Since discovering the Miles and Points game 3 years ago, Jeriel has now spent a disproportionate amount of time reading the T&Cs of credit cards and frequent flyer programs. His grand plans for round-the-world premium travel has taken a hit since the arrival of his daughter, but he is still determined to fly as far, frequently and luxuriously as possible on Miles and Points. Expect more family-orientated trip reports and travel tips from him!

The HSBC Advance Visa Platinum – Worth the Hassle?

.png)

If you are just starting out on this miles and points endeavour, you’d soon realize that juggling a portfolio of >10 active cards (and even more inactive sock drawer cards) may start to get a little confusing. Each card usually has 1 or 2 specific uses, and some of these uses may overlap with each other. Perhaps the most frustrating aspect is trying to explain to and convince your spouse to adhere to the myriad of ‘rules’ of the game.

To be successful, it is essential to have a good game-plan; a streamlined strategy.

The optimum strategy minimizes the number of cards one has to carry on a day to day basis, and limits the decision making process at the point of sale to 2, if not 3 steps maximum. All this, while maximizing the number of miles or points earned.

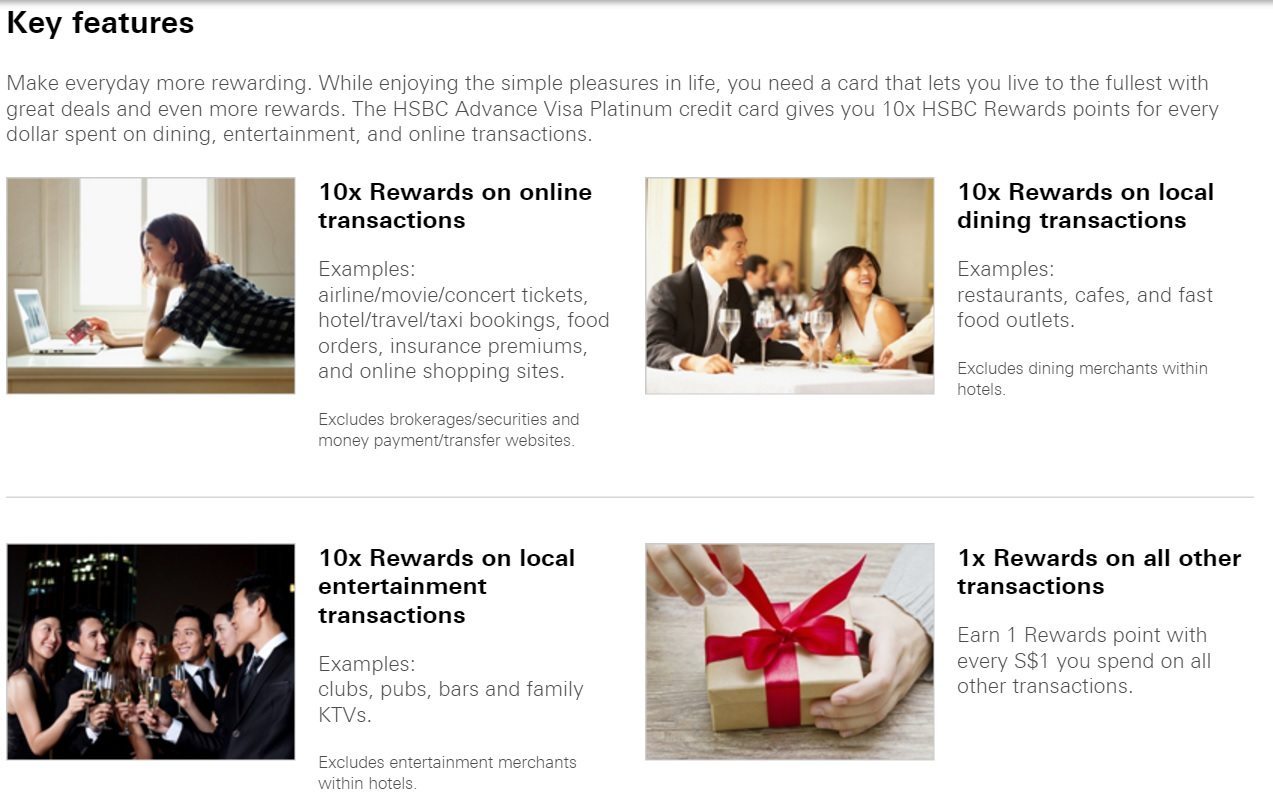

There is no one-size-fits-all solution, and best strategy for you entirely depends on your spending patterns and habits. However, it is obvious that you should try to find a card which offers the maximum rewards bonus (in Singapore, this will generally be 10x rewards points, usually equivalent to 4 miles per dollar spent) for the most number of spending categories.

