Here’s The MileLion’s review of the HSBC TravelOne Card, which shook up the market when it launched in May 2023 with 12 transfer partners, free, instant points conversions, and a welcome bonus even existing HSBC cardholders could enjoy.

In the months that followed, the number of transfer partners grew to 20, points pooling was added, and free conversions — originally a limited-time perk — were made evergreen (thank goodness that absurdly-expensive 10,000 points conversion fee never saw the light of day!).

So does that make the HSBC TravelOne Card an essential addition to your wallet? Well, I can’t say that any non-4 mpd card is truly essential, but it’s certainly a capable general spending option. In the first year, with the welcome bonus and “extra” lounge visits (derived from tapping the second calendar year’s entitlement; more on this later), it’s hard to lose.

The earning potential is somewhat stunted by the lack of bonus categories and the exclusion of bill payment services like CardUp or ipaymy, but it can pair well with the 8 mpd HSBC Revolution. And even though HSBC is reportedly getting tough on annual fee waivers, it’s also increased the incentive for paying it.

Provided you’re not a “KrisFlyer-only” person, then the TravelOne would be worth some consideration.

HSBC TravelOne Card HSBC TravelOne Card |

|

| 🦁 MileLion Verdict | |

| First Year | Recurring |

| ☑ Take It ☐ Take It Or Leave It ☐ Leave It |

☐ Take It ☑Take It Or Leave It ☐ Leave It |

| What do these ratings mean? |

|

| Versatile points and a generous lounge benefit make the HSBC TravelOne Card a solid general spending option — though it’s not the card you want to earn KrisFlyer miles with. | |

| 👍 The good | 👎 The bad |

|

|

| 💳 Full List of Credit Card Reviews | |

Overview: HSBC TravelOne Card

Let’s start this review by looking at the key features of the HSBC TravelOne Card.

|

|||

| Apply | |||

| Income Req. | S$30,000 p.a. (with S$50K TRB) S$65,000 p.a. (otherwise) |

Points Validity | 37 months |

| Annual Fee |

S$196.20 |

Min. Transfer | 25,000 points (10,000 miles)^ |

| Miles with Annual Fee | 12,000 | Transfer Partners | 20 |

| FCY Fee | 3.25% | Transfer Fee | Free |

| Local Earn | 1.2 mpd | Points Pool? | Yes |

| FCY Earn | 2.4 mpd | Lounge Access? | Yes (4X) |

| Special Earn | N/A | Airport Limo? | No |

| Cardholder Terms and Conditions | |||

| ^After the first block of 10,000 miles, additional transfers are in blocks of 2 miles | |||

Fun fact: the HSBC TravelOne Card continues the trend towards “portrait-style” credit cards, designed vertically instead of horizontally. This supposedly allows for a smoother user experience, as it mimics how customers typically handle their cards when they tap to pay or dip the card into a chip reader. It’s even got a notch at the bottom, a thoughtful touch that’s designed as an accessibility feature for the visually-impaired (so they know which end they insert into the card reader).

But Apple and Google Pay wallets don’t support vertical card faces yet, so if you add it to your phone, you’ll see the secondary design that HSBC created, in landscape.

![]()

Despite its silver Mastercard logo, do note that the HSBC TravelOne Card is a World Mastercard and not a World Elite Mastercard.

How much must I earn to qualify for a HSBC TravelOne Card?

Back in October 2025, HSBC made a major change to the minimum income requirements for their entire suite of cards.

The HSBC TravelOne Card now has a minimum income requirement of:

- S$30,000 a year, for customers with a minimum Total Relationship Balance (TRB) of S$50,000

- S$65,000 a year, for everyone else

The S$50,000 does not necessarily have to be in a fixed deposit or savings account; you can use it to invest in equities, money market securities, insurance or whatever other products HSBC has to offer.

Still, that’s a significant hurdle for fresh graduates who don’t already have a pre-existing banking relationship with HSBC, and from what I understand, the bank is enforcing the requirement quite strictly.

How much is the HSBC TravelOne Card’s annual fee?

| Principal Card | Supp. Card | |

| First Year | S$196.20 | Free |

| Subsequent | S$196.20 | Free |

The HSBC TravelOne Card has an annual fee of S$196.20 for principal cardholders. All supplementary cards are free for life.

In subsequent years, the annual fee can be waived with a minimum spend of S$25,000 in the previous membership year.

