The HSBC Revolution received a major refresh on 1 April 2026, which permanently reinstated bonuses for travel and contactless spending, while boosting the earn rate to up to 8 mpd.

This makes it an excellent option for dining, shopping, transport and travel — a remarkable turnaround for a card which looked dead and buried not that long ago!

As part of the refresh, HSBC has also launched a new welcome offer worth up to 16,800 bonus miles, replacing the previous Samsonite luggage gift. Unfortunately, unlike the improvements to the card’s CVP, this promotion is significantly weaker. Not only is this welcome gift inferior to those offered by alternative channels like SingSaver, but there’s the added requirement to take up a fee-incurring HSBC Cash Instalment Plan.

HSBC is also running a separate promotion offering up to 55,200 bonus miles for customers who open a HSBC Everyday Global Account (EGA) and maintain at least S$50,000, which I’ll cover in a different post.

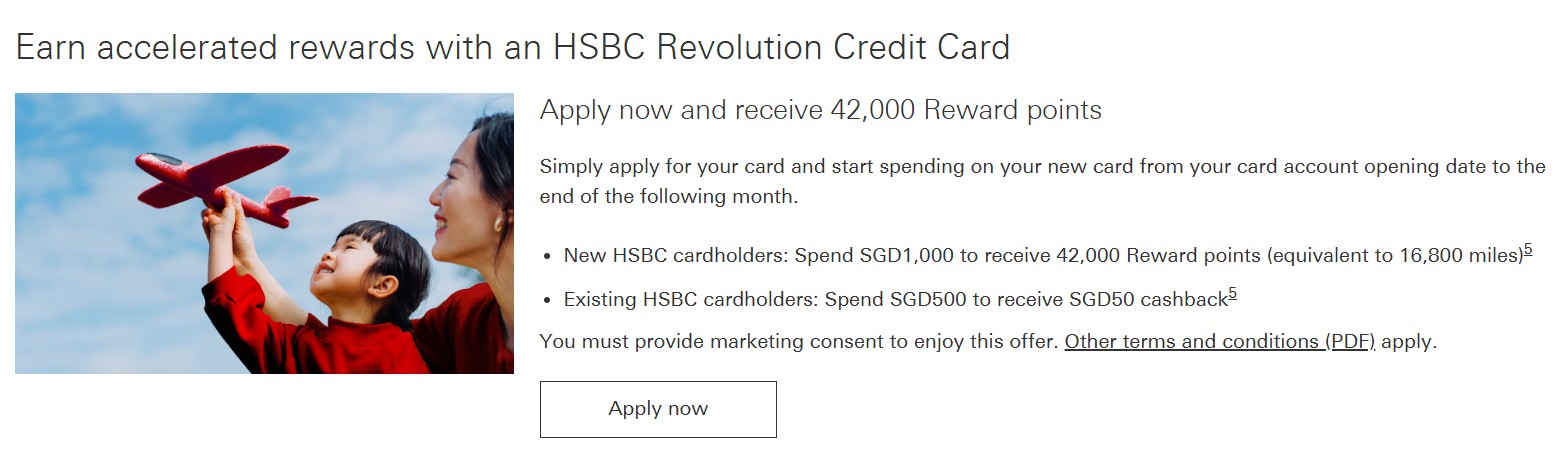

HSBC Revolution launches 16,800 bonus miles sign-up offer

|

|||

| Apply |

From 1 April to 30 June 2026, customers who apply for a HSBC Revolution Card will receive either 16,800 bonus miles, or S$50 cashback.

| New HSBC Cardholder | Existing HSBC Cardholder | |

| Min. Spend | S$1,000 | S$500 |

| Gift | 16,800 miles (42,000 HSBC points) |

S$50 cashback |

To receive the welcome gift, cardholders must:

- Receive approval by 14 July 2026

- Meet a minimum spend of S$500 (for existing HSBC cardholders) or S$1,000 (for new HSBC cardholders)

- Provide consent to receiving marketing and promotional materials during application (an important step that people often forget!)

- Sign-up for a new HSBC Cash Instalment Plan with a minimum loan amount of S$5,000 and minimum tenure of 12 months

The welcome gift is in addition to the usual miles that HSBC Revolution Cardholders usually earn. For example, if a cardholder spends the entire S$1,000 on eligible bonus categories, and maintains a minimum of S$50,000 in their HSBC EGA, they will earn an additional 8,000 miles (S$1,000 @ 8 mpd).

Who is eligible?

HSBC defines new and existing cardholders as follows:

- New cardholders: Customers who do not hold any existing principal HSBC credit card, and have not cancelled a principal HSBC credit card in the past 12 months

- Existing cardholders: Customers whose most recent principal HSBC credit card was issued more than 12 months ago, and have not cancelled a principal HSBC credit card within the past 12 months

While other banks define an existing cardholder as anyone who doesn’t meet the new cardholder definition, HSBC does things a little differently.

To meet the “existing cardholder” definition, at least 12 months must have passed since your last principal HSBC credit card was approved, and you must not have cancelled any principal HSBC credit card in the past 12 months.