Well, the HSBC Advance Visa Platinum (AVP) seems to fit the bill perfectly.

Aaron had briefly touched on this card awhile back in his article on Dining cards in Singapore. Yes, the HSBC AVP does award 10x points for all dining spend (based on merchant coding) in Singapore. However, the 10x point bonus also applies to online spending, and spending on merchants with entertainment listed as their main business.

Features (with the main exclusions) of the HSBC AVP Card.

Of course, they come with certain exclusions, the main ones listed in the extract from HSBC Singapore’s website above. For the exact terms and conditions, they can be found here. But all things considered, this seems pretty generous.

For starters, there is no mention of a spending cap for online spend, which expressively includes airline and hotel purchases, and even insurance payments. EZ-link/Transitlink transactions do have a cap of S$200 a month, but that is the only exception. Buying airfare and accommodation for your whole family, or perhaps an S$20,000 round-the-world business class ticket? No sweat. This is in contrast to the other options – DBS’ Women’s World MasterCard has online spend capped at S$2000 a month, and DBS’ Altitude Series only gives 3 miles / dollar and has a cap of S$5000 a month (from 1 June onwards).

Secondly, the AVP seems to be a potential successor for the now dead (?) UOB Preferred Platinum Amex. It has similar terms to the UOB PPAmex, awarding 10x points based on the MCC of the establishment. Of note, this only applies to local dining, as opposed to worldwide dining for the UOB PPA.

If you are the chiongster kind, or frequent pubs often, the bonus points for entertainment will come in handy as well. No free club entry, 1-for-1 drinks or similar perks, but I’d take more points over rewards-in-kind any day.

To top it off with a cherry on top, annual income requirements are ridiculously low at S$30,000 p.a. for Singaporeans and PRs, and S$40,000 p.a. for foreigners. Not forgetting the perpetual annual fee waiver as well. A bit of a moot point given that an annual fee waiver is usually just a short phone call away, but it does save you that 5 minutes of annual irritation. 😀

Now we get to the interesting part. What is the catch? Simple, you’d have to be a HSBC Advance Account holder first.

The HSBC Advance Account is something like an entry-level preferred banking account with HSBC. The Relationship Balance requirement (bank parlance for amount of money you park with them) is a princely sum of S$30,000. (For home mortgage account holders with HSBC, your initial loan quantum must be at least S$200,000). This is in contrast to other banks’ preferred banking programs (including HSBC’s own Premier Banking) which usually require a Relationship Balance requirement north of S$200,000. In return for maintaining this S$30,000 with them, you get the following perks;

HSBC Advance Account Perks

What you’re done reading that already? Sorry, I must have fell asleep. Yeah, nothing much exciting there.

TL;DR – Park S$30,000 with HSBC and you get the HSBC AVP Card.

Unless you already have a qualifying Relationship Balance with HSBC, the million dollar question (or in this case, the $30k question) naturally will be – is the hassle (going through all that bank admin) and opportunity cost of parking S$30k with HSBC worth getting the card?

The answer, without fail, is that it depends.

I have been eyeing this card for about half a year now, and am still yet to take the plunge. Let me share a few of my reservations.

- Money, Money, Money

Do you even have S$30k lying around? Obviously not an option if your savings are still non-existent, or if you need the cash eminently for some massive spending.

- Opportunity Cost

If you have S$30k lying around, why do you have S$30k lying around?! It is certainly not a small sum of money and instead of lying in a bank doing nothing, it could be (and should have been) put to work earning you some interest in a fixed deposit (if you are risk-adverse) or flipping some profits in the stock market.

- Better Options?

I already have the UOB Preferred Platinum Amex for dining, and between the DBS Women’s World MC, DBS Altitude, UOB Preferred Platinum Visa and Citibank Rewards series, my online purchases are almost completely covered. Do I really need another card?

