About a week ago, I wrote about some changes to the BOC Elite Miles World Mastercard T&Cs that Cheaponana had spotted.

At the time, it appeared like BOC was bringing (1) forward the expiry of rewards points, (2) removing Plaza Premium Lounge access and (3) changing the definition of overseas spending.

My BOC contact confirmed the first two weren’t happening, but did mention that they’d be updating the definition of overseas spending and “a few other things” in a set of new T&Cs to be published shortly.

Those new T&Cs have quietly appeared on BOC’s webpage, confusingly future-dated as 15 Mar 2019. It appears there are now three sets of T&Cs floating out there, which I’ve documented here for posterity.

- 23 July 2018 T&Cs (the time the card was launched)

- 28 Dec 2018 T&Cs (the focus of last week’s article)

- 15 March 2019 T&Cs (the focus of today’s post)

We do not know yet when these new T&Cs will be effective from. My best guess is 15 March, but I’m waiting for official confirmation.

Here’s what’s changed.

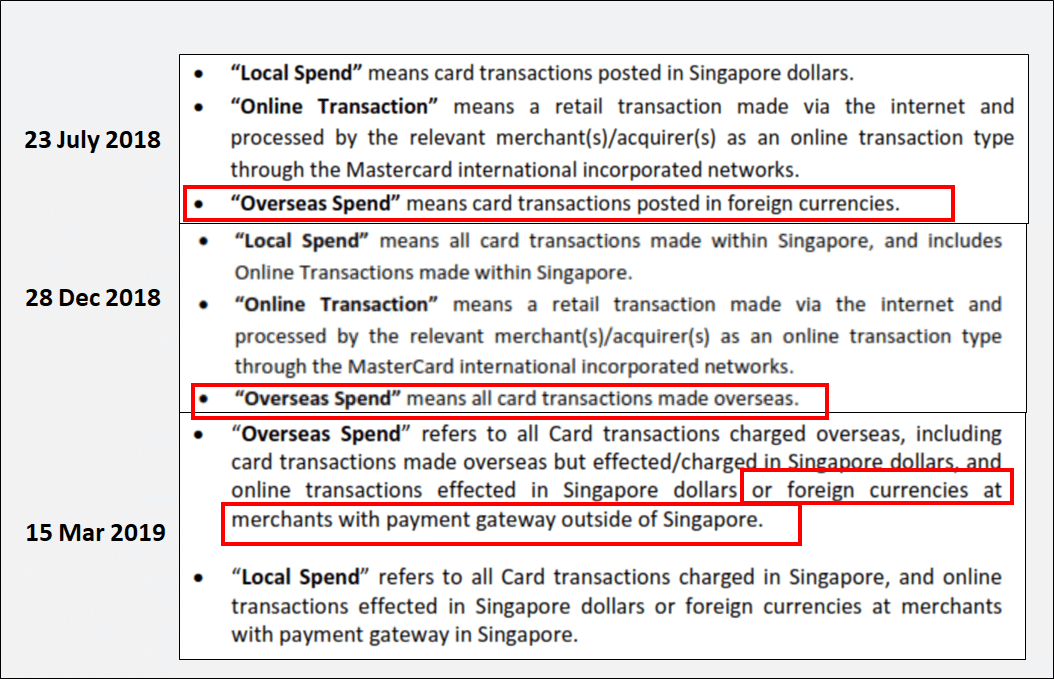

Overseas spending redefined: payment gateway clause added

A bit of context here first. In my previous article on the BOC T&C changes, I mentioned that the 28 Dec 18 T&Cs had updated the definition of local and overseas spend.

In particular, “overseas spend” had been changed from “card transactions posted in foreign currencies” to “all card transactions made overseas”. I speculated that this could mean one of two things:

- Only transactions physically carried out overseas would earn foreign currency spend rates

- Only transactions physically carried out overseas or by an overseas-based payment processor would earn foreign currency spend rates

(2) seemed more likely than (1), given the precedent that UOB had set. Indeed, it seems like BOC has gone down that route:

Perhaps BOC saw that too many people were making purchases on Singapore sites and opting to pay in foreign currency (e.g. the SQ website lets you select what currency to pay in) to enjoy the upsized miles.

