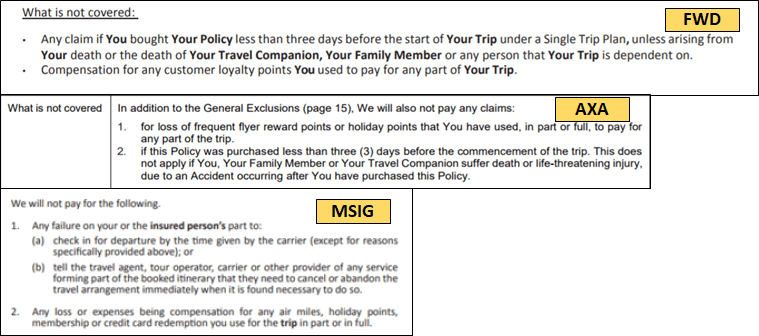

Even though your miles and points are as good as cash to you, most travel insurance companies don’t see it that way. The vast majority of policies explicitly do not cover frequent flyer miles or points.

Why does this matter, you ask, when most award bookings can be cancelled?

Well, you hit the nail on the head. Most redemptions using miles and points can be cancelled with a small penalty fee. However, there will be certain situations where that doesn’t apply. For example:

- Tickets redeemed under KrisFlyer Spontaneous Escapes cannot be refunded

- Your miles may have expired by the time you request a refund of your award ticket (read this article for more details)

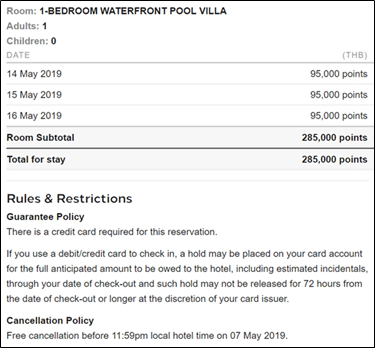

- If you’ve booked a hotel with points, the deadline for cancellation without penalty may have passed. This is particularly a concern in resort destinations like the Maldives or Koh Samui, where award cancellation deadlines may be as long as 1 month before arrival during peak periods

In these cases, you’re going to want to get travel insurance that covers your miles and points in the event you can’t travel.

Here are some general principles governing all policies.

Compensation can only be claimed if your trip cancellation is for a covered reason

It seems almost silly that I have to say this, but if your travel insurance does cover miles and points, claims can only be made if you can’t travel for a covered reason. That’s to say, you can’t just change your mind about traveling and expect to be compensated (exception: Aviva’s “trip cancellation for any reason” feature, see below).

Look at the “trip cancellation” section of your insurance policy and see what “insured events” it covers. This typically includes situations like accidents or medical emergencies that prevent you from traveling. If one of these events causes your trip to be cancelled and your miles and points cannot be recovered, then yes, you can claim the value from your insurer.

Compensation can only be claimed if your points are not recoverable

I mentioned at the start that there are certain situations where your miles and points may not be recoverable. However, in the vast majority of situations, they will be.

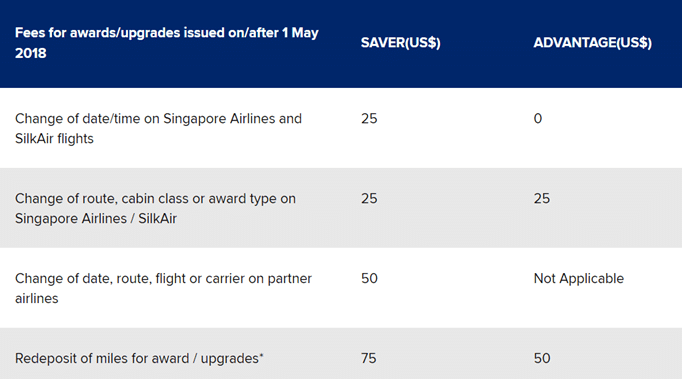

Suppose you fall ill a week before your trip and can’t fly. If you’ve booked a Saver award ticket with Singapore Airlines, you can recover your miles with a US$75 cancellation penalty. Since your miles can be recovered, no compensation is due (it’s worth a shot asking if your travel insurance can cover the US$75 cancellation fee).

Similarly, if you break your leg one week before your vacation, but your hotel lets you cancel your award night without penalty up to 24 hours before check-in, you’re expected to cancel the reservation immediately and won’t be eligible for any compensation.

Valuing miles and points is a tricky business

Because there’s no open market for miles and points (well, except these guys), you may wonder how travel insurance companies assign a value to them. There are two general approaches used:

- The retail price for the ticket/accommodation expense at the time it was issued

- The cost to purchase the lost points according to the loyalty program

Obviously, (1) is much more financially lucrative to the policyholder- just imagine if you redeemed a First Class ticket. Do remember that whatever payout you get is still subject to the policy limits, but given that those can be as high as $20,000 in some cases…

For (2), I can only assume that the insurance company has some sort of internal valuation of miles and points that they use. I’m going to fall back on my usual 2 cents per mile valuation in this case as a best guess, although you’re going to want to check this with them when the situation arises.