- Lack of Good General Spend HSBC Card

A big part of miles and points strategy is trying to consolidate your points earned into as little banks as possible so that you don’t end up with ‘orphan’ miles or points – a negligible balance of points in an obscure bank not worth paying the transfer fee for. Having an equal number of points spread across all 5 to 6 banks isn’t wise as well, as you’d end up paying 5 to 6 different transfer fees to convert them to usable miles. These can add up to a significant amount. Bulk of my points are with DBS and UOB because of their solid general spend cards (the DBS Altitude and UOB Prvimiles Card respectively). Will adding HSBC to the fray complicate matters unnecessarily?

Of late, I’ve found myself running out of excuses to not get this card though. Let me refute my own arguments.

- Money, Money, Money

S$30k may be hard to come by, but HSBC does provide a grace period to hit the minimum Relationship Balance. If you credit your monthly salary (minimum of S$3750/month) or make a recurring monthly deposit of at least S$2500/month, you will be given a 24 month grace period to hit the required amount.

Even if you don’t want to change the account your salary is credited to now, setting up a recurring transfer isn’t too much of a hassle. Correct me if I’m wrong but I don’t see any clause prohibiting you from transferring that S$2500 right back, so at the very least you get to use the card for 24 months. 😀

- Opportunity Cost

Most financial planners would advocate you setting aside a sum of money in cash or liquid assets (usually a few months’ worth of expenditure) as an emergency or rainy day fund. In addition, it is also generally prudent to spread your investment portfolio across a spectrum of high to low risk products.

HSBC does have a portfolio of Timed-Deposit products, and also run occasional promotions which are worth taking a look at. The current promo runs till 31st May and offers a 1.5% p.a. interest for a 7-month timed-deposit for HSBC Advance account holders. These investment options are worth taking a look at.

Disclaimer: I am in no way a qualified or trained financial advisor; the above represents my own personal views on money management and investments, and do not constitute financial advice. I also do not have any vested interest in HSBC in any way.

- Better Options?

The UOB Preferred Platinum Amex is a great card for dining, but it does irritate me sometimes. It is no secret that in Singapore, Visa is accepted at a greater number of merchants than Amex. Also, the rule which divides points earned on UOB cards into blocks of S$5 is probably negligible in the grand scheme of things, but frustrates me to no end when the bill for my meal ends up being something like S$39.99.

There are many cards for online spend, but in practice, many of them impose many restrictions on what qualifies for the bonus 10x points. The DBS Women’s World MC is well known for being the most inclusive, but it has a monthly cap of S$2000. How inclusive is HSBC’s policy? I do not yet own the card and it is difficult for me to deliver a verdict, but here is where the collective experience of the internet can be very helpful.

- Lack of Good General Spend HSBC Card

You’d really only need one good general spend card, and if you plan your expenses well, you usually shouldn’t even need to use your general spend card much. If HSBC can replace either DBS or UOB as one of my main points accounts, then this is definitely a card worth getting despite the lack of a good general spending or traditional ‘miles’ card.

In conclusion, I am tending towards replacing UOB with HSBC as one of my 2 main points accounts. The HSBC AVP can very potentially replace both cards in the UOB Preferred Platinum series.

What do you think? Do you already own the HSBC Advance Platinum Visa Card? What is your experience with the inclusions and exclusions of the dining, online and entertainment categories? Do share in the comment section below!

Hey thanks for the writeup! To sum it up..

For the online spending portion:

The HSBC AVP card is the same as DBS Woman’s Card, just that the AVP card has no cap, and DBS Woman’s Card has $2000 monthly cap?

To give the HSBC AVP the ‘general spend’ benefit, you just need to use AVP card to top up Pre-paid Fevo card ($1=4miles), and spend on your Fevo card yea? 😀

yeah that’s basically jeriel’s point. it’s the DBS woman’s card without the $2k monthly cap. I ignored this card for a long time because I assumed it was ma fan to get. then spent $20k on a RTW ticket. then realised I could have 80,000 miles now if I had the hsbc advanced. then got pissed.

omg.. seriously boy. OK, i need to know more about this card now!!

Hey wait… I think the Fevo card trick might not work with HSBC AVP card. AVP states ez-link card top up is maxed at 200/month only. And top-ups of FEVO is paid to Ez-link company.

So seems like WWMC is still better than AVP for the fevo card trick yea.

Hey as mentioned in the article, there appears to be a cap of S$200 for certain top ups. ‘All transactions relating to Ezlink or Transitlink. (I didn’t wanna you know, spell it out so obviously ?)

