Last month, CardUp announced that it would hike its service fees from June 2026, citing an industry-wide increase in card processing costs.

However, the only detail shared at the time was that the standard service fee would increase from 2.6% to 2.9%. While concerning, this rate was largely theoretical, given CardUp’s frequent promotions for rent, income tax, and other recurring payments. What everyone really wanted to know was how the promotional rates would be affected.

Well, CardUp has now announced its new promotional rates, and the changes are brutal. From 13 June 2026, fees will increase by up to 36% across all categories, with nothing less than 2.25%.

To put things into perspective, the highest promotional fee today is roughly on par with the lowest promotional fee going forward!

Details: CardUp’s revised fee structure

| Details |

Here’s a summary of how CardUp fees will be changing for payments made from 13 June 2026 onwards.

| Category | Until 12 Jun 2026 | From 13 June 2026 |

| Standard Fee AMEX MC Visa |

2.6% | 2.9% +12% |

| Recurring Promo Visa |

1.85% | 2.35% +27% |

| One-off Promo Visa |

2.35% | 2.45% +4% |

| One-off Promo AMEX MC |

2.35% | 2.59% +10% |

| New Home Categories Promo Visa |

From 1.77% | From 2.28% +29% |

| Rent Promo Visa |

1.83% | 2.3% +26% |

| Reno Promo Visa |

2.1% | 2.39% +14% |

| Income Tax One-off Promo Visa |

1.73% | 2.35% +36% |

| Income Tax Recurring Promo Visa |

1.75% | 2.25% +29% |

| Income Tax Bonus Promo Visa |

1.77% | 2.3% +30% |

| International Payment Promo Visa |

1.85% | 2.35% +27% |

Fees are increasing by 4% to 36% across categories, and what’s more, the vast majority of promotions are for Visa cards only. If you have an American Express or Mastercard, the lowest rate you can hope for is 2.59%.

Of course, there may be targeted offers from time to time, but it looks to me like the days of sub-2% fees are well and truly over.

What about existing payments?

The most important thing to understand is that setting up your payments before the new fees come into effect does not lock in the current rates.

CardUp has provided the following transition timeline:

Note: The fee is determined by the due date, not when you create/schedule the payment. E.g. If you scheduled a payment on 15 May 2026 to be paid on 15 June 2026, the new pricing will apply. |

If you have existing payments under the current fee structure, you can adjust them up until the end of day on 8 June 2026. The last date where the current fee structure will apply is 12 June 2026.

On 13 June 2026, all your payments will be automatically updated to the corresponding new code. For example, if I’m currently paying rent with the code RENT183 for a 1.83% fee, the payment arrangement will be updated to RENT23 with a 2.3% code on 13 June.

If you’re not agreeable to the new fees, make sure you cancel any payments that take place from 13 June 2026.

In spite of all the comms that CardUp is doing about these changes, it’s probably inevitable that some people will miss the memo. I imagine they’re going to be in for a bit of a shock when they check their statement and see how much the fees have increased by…

What is the cost per mile?

In the table below, I’ve summarised the lowest possible cost per mile for the various general spending cards in Singapore following the changes, based on a 2.25% fee for Visa, and 2.59% fee for AMEX and Mastercard.

| Card | Earn Rate | Lowest CPM |

StanChart Beyond Card StanChart Beyond CardPriority Private Priority Banking Apply |