Here are the three policies I found which cover miles and points, and what each of them specify.

Sompo

From Sompo’s TravelJoy insurance policy:

We will pay for loss of frequent flyer or similar travel points used by the Insured Person as a registered member to purchase an airline ticket following the Trip Cancellation or Postponement if the Insured Person is unable to recover the lost points from any other source. The payment for lost points will be calculated based on the following, whichever

is the lower:

1. Cost of an equivalent class airline tickets based on the quoted retail price at the time of loss, less any financial contribution by the Insured Person; or

2. Cost to purchase the lost points according to the Frequent Flyer Program or similar travel points by the commercial airline company

tl;dr: Sompo covers your miles and points based on the lower of the retail price of the air ticket or miles. It’s worth confirming with Sompo whether this coverage extends to hotel points as well, because the policy doesn’t say so explicitly.

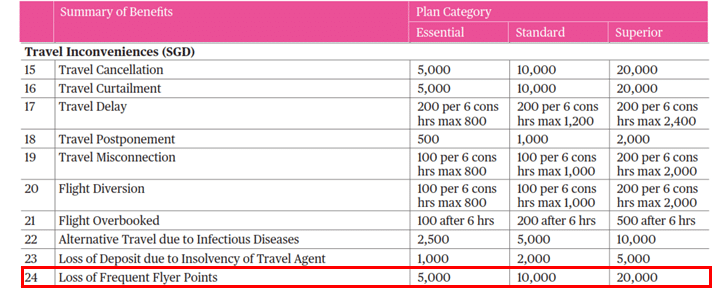

The table below shows the payout limit for trip cancellation under Sompo’s TravelJoy policy, which in other words is the limit to which your miles and points are covered for:

Sompo has another travel insurance policy called TravelEASE which is available through CIMB. This policy also covers miles and points as follows:

Sign up for Sompo travel insurance here

AMEX & Chubb

From Chubb’s My VoyageGuard Travel Insurance:

Section 24 – Loss Of Frequent Flyer Points

If, during the Period of Insurance, the Insured Person purchase an airline ticket (or other travel and/or accommodation expense) using frequent flyer points or similar reward points and the airline ticket (or other travel and/or accommodation expense) is subsequently cancelled as a result of any Specified Cause (as defined in Section 15) and the loss of such points cannot be recovered from any other source, the Company will indemnify the Insured Person the retail price for that ticket (or other travel and/or accommodation expense) at the time it was issued up to the Benefit amount specified in the Certificate of Insurance subject to the terms and conditions of this Policy, provided always that this coverage is effective only if this Policy is purchased before the Insured Person becomes aware of any circumstances which could lead to the disruption of his Journey.

| Edit 25/02: Chubb’s wording seems to suggest that for your miles to be covered, you’ll need to redeem them after you purchase travel insurance. This isn’t so much an issue if you buy an annual travel insurance plan, but it’s worth noting if you’re buying a single trip one. |

tl;dr: Chubb covers your miles and points based on the retail price of the air ticket or accommodation.

The table below shows the payout limit for trip cancellation under Chubb’s My VoyageGuard Travel Insurance policy, which in other words is the limit to which your miles and points are covered for:

Sign up for AMEX travel insurance here

[note: this particular link earns an affiliate commission that supports the running of The Milelion]

Aviva

From Aviva’s Travel Policy:

If You purchase airline ticket or Entertainment Ticket or book accommodation using Frequent Flyer Points or similar reward points and the airline ticket, Entertainment Ticket or booked accommodation is subsequently cancelled due to the events for which You are covered under this policy, We will pay You the retail price for that ticket or booked accommodation at the time it was issued, provided the loss of such points cannot

be recovered from any source

tl;dr: Aviva covers your miles and points based on the retail price of the air ticket or accommodation.

