Citibank has been putting some major marketing spend behind Citi PayAll of late. We recently saw some great deals, in the form of a 1% fee for existing customers, two fee-free payments for new customers, and some S$100 GrabFood vouchers thrown in for good measure.

And now, they’ve rolled out an almost impossible-to-lose promotion that’s perfect for income tax season. Citi cardholders can now earn 2.5 miles per S$1 spent on Citi PayAll, for any type of payment up till 31 August 2021. If you’re a first-time PayAll user, you’ll get an additional S$50 cash credit as well.

It’s almost too good to be true.

Earn 2.5 mpd on Citi PayAll transactions

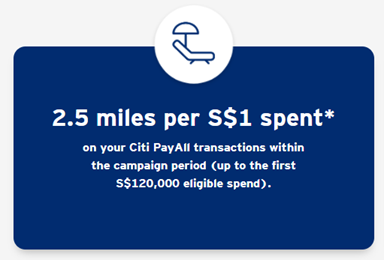

From 1 May to 31 August 2021, eligible cardholders will earn a flat 2.5 mpd on up to S$120,000 of Citi PayAll transactions with the following cards:

| Card | Earn Rate | Cost Per Mile @ 2% |

Citi ULTIMA Citi ULTIMA |

2.5 mpd |

0.8 cents |

Citi Prestige Citi Prestige |

2.5 mpd |

0.8 cents |

2.5 mpd |

0.8 cents |

|

2.5 mpd |

0.8 cents |

The Citi app will (unhelpfully) show the regular earn rate of 1.2-1.6 mpd by default, but don’t worry- the bonus miles (the difference between 2.5 mpd and your card’s regular earn rate) will be credited within 10 weeks from the end of the promotion period, i.e by 9 November 2021. The full T&C of this offer can be found here.

What’s particularly awesome about this deal is that Citibank is offering the same rate across all three eligible cards. You’ll earn 2.5 mpd, regardless of whether you’re using the Citi ULTIMA, Prestige, PremierMiles or Rewards. How’s that for egalitarian?

There’s no need to set up a recurring payment scheme, or meet any minimum number of transactions. Any payment made within this period will earn 2.5 mpd, as simple as that.

As a reminder, Citi PayAll currently supports the following types of payments:

|

|

There’s also a handy category of “miscellaneous payments”, which includes renovations, wedding expenses, storage, charitable donations, parking fees, domestic helper service fees etc. It’s basically a catch-all, and really, I don’t think they’re too fussed about what exactly you pay (so long as it’s not a mortgage repayment, crypto or gambling related transaction).

While there’s nothing stopping you from getting a friend or family member to invoice you for services rendered (love and affection ain’t free, y’know), do remember that there could be tax implications. After all, an invoice is evidence that one party has earned income from the other, and a person is liable to pay income tax if his/her collective earnings exceed S$20,000.

The most obvious use case for this promotion would be income tax payments. This 2.5 mpd offer makes Citi PayAll the cheapest way of paying your taxes by far (the next cheapest option costs ~35% more!), and if you hold one of these cards, it’s a no-brainer. Heck, even if you don’t have one now, you should at least get the Citi PremierMiles Card (first year free) and use it to make payment.

New customers: Get S$50 extra cashback

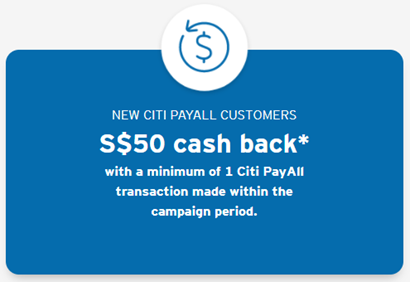

Cardmembers who have never made a Citi PayAll transaction prior to 1 May 2021 will receive a one-off S$50 cash credit when they complete at least 1 Citi PayAll transaction by 31 August 2021.

There’s no minimum amount that needs to be paid, so seriously, there’s no reason not to jump on this. If you’re in the market to buy miles, a S$50 cash credit is equivalent to free miles on a payment of up to S$2,500. Even if you’re not looking to buy miles, a simple S$1 payment to IRAS would be enough to trigger S$50 cashback.