Still, I dislike this approach because it’s fundamentally unfair to the consumer, who has no way of knowing which websites process payments inside or outside of Singapore. Sometimes it’s clear cut- if you’re buying from the US version of an e-commerce site like Amazon or eBay, that’s obviously processed outside of Singapore. But other times, it may not be readily apparent. How’s the customer to find out?

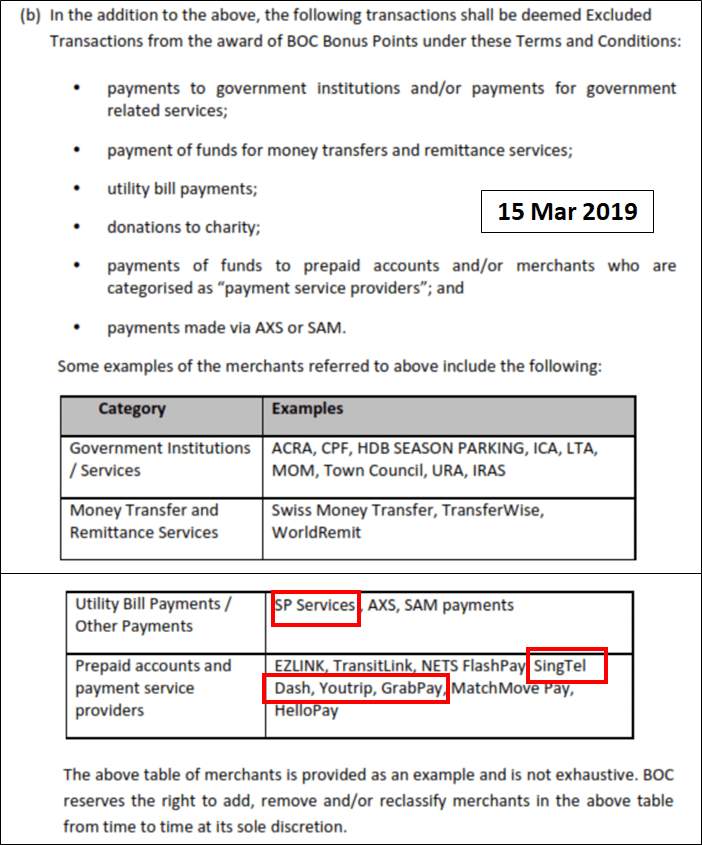

Additional exclusion categories added: GrabPay, YouTrip, SP Services and more

The BOC Elite Miles World Mastercard has been a great “miscellaneous” card for me, thanks in a large part to the absence of exclusion categories. I’ve been using it for payments that I know other banks exclude from rewards earning, such as government payments, utility bills, and charitable donations.

It seems like BOC has decided to tighten its rewards categories, however, as the new version of the T&C has added numerous exclusions:

BOC has provided some specific examples of excluded merchants, and it’s hard to argue with most of them, given that other banks have similar exclusions.

However, the one that really gets me is GrabPay. I can understand removing merchants with the potential for manufactured spend (hello YouTrip and TransferWise), but GrabPay for me has always been a legit expenditure. People top up their account to spend on F&B and taxi rides. If those are legitimate categories for earning points, why shouldn’t GrabPay? It’s not like your GrabPay balance can be cashed out to a bank account.

I’m reaching out to BOC to find out when these new exclusion categories will take place from, and will update the article when I hear back.

| Update: the new exclusion categories take effect from 15 March 2019. I have confirmed that transactions with payment platforms like Cardup and RentHero will continue to earn miles |

