If you have an income tax bill with IRAS, I certainly hope you have a GIRO payment arrangement set up too.

There’s absolutely no reason not to. IRAS is allowing you to spread your tax bill over 12 monthly instalments, with no interest, freeing up cash for other expenses or investments.

At the same time, however, there are lots of promotions for earning miles on ad-hoc or recurring income tax payments via platforms like CardUp or Citi PayAll. That raises a commonly asked question:

If I make an ad-hoc or recurring income tax payment while on a GIRO plan, will I suffer a double deduction?

It’s a valid concern— after all, the whole point of GIRO is to free up cashflow. A double deduction would undermine the benefit of earning miles.

Fortunately, the answer is no. There won’t be any double deduction, provided you time your payments right.

How do GIRO arrangements with IRAS work?

Setting up GIRO

Setting up GIRO for income tax can be done instantly via myTax Portal for the following banks:

|

|

If you don’t have an account with any of these banks (e.g. Trust Bank), you’ll need to submit a request for a manual GIRO form, which will take up to three weeks to process.

Once your GIRO arrangement has been approved, you can view the monthly instalment by logging in to myTax Portal, selecting Account > View GIRO Plan > View

GIRO deductions

Income tax is normally payable one month from the date of your tax bill (aka Notice of Assessment/NOA).

However, if you opt for a GIRO payment arrangement, IRAS will spread your liability over 12 months, in interest-free instalments paid from May of this year to April of the following year.

| ❓What if I join GIRO mid-way? |

| If you join GIRO after May, the instalment deduction will commence in the month after your GIRO application is approved and end in April of the following year. |

- Deductions take place on the 6th of each month

- If the deduction is unsuccessful, a second attempt will be made on the 20th

- If the date of deduction falls on a weekend or public holiday, the deduction will be made on the next working day

- GIRO will be automatically cancelled after two consecutive months of failed deductions (i.e. four failed deductions in a row)

- If your GIRO arrangement is cancelled, the remaining balance automatically becomes due immediately

In other words, don’t mess about with your GIRO plan. Cancelling it accidentally means you lose the benefit of the interest-free period!

| ❓Why are my instalments unequal? |

|

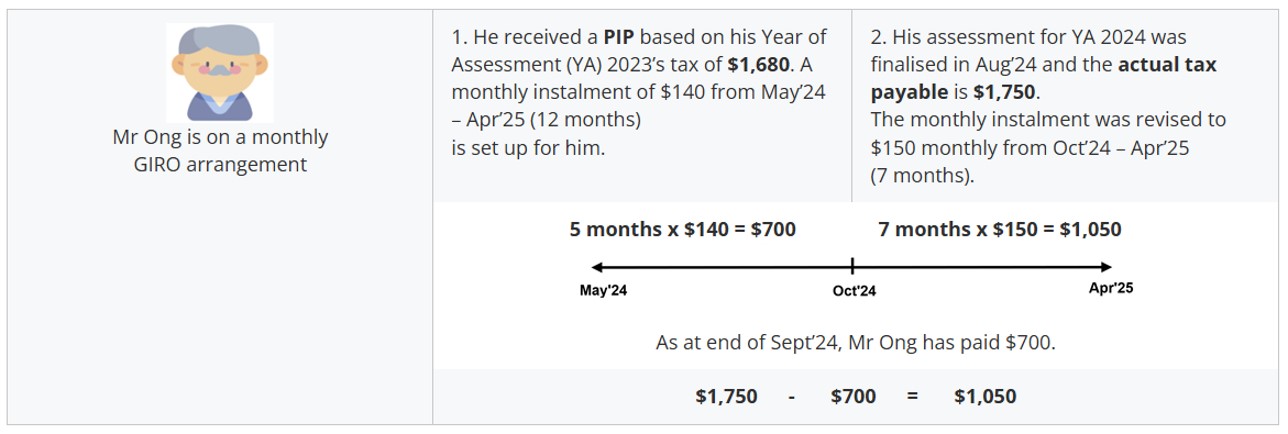

GIRO deductions for personal income tax commence from May, but IRAS needs time to calculate your income tax liability. Therefore, a Provisional Instalment Plan (PIP) will be prepared based on your previous year’s taxes (basically the previous year’s instalment amount). This will be deducted each month until your finalised tax bill is ready, after which the monthly instalments will be revised based on the actual tax payable. Excess payments, if any, will be automatically refunded when the final tax bill is ready. IRAS provides the following example:

|

Making manual payments while on GIRO

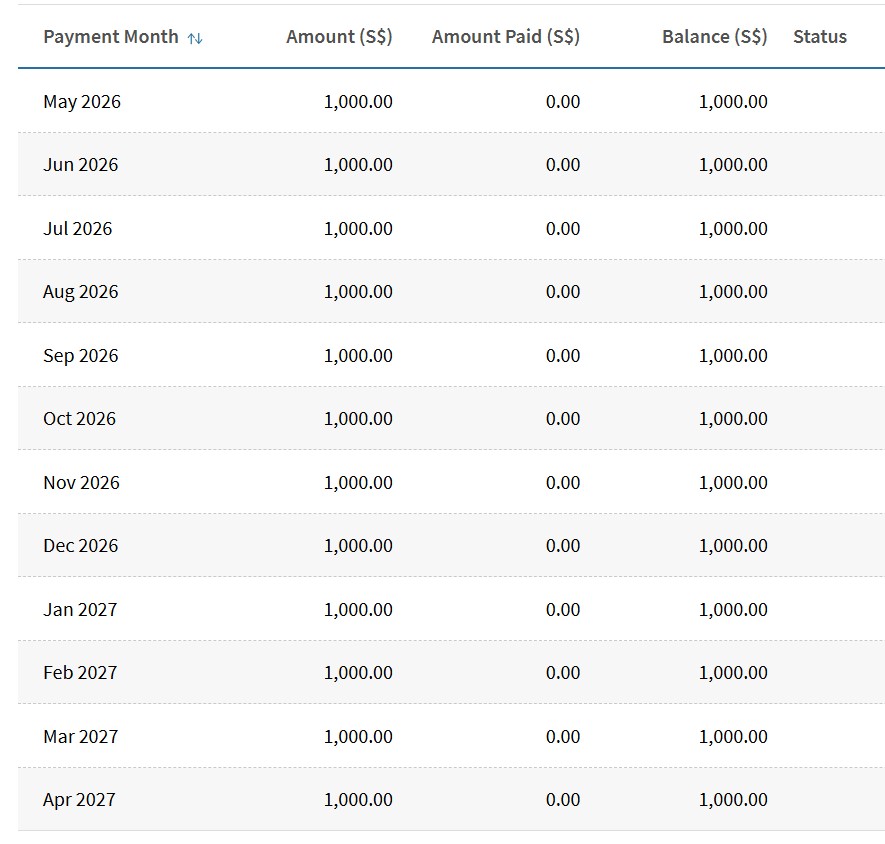

Suppose you have a tax liability of S$12,000, and apply for a GIRO payment arrangement. IRAS will split your bill such that S$1,000 is owed each month.

Without any ad-hoc payments, this is what the schedule should look like.

| Month | GIRO | Balance |

| Total Tax Due= S$12,000 | ||

| May 2026 | S$1,000 | S$11,000 |

| Jun 2026 | S$1,000 | S$10,000 |

| Jul 2026 | S$1,000 | S$9,000 |

| Aug 2026 | S$1,000 | S$8,000 |

| Sep 2026 | S$1,000 | S$7,000 |

| Oct 2026 | S$1,000 | S$6,000 |

| Nov 2026 | S$1,000 | S$5,000 |

| Dec 2026 | S$1,000 | S$4,000 |

| Jan 2027 | S$1,000 | S$3,000 |

| Feb 2027 | S$1,000 | S$2,000 |

| Mar 2027 | S$1,000 | S$1,000 |

| Apr 2027 | S$1,000 | – |

Now let’s imagine that in the middle of June 2026, you decide to make an ad-hoc payment of S$400. After taking into account the May 2026 (S$1,000) and June 2026 (S$1,000) instalments that have already been paid, the amount owed to IRAS now stands at S$9,600 (S$12,000 – S$1,000 – S$1,000 – S$400).