Is it worth it?

Without a doubt, yes.

Buying miles at 0.8 cents each, even in the current pandemic situation, is an incredible offer. Remember, you’re not just buying KrisFlyer miles; Citibank points can be transferred to 11 different frequent flyer programs, including some with great sweet spots like Etihad Guest, British Airways Executive Club, and Turkish Miles&Smiles. Even the newly-revitalised Qatar Privilege Club might be a good bet.

| 💳 Citibank Transfer Partners | |

|

|

|

|

| For a full list of transfer partners, refer to this article | |

Assuming you opt for plain vanilla KrisFlyer miles, it’s easy to get >0.8 cents per mile when redeeming them.

| Redemption Option | Value per mile | |

| ✈️ | Award flights | 2-6 cents |

| 🏨 | Shangri-La Golden Circle conversion | 1.4 cents* |

| ✈️ | Pay for flights with miles | 1.02 cents |

| 🚘 | KrisFlyer vRooms | 0.8 cents |

| 🛍️ | KrisShop | 0.8 cents |

| 🏬 | CapitaStar conversion | 0.7 cents |

| 📱 | Kris+ | 0.67 cents |

| ⛽ | Esso Smiles conversion | 0.33- 0.67 cents |

| *Assumes you have GC Jade/Diamond status and use points for F&B at 10 GC points= US$1.25. If you’re a regular member, 10 GC points= US$1, i.e 1.1 cents/mile | ||

Conclusion

There’s very little to dislike about this Citi PayAll offer. 0.8 cents per mile is an extremely competitive rate for buying miles, the mechanics are simple, and the ceiling of S$120,000 is more than sufficient for most peoples’ needs.

It seems to me like Citibank is determined to dominate the payments space, and with rates this low, it’s hard to justify going any other route. I’m certainly going to make a few ad-hoc payments to IRAS, in an attempt to diversify my mileage collection.

Hi Aaron,

Can I check if Premiermiles and CRV points stack?

Thanks!

Citi does not pool points

A word of warning: The rebates for the last Citi Payall promotion which ended in February were supposed to be credited by April but are still not in. So make sure you monitor your accounts.

I haven’t got it either. Did you follow up with Citibank and get it? I’ve been meaning to contact them but wasn’t sure when the cashback was due. I just read the T&Cs – it is 8 weeks from 28th February. Which as you say is the end of April. Oh well time to contact them and complain. Geez banks are slippery. Miles and cashback all randomly seem to go missing unless you hold them to account.

Someone in the Milelion Telegram Prestige group apparently called and Citi confirmed this would be solved by Friday 7th. Fingers crossed.

I’ve still got nothing – i’ll chase too.

Hi isn’t the $400 rebate supposed to be due 30 June 2021? I am waiting for the $100 grab voucher this Friday.

Hi Aaron,

Sorry for the basic question – does $1 spend = 2.5 Citi Miles = 2.5 SQ/CX/TK/BA/QR miles?

It’s the Citi Miles –> KrisFlyer/AsiaMiles etc conversion that I’m not sure of, and the Citi website is not exactly user-friendly.

Thanks in advance!

All the same ratio yes

a simple S$1 payment to IRAS would be enough to trigger S$50 cashback. = will it trigger call from IRAS ?

Why? They only care if you overpay your noa

thanks will test, it seems minimum 5$

Shame the Singapore PayAll promotion isn’t as good as the Australian PayAll promotion. Currently there is a 0% fee for all PayAll transactions there including tax payments. I’d prefer to get 50,000 miles on my tax payment for free rather than 105,000 miles for a 2% fee. Oh well I got plenty of free tax payment miles last year via Citi->Grab->AXS.

interesting to know they’re making a global push on this! thanks for sharing.

Do I need to cancel and re-create a recurring transaction to make use of this?

0.8 cents per mile, assuming 25k business class redemption one way from SIN-HKG, that’s only $200 a ticket? Is my maths off?!

Yes but only if you have a $10,000 expense/bill to pay

Or you can pay $10,000 to your family member and then use the same money to pay of the credit card bill plus $200. I don’t think IRAS can consider that a legit income – after all you are just “outsmarting” the bank and not doing anything illegal. My 2 cents worth.

