| The following is a sponsored post by Citibank. The opinions and analysis remain those of The Milelion |

Good news for Citi PremierMiles Visa cardholders: from now till 31 December 2019, you’ll earn 1.5 mpd on all local spending, subject to a minimum spend of S$3,000 per statement month.

No registration is required and there is no cap on the bonus miles you can earn. Should you hit the S$3,000 threshold, the 1.5 mpd rate will apply to spending from the first dollar. For example, if you spend S$3,500, you’ll earn a total of 3,500 * 1.5= 5,250 miles.

| For the avoidance of doubt, this promotion does not apply to Citi PremierMiles AMEX cardholders- they’ll continue to earn the usual 1.3 mpd |

You’ll initially see the regular rate of 1.2 mpd credited to your Citi Miles account, and the bonus 0.3 mpd will be credited by the end of the current statement period.

A rate of 1.5 mpd would make the Citi PremierMiles Visa one of the highest earning general spending cards in the S$30,000 segment, as the table below shows:

| General Spend Rate (Local) | |

| Citi PremierMiles Visa |

min spend S$3,000 per statement period |

BOC Elite Miles World Mastercard BOC Elite Miles World Mastercard |

1.5 |

UOB PRVI Miles UOB PRVI Miles |

1.4 |

DBS Altitude DBS Altitude |

1.2 |

OCBC 90°N Card OCBC 90°N Card |

1.2 |

AMEX KrisFlyer Credit Card AMEX KrisFlyer Credit Card |

1.1 |

| Only cards with $30,000 income requirements shown. You could earn 1.6 mpd on cards like the DBS Insignia/UOB Reserve/Citi ULTIMA, but these have $500,000+ income requirements |

|

The full T&C of the offer can be found here.

What counts towards the S$3,000 spending?

Good news here- Citi is defining qualifying spend fairly broadly, the only exclusions being:

|

This means that transactions which do not usually earn rewards points will still count towards the S$3,000 threshold for the purposes of this promotion, e..g insurance, education, government services, charitable donations, gambling, or top-ups of prepaid accounts.

For example, I may spend S$2,500 on dining (which normally earns points) and S$500 on insurance (which normally does not). Collectively, I’d have spent S$3,000 and will qualify for the 1.5 mpd earning rate. The number of miles I’ll receive, however, will be S$2,500 * 1.5 = 3,750 miles.

Whether or not it’s worth giving up the miles on a portion of your spending just to hit the S$3,000 threshold is another matter, but given that you can’t really earn miles on government services or charitable donations anyway, it would make sense to use the Citi PremierMiles for these transactions at least.

Spending on Citi PayAll will also count towards the S$3,000 threshold, which means that anyone with rent, tax, education expenses, condo management fees, or electricity bills to be paid has an opportunity to buy miles at the very low price of 1.33 cents each.

| Cost per mile @ 1.2 mpd | Cost per mile @ 1.5 mpd | |

|

1.67 | 1.33 |

| Based on 2% admin fee, certain Citi customers may be targeted for lower rates |

||

1.33 cents, for context, would be one of the lowest cost ways of buying miles in Singapore.