| ⚠️ Direct vs indirect payment facilities |

|

In this section, I’m assuming you’ve decided to use a direct payment facility, which makes a transfer to IRAS on your behalf. If you’re using an indirect payment facility, your GIRO arrangement is unaffected because there is no actual payment made to IRAS (instead, money is deposited into your designated bank account, and you’re responsible for paying IRAS).

|

According to the payment schedule, the remaining balance after July’s GIRO payment is supposed to be S$9,000. Therefore, the GIRO deduction for July 2026 will be automatically adjusted to S$600, to keep the payment schedule on track.

| Month | GIRO | Balance |

| Total Tax Due= S$12,000 | ||

| May 2026 | S$1,000 | S$11,000 |

| Jun 2026 | S$1,000 | S$10,000 |

| Ad-hoc Payment: S$400 |

S$9,600 | |

| Jul 2026 | S$600 | S$9,000 |

| Aug 2026 | S$1,000 | S$8,000 |

| Sep 2026 | S$1,000 | S$7,000 |

| Oct 2026 | S$1,000 | S$6,000 |

| Nov 2026 | S$1,000 | S$5,000 |

| Dec 2026 | S$1,000 | S$4,000 |

| Jan 2027 | S$1,000 | S$3,000 |

| Feb 2027 | S$1,000 | S$2,000 |

| Mar 2027 | S$1,000 | S$1,000 |

| Apr 2027 | S$1,000 | – |

In other words, making a manual payment does not trigger a recalculation of the remaining instalment amounts. As far as IRAS is concerned, the instalment amount is decided at the point of GIRO approval, and in this case you owe S$1,000 per month, period.

Then suppose the following month, you’re feeling generous and want to make an ad-hoc payment of S$3,400, which reduces the balance owed to IRAS to S$5,600 (S$12,000 – S$1,000 – S$1,000 – S$400 – S$600 – S$3,400).

When August 2026’s deduction comes round, IRAS looks at the amount you should owe as of this date, per the original payment schedule: S$8,000.

Your actual balance is less than this, so IRAS basically says “you’re good,” and does not trigger a GIRO deduction for August 2026. The same repeats in September 2026 (when your scheduled balance should be S$7,000) and October 2026 (when your scheduled balance should be S$6,000).

But come November 2026, when your scheduled balance should be S$5,000, IRAS will trigger a S$600 payment to put you back on schedule.

| Month | GIRO | Balance |

| Total Tax Due= S$12,000 | ||

| May 2026 | S$1,000 | S$11,000 |

| Jun 2026 | S$1,000 | S$10,000 |

| Ad-hoc Payment: S$400 | S$9,600 | |

| Jul 2026 | S$600 | S$9,000 |

| Ad-hoc Payment: S$3,400 | S$5,600 | |

| Aug 2026 | – | S$5,600 |

| Sep 2026 | – | S$5,600 |

| Oct 2026 | – | S$5,600 |

| Nov 2026 | S$600 | S$5,000 |

| Dec 2026 | S$1,000 | S$4,000 |

| Jan 2027 | S$1,000 | S$3,000 |

| Feb 2027 | S$1,000 | S$2,000 |

| Mar 2027 | S$1,000 | S$1,000 |

| Apr 2027 | S$1,000 | – |

So the basic logic is:

- If ad-hoc payment < upcoming instalment, IRAS will deduct the difference in the upcoming instalment

- If ad-hoc payment = upcoming instalment, IRAS will skip the upcoming instalment

- If ad-hoc payment > upcoming instalment, IRAS will skip the upcoming instalment, and skip/adjust future instalments based on the original payment schedule

Watch the dates!

In the previous section, I’ve assumed that your ad-hoc payment reaches IRAS in time to avoid a double deduction.

A double deduction happens when your ad-hoc payment reaches after IRAS has sent GIRO debiting instructions to your bank.