Does anyone else have any data points to share on the below?

Aaron says that it is egalitarian with all 3 cards earning same mpd, but I thought in the previous year my prestige still earned relationship bonus points including on payall spend? Otherwise I don’t know how I got so many relationship bonus points as I didn’t really pass a lot of spend through my prestige last year.

If that’s true then prestige > PM (no idea if ultima has an equivalent scheme)

yes, you will still earn a relationship bonus with prestige on payall spending.

Even if you’re not looking to buy miles, a simple S$1 payment to IRAS would be enough to trigger S$50 cashback.

-> How does the cashback work? If you did S$1 payment wouldn’t that be just 2% ($0.02 cashback)?

Do I have to spend $2,500 to get $50 cashback (2%)?

Do we have to cancel current scheduled recurring payments and set up a new payment? Like the grab promo?

Also I have yet to receive the grab vouchers promo. Wonder if we need to chase citi ourselves?

Yes I believe so. If you read the T&C. It specifically states that

1. The application date aka the date you apply for the Payal transaction AND

2. The payment date

Must fall in the promo period.

Made a tough decision to cancel my previous transaction with the grabfood vouchers promo and apply for this one instead

Excellent deal – thanks! Have similar issues as others have voiced above with the prior Citi PayAll promos not showing up yet. Btw., I didn’t get any invite/info on this one. It’s open to any cardholder of the three eligible cards, right? I.e. no sign-up, etc. necessary.

Yes, it’s not targeted

Hi Aaron,

How would the tax implication come about, via a tax audit?

Will Citibank be reporting the type of payments made to which party to IRAS?

Thanks!

i dont know what citi does and does not report. all i know is that you’ll create a paper trail, and it’s always unwise to cheat the taxman.

You know what, I made a huge amount of income tax payment via PayAll on April 21… unacceptable.

Hi Aaron,

Im planning to transfer abt $10k to my parents account via ibanking. If i use citipayall instead :-

1. Will it be eligible for the bonus?

2. Will they be taxed?

Appreciate your oponion on this.

citi payall does not allow for peer to peer fund transfers. the only way to do this is to have your parents invoice you for something, i dunno, rent. in that case, it will be subject to tax if their total taxable income exceeds $20k

Does it apply to citi rewards card too?

Yes it does.

not originally, but the citi rewards card was belatedly added

Hi Aaron, is there anything preventing me from using my Citi card to pay for my wife income tax through Citi PayAll ?

by right you can’t, by left…

I love your posts and actually used PayAll for the first time because of this one only to be disappointed by Citibank’s customer service team. They’ve somehow used my points to redeem against card payment and can’t provide me details or evidence of how that’s happened and keep wasting my time. No response over email either. Just chats and calls. Quite frustrating.

Hi, I had same experiences with Citibank CSO recently. Their replies show that they either don’t understand simple English or are so dyslexic that they cannot comprehend the questions asked or simply chose to ignore what they find inconvenient to answer or all the above. They probably hope that you give up after all the hassle. I supposed that is the price of chasing miles – you got to let go sometimes before they cause you serious health issues. :))

I see that cannot set up recurring payment for income tax. Would I be able to set-up multiple payments then?

you can set up as many payments as you wish!

Is this still a good idea when counting the Citi Pay All 2% fee? I don’t see that factored in anywhere?

Hi all, new to this here. How is the cost per mile of 0.8 cents calculated? Thanks!

2% fee, 2.5 mpd. spend $1, pay 2 cents, get 2.5 miles. cost of 1 mile= 2/2.5=0.8

With the 2.5miles citipayall promotion expired now, is it still worth it to purchase the miles at 1.66cpm? (Citipremier)

Anyone got the extra points yet?

Not yet…I think they are really going to make us wait until Nov 9 to give them to us

I did (last week) and pending for the 50$ cashback. Should be posted next week

Anyone received the bonus point yet ? I have not received mine..

the bonus miles (the difference between 2.5 mpd and your card’s regular earn rate) will be credited within 10 weeks from the end of the promotion period, i.e by 9 November 2021

my bonus points came in on 29th Oct…

Yeah, received on 5th Nov / in the Nov statement