For example:

- John has a HSBC TravelOne Card approved six months ago. He will not be eligible for the HSBC Revolution Card’s existing cardholder welcome bonus

- Jack has a HSBC TravelOne Card approved >12 months ago, and a HSBC Live+ Card approved >12 months ago. Last month, he cancelled his HSBC Live+ Card. He will not be eligible for the HSBC Revolution Card’s existing cardholder welcome bonus either

Therefore, when it comes to HSBC, it’s possible that you’re neither new nor existing!

To learn more about HSBC’s “applicant limbo”, refer to this post.

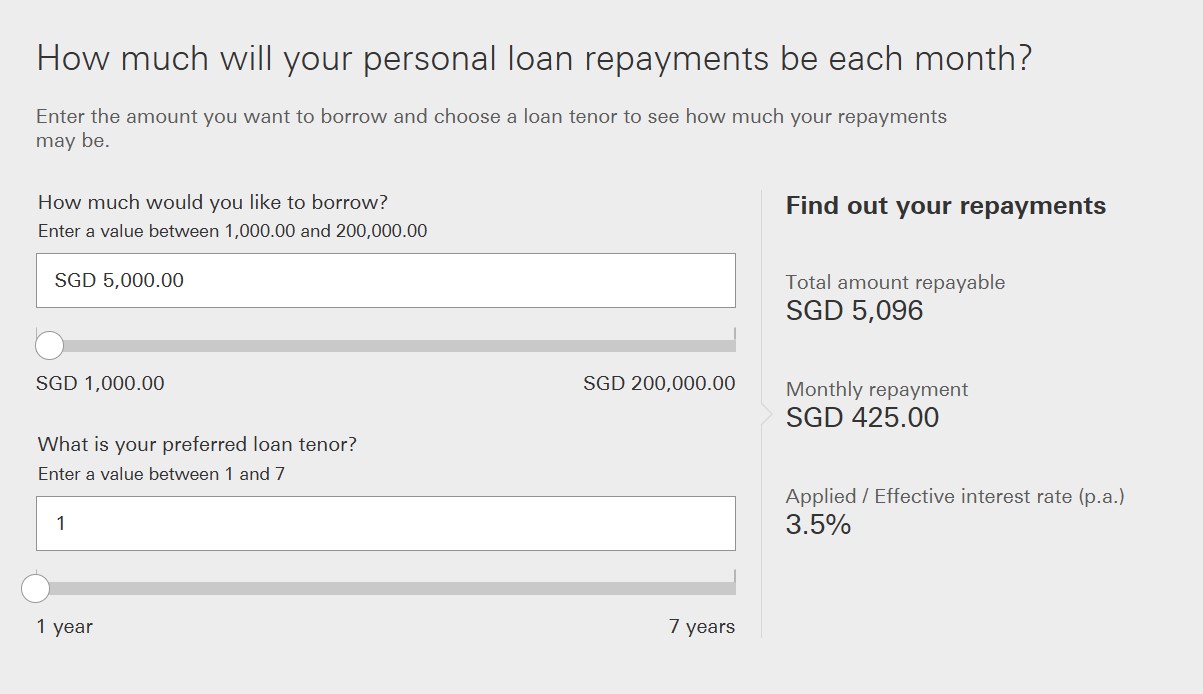

The catch: HSBC Cash instalment requirement

For this welcome offer, HSBC has added a new requirement for customers to apply for a HSBC Cash Instalment Plan with a minimum loan amount of S$5,000 and a minimum loan tenure of 12 months.

Based on the quoted EIR of 3.5% p.a., you’ll repay a total of S$425 per month, or S$5,096 over the life of the loan. Mind you, the 3.5% p.a. EIR is for HSBC Premier customers only. A higher rate may apply to regular HSBC customers.

Unfortunately, this effectively means you’ll have to “pay” for your welcome gift, and you should stick to the minimum loan amount and tenure as far as possible.

What counts as qualifying spend?

Cardholders must make a minimum qualifying spend of S$500 or S$1,000 by the end of the month following card approval.

| Card Account Opening Date | Qualifying Spend Period |

| 1-30 April 2026 | 1 April to 31 May 2026 |

| 1-31 May 2026 | 1 May to 30 June 2026 |

| 1-30 June 2026 | 1 June to 31 July 2026 |

| 1-14 July 2026 | 1 July to 31 August 2026 |

This means that you have anywhere between 1-2 months to meet the minimum spend, depending on when your card is approved. If you have concerns about meeting the minimum spend, try to get approved early in the month so you have more time.

Qualifying spend includes all online and offline retail transactions, excluding those found at 3.4 and 3.5 of the T&Cs.

The key exclusions to note here are insurance, utilities, education, government transactions as well as CardUp/ipaymy payments.

When will the gift be credited?

Welcome gifts will be credited within 120 days of the account opening date.

Terms & Conditions

The T&Cs of this offer can be found here.