It’s unclear just how strictly HSBC enforces this requirement because of the conflicting data points out there.

- Some cardholders (myself included) managed to get a fee waiver despite spending nowhere near S$25,000

- Other cardholders have been told that fee waivers will not be granted if the minimum spend is not met

- Still other cardholders have been told that fee waivers will not be granted and they must still pay the annual fee even if they cancel the card!

Needless to say, point (3) is absolute nonsense, and you shouldn’t accept it. The annual fee is charged in respect of the upcoming year, so if you decide to cancel your card after the first year, you should be getting a refund of the second year’s fee.

Two caveats to this. I’m assuming:

- You haven’t waited more than a month after the renewal date to cancel the card. If it’s been two or more months already, then the bank has a stronger case to deny you a fee waiver even if you cancel the card

- You haven’t redeemed any of the HSBC points credited for paying the second year’s annual fee. If so, then the bank has the right to charge you for those

If you fail to get a fee waiver, paying the second and subsequent years’ annual fees gets you 30,000 HSBC points (12,000 miles) from 1 January 2026 onwards (prior to which it was 25,000 HSBC points). This will be credited 2-3 months after the annual fee is charged.

For the avoidance of doubt, your annual lounge entitlements (see below) will be renewed even if the annual fee is waived. However, do remember that they are only renewed at the start of the calendar year, and not upon card renewal.

What sign-up bonus or gifts are available?

|

| Apply |

From now till 31 March 2026, customers who apply for a HSBC TravelOne Card will receive a welcome bonus of up to 33,600 miles, as summarised in the table below.

| New HSBC Cardholder | Existing HSBC Cardholder | |

| First S$500 Spend | 25,000 miles (62,500 HSBC points) |

13,000 miles (32,500 HSBC points) |

| Next S$500 Spend | 8,600 miles (21,500 HSBC points) |

8,600 miles (21,500 HSBC points) |

| Welcome Bonus | 33,600 miles (84,000 HSBC points) |

21,600 miles (54,000 HSBC points) |

Cardholders must meet a minimum spend of S$500 or S$1,000 by the end of the month following approval to receive the bonus miles.

In addition to meeting the minimum spend all applicants must also:

- Pay the first year’s S$196.20 annual fee

- Provide consent to receiving marketing and promotional materials during application (an important step that people often forget!)

The welcome bonus is in addition to the base miles that HSBC TravelOne Cardholders usually earn, namely 1.2 mpd for local currency spend, and 2.4 mpd for foreign currency spend.

For example, a new-to-HSBC cardholder who spends the full S$1,000 in foreign currency will receive a total of 36,000 miles (33,600 bonus, 2,400 base). This is the assumption that HSBC makes in its marketing materials, hence the advertised 36,000 miles figure.

HSBC defines new and existing cardholders as follows:

- New cardholders: Customers who do not hold any existing principal HSBC credit card, and have not cancelled a principal HSBC credit card in the past 12 months

- Existing cardholders: Customers whose most recent principal HSBC credit card was issued more than 12 months ago, and have not cancelled a principal HSBC credit card within the past 12 months

While other banks define an existing cardholder as anyone who doesn’t meet the new cardholder definition, HSBC does things a little differently.

To meet the “existing cardholder” definition, at least 12 months must have passed since your last principal HSBC credit card was approved, and you must not have cancelled any principal HSBC credit card in the past 12 months.

For example:

- John has a HSBC Revolution Card approved six months ago. He will not be eligible for the HSBC TravelOne Card’s existing cardholder welcome bonus

- Jack has a HSBC Revolution Card approved >12 months ago, and a HSBC Live+ Card approved >12 months ago. Last month, he cancelled his HSBC Live+ Card. He will not be eligible for the HSBC TravelOne Card’s existing cardholder welcome bonus either

Therefore, when it comes to HSBC, it’s possible that you’re neither new nor existing!

How many miles do I earn?

| 🇸🇬 SGD Spend | 🌎 FCY Spend | ⭐ Bonus Spend |

| 1.2 mpd | 2.4 mpd | N/A |

SGD/FCY Spend

HSBC TravelOne Card cardholders will earn:

- 3 HSBC points per S$1 (1.2 mpd) on local spend

- 6 HSBC points per S$1 (2.4 mpd) on foreign currency spend

Remember, the actual earn rates depend on the partner you choose, because different partners have different conversion ratios (I cover this in more detail later in the review).