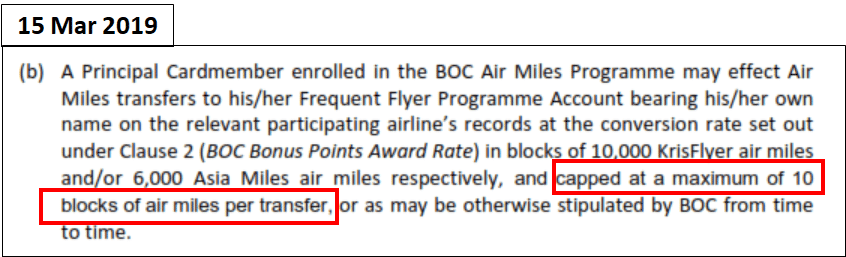

Mileage conversions capped at 60K Asia Miles/100K KrisFlyer miles per transfer

Here’s a puzzling new addition that I totally don’t understand. The new T&Cs add a restriction to the maximum number of miles that can be transferred at one time. You can now transfer a maximum of 10 blocks, i.e. 60,000 Asia Miles or 100,000 KrisFlyer miles at one go. I realise that may sound like a substantial amount for some people, but if you’re looking to redeem premium cabin travel then it’s really nothing at all (especially for Asia miles).

Moreover, it seems like an arbitrary restriction. Why would you cap the number of points that people can transfer at one go? I can’t imagine there are IT restrictions limiting the number of points that can be transferred at one go (although with BOC you never know), and BOC’s transfer fee of $30 is already slightly above the market rate of ~$25. Therefore, it’s hard to see this as anything other than an attempt to earn more from transfer fees.

I am also checking when the new transfer restriction comes into play and will update this post when I know.

| Update: the new transfer restriction is effective from 15 March 2019 |

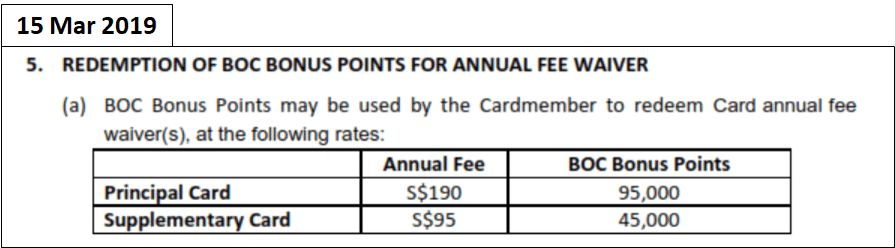

You can now redeem 95,000 points for your card’s annual fee

A new clause has been added that allows cardmembers to redeem 95,000 BOC points (31,667 miles) to cover the card’s annual fee. This is a pretty abject valuation of 0.6 cents per mile, but so long as they don’t automatically deduct people’s points to cover the annual fee ala UOB, I really couldn’t care. Don’t like it? Don’t use it.

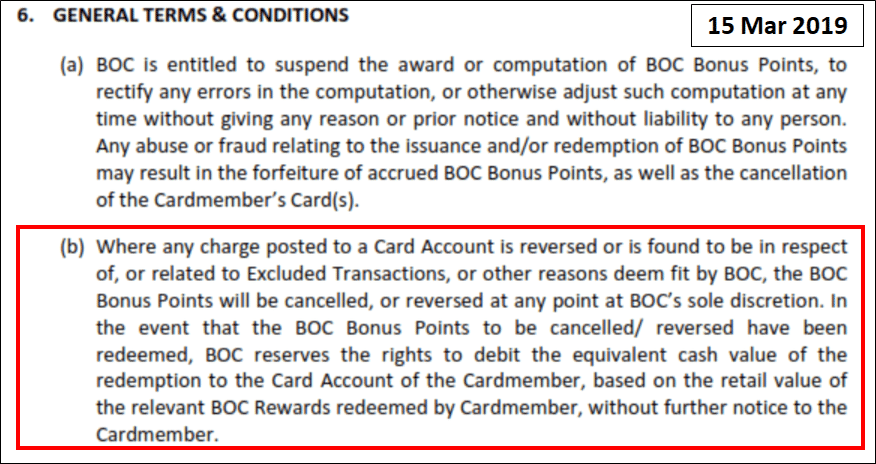

BOC reserves the right to reverse points “found in respect of excluded transactions”

In case you hadn’t gotten the sense by now, the new clause 6(b) should really drive home the point that BOC is starting to tighten the screw on this once-generous card. Have a read below:

Now, I know that most banks have a clause that says something to this extent, but the fact that this did not appear in any of the previous versions of the T&Cs suggests that BOC is wising up to the fact that some users were earning miles on pretty questionable transactions.