For example, let’s say you make an ad-hoc payment of S$1,000 on 3 December 2026. However, this is too close to the GIRO deduction date, and IRAS has no idea you did this. It therefore bases its 6 December 2026 deduction instructions on the assumption that it needs to reduce your current S$5,000 balance outstanding to S$4,000, and triggers a S$1,000 deduction from your bank account nonetheless.

| Month | GIRO | Balance |

| Total Tax Due= S$12,000 | ||

| May 2026 | S$1,000 | S$11,000 |

| Jun 2026 | S$1,000 | S$10,000 |

| Ad-hoc Payment: S$400 | S$9,600 | |

| Jul 2026 | S$600 | S$9,000 |

| Ad-hoc Payment: S$3,400 | S$5,600 | |

| Aug 2026 | – | S$5,600 |

| Sep 2026 | – | S$5,600 |

| Oct 2026 | – | S$5,600 |

| Nov 2026 | S$600 | S$5,000 |

| Ad-hoc Payment: S$1,000 (misses GIRO cut-off) | S$4,000 | |

| Dec 2026 | S$1,000 | S$3,000 |

| Jan 2027 | – | S$3,000 |

| Feb 2027 | S$1,000 | S$2,000 |

| Mar 2027 | S$1,000 | S$1,000 |

| Apr 2027 | S$1,000 | – |

Therefore, your outstanding balance with IRAS is now S$3,000.

Assuming no further ad-hoc payments, IRAS will skip the January 2027 deduction and only resume debiting from February 2027.

To prevent this from happening, make sure any ad-hoc payments reach IRAS before they send debiting instructions to your bank! However, we don’t know for sure when that happens. Some say it’s the last day of the month prior, but I can’t find any official source to confirm.

So my advice is to make any ad-hoc payments at least 1 week before the end of the month. If you’re using CardUp, a safeguard has already been built into the system which disallows tax payments in the last week and first week of each month.

CardUp 11 month limit

If you’re paying taxes through CardUp, do note that you can only set up 11 months’ worth of payments and not 12.

This is because IRAS requires that the first payment of each new tax cycle is deducted through GIRO, to ensure it remains active and valid. You can read more about this here.

Earning miles on income tax

To learn more about the best credit cards for earning miles on income tax, and the various payment promotions, be sure to check out my detailed guide below.

2026 Edition: How to earn credit card miles on IRAS income tax

Conclusion

A GIRO arrangement for personal income tax allows you to take advantage of interest-free instalments, and avoid the pain of a lump sum payment. Even better, you can still make additional payments via platforms such as CardUp and Citi PayAll, to take advantage of cheap miles promotions.

Just make sure these payments reach IRAS before the last week of the month prior. Cut it too close, and you may end up being hit with a double deduction— which doesn’t mean you lose money as such, just that you’re paying off your tax bill faster than you’re obligated to.

this was EXACTLY the question i had. thanks for clarifying it!

I’m not sure if this is right . For ad-hoc payment > upcoming instalment , next month iras continued with the same monthly instalment . The reduction of taxes only comes in the final months . Ie if u paid 3 months in advance the reduction only applied to final 3 months

Nope, if you pay sufficiently in advance the upcoming instalment is reduced

Hi checking if this is still the same process on adhoc payments?

So hang on: In order to earn miles with CardUp, does this mean we would have to: (1) set up a giro between IRAS and our bank, e.g. Citibank, for $12,000 to be deducted over 12 monthly instalments à $1,000 each, and then… (2) Manually initiate a CardUp payment every month, say 2 week prior to the Giro deduction date, for $1,000 each month… …so that we can benefit from earning miles via CardUp? Did I understand the actual mechanics of the miles earning part correctly? Or how would we otherwise be able to earn miles and spread our cash-flow… Read more »

Is this still valid? Cardup says you need the first month to be deducted from GIRO and they will only pay from the second installment, otherwise the GIRO gets cancelled.

Would be good to shed some light on this. Is the issue due to paying too early, or too much?

Oh dang, I just cancelled my GIRO last night due to paying partial tax with PayAll. If only I’ve seen this article earlier..

Adhoc payment should be made before 25th of the giro deduction month.