It’s been an eventful weekend for the HSBC TravelOne Card, to say the least.

First came the news that cardholders could now transfer points to eight new airline and hotel partners, with exciting names such as Air Canada Aeroplan and Japan Airlines Mileage Bank. Unfortunately, the conversion ratios left a lot to be desired, with the new partners costing 20%-100% more points than the existing slate.

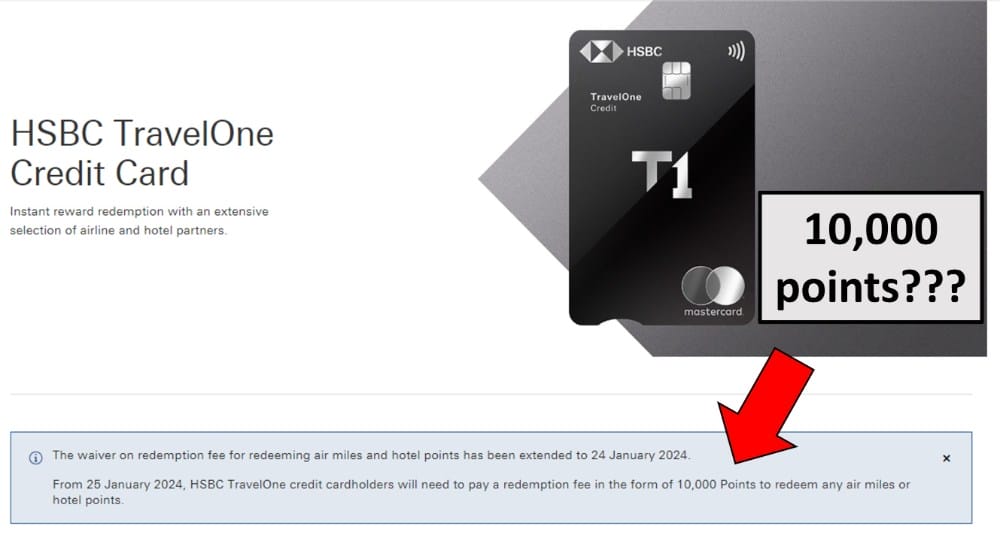

But even that paled in comparison to the uproar surrounding HSBC’s decision to charge an absurdly expensive conversion fee of 10,000 points, effective 25 January 2024.

This inexplicable decision would make HSBC transfers the most expensive in the market at ~S$60 a pop, and even though no one expected the current fee-waiver promotion to continue forever, most were expecting a fee in the region of S$25.

So where does that leave us, if you’re considering a HSBC TravelOne Card or already a cardholder?

Recap: HSBC TravelOne Card changes

In case you slept through the weekend, here’s what’s happened to the HSBC TravelOne Card.

HSBC TravelOne Cardholders can now transfer points to 20 different airline and hotel partners at the ratios below.

| ✈️ HSBC TravelOne Airline Partners | |

| Frequent Flyer Programme | Conversion Ratio (HSBC Points : Partner) |

| 50,000 : 10,000 | |

| 40,000 : 10,000 | |

| 35,000 : 10,000 | |

| 35,000 : 10,000 | |

| 35,000 : 10,000 | |

| 35,000 : 10,000 | |

New New |

30,000 : 10,000 |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 |

|

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

|

25,000 : 10,000 |

| 🏨 HSBC TravelOne Hotel Partners | |

| Hotel Programme | Conversion Ratio (HSBC Points : Partner) |

New New |

30,000 : 10,000 |

| 25,000 : 5,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

Unfortunately, the new airline partners have ratios ranging from 30,000 to 50,000 points to 10,000 miles, 20%-100% more than the 25,000 points to 10,000 miles that was standard for all nine airline partners prior to this.

To put it another way, HSBC TravelOne Card cardholders currently earn:

- 3X HSBC points per S$1 on local spend

- 6X HSBC points per S$1 on foreign currency spend

That works out to 1.2 mpd/2.4 mpd, but only if you’re choosing a partner with a 25,000 points to 10,000 miles ratio. Otherwise, the earn rates can fall as low as 0.6 mpd/1.2 mpd respectively.

| If the transfer ratio is | Local Spend | FCY Spend |

| 25,000 : 10,000 | 1.2 mpd | 2.4 mpd |

| 30,000 : 10,000 | 1 mpd | 2 mpd |

| 35,000 : 10,000 | 0.86 mpd | 1.71 mpd |

| 40,000 : 10,000 | 0.75 mpd | 1.5 mpd |

| 50,000 : 10,000 | 0.6 mpd | 1.2 mpd |

This problem is compounded by the fact that it’s not easy to accrue HSBC TravelOne points:

- HSBC points don’t pool — the bank says they’re working on adding this, but it won’t be coming in 2023 — so you can’t tap the 4 mpd earning power of the HSBC Revolution

- HSBC does not have an equivalent of Citi PayAll; in fact, they ended their income tax payment facility for credit cards in January this year

- HSBC does not allow cardholders to earn points on CardUp/ipaymy transactions

Therefore, it’d take a significant amount of spending to reach the critical mass required for a long-haul Business Class award, let alone several, let alone if you’re looking at a frequent flyer programme with a 30,000-50,000 points : 10,000 miles ratio!

But never mind the ratios; it’s the conversion fee that’s got everybody up in arms. HSBC TravelOne Cardholders will continue to enjoy free conversions till 24 January 2024, but from 25 January onwards, it’s a flat fee of 10,000 points.

10,000 HSBC Points is the equivalent of 4,000 KrisFlyer miles, and if we use my value of 1.5 cents per mile, that’s a hefty $60 per conversion, head and shoulders above what any other bank is charging.

I like how someone on the Telegram group phrased it: HSBC is going the extra mile to make things worse for customers. I mean, if they had gone with the market average of S$25, no one would have bat an eyelid. For them to specially come up with a 10,000 points fee feels intentionally antagonistic, and even if they walk it back, the damage has already been done.

If you don’t have a HSBC TravelOne Card

Let’s start with the easier scenario.

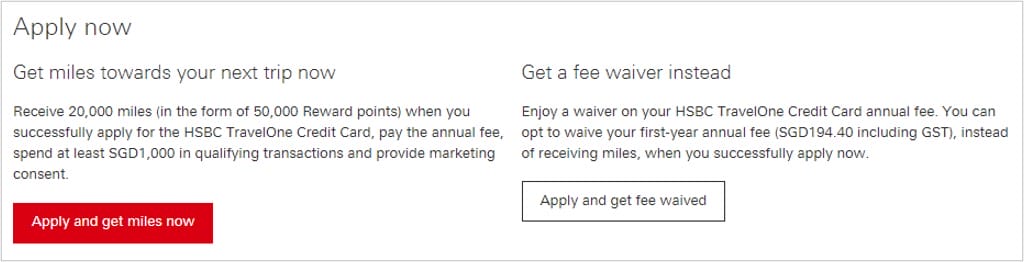

If you don’t have a HSBC TravelOne Card yet, it’s a bad idea to sign up now unless you take the first year free option.

Fee paying option

If you take the fee-paying option, HSBC will award 50,000 bonus points (20,000 miles) when you:

- Pay the annual fee of S$194.40

- Spend at least S$1,000 by the end of the second month after approval

Here’s the thing: these bonus points are credited within 90 days from the card account opening date. Based on today’s date, that’s 12 February 2024.

So you’re effectively rolling the dice here, because if the points are credited from 25 January 2024 onwards, your bonus is reduced by 10,000 points (4,000 miles) due to the conversion fee, becoming 40,000 points (16,000 miles) in total.

That’s a 20% haircut on the promised bonus, and a much less convincing offer.

Fee waiver option

But there’s still a case to be made for signing up for a HSBC TravelOne Card, if all you care about is free lounge visits.

HSBC offers a first year fee waiver option, which does not include the 50,000 bonus points. It does, however, include four DragonPass lounge visits per year.

Since the allowance is tracked by calendar year, you enjoy eight visits in your first membership year: the first set valid till 31 December 2023, the second set valid from 1 January 2024.

Enjoy the visits, then cancel the card when renewal comes round in 2024.

| ❓ Won’t this affect my new-to-bank status? |

|

If you’re hoping to leverage your new-to-bank status for a welcome gift, the good news is that a HSBC TravelOne Card won’t affect it. For example, if I only hold a HSBC TravelOne Card, I will still count as a new-to-bank customer when signing up for a HSBC Revolution, Advance or Visa Platinum, and can enjoy gifts such as S$350 cash, a Dyson Supersonic hairdryer or an Apple iPad 9th Gen from SingSaver. |

If you have a HSBC TravelOne Card

If you already have a HSBC TravelOne Card, I’d like to provide this nugget of wisdom.