Clause 6(b) gives BOC the power to retroactively reverse points awarded on charges related to excluded transactions. I believe those who have been indulging in YouTrip top ups have found themselves on the receiving end of this newly-added clause. I’m sure people doing bona fide transactions have nothing to be scared of, but the broadness of this clause might make them nervous anyway.

Conclusion

The BOC Elite Miles World Mastercard represents BOC’s first crack at introducing a miles card in Singapore. I was always of the quiet opinion that the original T&Cs were generously broad in their interpretation, which made the card so useful in my opinion.

However, this also meant the card was vulnerable to gaming and abuse, and it’s probably gotten so bad that the team is starting to crack down. That’s sad for those of us who were using the card for legitimate (but often unrewarded) spending like parking, utilities, government agency payments and donations, but it’s ultimately BOC’s prerogative what categories they award points for.

What I find hard to accept is the seemingly arbitrary restriction on the number of points that can be transferred in a single transaction, and the shifting of the onus onto the customer to know which websites process payments in and out of Singapore. Both strike me as consumer-unfriendly, and really not the direction the bank should be heading.

I’m keeping my BOC Elite Miles World Mastercard for now, as the general earning rates remain the best in the market. That said, I’ll be keeping a close eye on the T&Cs to see if anything fundamentally changes the value proposition of the card.

I will likely transfer my points and terminate the card as a protest to BOC. Their service is slow and lousy which is another push factor. Their app is hard to get in and I was locked out and had to physically go down to reset it! They couldn’t even have a low threshold alert (their lowest is $100) amd is hard to catch fraudulent charges if it is below 100 especially when I couldn’t get into the app. If more can cancel or boycott the card, it would wake them up a bit to ask why they are losing… Read more »

Totally agreed. But too bad, a lot of miles chasers on this site are so hard up for the miles that they’ll do anything to get it, including signing up for and using this junk card. So BOC may still be thinking they got themselves a winner here.

The alert set at $100 is by choice. Just BOC being cheap by not wanting to pay for more SMS’es than necessary when weighed against their willingness to incur the fraud risk below $100.

But curiously, any transaction in FCY, is alerted even if below the $100 threshold.

how can I apply for it?

Cap at 100k is really unfair, this was never stated when the card was applied.

When I called BOC today to check my latest point stash to do a onetime conversion, it would appear that the CSO wasn’t even aware that there’s a change in terms from 15 March that imposes this cap per conversion! I had to insist that he checked again, which he had to put me on hold, then came back with an about turn that yes, the conversion cap will be imposed from 15 March.

This is why we can’t have nice things.

On a more serious note, this is the first T&C that explicit says they’ll charge you for the retail price of your redemption should you have used up the points.

I can understand the price when you redeem say 5 dollar voucher, but I wonder what would be the price of the krisflyer or Asiamile

Just curious, does this means BOC has the rights to recover the points of any excluded transactions (bonus points awarded) before 15 March ? Seems like some ppl got their Youtrip bonus points clawed back without being informed. Meaning those who spent on Government spending, grabpay and SP services will get their points clawed back even if the transactions was before 15 March ?

well the T&C in any case always gave BOC the right to change things without prior notice (as do the T&Cs of every bank). I’m somewhat less sympathetic to those who spammed youtrip transactions, but i’d think it’d be unfair to clawback government spending/sp/grabpay

BOC do not have any rights to clawback the points when the TNC did not clearly exclude any government spending or utilities. Well, even for prepaid it’s clearly contestable as well . There’s a reason why they suddenly revise the tnc and state which specific transactions are excluded..

Just go lodge a complaint with MAS and MAS will handle from there.

<>

Perhaps one is too hopeful ?

Personally , I doubt very much if we have a strong case given their TNCs.

Spot on. Woe to those who think that the banks somehow have some special duty or obligation to be as accommodating in their T&Cs as possible .

Zzz. The MAS is not an arbiter of consumer disputes with banks. Do you know what the role of a financial regulator is? It’s definitely not to deal with such consumer quibbles.