Statement month vs calendar month

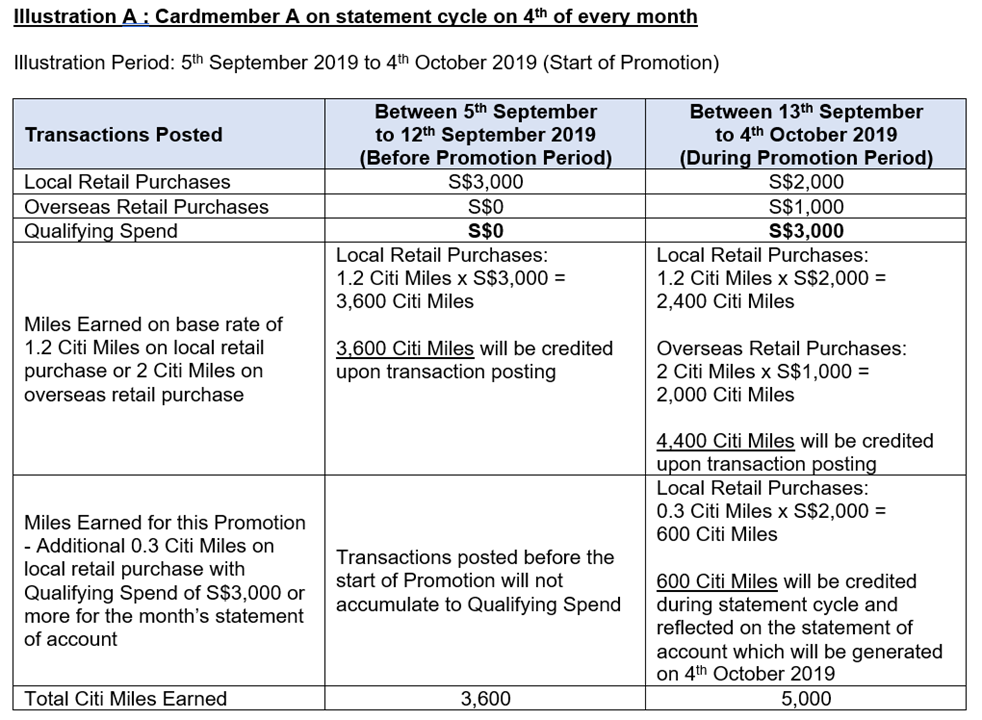

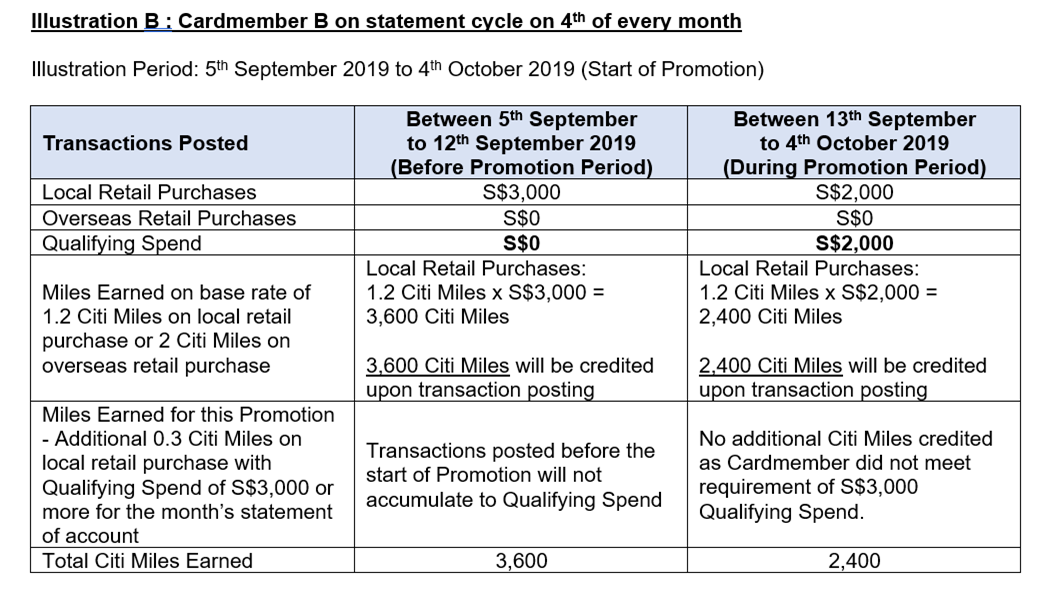

Remember: the S$3,000 spending is based on your statement month, which may be different from the calendar month. For example, your statement cycle may run until the 4th of every month, which means you’ll need to spend S$3,000 from 12 September 2019 to 4 October 2019 to qualify for the 1.5 mpd rate.

Here’s some illustrations as to how it works; additional scenarios can be found in the T&C.

You can check your statement month by logging into Citibank’s ibanking portal and clicking on your credit card account. You’ll see a line for “last statement date”, which shows when your statement period ends. In my case, my statement runs from 12th of each month to the 11th of the following month.

Use the Citi PremierMiles Visa to access a wide variety of transfer partners

One of the best features of the Citi PremierMiles Visa card is its numerous transfer partners. Citi Miles can be transferred to 11 different frequent flyer programs and 1 hotel partner at a 1:1 ratio.

| Transfer Ratio | |

| 1:1 | |

| 1:1 | |

| 1:1 | |

| 1:1 | |

| 1:1 | |

| 1:1 | |

| 1:1 | |

| 1:1 | |

| 1:1 | |

| 1:1 | |

Thai Airways Royal Orchid Plus Thai Airways Royal Orchid Plus |

1:1 |

| 1:1 |

Why would you be interested in earning anything other than KrisFlyer miles? Well, other frequent flyer programs have great sweet spots for certain destinations, which means you could earn your free flight with even less spending than if you had chosen KrisFlyer.

Some examples of sweet spots accessible through the Citi PremierMiles Visa are shown below:

| One Way Business Class | With Miles&Smiles | With KrisFlyer |

| Singapore to Europe | 45,000 miles | 92,000 miles |

| Singapore to North America | 67,500 miles | 92,000-99,000 miles |

| Singapore to South America | 75,000 miles | 119,000 miles |

| With Etihad Guest | With KrisFlyer | |

| Singapore to Koh Samui | 10,000 miles (Business) | 21,500 miles (Business) |

| Singapore to Seoul | 30,000 miles (Business) | 47,000 miles (Business) |

| Singapore to Colombo | 28,000 miles (Business) | 39,000 miles (Business) |

| Intra-Brazil | 3,000-17,000 miles (Economy) | 12,500 miles (Economy) |

| Intra-Europe | 5,000-10,670 miles (Economy) | 12,500 miles (Economy) |

| One Way Economy | With BA Executive Club | With KrisFlyer |

| Intra-Europe | 4,000-13,000 miles | 12,500 miles |

| Intra-Japan | 6,000-9,000 miles | 12,500 miles |

| Intra-Australia/Trans Tasman | 6,000-13,000 miles | 11,000-20,000 miles |

| Singapore to Hong Kong | 11,000 miles | 15,000 miles |

| Singapore to Perth | 13,000 miles | 20,000 miles |

Citi Miles do not expire, and can also be used to offset the cost of revenue flights and hotels via Citi’s travel portal (although for the best value, you’ll obviously want to convert them to miles).