So in short, no general spend benefit sadly unless you spend less than $200 a month

I got this card a few months ago, and it’s fast becoming one of my most used cards. One caveat though. Technically, there is still a monthly cap, which is your credit limit. Ordinarily, with most cards that’s not an issue, but it seems that HSBC is very conservative with this. In my case, they were only willing to give a limit which was about third of what other banks gave me.

I’ve experienced this as well. They are really VERY conservative… like giving me a monthly credit limit that is 1/3rd of my monthly salary…

I had actually got a limit that is 4 times of my salary.

To add on, they are also very conscious about security. I tried booking tickets on the Air Canada website, and the transaction was rejected. Few minutes later, I got a call from the bank asking me if I tried to use my card on the Air Canada website. I said yes, and they said ok and asked me to try again in a few minutes. Another example. I had to apply and pay for electronic visas for me and my family. This had to be done online, and I had to apply and pay for each one separately. The first… Read more »

Interesting input, thanks Jon!

In general though the points have come through for your online spend? Dining as well?

To me the HSBC AVP is a candidate to replace the UOB PPA, but not the DBS WWMC

Sorry. I asked this once but I am still confused and might be missing something. Eligibility is stated on this link https://www.hsbc.com.sg/1/2/hsbc-advance/apply-now There is an ‘or’ statement which seems to mean as long as any requirement is met – the individual is eligible. That said, the preceding line said it is for waiver of the $10 monthly charge. Where do we see that clause that says individuals must park 30k with them? I do have a mortgage with them over 200k initial, so I don’t know if I qualify for it purely based on that alone. This will be a… Read more »

For the avoidance of doubt, transactions made on brokerage/securities and/or money payment/transfer websites are not classified as retail transactions and are expressly excluded.

saw this on the t n c. Anyone able to confirm they got the 4miles from topping up the FEVO cards.?

Thanks

Heya! Tried to do some math – let’s see if this makes sense. I’m working on maintaining the $30k requirement – not in love with the idea of setting it up with the intent of closing it after 2 years. Taking into account opportunity cost from not parking that sum with OCBC 360 (I’m not even maxing that – just 1.75% at the moment) 1.75% or $30k = $525 (effectively an annual fee) 2c per mile – 26250 miles 2.8miles/dollar more than usual 1.2miles/dollar general spend cards 26250 / 2.8 = 9375 I will only ‘break even’ after spending $9375.… Read more »

You need a $30k relationship with HSBC, so you could put your $30k in a short term (or even long term) fixed deposit. The latest promo was 1.5% pa for 7 month term. That’s only marginally (0.25%) worse off than your OCBC 360

but the T&C says: The programme period for the 10x HSBC Rewards points programme ends on 31 December 2016 or such other date as may be determined by HSBC at its sole discretion….

i’m not surprised really, because I don’t think the program is financially sustainable for them. i guess they’re using it as a loss leader and hoping that people will retain their accounts after that out of habit.

just afraid that one would have accumulated some miles from the card and would not be able to utilise it.

hence dbs, citibank, uob are still better banks as there have more than two cards linked to one account. even anz might be better as it has the annual 10k miles for annual fee.

There was a period last year where the “promotion” ended and the card was reduced to a worthless piece of plastic for a couple of months until they decided to renew the deal again….

The promotion is supposedly to end this March but they renewed it to December. Though I doubt they will change it after december, but that’s a good point.

I have had this card for over a year now and its awesome. Yes, the FEVO topups are restricted to $200 a month, but everything else online and dining is virtually unlimited (HSBC gave me a $50k+ credit limit so I haven’t hit that in any month). Everything that’s card-not-present counts for 4miles/$. Yes, that includes a Spotify recurring billing subscription. Uber, Grab, Paypal everything. They’re a bit anal about fraud checks compared to other banks, and every month or two I get an email or call after an unusual charge (like a certain south American airline 😉 )to verify… Read more »

thanks savage,

that’s what I thought so too. I would go for it for the dining and online .

general spending would still have to use DBS WWMC plus fevo.

Great data point for the qualifying online spend, thanks!

Hi Savage, what is the name of this savings plan that allows you to earn miles on?

I used this card to buy my engagement ring online. My recommendation is to use it if you have an upcoming big online spending; you get a chunk on miles on this cards so that you can accumulate other spending from dining and transfer it out together.

