HSBC has launched the HSBC TravelOne Card, its first entry-level miles card for the Singapore market.

Do we really need another miles card? Well, that’s the thing- it’d be a mistake to dismiss the TravelOne as “just another miles card”.

I attended the launch event today and spoke with the team behind the product. There’s a lot to get into, but here’s the key highlights:

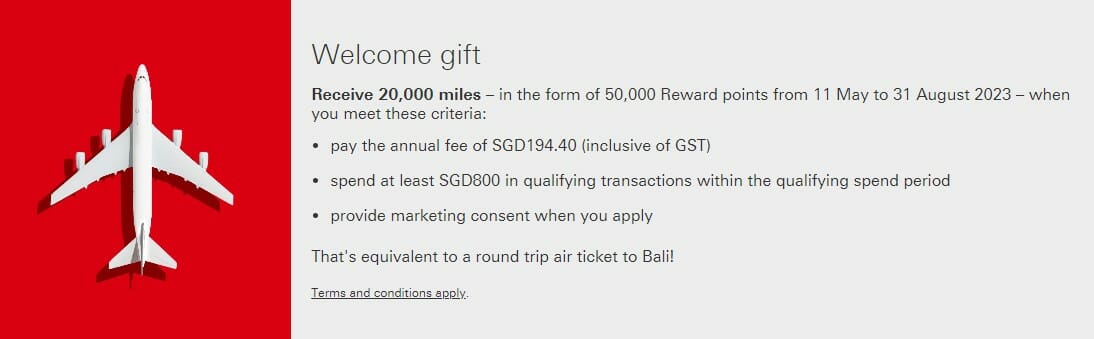

- A 20,000 miles sign-up offer with S$800 min. spend, valid for new and existing customers

- 1.2 mpd on local spend, 2.4 mpd on FCY spend

- 4 complimentary lounge visits per calendar year

- No conversion fees till 31 December 2023

- Transfers completed “instantly or within one business day”

- 12 hotel and airline transfer partners

I want to focus specifically on the final point, because that’s what’s got me the most excited. Not only does HSBC now have the most transfer partners in Singapore (taking the crown from Citi), it intends to add new airline and hotel partners at an aggressive pace, and I mean aggressive. The goal is more than 20 partners by the end of 2023!

I’ve seen the roadmap, and while I can’t share specifics, there are some names that would make the miles community here very happy…

Overview: HSBC TravelOne Card

HSBC TravelOne Card HSBC TravelOne Card |

||

| Apply Here | ||

| Card T&Cs | ||

| Sign-Up Bonus T&Cs | ||

| Income Req. | Annual Fee | FCY Fee |

| S$30,000 |

S$194.40 | 3.25% |

| Local Earn | FCY Earn | Transfer Partners |

| 1.2 mpd |

2.4 mpd | 12 |

The HSBC TravelOne Card (which I suspect we’ll soon be calling the T1 Card, given the styling on the card face) has a minimum income requirement of S$30,000. If you do not meet the minimum income requirement, a minimum fixed deposit collateral of S$10,000 will apply.

Cardholders will pay an annual fee of S$194.40, waived from the second year onwards if they spend at least S$25,000 in a membership year.

It’s not clear from the T&Cs whether cardholders will receive any miles for paying the annual fee each year.

Earn rates

HSBC TravelOne Cardholders earn:

- 3X HSBC points per S$1 (1.2 mpd) on local spend

- 6X HSBC points per S$1 (2.4 mpd) on foreign currency spend

There is no minimum spend required, nor cap on the points that can be earned.

While it won’t be a substitute for a 4/6 mpd card, these are very compelling earn rates compared with other entry-level general spending cards. That’s all the more when you remember that HSBC awards points for transactions as small as S$0.50, compared to S$5 for the UOB PRVI Miles Card and OCBC 90°N Card, its two closest rivals.

| 💳 Entry-Level Miles Cards: Earn Rates | |||

| Cards | Local Earn | FCY Earn | Min. Spend to Earn Points^ |

UOB PRVI Miles UOB PRVI Miles |

1.4 | 2.4 | S$5 |

| HSBC TravelOne Card |

1.2 | 2.4 | S$0.50 |

OCBC 90°N Card OCBC 90°N Card |

1.3 | 2.2 | S$5 |

| 1.2 | 2.0 | S$1 | |

DBS Altitude Card DBS Altitude Card |

1.2 | 2.0 | S$1.67 |

| 1.2 | 2.0* | S$0.42 | |

AMEX KrisFlyer Credit Card AMEX KrisFlyer Credit Card |

1.1 | 2.0* |

S$0.45 |

KrisFlyer UOB Credit Card KrisFlyer UOB Credit Card |

1.2 | 1.2 | S$5 |

| *June and Dec only, otherwise 1.1 mpd ^Assuming SGD spend |

|||

My main concern here is the lack of a bonus category. While earn rates of 1.2/2.4 mpd are decent, it’ll take quite a lot of spending to reach a critical mass of points, especially since HSBC excludes CardUp and ipaymy transactions from earning rewards, and because points don’t pool with other HSBC cards.