LOL.. your assumption again? Go to FIDREC and MAS contact us webpage, there is a form for dispute resolution. If you tried lodging a complaint before, you would have know that MAS will get involved in the entire investigation very promptly. Have you ever seen other banks acting the same way as BOC? None. All the other banks did was revise the TNC to exclude the transactions and no clawback was done. How can any banks apply the TNC retrospectively and arbitrarily? So if today I used the card for Singtel/M1/Starhub, insurance and education bill and it is not excluded.… Read more »

Whose assumption again? Do you know what the MAS complaint form was designed for? Confidential, but let’s just say that it was not for this type of complaint. Do you know what happens behind the scenes when there is a complaint like that about T&Cs?

How can any banks apply the TNC retrospectively and arbitrarily? Simple – if you agreed to it. Bad practice, yes. Can the bank do it? Hell yes.

Going to FIDREC immediately without getting MAS involved is the much more feasible option.

Lol… If you think that BOC is the first and only bank to pull a stunt like this, you clearly haven’t been playing this game for long.

Every card issuing bank in Singapore has done something like this or even worse. Part & parcel of the game.

Thanks!

Anyone knows what about transactions made via cardup and ipaymy, for the excluded transactions, like iras ?

They already started clawing back for cardup and ipaymy too..

It was an exciting prospect when they first announced it, but now the program/card is really too much of a hassle to bother with. From approval times to earning restrictions to redemption limitations, it’s just not that worth it to me any more.

will the card still enjoy 4x lounge ?

They seem to exclude all “payment service providers” like cardup.

So these transactions will not even yield the basic 1.5mpd.

Probably gotta switch back to PRVI except for all my physical overseas transactions.

does insurance payments still get points/miles?

Why do you think excluding GrabPay top ups is any less unfair relative to Youtrip top ups? Sure, Youtrip is a Mastercard, and is therefore much more widely accepted, but GrabPay and Youtrip are both wallets you can top up to, as you put it, make perfectly legitimately purchases at F&B and even random watch/jewellery shops (I’ve seen some in People’s Park)? You can’t transfer the balance on a Youtrip card to a bank account either. I mean, the only argument I can really think of is as above, that Youtrip being a Mastercard, is much more widely accepted by… Read more »

Quite disappointed on the latest change and unsure if BOC will waive Annual fee. I cancelled the Family card as they decided to waive 50% last year. Currently, I have more than 500k Rewards points. (Lodge a complain with MAS to dispute the transactions in FCY under Singapore payment gateway to get back the reward points). After 15 March, I have to pay $60 to transfer all the miles. Customer service is non-existence until you lodge a complain with MAS. As I have a Smartsaver account with BOC, I do get 0.8% or 1.6% (P.A.) monthly interest on first $60000… Read more »

Did BOC return you back the points quickly after MAS intervention? If the points are now in your account, I would suggest you transfer to your KF/AM asap, before they implement more rules in their favour. God knows what they will change next? Maybe cap of KF miles to be redeem in a year/quarter, increase of transfer fee.

This card has quite frankly shown the very ugly side of BOC and has lost any goodwill/reputation (if any) it used to have.

Yes, I got back the remaining miles after 2 – 3 weeks. They used an excel sheet to calculate all transactions till End of Dec 2018.

I will consider on transferring next week.

Thank you

May I know where did you find the T&C? I couldn’t even find the card in BOC website.

the bit.ly url was available in a past card statement

I concur with many of your comments that BOC’s customer service response times are languid. Plus emailing them typically garners a perfunctory automatic response stating that BOC has “received your email and have forwarded to the relevant department”. But if you do manage to call through to their hotline, the staff seem quite experienced and capable. However, this latest revision to their terms & conditions has devalued the attractiveness of their BOC Elite Miles World Mastercard. The inclusion of the ill conceived “payment gateway clause” to their Overseas spending further limits this card’s usefulness. Customers have no way of determining… Read more »

So glad I didn’t sign up for this card. With the Prestige card, find little incentive to do so especially with the long application waiting time. Now with so many rules revision… Zzz

Would it be highly likely that payments to foreign government institutions (outside of Singapore) will fall under the exclusion category too?

Aaron, did BOC confirm that the new tnc apply from 15/3? Thanks

They didn’t reply to me

Wow. They snubbed you because they don’t know who you are?! 😁

[…] devil is in the details (of Bank of China’s T&Cs, which were revamped in March 2019). Here are a few things you should know before signing […]