For the online spending, everything else as long as you go through the visa payment gateway.

everything else except 200 dollar restrictions to ezlink*

Don’t they cap the bonus points earned to your credit limit?

do they? i thought the solution to a low credit limit would be to use your credit card like a prepaid card and “recharge it” by paying off more than your credit limit. EG if your credit limit is $10k, by prepaying $10k of your bill you get a $20k credit limit to earn points on. assuming you work on a reimbursement basis and doing that doesnt put you in financial jeopardy of course…

They had given me a credit limit that is 4 times my salary. Its more than enough for anything.

One caveat is the there is a limit to the number of “bonus points” you can earn per month.

If your credit limit is SGD 10,000, then the maximum number of bonus points is 10,000.

Effectively it’s a $1000 cap in this case.

HSBC also tends to be very conservative with it’s credit limits, so to be frank, the only true use of this card is to buy the occasional movie ticket and to top up your EZ Link cards.

I had just gone through the T & C of the card again and did not see any statement that indicate this. Can you copy paste from the T & C on the statement can indicate this?

I think you need to check on your facts sources again; I just checked my account and can confirmed I had earned more than 70k rewards point from April to May, which came from the spending I made on my engagement ring, that’s many times more than my credit limit.

https://www.hsbc.com.sg/1/PA_ES_Content_Mgmt/content/singapore/personal/cards/09/hsbc-advance-visa-platinum/tnc.html#B

13. The 10X HSBC Rewards points earned on qualifying transactions will be limited to the approved credit limit within the qualifying calendar month.

I went down to HSBC to confirm this with one of their employees.

If you’re saying that you made a purchase for $7000~ and got 70k points, and your credit limit is less than 70k, then the employee is wrong.

Either way I’d be happy to be wrong because I just moved my money to HSBC Advance.

That statement seems really ambiguous, i think the credit limit defines here means the 10x is base on top of your credit limit (ie 10k limit allows you to earn 100k points). This statement define here is probably for cases where the consumer request a temporary credit limit increase, and didnt pay off the the bills after the temporary increase period. This statement would make sense then.

I hope Lionel is correct. I fought hard (several sms’ heh) for the UOB PP Amex. The acceptance is quite limited that HSBC AVP has been my go to card for dining now.

Anyone know if you do paywave at a restaurant whether it will still count as dining for the 10X rewards?

Should be counted though I had not verified it. Counted my points few months ago amd havnet notice I had loss any points although I had quite a lot of paywave transaction. The bonus points is awarded base on merchant code, with or without paywave, merchant code stays the same.

Would ez reload via HSBC AVP be considered as online transaction?

theoretically yes, because the server that stores your CC information to use during ATU would have to go through the same visa payment gateway in order to get the top up reflected on your statement account (as oppose having the card insert into a card reader). This is aligned with the criteria for online spending stated in HSBC Advance T & C. I did not check the rewards point manually but in a similar situation, I had been using the same ATU transaction for net flashpay with DBS WWMC for months, last calculated that I had about 99% of the… Read more »

oh? i didnt know nets flashpay would be qualified for 9x!

but with the new WWMC tncs, would the ATU tranx for Nets flashpay be affected by clause 5(i) on “eNets transactions”?

The new tncs does bothers me. I had both DBS Woman card, so I plan to throw in 5 dollars around to check regularly if the points are still awarded. While the T&C is updated, but the back end calculations may had not been changes yet, so will have to monitor a while to confirm this.

Can you apply for the advance card if you have a premier relationship?

Tried this, RM said not possible. Seems to be strictly for Advance account.

Anyone has had to call up HSBC for missing bonus points? I called the customer service hotline but there was no way to speak to a CSO?

I cant find anyway to reach their cso as well.

Just choose the option “to report a lost card”. They don’t seem to know that was the option in the first place. Another option is to repeatedly press # i think. I can’t remember though.

[…] it’s time to consider getting that HSBC Advance […]

“Qualifying Transactions means retail transactions made locally or overseas (including Online Transactions)”

If i go in the mall for a shopping spree, does that constitute retail and so entitles to 10x rewards? If thats the case, it seems like almost everything u pay face to face is retail?

Thanks for clarifying in advance

Does AXS payment count towards online?

You can’t pay AXS payment with VISA card. You can pay using VISA through your ISP bill portal.

Has HSBC extended the offer of 10x before? The card seems to be good but with the current 10x offer expiring on 31st Dec, am thinking if its worth moving to HSBC.

