DBS has launched a new Points Purchase Programme, which allows cardholders to buy as many miles as they wish, no questions asked.

Unlike other payment platforms such as CardUp, you don’t have to submit any documentation, or otherwise prove you have a legitimate bill to pay. If you want it, you got it.

Of course, this convenience comes at a price, and a hefty one at that. At 2 to 2.2 cents per mile, this ranks as one of the most expensive ways of buying miles. And with plenty of cheaper alternatives available, this should only be an option for the lazy — or uninformed.

Details: DBS Points Purchase Programme

|

| Details |

From 2 July to 30 September 2026, principal cardholders of the following cards can purchase additional DBS Points through the DBS Points Purchase Programme.

- DBS Altitude AMEX

- DBS Altitude Visa

- DBS Insignia Card

- DBS Vantage Card

- DBS Woman’s Card

- DBS Woman’s World Card

There are a total of four tiers to choose from, with the cost per mile ranging from 2 to 2.2 cents.

| Tier | DBS Points (Miles) |

Fee | Cost Per Mile |

| 1 | 12,500 (25,000) |

S$550 | 2.2¢ |

| 2 | 37,500 (75,000) |

S$1,600 | 2.13¢ |

| 3 | 75,000 (150,000) |

S$3,000 | 2¢ |

| 4 | 250,000 (500,000) |

S$10,000 | 2¢ |

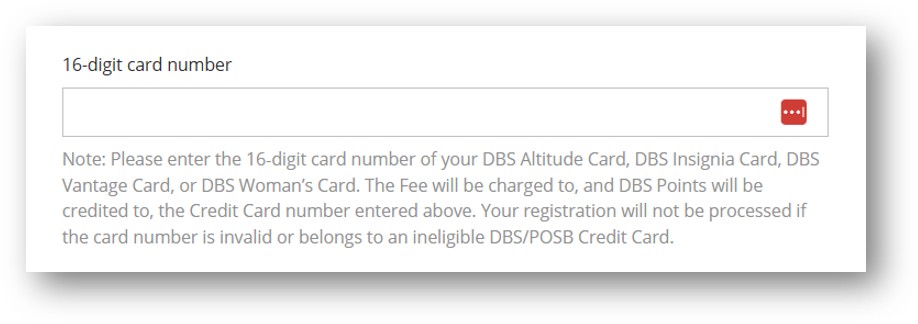

To participate, select your preferred tier via this landing page and log in using your banking credentials.

- The applicable fee will be charged to your card within 30 days

- DBS Points will be credited within 10 days after the fee is charged

This means you should receive your miles within six weeks from the time of expressing interest.

There is no limit on the number of DBS Points you can purchase through this programme, and you can make multiple purchases of the same tier if you wish, by submitting separate registrations.

| ⚠️Watch your credit limit |

| While there’s no limit on the number of DBS Points you can purchase, the fee paid counts against your credit limit. Be careful not to exceed this, or else a non-waivable over limit fee will be charged. |

Registrations cannot be withdrawn once submitted, so don’t fool around with the registration form — during a similar promotion last year, numerous trigger-happy users inadvertently registered themselves!

The card you choose matters!

At the point of registration, you’ll be asked to submit your 16-digit number. This is the card to which the fee will be charged and DBS Points credited to.

If you have more than one DBS credit card, choose carefully! Different DBS cards have different points expiry policies:

- DBS Woman’s Card, DBS Woman’s World Card: 1 year

- DBS Vantage: 3 years

- DBS Altitude AMEX, DBS Altitude Visa, DBS Insignia: No expiry

Since DBS Points are all pooled for the purposes of redemption, it would be silly to nominate the DBS Woman’s World Card when you have a DBS Altitude, for example.

Is it worth it?

Speaking of silly, perhaps a better question to ask is whether the DBS Points Purchase Programme is worth it in the first place.

