If you’ve ever applied for a credit card, then you’re probably aware of the distinction banks draw between new cardholders — who usually get the most lucrative gifts — and existing cardholders.

A new cardholder is generally defined as someone who does not hold a principal credit card, and has not cancelled one in the past 6-12 months. An existing cardholder, then, is simply anyone who does not meet the definition of a new cardholder.

However, HSBC defines things differently, which can often lead to confusion. With HSBC, it’s possible to fall into a weird sort of “applicant limbo”, where you’re neither new nor existing!

How does HSBC define new and existing cardholders?

New cardholders

![]()

HSBC defines a new cardholder as someone who meets both of the following conditions:

- Does not currently hold a principal HSBC credit card, and

- Has not cancelled any principal HSBC credit card within the last 12 months prior to approval

There’s nothing remarkable here, as this definition basically matches that used by other banks.

| 😞 It used to be better… |

|

HSBC previously took a more generous approach to defining a “new cardholder” by carving out an exception for the HSBC Visa Infinite and HSBC TravelOne Card. Holding either of these cards would not disqualify you from receiving new cardholder bonuses on the HSBC Advance, Premier, Revolution, or Visa Platinum cards. Unfortunately, this policy was changed in early 2025 to the stricter wording we have today. |

Existing cardholders

Here’s where things get significantly more complicated.

HSBC defines an existing cardholder as someone who meets both of the following conditions:

- Most recent principal HSBC credit card was issued more than 12 months ago, and

- Has not cancelled any principal HSBC credit card in the past 12 months

To qualify as an existing cardholder, all your principal HSBC credit cards must have been issued more than 12 months ago. To put it another way, if you were approved for any HSBC principal credit card within the past 12 months, you will not count as an existing cardholder.

That’s not all — you must also not have cancelled any principal HSBC credit cards in the past 12 months.

The second requirement may seem strange, since it’s typically applied to new cardholders only. I believe it exists because HSBC is one of the few banks that offers welcome gifts to existing cardholders as well. The intention is to keep people from signing up for a card to receive an existing cardholder gift, cancelling it shortly after, then reapplying to receive the gift again. That said, such behaviour would already be prevented by the first condition.

In fact, all the second requirement serves to do is penalise customers who have no intention of gaming the system. Suppose I’ve held HSBC Card A for several years. Then I decide HSBC Card B is a better fit for my lifestyle, so I cancel Card A and apply for Card B. That cancellation would make me ineligible for the existing cardholder welcome gift on Card B.

To preserve eligibility, I would instead need to apply for Card B first, fulfill the criteria for the gift, then cancel Card A subsequently.

It’s possible to be neither new nor existing!

You might think that new and existing are MECE (mutually exclusive, collectively exhaustive) categories. If you’re not new, you must be existing. If you’re not existing, you must be new. And indeed, that’s the case for every bank in Singapore.

But not HSBC. With HSBC, it’s possible to be neither new nor existing.

I would be neither new nor existing if I:

- Was approved for a principal HSBC credit card within the past 12 months, or

- Cancelled a principal HSBC credit card within the past 12 months

My guess is that HSBC wants to discourage customers from signing up for or cancelling cards too frequently, but it is very counterintuitive that there’s a third category of cardholders who are neither new nor existing!

Exception: HSBC Premier Mastercard

The HSBC Premier Mastercard has a different set of eligibility criteria for its welcome offer. To be eligible, customers must meet both of the following conditions:

- Do not currently hold a principal HSBC Premier Mastercard, and

- Have not cancelled a principal HSBC Premier Mastercard in the past 12 months

In other words, holding any other principal HSBC credit card, or cancelling one in the recent past, will not disqualify you from being eligible.

Here’s a reminder of the current welcome offer, valid for applications submitted by 31 March 2026.

| Customer | Criteria | Gift |

| Premier Qualified Customer |

|

Up to 91,800 miles (229,500 HSBC Points) |

| Non-Premier Qualified Customer |

|

Up to 34,200 miles (85,500 HSBC Points) |

More details on this can be found in the post below.