Conclusion

A 1.5 mpd rate is a great opportunity to earn additional miles on general spending, and the inclusion of PayAll transactions means that anyone with rent, tax bills or education expenses should be able to hit the S$3,000 threshold.

If you don’t already have a Citi PremierMiles Visa card, signing up as a new-to-bank customer through the link below and spending $7,500 in the first 3 months after approval will get you a total of 30,000 miles. You’ll also be eligible for the 1.5 mpd promotion, even if you were approved after it began.

Hi Aaron – does payment made to ipaymy / cardup qualify? Thanks.

yes

Hi Aaron, just wanted to clarify whether a cardup or renthero payment for rent and/or private school fees would (1) count towards the $3,000 minimum payment and (2) accure 1.5 mpd? Or would I have to use the Citi Payall instead for it to count towards the $3k monthly minimum threshold and/or accrue 1.5 mpd on the rent and education payment? Obviously asking because it would make sense to use cardup or renthero instead of citi payall as they offer a lower admin fee (1.9/1.85% compared to citi payall’s 2%).

with the exception of the 3 categories mentioned in the post, everything else will be qualifying.

i know most compare this to the boc em because of the 1.5mpd but seems it’s a direct response to the enhanced rates of the altitude amex to me (also I reallyx3 am not so tempted to test my patience by using boc’s antique banking set up) higher spend needed but lower mpd for a wider acceptance compared to altitude’s amex premiermiles has no cap but has rigidity of min 3k in a statement cycle whereas altitude is more direct at total 6k spend across 3mths which if one signed up recently will cover till near year end as well;… Read more »

aye, I missed out on the para below the one i quoted

so regardless, spends across those usually ineligible categories will still earn no pts

have quite a bit of those coming up and got excited for nth

blah

Spending on things like charitable donations etc will count towards 3k but not earn points. So if you are intending to do those donations anyway, you might as well put on premiermiles since no other card (bar Amex, where accepted) will give you points

got it, kinda reverse of the scb x where some categories earn pts but doesn’t add towards qualifying spend for the bonus

have quite a bit of insurance and govt related spends coming up, guess the excitement activated selective reading, just saw the parts I wanted and skimmed through the rest

might give it a miss since I just got started on the altitude amex promo with 1.8mpd but I guess it’ll be useful for those who have already done the altitude amex run since June

Yeah actually your analysis RE: altitude Amex is spot on. I’d advise you to do the same

since we’re at it, can I check if my understanding is correct that for a new sign up altitude amex,, no registration is required and as long as we hit 6k spend across 3mths we will be eligible for existing bank customer 5k miles bonus + enhanced 50% earn rate with cap of 10k miles, ie. up to 16667 at 1.8mpd?

no love for existing altitude amex holders to enjoy 50% enhanced rates at least?

i’m using payall every month for about $3K of expenses so this is actually perfect for me.

loved the part on the citi sweet spots, didn’t know about most of those. all this time i’ve been just blindly converting to krisflyer.

prestige card hurts

Promo benefit for prestige usually come in the form of perks which is why I’m still holding on to the premiermiles even though I hate the thought of paying another transfer fee.

No point to cancel and wait for another sign up promo either since those are generally pretty weak for existing bank customers or only for new to bank applicants but premiermiles is the only card that runs decent promos for current cardholders from time to time.

hm, is it just me but i can’t seem to find a flight for ethihad from singapore to seoul?

Asiana. Read the post I wrote about Etihad’s 23 award charts- asiana is a partner

Does top-up of EZ-Link / NETS flashpay count towards the $3k qualifying spend AND getting miles? E.g., Monthly card spend $4000, with $200 from topping up NETS flashpay. Do I get 6000 miles?

No

Looking at the T&C it states “”Eligible Cardmember” refers to an individual who holds an Eligible Card as a main cardholder.”

How about the spending on the supplementary card?

Appreciate you insights to the T&C. Thank you

all pooled to main cardholder

Has anyone tried Grabpay top up with the card and know if that counts toward the 3k requirement?

Quote: “Spending on Citi PayAll will also count towards the S$3,000 threshold, which means that anyone with rent, tax, education expenses, condo management fees, or electricity bills to be paid has an opportunity to buy miles at the very low price of 1.33 cents each.” Hi Aaron, Simply put, if i pay $6,000 income tax lump sum and solely using Citi payall + Premier miles card, that means i get 6,000 x 1.5 = 9,000 miles? Are you able to verify this? I called customer service and they said this will only count to $1: 1.2 miles instead of $1:1.5… Read more »

it should be 1.5 mpd, as per the citi PM team.

can you earn miles from topping up your grabpay?