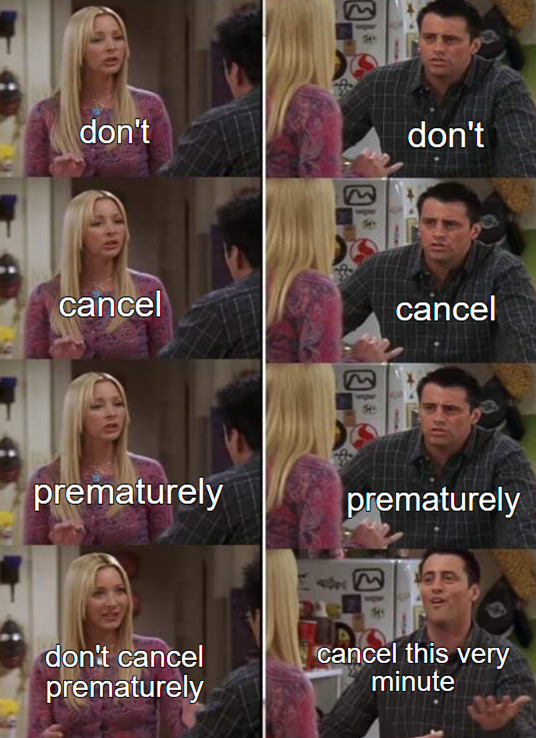

Even if you dislike where the TravelOne Card is heading, there’s no point cancelling early for three main reasons.

First, you’re going to receive four more lounge visits from 1 January 2024. You might as well use those before closing out your account.

Second, if you cancel the card too early, your welcome bonus can be clawed back. Per the HSBC T&Cs:

11. In the event that a customer cancels the Card within 12 months from the date such Card is issued to him/her, HSBC reserves the right to (i) debit that customer’s account for any HSBC Rewards Points awarded to him/her in connection with the Gift, or (ii) charge that customer for the equivalent value of any Gift awarded, as determined by HSBC in its discretion.

In other words, even if your plan is to cancel the card, you should wait until your first year is up. After that, you can cancel and seek a refund of the second year’s annual fee (remember: annual fees are charged upfront in respect of the upcoming year).

Third, annual fees are not pro-rated. It’s not like you’ll get some money back if you cancel now, versus waiting till your membership year is up.

In the meantime, it goes without saying that you should also transfer out all your points before 25 January 2024 to avoid the 10,000 points conversion fee. While HSBC has stated that points pooling is on its roadmap, I wouldn’t hold my breath for it to arrive before the new conversion fee comes into effect.

As for which programme you choose, that really depends on what you’re trying to solve for. Unfortunately, 50,000 points won’t get you very far with Aeroplan or Japan Airlines Mileage Bank, so I’ll probably be boring and send them to KrisFlyer- rather a damp squib of an ending for a card which promised so much variety when first launched.

What if HSBC walks back the changes?

There’s still time before 25 January 2024 rolls round, so it’s possible that the uproar forces HSBC to nix its plans and go with a more traditional S$25 per transfer.

But even if they do, it’s hard to make a case for continued use of a general spending card that earns at best 1.2/2.4 mpd on all spending. I’d much rather focus my attention on the HSBC Revolution, and wait till the new partners become available.

My bigger concern, actually, is that they expand this boneheaded fee to cover the Revolution and other HSBC cards when they’re brought on to the same platform. And if that happens, we’ll need to take a long, hard look at using HSBC cards in the first place.

Conclusion

HSBC TravelOne Cardholders now have access to 20 different airline and hotel transfer partners, by far the most of any bank in Singapore.

But dig beneath the surface, and not all is well. Some of these partners have conversion ratios that nerf any potential value, and regardless of which programme you choose, you’ll be subject to a 10,000 points conversion fee come 25 January 2024.

That means you’d be well advised to start thinking of an exit plan- though you should hold off actually cancelling your card until the first 12 months have lapsed to avoid a clawback of the welcome offer.

HSBC TravelOne Cardholders: What’s your plan now?

Good point about the points claw-back. Yes, I will hold and see what happens but not spending on it anymore.

Plan to wait till 20th Jan to see if they reverse this decision. If they don’t then as you advised, transfer points before 25th Jan, and enjoy the dragon pass, and cancel at 12 month mark.

I had 55k points – transferred out already. Trust Broken.

Will use the 4 lounge access in 2024 and then cancel once the annual fee is charged – meanwhile no more spending on this ‘much promised land’ card

Hi Aaron, I signed up for this card literally one day before the announcement of the 10,000 point conversion fee. Since the conversion fee seems to be unavoidable for me, I was wondering if I should continue spending on this card to meet the $1,000 spend for the promo (I’ve spent $180 so far), or if I should call in for the fee waiver option and spend on my existing Revolution card instead?

Telecos should be valid spends for the min required spending for the sign up bonuses