HSBC Premier Mastercard boosts welcome bonus to 91,800 miles

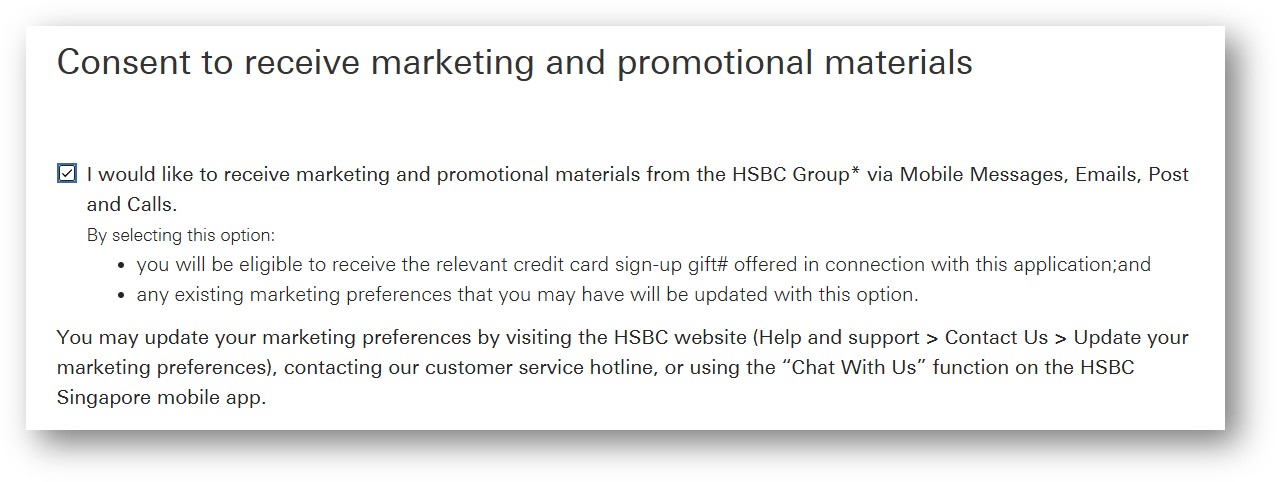

Don’t forget to provide marketing consent

In order to receive your welcome gift, HSBC has one more requirement: you must provide consent to receive marketing and promotional materials from HSBC at the time of application submission. This cannot be revoked until after the gift is credited.

Yes, this means you’ll get some advertisements in your inbox, but you can always set up a filter on your end to send these to the spam folder.

Conclusion

While HSBC’s definition of a new cardholder is in line with the market, its existing cardholder definition is much more unusual. You will not be considered an existing cardholder (for the purposes of welcome offers at least) if you recently opened or cancelled a principal HSBC credit card.

So the next time you apply for a HSBC card, double-check to make sure you’re not in “applicant limbo” — that’s a bad place to be!

HSBC is making application unusually difficult or perhaps due to MAS Rules but this did not helped with HSBC very poor customer service with a take it or leave it attitude. I am an existing HSBC card holder for say 30 years. No bad credit record and everything is settled on time. My income is ad hoc and not under employment as it is my own business. They asked for 3 months income statement so I provided the annual assessment from IRAS. I called up HSBC hotline and explained to them and asked for the card application personnel to call… Read more »

Unfortunately that’s not an exception with HSBC. Long time ime premier customer, first in Hong Kong, now in Singapore as well. When relocating from Hong Kong to Singapore, it took me 4 months to get a credit card, only got ot after yelling at the staff in downtown branch. Service in HK already with ups and downs unfortunately I had to learn in SG even more disappointing what HSBC does in regards of service. Further, I wasn’t treated as new to bank, as I had several cards in HK

Seems I am not the only one and they not making an exception in my case. Just to update, I made a call and this time an agent in Malaysia call centre picked up and I give it to Ameer who was very patient and spend a lot of time talking to his colleagues to push it through. In the end, they said give CPF statements (perhaps looking at interest income generated from CPF account per year) and also past two IRAS assessments. So I submitted and waiting for their approval or non-approval. Importance of getting the right customer service… Read more »

Not sure why all you humans have difficulties with HSBC… I never had a single problem in all my years of not banking with them.

i juz signed up and received my card. but the app they forced u to download (u need the security toKen) kept crashing. had to call them to sync up thereafter problem solved.