2 mpd | 1.26¢ |

DBS Insignia Card DBS Insignia CardApply |

1.6 mpd | 1.38¢ |

OCBC VOYAGE Card OCBC VOYAGE Card(Premier, PPC, BOS) Apply |

1.6 mpd | 1.38¢ |

UOB Reserve Card UOB Reserve CardApply |

1.6 mpd | 1.38¢ |

Apply |

1.5 mpd | 1.47¢ |

StanChart Visa Infinite StanChart Visa InfiniteApply |

1.4 mpd |

1.57¢ |

UOB PRVI Miles Visa UOB PRVI Miles VisaApply |

1.4 mpd | 1.57¢ |

UOB Visa Infinite Metal Card UOB Visa Infinite Metal CardApply |

1.4 mpd | 1.57¢ |

Citi ULTIMA Mastercard Citi ULTIMA MastercardApply |

1.6 mpd | 1.58¢ |

| StanChart Beyond Card Regular Apply |

1.5 mpd | 1.68¢ |

DBS Altitude Visa DBS Altitude VisaApply |

1.3 mpd | 1.69¢ |

OCBC 90°N Visa OCBC 90°N VisaApply |

1.3 mpd | 1.69¢ |

OCBC VOYAGE Card OCBC VOYAGE CardApply |

1.3 mpd | 1.69¢ |

OCBC Premier Visa Infinite OCBC Premier Visa InfiniteApply |

1.28 mpd | 1.72¢ |

UOB PRVI Miles Mastercard UOB PRVI Miles MastercardApply |

1.4 mpd | 1.80¢ |

Maybank Visa Infinite Maybank Visa InfiniteApply |

1.2 mpd | 1.83¢ |

StanChart Journey Card StanChart Journey CardApply |

1.2 mpd | 1.83¢ |

Citi Prestige Card Citi Prestige CardApply |

1.3 mpd |

1.94¢ |

OCBC 90°N Mastercard OCBC 90°N MastercardApply |

1.3 mpd | 1.94¢ |

AMEX KrisFlyer Ascend AMEX KrisFlyer AscendApply |

1.2 mpd | 2.10¢ |

Citi PremierMiles Card Citi PremierMiles CardApply |

1.2 mpd | 2.10¢ |

KrisFlyer UOB Credit Card KrisFlyer UOB Credit CardApply |

1.2 mpd | 2.10¢ |

AMEX KrisFlyer Credit Card AMEX KrisFlyer Credit CardApply |

1.1 mpd | 2.30¢ |

| Note: BOC and HSBC cards, along with DBS- and UOB-issued AMEX cards, do not earn rewards with CardUp | ||

It makes for pretty grim reading. Unless you have a Visa card that earns at least 1.5 mpd, or a StanChart Beyond Card with Priority Private/Priority Banking status, you can no longer achieve a cost per mile below 1.5 cents — my personal cutoff for buying miles. Such cards are largely inaccessible to the average miles chaser, due to hefty minimum income or AUM requirements, as well as substantial annual fees in most cases.

That said, miles valuation is a highly subjective figure, and there are valid arguments for buying miles above the 1.5 cents threshold. However, I would set a ceiling of 1.8 cents, since that’s the rate at which UOB PRVI Miles Cardholders can buy unlimited miles through the no-questions-asked UOB Payment Facility (which, unlike CardUp, does not require documentation).

It’s worth noting that Citi and StanChart cardholders in particular have much cheaper options at their disposal too:

- Citi cardholders can pay tax and non-tax payments with a lower cost per mile (starting from 1.19 cents) through the ongoing Citi PayAll promotion

- StanChart cardholders can pay tax and non-tax payments with a lower cost per mile (starting from 0.95 cents) through SC EasyBill or the SC Income Tax Payment Facility.

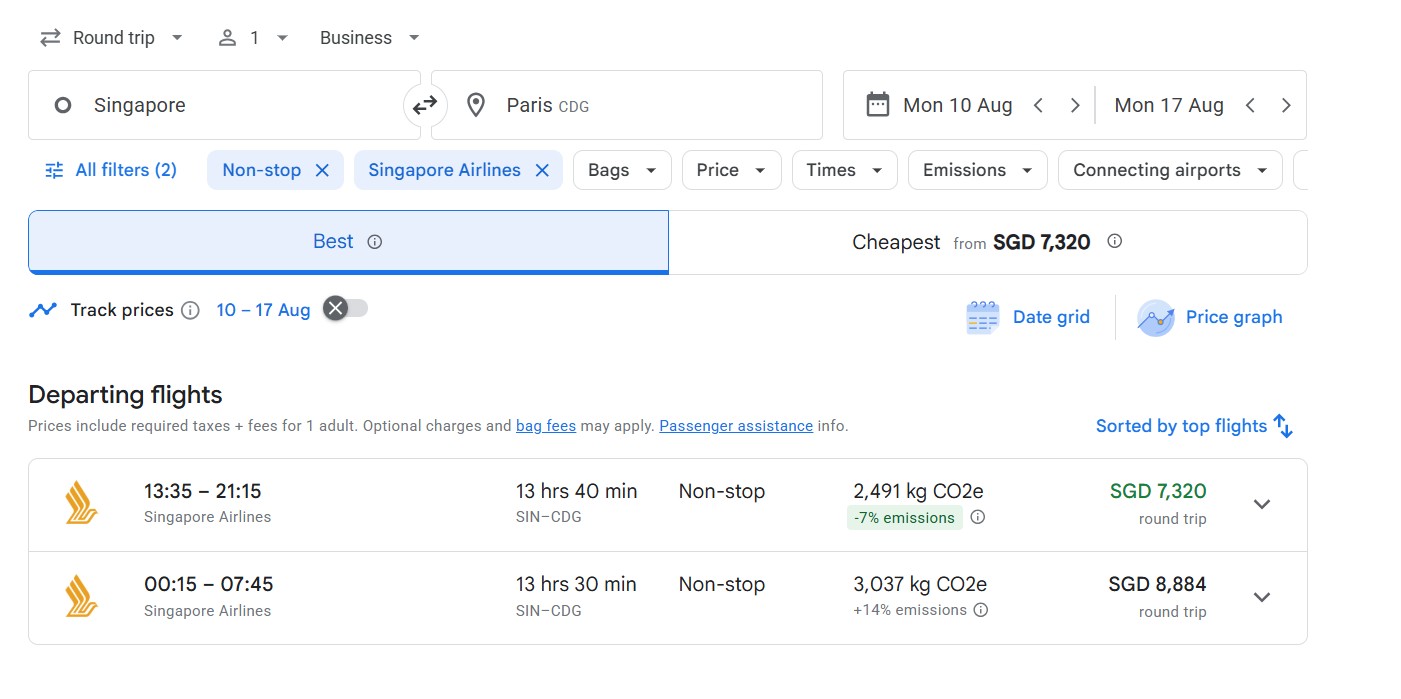

Save 73% off Business Class tickets?

