UOB cardholders typically pay a S$27 fee (recently increased from S$25) each time they convert UNI$ to airline miles, unless they happen to hold a UOB Reserve Card, UOB Visa Infinite Card, UOB Visa Infinite Metal Card, or UOB Privilege Banking Card.

However, there is an alternative option for those who wish to convert their points more frequently, or want to break up the minimum conversion block: the KrisFlyer Auto Conversion Programme.

In this post, we’ll look at how this programme works, and who stands to benefit the most from it.

Overview: UOB KrisFlyer Miles Auto Conversion Programme

|

| FAQs |

| T&Cs |

| Read Point 51-54 |

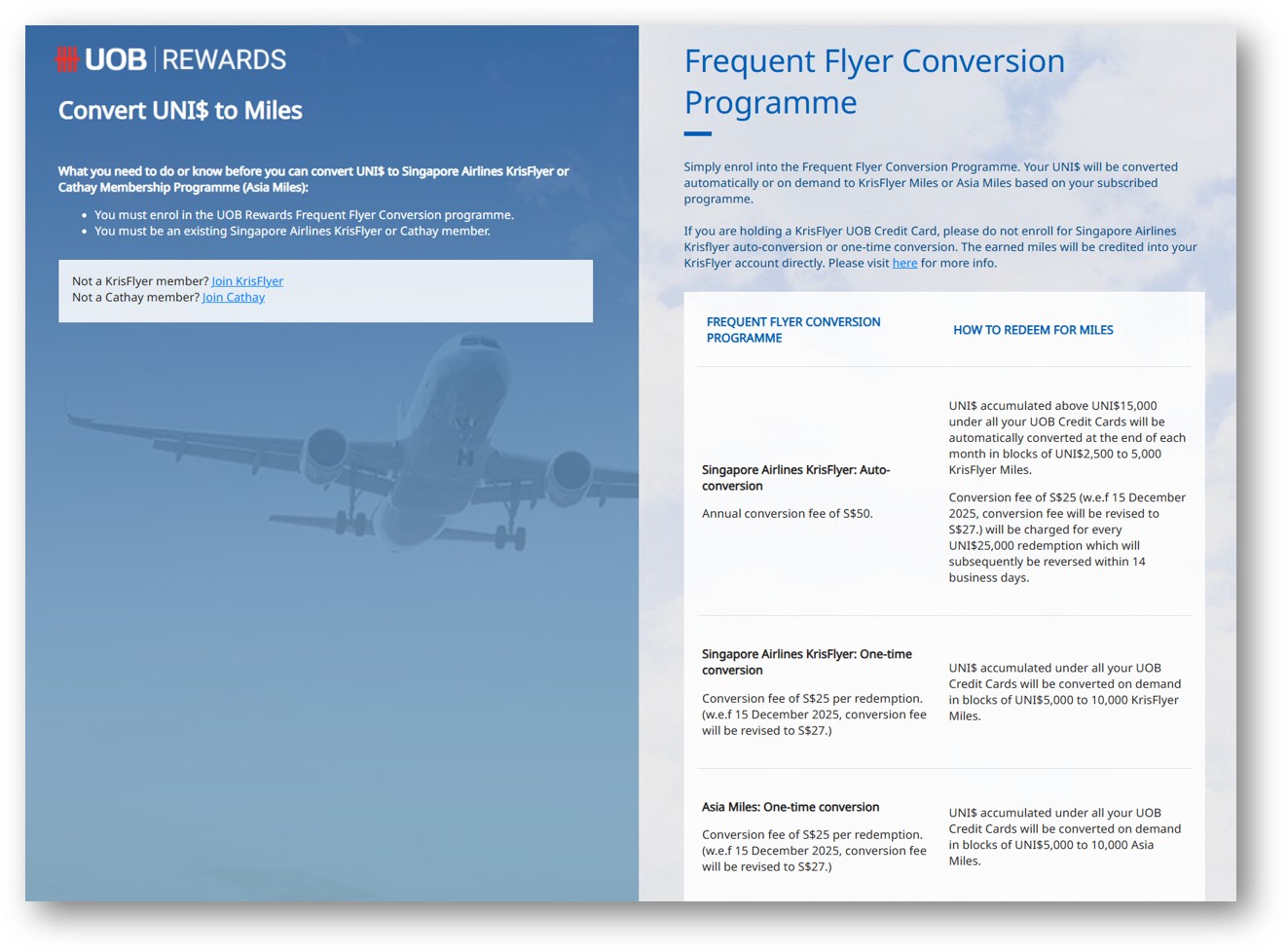

The UOB KrisFlyer Auto Conversion Programme is available to any principal UOB credit cardholder (though it only makes sense if you have a UNI$-earning card, obviously).

Since UNI$ are pooled, it’s only necessary to enrol a single card. That card can subsequently be used as the conduit to convert points earned on other cards too.

| ✈️ KrisFlyer miles only |

| As the name suggests, this programme is only available for conversions of UNI$ to KrisFlyer miles. No such equivalent exists for any of UOB’s other transfer partners (Air Asia, Asia Miles). |

The programme fee is S$50 per year, inclusive of GST.

Interested cardmembers can enrol via this online form. Approval must be granted by the 20th calendar day in a calendar month for the auto-conversion to be effected within that same calendar month.

How does it work?

Upon successful enrolment, an automatic conversion will be effected on the last calendar day of each month. Should this fall on a Saturday, Sunday or Public Holiday, the auto conversion will take place the next working day.

All UNI$ above 15,000 UNI$ will be converted in blocks of 2,500 UNI$ (5,000 KrisFlyer miles). A temporary S$27 conversion fee will appear in your card account, which will be automatically reversed within 14 working days.

