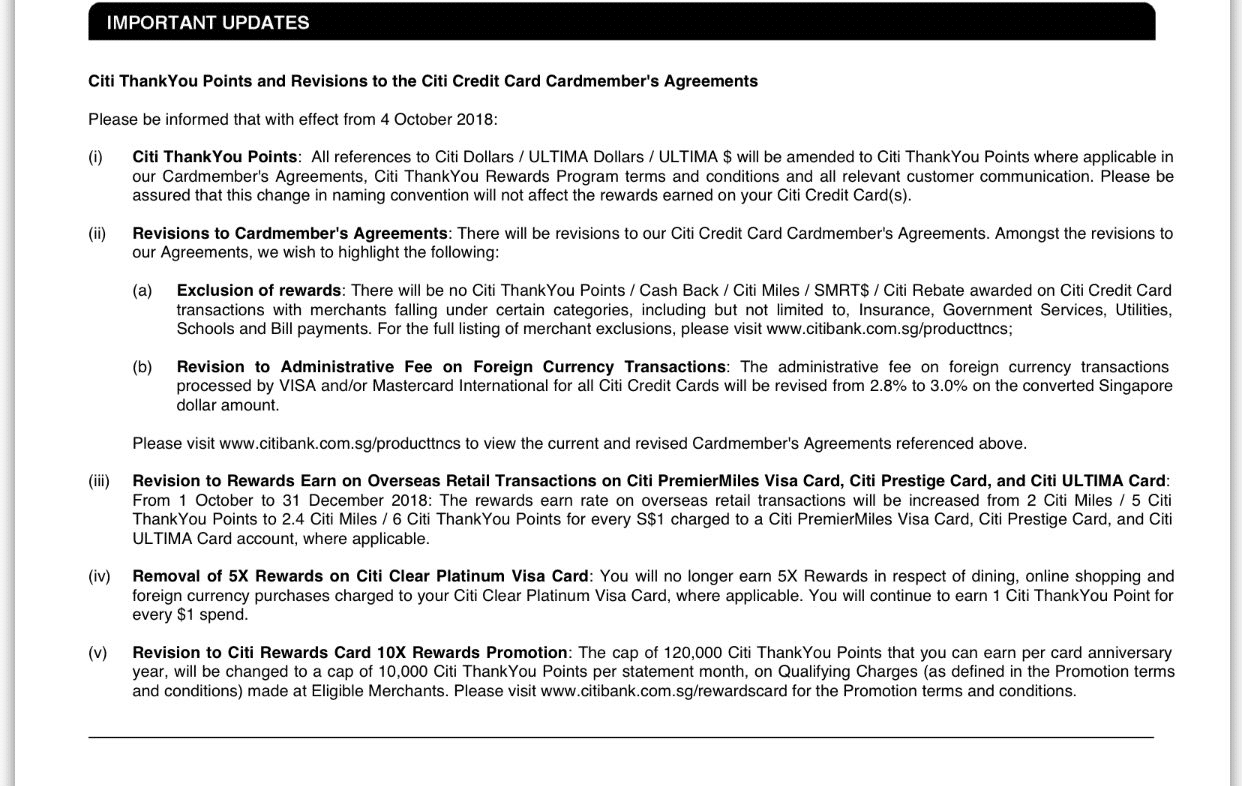

Update: Citi has uploaded the new sets of Terms and Conditions on the respective credit card pages.

This morning, I was notified by a reader from the Milelion Telegram Group that Citibank will be making big changes to the way points will be earned come 4 October 2018. These changes aren’t reflected on the Citibank website yet but appeared in the reader’s monthly credit card statement for the month of August 2018.

Here’s a screengrab courtesy of Jo from his credit card statement generated on 8 August 2018:

Here’s the changes:

Citi PremierMiles Visa, ULTIMA, Prestige will earn 2.4 mpd on FCY transactions up from 2.0 mpd…but FCY fees go up to 3%

From 1 October 2018 until 31 December 2018, all overseas retail transactions charged to the Citibank PremierMiles Visa, Citi Prestige and Citi ULTIMA card will see an increased earn rate of 2.4 miles per S$1 up from the current 2.0 miles per S$1 charged in foreign currency.

This improvement on the earn rate for foreign currency spend overseas puts this in line with the UOB PRVI Miles card which also earns 2.4 mpd on overseas foreign currency transactions. However, Citi does have the upper hand here as you earn points for every S$1 charged on your Citibank credit cards but with UOB, you earn points for every S$5 block.

