, I received no points at all for my Pay Any Bills transaction.

Standard Chartered

Standard Chartered’s T&Cs explicitly exclude MCC 6513, and do not have any exceptions carved out for AXS Pay+Earn/Pay Any Bills.

My Pay Any Bills transaction did not earn any points.

![]()

UOB

UOB’s T&Cs explicitly exclude MCC 6513, and do not have any exceptions carved out for AXS Pay+Earn/Pay Any Bills.

I didn’t personally test this, but I’ve received data points from a few readers that their UOB card transactions did not earn any points with AXS Pay Any Bills.

If it’s any consolation, one reader told me they complained to AXS, and while they didn’t get a refund of the admin fee, they got…wait for it…a KFC voucher for free chicken wings.

So…no go?

So here’s a summary of the findings once more:

| Bank | Points for AXS Pay Any Bills? |

| Citibank | Not accepted |

| DBS | Yes |

| HSBC | Yes |

| OCBC | No |

| StanChart | No |

| UOB | No |

Out of the six cards tested, AXS Pay Any Bills did not earn rewards for three, and wasn’t compatible with a fourth.

So my question is this: why does the marketing for AXS Pay Any Bills make it seem like credit card rewards should be expected, when it’s really the exception rather than the norm?

Throughout the AXS website and app, Pay Any Bills is marketed as a way of earning credit card rewards, without any sort of disclaimers or exceptions. Why not take a leaf out of CardUp’s book, and publish a list of cards which do and don’t earn rewards?

After all, they’re already fighting a losing battle where fees are concerned (current promotion for rental aside). Wouldn’t it make sense for them to do the testing, and provide cardholders with reassurance as to which cards do and don’t work?

Conclusion

AXS Pay Any Bills is hit and miss when it comes to rewards. While I did earn points with DBS and HSBC credit cards, there was no joy with OCBC, StanChart and UOB. Citi cards aren’t accepted, and I don’t see much of a point in testing BOC or Maybank, given their limited footprint.

Once you factor in the expensive admin fee (outside of the 1.7% rental promotion), there’s just very little reason to use this service.

Any other data points for Pay + Earn/Pay Any Bills?

hihi, woww then does it mean can use DBS Altitude Visa on all bill payments via AXS to get the 1.2miles/dollar?

Thanks a lot for sharing this trial!

an update, see t&c page 4 table 2

https://www.dbs.com.sg/iwov-resources/pdf/cards/rewards_programme_tnc.pdf

DBS recently excluded AXS * payment, effectively exclude all AXS Pay + Earn transaction from points. However, this contradicts with 2.6(e) in the t&c, which explicitly mention Pay + Earn do earn points.

Tested last week, AXS Pay + Earn does not earn any DBS points.