Yes they extended it twice. Once there is a few months with no bonus point is awarded for any transaction. However, they had extended the rewards program on time this year back in March.

In relation to the article stating that “For starters, there is no mention of a spending cap for online spend, which expressively includes airline and hotel purchases, and even insurance payments.” – has anyone tried using this for insurance payments and have gotten the rewards points?

Hmm… think I might be getting this soon. The main thing that tipped me over was the 3-year expiry period for rewards points. 1 year for DBS WWMC is far too soon!

Can we pay roadtax through one motoring website using this hsbc advance card and get 4mpd?

How about paying for hdb season parking through hdb website, can get 4mpd?

As long as you go through the online VISA gateway (ie, usually comes with the OTP pin), you will receive the bonus.

Hello all

Has anybody try Visa Checkout? Is it counted as online transactions?

I try to book hotel on Marriott.com but seems the transaction is offline based on my previous experience, alternatively the website offers Visa Checkout so i am thinking if its eligible.

Thanks

Ok reply to myself, just called the CSV, confirmed VisaCheckout will NOT earn 10x points.

thanks for clarifying. i do find that strange though, wouldn’t that be a nailed on online transaction?

I agree with Aaron. What reason or TnC did the CSO give for saying it does not count?

I thought so too given DBS WWMC accepts MasterPass…

Ain’t visa checkout just like master pass? A way to save card details – not a payment gateway like PayPal?

Does paying for AXS via masterpass earn 10x rewards? Am thinking of getting this card to pay all my IRAS taxes, season parking, telco bills, insurance premiums via this route. WOuld be good if anyone with experience could share 🙂

To clarify, its paying with masterpass via AXS e-station to qualify as online transactions.

AXS doesn’t currently accept Visa (even via MasterPass), so it’s not going to work…

I just created a Masterpass account last night and was able to add a VISA card as my preferred card. Would have thought that would be sufficient for me to make payment on AXS e-station…

I don’t have personal experience myself, but have read that when it gets to the payment page, Visa on MasterPass is still rejected.

Why not just give it a try yourself and see whether it works? A lot less trouble than applying for a new card. 😉

Anyway I have just applied for the card. Will test it out and do some reward points reconciliation thereafter 🙂

Hopefully the 10x rewards will continue to be extended…

hi zac,

may i know how you reconciliate your points.

you keep all the receipts and tally with the points at the end of ech month?

AY

Yep just keep the statements and reconcile subsequently. You will get 1x rewards the first month, followed by 9x rewards (under Points Adjusted) the following month..

I have tried it before and can confirm that it doesn’t work. If I’m paying any bills on AXS, I’m using FEVO.

And I think the underlying reason is AXS does not take Visa now, unless they have recently changed their mind.

Masterpass/Visa Checkout are like Wallets, so you can could add any card you want to it, but it would not change the transaction. Using a card at a merchant(AXS) that does not support the scheme would work.

The personal banker told me it’s extended to April and would be reviewed then.

I am still trying to reconcile my point from Dec and Jan. Spend 20 min on the phone with the CSO. Appears x1 points are given in the first bill and the x 9 points can be given up in the subsequent 2 months. So far doesn’t look like I have the full x 10 points yet. Must wait for Mar statement to check for Jan spending. What a pain in the A**

to transfer to Krisflyer, you will need to pay $40 + GST yearly.

and once you do it, it is $40 + GST per year.. i do not think you can cancel the subscription.

if anyone is planning to sign up for this card to utilise it when (if) it ends on 31 May 2017, you have to take the $40 + GST into account. If you do not spend much, please dont bother…

yes the $40 + GST per annum ends when you cancel the card..

At least for the HSBC premier card it was possible to cancel the fee after one year.

I am thinking of getting the HSBC Advance credit card. but since the T&C states the 10X ends on 31 May, will wait and see what happens after.

i understand the inertia, but with something like this I think it’s better to bite the bullet and get the paperwork started now. And if it gets extended, count that as a bonus. I can think of way too many people who have thought- ok, the promotion is expiring soon, i’m going to wait and see what happens. And then this and that happens, and before you know it you’re too close to the 10x expiry deadline to think about applying.

I just received a letter that they are replacing the 10x rewards system with a cashback system. 2.5% for less than 2000 spent/month. 3.5% more than 2000 spent/month. the valid spending categories are same as the 10x points categories.