It’s a simple and relatively quick way of topping up your miles balance in large volumes. But, as mentioned, the catch is the price. Could you get more than 2 to 2.2 cents per mile from a flight redemption? Yes.

But could you buy miles for less than 2 to 2.2 cents each? Also yes.

UOB Payment Facility

![]() The UOB Payment Facility is the closest equivalent to the DBS Points Purchase Programme, since it’s also a no questions asked kind of deal.

The UOB Payment Facility is the closest equivalent to the DBS Points Purchase Programme, since it’s also a no questions asked kind of deal.

UOB cardholders can currently purchase unlimited miles at 1.8 cents per mile (1.6 cents for the UOB Reserve Card) until 31 August 2026, which in my opinion, makes the DBS Points Purchase Programme virtually irrelevant.

What’s more, the UOB Payment Facility doesn’t have fixed purchase blocks, so you can tailor the amount you wish to purchase more precisely.

Citi PayAll

Citi PayAll is currently offering an effective admin fee of 1.9% for tax payments to customers who charge a minimum of S$6,000 by 31 July 2026.

This reduces the cost to 1.19 to 1.58 cents per mile for the Citi ULTIMA, Citi Prestige and Citi PremierMiles Card — and that’s before taking into account the additional S$80 eCapitaVoucher offered for customers who charge at least S$8,000.

SC EasyBill

SC EasyBill allows Standard Chartered cardholders to pay rent, insurance, education and tax bills with a 1.9% admin fee.

Depending on the card you hold, that’s equivalent to paying 0.95 to 1.9 cents per mile.

CardUp

![]()

CardUp is no longer the force it used to be, following a major increase in their payment processing fees from 13 June 2026. So it says quite a bit that you can still purchase miles well below the 2 to 2.2 cents threshold with the various ongoing promotions.

For example, a customer paying income tax with a 2.3% fee and a DBS Altitude Visa (1.3 mpd) would be paying 1.73 cents per mile. Heck, even with the 2.45% fee offered for any kind of Visa payment, a DBS Vantage Card (1.5 mpd) would achieve a cost of 1.59 cents per mile.

Terms & Conditions and FAQs

What can you do with DBS Points?

DBS Points can be converted to the following frequent flyer programmes.

| Frequent Flyer Programme | Conversion Ratio (DBS Points : Miles) |

| 5,000 : 10,000 | |

| 5,000 : 10,000 | |

| 5,000 : 10,000 | |

| 500 : 1,500 |

Each conversion costs S$27.25, regardless of the number of miles transferred.

Conclusion

DBS cardholders can now purchase as many miles as they need through the DBS Points Purchase Programme, but at 2 to 2.2 cents each, it should only be an option for those who value convenience over everything else.

And even if convenience is key, the UOB Payment Facility offers miles at just 1.6 to 1.8 cents each, with no paperwork necessary and the ability to purchase miles in smaller, more precise blocks. You could buy miles for even less through Citi PayAll or SC EasyBill, provided you’ve got the right documentation.

Therefore, I’m struggling to see who would find this useful. It’s not like DBS Points have the kind of flexibility that Citi or HSBC offer, with Asia Miles, KrisFlyer and Qantas the only viable options.

You’re better off sitting this one out, if you ask me!

can a family member that has a UOB Reserve Card buy them to credit to another family member?

This is still cheaper than purchasing from SIA themself no? They are charging USD 40 per 1000 miles which works out to be 5.2 cents per mile. But yes, admit there’s cheaper options available

Hi Aaron.

Love your works and postings.

Are you aware of any change in the annual fee waiver policy for the Vantage card? I had checked with the DBS call center 2-3months ago, and they responded ‘strictly no fee waiver anymore from this August’

Love this card, and this is a real bummer…

https://milelion.com/2025/08/14/dbs-vantage-card-ending-s60k-spend-path-to-annual-fee-waiver/

Hi Aaron, If I avail of this promotion, and chunk the fee into installment, will I still be getting the poin

ts?