The downside though, is that Citibank is also increasing the administrative fee imposed on all foreign currency transactions charged to all Citibank Visa and Mastercard credit cards from 2.8% to 3.0% from 4 October 2018. This would mean that your cost of acquiring points when using credit cards overseas will now be higher. While the increase of the earn rates for overseas foreign currency transaction seems like a temporary one, the increase in the administrative fee is permanent.

While an administrative fee of 3.0% is on the high side compared to the 2.5-2.8% which most other card issuers charge (i.e BOC), it’s still lower than what UOB charges for foreign currency transactions at 3.25% on the UOB PRVI Miles card which offers the same earn rate of 2.4 miles per S$1 for overseas foreign currency transactions.

If you’ve applied for the BOC Elite Miles World Mastercard however, you should be using that card for all overseas transactions from the time you get the card until the end of the year since it earns a whopping 5.0 mpd and the FCY fee is pegged at 2.5%.

Payments made to Insurance, Government Services, Utilities, and Schools will no longer earn rewards

From 4 October 2018, you will not be able to earn reward points for payments these MCCs. I’m assuming this will be for direct payments made to these billing merchants as Citibank still has its One Bill facility where you will be able to earn reward points when making payment to selected billing organizations which include Insurance, Utilities and Town Council payments through the One Bill facility.

Citibank hasn’t updated its T&C to reflect the full list of categories which will be specifically excluded but we will update this post once they do. (Edit: Citi has uploaded a new set of Terms and Conditions laying out the full list of exclusions here.)

Citi Clear Platinum Visa will not earn 5X Citi ThankYou points

The Citi Clear Visa Platinum card was demarketed by Citibank a few years ago. It currently earns 5X Citi ThankYou points (2.0mpd) on categories such as dining, online shopping and overseas retail transactions.

From 4 October 2018, you will only earn 1X Citi ThankYou point (0.4mpd) on all spend on the Citi Clear Visa Platinum. There are plenty of direct competitors offering the same earn rates to this card such as the HSBC Revolution which covers both dining and online spend and the DBS Woman’s Card which gives 2.0mpd for online spend as well.

This change shouldn’t really impact the majority as there are plenty of other cards which offers a higher earn rate for the categories which Citi Clear awards bonus points for. But for those of you who are still holding on to this card, I’m guessing it’s time to sock drawer it.

Citi Rewards card switches to a monthly cap on bonus 10X instead of an annual cap

The Citi Rewards card is one of my favourite cards to use as it has a very broad definition of what constitutes shopping. It did come with an annual bonus points cap of 120,000 Citi ThankYou points per card anniversary year which translates to a total spend of S$12,000 on categories which award you 10X points.

From 4 October 2018, the annual cap of 120,000 Citi ThankYou points will instead be in the form of a monthly statement period cap of 10,000 Citi ThankYou points on 10X categories. This means that the total amount you can charge to your Citi Rewards card, which will earn10X points, will be capped at S$1,000 per statement period.

This to me is a huge devaluation as many people have been performing big-ticket purchases using the Citi Rewards cards and hitting the 120,000 points cap easily within days of getting their cards and even for everyday spend, this would decrease the appeal of the Citi Rewards card especially if you’re thinking of charging big-ticket items to the card.

Currently, the Citi Rewards card and the OCBC Titanium Rewards card are close competitors as they both award 4.0 mpd for purchases of clothes, purchases at departmental stores and online shopping sites. With the change from 4 October 2018, the OCBC Titanium Rewards would be the better option if you’re intending to charge large purchases to your card, especially so now that they’ve cut the earning of 10X on mobile payments prematurely on the OCBC Titanium Rewards.

Concluding Thoughts

This is certainly very sad news, especially for the Citi Rewards card with the move to a monthly statement cap. With the monthly statement cap, I will not be surprised if people end up exceeding this cap due to them forgetting their credit card statement period. The annual cap which the Citi Rewards card currently uses has been around for quite some time and it has certainly been very generous.

Oh and another positive change that is coming out from this is that they are finally going to standardize the use of Citi ThankYou points instead of Citi Dollars and ULTIMA$ for the naming of their points currency.

time to slice em up

Hi Aaron, Sigh…. Now what…? Both my blue and pink OCBC Ti cards (4mpd benefit) have been maxed til Apr, so there I was thinking that I’ll pick up the Citi Rewards MC (on top of the Rewards Visa) cos I’ve already ‘used up’ about a third (accidentally) tapping at Taka last month, so the MC would’ve been ‘the plan’ to have for EU trip next Mar… to me, asking for and bringing the card (even 2) for S$1k each seems a way too much trouble.. ☹️ No other more-than 3mpd (SCB VI) for overseas use, at the moment, is… Read more »

Sorry.. Matthew.. ??

yeah, give credit when credit it due 🙂

UOB Visa Signature should still score you 4 miles on PayWaves/Online for foreign spending, just spend between $SGD1-2k/month.