Sign-up bonus

|

| Apply Here |

From 11 May to 31 August 2023, customers who apply for a HSBC TravelOne Card will enjoy 20,000 bonus miles (in the form of 50,000 HSBC points) when they:

- Pay the annual fee of S$194.40

- Spend at least S$800 by the end of the month following approval

- Opt-in for marketing communications during the sign-up

This offer is valid for both new and existing HSBC cardholders.

The qualifying spending period is as follows:

| Card Account Opening Date | Qualifying Spend Period |

| 11-31 May 2023 | 11 May to 30 Jun 2023 |

| 1-30 Jun 2023 | 1 Jun to 31 Jul 2023 |

| 1-31 Jul 2023 | 1 Jul to 31 Aug 2023 |

| 1-31 Aug 2023 | 1 Aug to 30 Sep 2023 |

| 1-15 Sep 2023 | 1 Sep to 31 Oct 2023 |

20,000 miles for S$800 spend and a S$194.40 annual fee is a tidy return; put it another way, you’re paying about 0.97 cents per mile (S$194.40/20,000 miles), which is a great price especially when you factor in transfer partner variety.

If you’re a new HSBC cardholder, you’ll also receive a further S$30 cash when you apply via SingSaver. You can use any of the links in this post, or refer to this article.

Bonus crediting

Bonus miles (in the form of HSBC points) will be credited within 90 days from the card opening date, provided the eligibility criteria is met.

Terms & Conditions

The terms and conditions for the welcome offer can be found here.

Points Expiry

HSBC points earned on the HSBC TravelOne Card expire after 37 months, same as other HSBC credit cards.

Transfer Partners

Here’s what I think is the biggest selling point of the HSBC TravelOne Card: transfer partners.

HSBC points could previously be transferred to just Singapore Airlines KrisFlyer and Cathay Pacific Asia Miles, but the HBSC TravelOne Card comes with nine airline and three hotel partners.

| ⚠️ HSBC TravelOne Exclusive |

|

Unfortunately, these additional partners will not be available to HSBC Revolution and HSBC Visa Infinite Cardholders, who will only be able to convert their HSBC points to KrisFlyer and Asia Miles for the time being. While there are plans to eventually make these new partners available to the rest of HSBC cardholders, it won’t be happening in the near future. |

Conversions can be done via the HSBC Singapore app (Android | iOS) and are processed “instantly or within one business day” (except Accor, which takes five business days). During the media event, they consistently emphasised the “instant” aspect, but the website uses more nuanced language “instant or within one business day”. I suppose that’s just in case.

All conversion fees will be waived until 31 December 2023. It’s unclear what they’ll be after that, so stay tuned.

| ✈️ HSBC TravelOne Airline Partners | |

| Frequent Flyer Programme | Conversion Ratio (HSBC Points : Partner) |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 |

|

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

|

25,000 : 10,000 |

| 🏨 HSBC TravelOne Hotel Partners | |

| Hotel Programme | Conversion Ratio (HSBC Points : Partner) |

| 25,000: 5,000 | |

| 25,000: 10,000 | |

| 25,000 : 10,000 | |

The upshot is that HSBC (9 airlines, 3 hotels) has now wrestled the “most transfer partners” crown from Citibank (10 airlines, 1 hotel).

It’s nice to see three hotel partners, although the transfer ratios won’t be worthwhile for most people. This isn’t a HSBC-specific problem, mind you; Citibank and Standard Chartered have similarly weak ratios for hotels. We might just need to accept that we’ll never have a decent hotel points card in Singapore.

On the airline side, all three alliances are represented: Star Alliance (SIA, EVA) oneworld (BA, Cathay, Qantas) and SkyTeam (Air France/KLM, Vietnam).