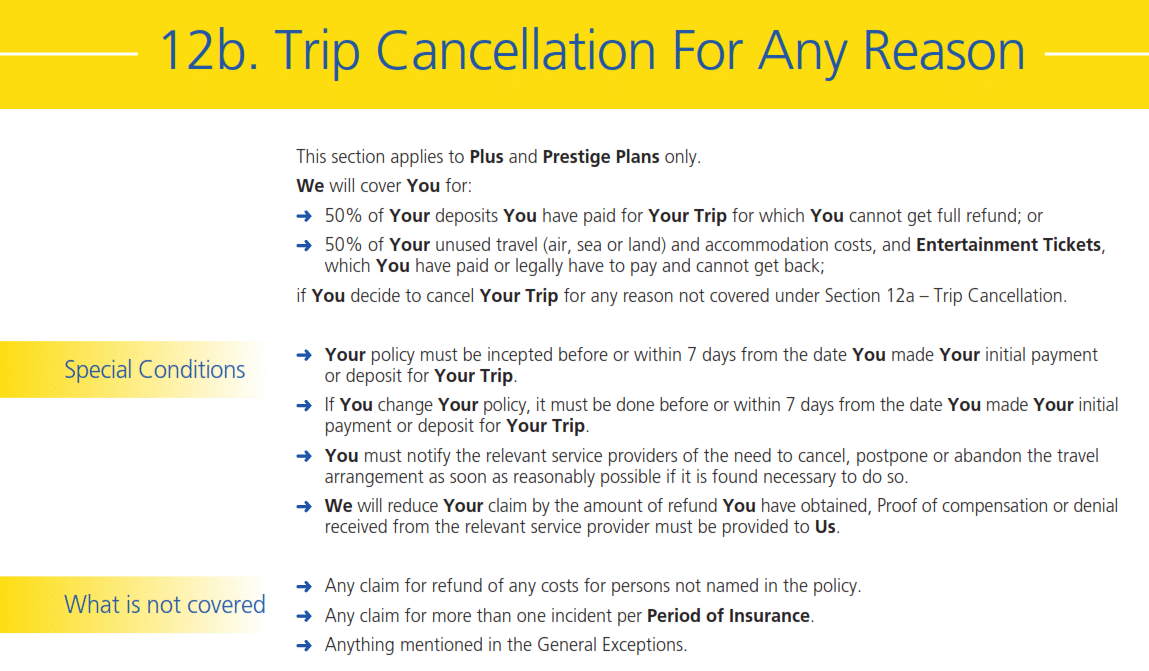

One interesting thing about Aviva’s travel insurance is the Plus and Prestige plan have a “trip cancellation for any reason” feature, which covers you for 50% of your unused travel/accommodation costs which you can’t recover, capped at $5,000.

This conjures an interesting scenario in my mind: what if someone were to redeem a Spontaneous Escapes Business Class ticket and then decides not to travel for “any reason”? Even with the $5,000 cap, 50% of the retail cost of a business class ticket to Europe would surely be much more than the cost of the policy.

I imagine Aviva has some mechanism built in to prevent abuse like this, but it’s still an interesting thought experiment…

Sign up for Aviva travel insurance here

Conclusion

These were the three policies I managed to find that cover your hard earned miles and points. When choosing among these three, you obviously want to look at the policies in their entirety- medical expense coverage, emergency evacuation, rental car excess, the whole shebang.

Great insights in this ariticle! I have a clarifying question – for the ‘trip cancellation for any reason’ under Aviva it says the policy, “must be incepted before or within 7 days from making the initial deposit or payment for your trip”. So does that mean that if I make an award redemption months in advance of my actual flight, within 7 days of the booking I should also buy insurance for the days covering that trip?

[…] A reminder that tickets issued under the Spontaneous Escapes promotion are non-changeable and cannot be canceled as well. This is unlike regular award tickets which at least allow you to refund your booking and miles for a fee. Thus, your travel plans have to be very firm before taking advantage of this promotion (or you should buy a travel insurance policy that covers miles and points bookings). […]

[…] Tickets issued under Spontaneous Escapes cannot be changed or cancelled, unlike regular award tickets which allow this for a fee. If you’re booking a Spontaneous Escapes award, be sure about your travel plans, or buy a travel insurance policy that covers miles bookings. […]

Has anyone successfully gotten 4mpd from using DBS WWMC to pay Chubb’s My VoyageGuard premiums online?

DBS Ts & Cs actually specifically states that Insurance Premiums aren’t a “Qualifying Spend”, but HWZ’s Excel Sheet shows success for Directasia.com and MSIG Travel, unsuccessful for FWD.com, and no info on Chubb…

Thanks!

I have a question though… if the points can be recovered with a fee, the insurer simply pays for the fee but I’d have to find another available flight (on saver biz for instance) and it’s a problem if i’m already overseas and have to fork out of pocket for the return flight? Any thoughts on this? Thanks!

Perhaps you may be allowed some reimbursement under terms of trip curtailment/interruption for covered reasons. You may have to check the fine print of those scenarios.

Please avoid Sompo. Terrible company. You will regret it. Despite buying a rather expensive annual plan, I can’t claim for many cancellation due to covid. The customer service is really lousy. No one picks up the telephone and when you email them, they don’t reply for more than 2 weeks! By that time, it’s too late and I had to make a decision on change to travel plan. Worst company I have experienced so far. Doesn’t matter what extra they cover like loss of miles if they don’t even consider the event as insured event. I find it strange how… Read more »