Thanks, Yar.. yeah, I’ve got the UOB VS.. I should’ve mentioned that.. I actually use that in dept stores and small shops that have Paywave.. but $4k into 3 cards, in Europe.. not quite enough and really not worth the effort.. What I mean is.. let’s say you’re in a boutique and made a more-than-4k-purchase.. tell cashiers €630 on this, €630 on that, €1260 on this one, and the balance on that one..? A bit unglam lah.. hahaha.. I don’t mind doing it if it’s €6000 here and €6000 there, and actually did do that this year.. but……. not 1k… Read more »

Yeah, agree. I am also waiting for my BOC card 🙂

to standardize the use of Citi ThankYou points, does it mean I can combine Citi Miles and Citi Dollars?

Ditto. I don’t see them doing this, but we can hope. Or at least allow them to be pooled during transfer for just one transaction fee.

i guess someone got fired over the Apple Pay decision.

So which bank still award points to insurance payment? Quite some amount to pay every month.

HSBC Revo for 2mpd?

Prudential doesn’t accept HSBC credit card payment. For UOB card, can they earn points from insurance premium? Like UOB Visa Infinite?

UOB excluded all insurance payment. DON’T touch any UOB cards ever for insurance payment.

Well, there goes the ‘competition’. This probably had nothing to do with the release of the BOC EMWMC but the timing couldn’t have been any worse.

Are they going to pool points together from different Citi cards?

i wouldn’t count on it.

So what happens if lets say I’m on my 8th anniversary month of my card and I’ve already accumulated 100,000 points?

Does that mean I’ll be able to earn 10,000 points per month and not worry about exceeding the 120,000 point cap for that anniversary year (140,000 points total assuming I max out the cap every month for the remaining 4 months.)

This is I want to know. If current annual cap is removed and only monthly cap remains, it is bearable, but if both are there, then…

120k cap still applies, as per my understanding.

Thank you for this post. I am sad although I never hit $10k a month on my Citi Rewards as it is not my main card. This year, I charge most spending to UOB Preferred.

ipaymy isn’t mentioned in the list of excluded merchants, but does the change in MCC affect it?

CardUp isnt mentioned as well.

[…] covered the broad strokes of these changes yesterday, but now that the new T&Cs have been uploaded I wanted to talk about them in more […]

[…] Citi PremierMiles Visa earns 1.2 mpd locally and 2.0 mpd overseas (2.4 mpd from 4 October till 31 December), with up to 7 mpd on Expedia and 10 mpd on Kaligo. The card also comes with two complimentary […]

Do anyone know for sure..? Cos HWZ Excel sheets says “yes” but if anyone knows for sure if buying on Ikea.com gets 4mpd on Citi Rewards Visa..? many thanks…

Went ahead and made online purchase on SG Ikea website using Citi Rewards Visa.. and I did get 4mpd..

[…] Citibank Rewards- 4.0 mpd, max S$12K per annum ($1K a month from 4 Oct) […]

[…] in August, Citibank quietly announced a raft of significant changes to its rewards program that were to take effect from 4 October 2018. To […]

[…] have edged up over time. DBS raised its fee from 1.5% to 1.8% at the end of 2016, and Citibank raised its foreign currency transaction fee from 1.8% to 2% in October this […]

[…] Citibank Rewards- 4.0 mpd, max S$12K per annum ($1K a month from 4 Oct) […]

[…] this is contagious. After HSBC and Citibank announced their intentions to hike foreign currency transaction fees, BOC credit card holders […]

[…] Citi PremierMiles Visa earns 1.2 mpd locally and 2.0 mpd overseas (2.4 mpd from 4 October till 31 December), with up to 7 mpd on Expedia and 10 mpd on Kaligo. The card also comes with two complimentary […]

[…] Citi PremierMiles Visa earns 1.2 mpd locally and 2.0 mpd overseas (2.4 mpd from 4 October till 31 December), with up to 7 mpd on Expedia and 10 mpd on Kaligo. The card also comes with two complimentary […]

You mentioned ” Citibank still has its One Bill facility where you will be able to earn reward points when making payment to selected billing organizations which include Insurance, Utilities and Town Council payments through the One Bill facility.” But I can’t seem to find any information from Citi that says one bill payments still get miles (e.g Prudential is one of the billing organisations available)

Is that statement still true?