Yes, you read that right: UNI$ above 15,000 UNI$. UOB requires you to maintain a minimum “working capital” of 15,000 UNI$ in your account, for which it gives the following explanation:

|

Why must a minimum balance of UNI$15,000 be kept KrisFlyer auto conversion programme? This is to give card members the flexibility to convert the UNI$ to other items from UOB Rewards Catalogue. Card members can still choose to convert this UNI$15,000 to KrisFlyer miles by the one time miles redemption process through UOB Rewards Catalogue, subjected to S$27 conversion fee and must be in blocks of 10,000 miles. |

Here’s an example of a cardholder with a UOB Preferred Platinum Visa (registered in the auto-conversion programme) and a UOB Lady’s Card, with a total of 27,000 UNI$.

| Card | UNI$ |

UOB Preferred Platinum Visa UOB Preferred Platinum VisaAuto-Conversion |

14,000 |

UOB Lady’s Card UOB Lady’s Card |

13,000 |

| Total | 27,000 |

| Converted | (10,000) |

| Remainder | 17,000 |

During the auto-conversion, 10,000 UNI$ will be converted to 20,000 KrisFlyer miles, with 17,000 UNI$ left in the cardmember’s account.

Why not 25,000 UNI$, if the conversion blocks are 2,500 UNI$? Remember, only UNI$ above 15,000 are considered for conversion, so the actual amount eligible to be converted here is 12,000 UNI$!

For what it’s worth, UOB will convert the earliest expiring points first, which means that your 15,000 UNI$ “working capital” balance will always consist of the UNI$ with the latest expiry.

All conversions will be processed within the usual timeframe, i.e. 1-3 working days.

Can I still make ad-hoc conversions?

Yes, but it won’t be free.

Cardmembers who wish to make ad-hoc conversions can still do so, subject to the payment of the usual S$27 fee per conversion, in standard blocks of 5,000 UNI$ (10,000 miles).

Is it worth enrolling?

First of all, there’s little point in enrolling in the UOB KrisFlyer Auto Conversion Programme if you have a UOB Reserve Card, UOB Visa Infinite Card, UOB Visa Infinite Metal Card, or UOB Privilege Banking Card.

Since these cardholders already enjoy free-of-charge conversions, the only thing you stand to gain is a smaller conversion block of 2,500 UNI$- but keep in mind you still have that pesky 15,000 UNI$ balance to maintain!

Even if you don’t hold any of those cards, however, it’s safe to say the cons of automatic conversions outweigh the pros.

Pros

- Pay a single fee for 12 automatic conversions a year

- Reduces the minimum conversion block from 5,000 UNI$ (10,000 KrisFlyer miles) to 2,500 UNI$ (5,000 KrisFlyer miles)

Cons

- The 3-year KrisFlyer mile expiry starts as soon as they are converted. Had you kept your UNI$ on the UOB side, you’d enjoy two extra years of validity

- Ad-hoc conversions still cost you S$27

- Only balances in excess of 15,000 UNI$ are converted

- Effectively locks you into KrisFlyer, as opposed to UOB’s other transfer partners (you can still make ad-hoc conversions to Asia Miles between quarters, but it’s likely you’ll need to end participation in the Automatic Conversion Programme to acquire a critical mass)

Given these drawbacks, it’s just very hard to make a case for the UOB KrisFlyer Auto Conversion Programme.

What if I want to withdraw?

To withdraw from the KrisFlyer Auto Conversion Programme, you will need to call UOB at 1800 222 2121.

Do note that there will be no whole or partial refund of the S$50 enrolment fee. Following a successful withdrawal, you’ll be charged the usual S$27 fee per conversion.

How does this compare to the DBS automatic conversion programme?

UOB isn’t the only bank with an automatic conversion scheme; DBS has its own scheme too.

Here’s how the two programmes measure up:

| DBS | UOB | |

| Annual Fee | S$43.60 | S$50 |

| Availability | Selected cards | All UOB cards |

| Auto Conversion Frequency | Quarterly | Monthly |

| Auto Conversion Block | 1,000 miles | 5,000 miles |

| Ad-hoc Conversions | Free | S$27 |

| Min. Balance on Bank Side | None | 15,000 UNI$ (30,000 miles) |

My take is that DBS’s scheme is much superior. Even though it only converts every quarter (instead of every month), the minimum conversion block is 1,000 miles, ad-hoc conversions are free, and there’s no silly “working capital” balance that needs to be maintained on the bank side.

The fact that the DBS automatic conversion scheme is only available for selected cards should be no barrier either, since DBS Points pool. If you have an Altitude, Treasures Black Elite or Insignia Card, you can use that as a conduit to cash out points earned on the Vantage or Woman’s World Card.

Conclusion

UOB cardmembers can choose to enrol in the KrisFlyer Auto Conversion Programme, which offers twelve monthly conversions per year for a flat fee of S$50. This has the added benefit of reducing the minimum transfer block from 5,000 to 2,500 UNI$, although it also means starting KrisFlyer’s 3-year expiry clock early.

The big problem here is that UOB insists you keep 15,000 UNI$ with them at all times. This minimises the scheme’s usefulness as a tool to minimise orphan balances, and seems downright silly to me.

Would you use UOB’s KrisFlyer Auto Conversion Programme?

How does the point pooling works together with the auto conversion if I own both PRVI and uob krisflyer? Does the points earned from PRVI being converted automatically together with the krisflyer card?

there is no such thing as points with the uob krisflyer card. you earn miles that are directly converted to Krisflyer.

Hello Aaron, for this case if my credit card is cancelled, does the auto conversion also automatically cancel, or i have to call them to cancel it? Thank you

UOB is doing this auto conversion manually. When i used it, the monthly conversion failed quite often. Then I need to ask CS to escalate and fix. Sometimes they even forget to refund the 25 dollar charge.