In addition to mainstays like Singapore Airlines KrisFlyer and Cathay Pacific Asia Miles, it’s great to see British Airways Executive Club with their sweet spots for short-haul Economy travel. Don’t forget that British Airways Avios can also be used within Qatar Privilege Club too, which offers great value for Singapore-Europe/North America travel, with no fuel surcharges.

This will also be the first time Vietnam Airlines LotusMiles has partnered with a bank in Singapore. I don’t know a lot about this programme, but based on some quick research I don’t think there’s much to get excited about; award tickets cost significantly more during peak periods, there are fuel surcharges, and partner awards can’t be booked online.

What you should be excited about, however, are HSBC’s plans to ramp up its airline and hotel partner count over the rest of 2023. HSBC aims to have more than 20(!) airline and hotel partners by the end of 2023, including one name I can’t disclose now, but let me put it this way: if it happens, it’s going to make a lot of miles chasers very happy.

Lounge Visits

HSBC TravelOne Cardholders enjoy four complimentary lounge visits per calendar year, provided by DragonPass.

This is a relatively generous allowance for the segment in which the card competes.

| 🛋️ Entry-Level Miles Cards: Lounge Access | ||

| Card | Lounge Access? | Network |

| HSBC TravelOne Card |

✔ (4 per year) |

Dragon Pass |

| ✔ (4 per year) |

Plaza Premium | |

| ✔ (2 per year) |

Priority Pass | |

DBS Altitude Card DBS Altitude Card |

✔ (2 per year, Visa version only) |

Priority Pass |

| AMEX KrisFlyer Credit Card |

✖ | N/A |

| KrisFlyer UOB Credit Card |

✖ | N/A |

UOB PRVI Miles UOB PRVI Miles |

✖ | N/A |

| OCBC 90°N Card |

✖ | N/A |

Two interesting things to note.

First, the allowance is based on calendar year, not membership year. This means that a HSBC TravelOne Cardholder who gets approved in May 2023 will receive four visits to use from May to December 2023, then another four visits come 1 January 2024 (unused visits cannot be carried forward).

They could theoretically use up to eight lounge visits in their first membership year, regardless of whether they choose to renew the card.

Second, it’s interesting to see that HSBC is going with DragonPass for the TravelOne Card, since the HSBC Visa Infinite uses LoungeKey.

And yet I’m glad they have, because the DragonPass network is arguably more useful given Plaza Premium’s divorce from The Collinson Group (which runs Priority Pass and LoungeKey). DragonPass members can still access Plaza Premium Lounges as per normal, and at some airports (e.g. Kuching, Penang) that’s the sole contract lounge option.

Lounge visits can only be used by the principal cardholder, however. That’s a bit odd, since you can normally share allowances with other cards.

Travel Insurance

An expected feature, but still worth mentioning: HSBC TravelOne Cardholders who charge their air tickets to the card will receive complimentary travel insurance coverage (including COVID-19) of up to US$100,000, underwritten by HSBC Life.

This covers both the cardholder and their family.

HSBC has confirmed that coverage will also apply in situations where you redeem a ticket with miles and use the HSBC TravelOne Card to pay the taxes and surcharges.

Conclusion

| HSBC TravelOne Card |

||

| Apply Here |

What excites me most about the HSBC TravelOne Card is not its earn rates or lounge access, competitive though they may be. It’s the possibilities.

This card isn’t even one day old and it’s already dethroned Citi in terms of transfer partners, with plans to pull even further ahead as 2023 progresses. Granted, not all the new partners will be “useful” to miles chasers, and otherwise useful ones may have transfer ratios that negate their value. We simply don’t know at this point.

But I’m choosing to be optimistic here. After a steady diet of KrisFlyer and Asia Miles (nothing wrong with them, mind you), it’s refreshing to see the miles universe expanding in Singapore. New programmes mean new sweet spots, new routing rules, new quirks and loopholes that diligent users can leverage. It’s about time, if you ask me.

What’s missing here is the addition of a bonus category. With earn rates of 1.2/2.4 mpd, it would take a significant amount of spending to earn your way to a redemption. The next step here would be to expand the new partners to the HSBC Revolution, because that’s when things will truly fall into place.

What do you make of the new HSBC TravelOne Card?

No mention when the HSBC points will expire?

standard 37 month expiry policy, same as rest of hsbc cards. will update the post.

Does it work with amaze to hit the minimum spend of $800??? Cardup is excluded but not shown whether amaze spend is included.

hsbc has not excluded amaze- yet.

does paying annual fee renewal get you 10k miles?

NO

The article says lounge can be used by principal cardholder bringing their guest with them. But the T&C that’s linked doesn’t mention?

clarified with hsbc that lounge visits are only for principal cardholder. updated, thanks.