In the eDM that CardUp sent out announcing these changes, there’s one claim that I want to address.

|

✈️ Why it’s still worth it: Save over 73% on Business Class Seats Even at a 2.30% fee, a 1.5 MPD card remains a strategic win for earning miles. For context, a round-trip Business Class flight to Paris via CardUp fees costs just S$3,327—that’s 73% less than the S$12,500 retail price. Luxury travel, smartly priced. |

Basically, CardUp argues that they’re still worth it because you can buy miles to redeem a Business Class flight to Paris for S$3,327, saving 73% off the S$12,500 retail price.

But there are a lot of problems with these figures.

First of all, I’m not quite sure how they came to a S$3,327 figure, given that my own calculations show something slightly higher:

- With a 2.3% fee and 1.5 mpd card, the cost per mile is 1.5 cents

- A round-trip Business Saver ticket from Singapore to Paris costs 217,000 miles + S$333.10

- The total cost is S$3,588

Second, and more importantly, the price of this ticket usually hovers between the S$7,000 to S$9,000 range, and can even be as low as S$6,526.

It’s certainly possible for the price to reach S$12,500, but if it did, that would typically indicate that only a few seats are left. At that point, it’s highly unlikely that a Business Saver award would be available.

Third, when comparing a commercial ticket to an award ticket, we have to account for the following:

- The commercial ticket offers far more availability than a redemption ticket

- The commercial ticket earns PPS Value and KrisFlyer miles, while the redemption ticket does not

- The commercial ticket would earn more credit card miles (fare + taxes) than the redemption ticket (taxes only)

All this to say: a 73% savings figure is probably vastly inflated, and in any case, the savings are only real if you would have been willing to pay for a Business Class ticket with cash in the first place.

Conclusion

CardUp’s revised fee structure takes effect on 13 June 2026, and it’s not pretty. Regardless of payment type, the fees will be substantially higher than before, pushing the cost per mile on many cards into unattractive territory.

Obviously, CardUp didn’t want any of this, but its business model is such that it will always be at the mercy of the card associations. That makes it difficult to compete with in-house payment facilities like Citi PayAll and SC EasyBill, which can undercut pricing by bypassing card associations entirely.

Be sure to review any existing CardUp payments ahead of the deadline and adjust or cancel them as necessary, if you’re no longer comfortable with the new fees.

Well, we’ve had a good run. Thanks for all the miles and good luck for your future endeavors, dear Cardup.

RIP, CardUp. As an ex-employee and a fervent supporter/user of CardUp, I have to admit that the days are numbered. I am taking my business elsewhere with these fee increases.

But where. The problem is not many ways to earn miles for the bills spending

When it becomes too expensive to try earning miles for bills, maybe it just isn’t worth doing so anymore. Alternatively, ipaymy and Citi PayAll when there are promos.

What about the milelion 2026 promo?

the milelion tax payment promo will be adjusted to 2.25%, to match cardup’s public offer

Yesterday, after I received the not so good news, I wrote in to Cardup to ask for better rates. Here’s their reply:

“At the moment, we are still in discussions regarding the new rate. Once it has been confirmed, we will send an email with the updated details.

Please also note that additional promotional offers may be introduced after 13 June 2026. We will keep you informed of any new promotions as they become available.”

Huh??? Still got new news coming?

Time to say goodbye, I’ve been using Cardup for 5 years now and also referred more than 10 members, bon voyage

What about Ipaymy?

On this site it’s known as “It Who Must Not Be Named”…

“Basically, CardUp argues that they’re still worth it because you can buy miles to redeem a Business Class flight to Paris for S$3,327, saving 73% off the S$12,500 retail price.”

This is only relevant if (1) you’re a stickler for flying SQ and (2) would pay inflated cash prices at that level.

Indirect airlines do sell J airfares in the range of $3,000-4,000 when there are promotions.

Bye bye CardUp

UOB promotion for miles purchase is now anytime better than Cardup!

correct me if im wrong, but isnt uob payment facility 1.8 cents? compared to cardup + prvi which is 1.57 cents, isnt latter still better?

i think the idea is that 1.8 cents sets the ceiling. as in- there is now no reason to ever pay more than 1.8 cents per mile because you could use the uob payment facility otherwise.

Yes this exactly. Sigh, I was just starting to use cardup more frequently, but with this price increase, it’s no longer feasible for me. Disappointed.

I dunno, the rent promo is an extra .5% per month on what I was paying before. Since I am already set up, I am thinking to just ride out the remaining rent promo that I set up.

Anyone has a better altenative to get miles thru mortgage payments ;-;

I want to know too!