Is it worth it?

|

| Apply |

Instead of applying through HSBC, customers have the option of applying through SingSaver and enjoying one of the following gifts:

| HSBC | SingSaver | |

| Min. Spend | S$1,000 | S$500 |

| Cash Instalment Plan? | Yes | No |

| Gift |

|

|

If you ask me, the SingSaver option looks much more attractive:

- The minimum spend is lower at S$500

- There’s no need to apply for a HSBC Cash Instalment Plan

I suspect it’s only a matter of time before HSBC requires affiliate partners like SingSaver to adopt the same eligibility requirements, but even so, S$400 cash is clearly superior to 16,800 miles (unless you value a mile at more than 2.4 cents each, which is pushing it):

For the avoidance of doubt, it is not possible to combine the HSBC and SingSaver gifts. You must choose one or the other.

What can you do with HSBC points?

HSBC points can be transferred to 20 airline and hotel partners, at the ratios shown in the table below.

| ✈️ HSBC Airline Partners | |

| Frequent Flyer Programme | Conversion Ratio (HSBC Points : Partner) |

| 50,000 : 10,000 | |

| 35,000 : 10,000 | |

| 35,000 : 10,000 | |

| 35,000 : 10,000 | |

| 35,000 : 10,000 | |

| 35,000 : 10,000 | |

| 30,000 : 10,000 |

|

|

30,000 : 10,000 |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 |

|

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

|

25,000 : 10,000 |

| 🏨 HSBC Hotel Partners | |

| Hotel Programme | Conversion Ratio (HSBC Points : Partner) |

|

30,000 : 10,000 |

| 25,000 : 5,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

The crucial thing to understand is that not all partners share the same transfer ratio. Therefore, the effective earn rate depends on the partner you choose.

For example, the HSBC Revolution only earns 8 mpd if you choose a partner with a 25,000 points = 10,000 miles transfer ratio, like British Airways Executive Club or EVA Air Infinity MileageLands. If you choose KrisFlyer, where the ratio is 30,000 points = 10,000 miles, then the earn rate is 6.66 mpd (that’s still not bad, mind you!).

| Transfer Ratio (Points : Miles) |

HSBC Revolution (Regular) |

HSBC Revolution (Enhanced) |

| 25,000 : 10,000 (8x partners) |

4 mpd | 8 mpd |

| 30,000 : 10,000 (2x partners) |

3.33 mpd | 6.66 mpd |

| 35,000 : 10,000 (5x partners) |

2.86 mpd | 5.71 mpd |

| 50,000 : 10,000 (1x partner) |

2 mpd | 4 mpd |

All conversions must be done via the HSBC Singapore app (Android | iOS) and are processed instantly, with the exception of the following:

- Hainan Fortune Wings Club: Within 5 business days

- Japan Airlines Mileage Bank: Within 10 business days

Conversions are free of charge until further notice, and HSBC points are pooled across cards.

While the minimum transfer block is 10,000 miles/points (Accor: 5,000 points), the subsequent block is just 2 miles (Accor: 1 point). In other words, you could choose to transfer 10,002 miles or 20,958 miles, which helps you avoid orphan points.

Overview: HSBC Revolution

|

|||

| Apply | |||

| Income Req. |

S$30,000 p.a. (with S$50K TRB) S$65,000 p.a. (otherwise) |

Points Validity |

37 months |

| Annual Fee |

None | Min. Transfer |

25,000 HSBC points (10,000 miles) |

| Miles with Annual Fee | None | Transfer Partners | 20 |

| FCY Fee | 3.25% | Transfer Fee | None |

| Local Earn | 0.4 mpd | Points Pool? | Yes |

| FCY Earn | 0.4 mpd | Lounge Access? | No |

| Special Earn | 4 -8 mpd on dining, shopping, transport & membership clubs, travel | Airport Limo? | No |

| Cardholder Terms and Conditions | |||

The HSBC Revolution splits customers into two categories:

- Regular cardholders

- Enhanced cardholders (defined as those who maintain ≥S$50,000 ADB for a given month in a HSBC Everyday Global Account in SGD)

Regular cardholders will earn 4 mpd on up to S$1,000 of monthly spending on bonus categories, while enhanced cardholders will earn 8 mpd on up to S$1,200 of monthly spending on bonus categories.

|

|

|

| Regular | Enhanced | |

| Dining | 4 mpd Online Contactless |

8 mpd Online Contactless |

| Shopping | 4 mpd Online Contactless |

8 mpd Online Contactless |

| Transport & Member Clubs | 4 mpd Online Contactless |

8 mpd Online Contactless |

| Travel | 4 mpd Online Contactless |

8 mpd Online Contactless |

| Bonus Cap | S$1,000 per c. month | S$1,200 per c. month |

For a detailed review of the HSBC Revolution, refer to the post below.

Conclusion

The HSBC Revolution has launched a new welcome offer worth up to 16,800 bonus miles, available for new-to-HSBC cardholders with a minimum spend of S$1,000.

However, the added requirement to apply for a HSBC Cash instalment Plan is annoying, and will incur some out-of-pocket cost. Moreover, 16,800 bonus miles is not as attractive as the alternative gifts offered through SingSaver, so that would be my preferred application channel.