Aaron, I understand that HSBC Points can’t be transferred to new airline partners yet, but when do you think that will happen? Asking as my Revolution points expire in October. Thanks

i do not know.

can i pool them together with hsbc revo card?

points do not pool.

im assuming TravelOne Card and Revolution card cant be pooled?

Would the points here pool with Revolution? Thanks!

just saw it does NOT. thanks

why singsaver?

Can’t milelion run its own redemption program?

yeah why not have run your own redemption program

yeah why not have your own redemption program

yeah why not have run your own redemption program

yeah not have run your own redemption program

yeah why not have run your own redemption program

yeah why not have run your own redemption program

Great to see development in the miles game in Singapore. I hope HSBC joins the fray for premium cards, 120k and 500k segments as well!

Competition is only good for the consumer.

They already do have a 120K card?

The Visa Infinite

Exciting times!!!

Unless I’m forgetting anything, 2.4mpd for FCY is best in class right?

well SCB VI offers 3 mpd, but has a min spend of $2k. it would be best in class for a general spending card.

Hard pass for me if the points don’t pool. Never going to be earning enough miles to make sense.

Also why do cards like these and the revised Amaze come with those concave cut outs at the end?

tiny bit of comfort for pushing it into the card reader, and also helps users instantly tell which side to push in.

an accessibility feature for visually impaired individuals, it lets them know which end to insert

Interesting… but somewhat unconvinced that the broader list of transfer partners is worth skipping 4/6 mpd. I would love to be proven wrong though.

2 things ok? General vs category spending card

I know we shouldn’t just a credit card by its looks, but that’s a beautiful card design!

Actually, what interest me is the hotel points transfer. 10k initial pts on Accor that should be EUR200? Better than IHG 20k @ USD0.5cents/pts

Qatar Privilege Club does charge fuel surcharge:

these are award segment fees, not fuel surcharge. they’re annoying for sure, but nowhere as bad as YQ. *shrugs*

Now I wonder how they gonna upgrade their VI card given the poor earning rate on the card

Curious to know if any miles will be given upon renewal from 2nd year onwards.

Good card but sadly I think it doesn’t offer any annual fee renewal. I am wondering if it’s possible to get subsequent annual fee waive if not I may not hold this for long other than potential cardup exploit.

I mean amaze* exploit

Can you tell us which is the one partner which will make a lot of mile chasers happy? I promise not to tell anyone.

Transfer partner would be – just like the partnership HSBC has for EveryMile Credit Card in Hong Kong.

Frequent flyer programmes

Aeroplan

Asia Miles™

British Airways Executive Club Avios*

Etihad Guest

Emirates Skywards

Finnair Plus

Flying Blue

Infinity MileageLands*

Lotusmiles

Turkish Airlines Miles&Smiles

Qantas Frequent Flyer

Qatar Airways Privilege Club*

Singapore Airlines KrisFlyer*

Hotel loyalty programmes

ALL – Accor Live Limitless*

IHG® Rewards

Marriott Bonvoy™

Talking about a massive hype up heading, leading into a product that whilst good also comes with some major issues that means it fizzles out, and then an unspecified promise that it is goong to be so awesome later on at some unspecified point in the future. Quite a let down as you sift through how this product could have so easily been improved but as it is now is decidedly so-so. It is a bit sad that what is actually a decent product is going to be let down by uncertainty over one factor – annual fee. Is this… Read more »

thanks for taking the time to share your thoughts! some valid points here worth discussing. is it a perfect product? hardly- but few things are. Re: annual fee, we’ll need to see what happens towards the end of the first year, but let’s cross that bridge when we get to it. In the meantime, paying the first year AF gets you the sign-up bonus (even for existing customers, mind you- that’s very rare among banks), so it’s something I’m ok with. Obviously if the AF cannot be waived in the second year, there’ll be an exodus of cardholders- and then… Read more »

Pass for me. HSBC service & support sucks big time and this is where I don’t want to stuck with them.

Also the sign up offer 20,000 if I spend 600 & pay the annual fee. The cost of the mile is > 1c (including the 600). Payall can give me that without another card.

Waive annual fee liao

miles devaluation is so bad nowadays, paying such rates now also need to think twice

Is it me? or does the card looks like a world elite mastercard?

Not just you. It really looks like the logo- but it’s a world mc

Same. I think it’s coz the logo is silver, not the red and yellow one.

How about payment of NTU fee using the card?