Assuming 1.2/2.4 mpd rates, however, this would make the HSBC TravelOne Card one of the better general spending cards in Singapore.

| 💳 Earn Rates for General Spending Cards (Income Req: S$30K) |

||

| Cards | Local Spend | FCY Spend |

UOB PRVI Miles Card UOB PRVI Miles CardApply |

1.4 mpd | 3 mpd IDR, MR, THB, VND 2.4 mpd All Others |

BOC Elite Miles Card BOC Elite Miles CardApply |

1.4 mpd | 2.8 mpd |

| HSBC TravelOne Card Apply |

1.2 mpd | 2.4 mpd |

DBS Altitude Card DBS Altitude CardApply |

1.3 mpd | 2.2 mpd |

OCBC 90°N Card OCBC 90°N CardApply |

1.3 mpd | 2.1 mpd |

Apply |

1.2 mpd | 2.2 mpd |

StanChart Journey Card StanChart Journey CardApply |

1.2 mpd | 2 mpd |

AMEX KrisFlyer Ascend AMEX KrisFlyer AscendApply |

1.2 mpd | 1.2 mpd |

KrisFlyer UOB Credit Card KrisFlyer UOB Credit CardApply |

1.2 mpd | 1.2 mpd |

AMEX KrisFlyer Credit Card AMEX KrisFlyer Credit CardApply |

1.1 mpd | 1.1 mpd |

Bonus Spend

Unfortunately, the HSBC TravelOne Card does not have a bonus earn category.

Those who want to rack up HSBC points more quickly should pair this card with the HSBC Revolution to tap its higher earning power of up to 8 mpd.

What is the FCY transaction fee?

All FCY transactions are subject to a 3.25% fee, which is on par with the market.

| 💳 FCY Fees by Issuer and Card Network |

||

| Issuer | ↓ MC & Visa | AMEX |

| Standard Chartered | 3.5% | N/A |

| American Express | N/A | 3.25% |

| Citibank | 3.25% | N/A |

| DBS | 3.25% | 3% |

| HSBC | 3.25% | N/A |

| Maybank | 3.25% | N/A |

| OCBC | 3.25% | N/A |

| UOB | 3.25% | 3.25% |

| BOC | 3% | N/A |

| CIMB | 3% | N/A |

With a 2.4 mpd earn rate and a 3.25% FCY fee, using the HSBC TravelOne Card overseas represents buying miles at 1.35 cents apiece.

It is possible to pair the HSBC TravelOne Card with Amaze to enjoy better conversion rates, but you’ll earn 1.2 mpd instead of 2.4 mpd, since Amaze converts transactions into SGD. Based on Amaze’s ~2% spread, the cost per mile is actually higher at 1.67 cents apiece, so I would not recommend pairing it.

When are HSBC Rewards Points credited?

HSBC Rewards Points are credited when the transaction posts, usually in 1-3 days.

How are HSBC Rewards Points calculated?

Here’s how you can work out the HSBC Rewards Points earned on your HSBC TravelOne Card.

| Local Spend (3x) | Multiply by 1, round to the nearest whole number. Multiply by 2, round to the nearest whole number. Add both figures |

| FCY Spend (6x) |

Multiply by 1, round to the nearest whole number. Multiply by 5, round to the nearest whole number. Add both figures |

The minimum spend required to earn points is S$0.25 (SGD) and S$0.10 (FCY) respectively.

This means that the HSBC TravelOne Card (1.2 mpd) can outperform the ostensibly higher earning UOB PRVI Miles Card (1.4 mpd) in certain circumstances, depending on transaction size.

| HSBC TravelOne Card 1.2 mpd |

UOB PRVI Miles Card UOB PRVI Miles Card1.4 mpd |

|

| S$5 | 6 miles | 6 miles |

| S$9.99 | 12 miles | 6 miles |

| S$15 | 18 miles | 20 miles |

| S$19.99 | 24 miles | 20 miles |

| S$25 | 30 miles | 34 miles |

| S$29.99 | 36 miles | 34 miles |

If you’re an Excel geek, here’s the formulas you need to calculate points:

| Local Spend | =ROUND(X*1,0) + ROUND(X*2,0) |

| FCY Spend |

=ROUND(X*1,0) + ROUND(X*5,0) |

| Where X= Amount Spent |

|

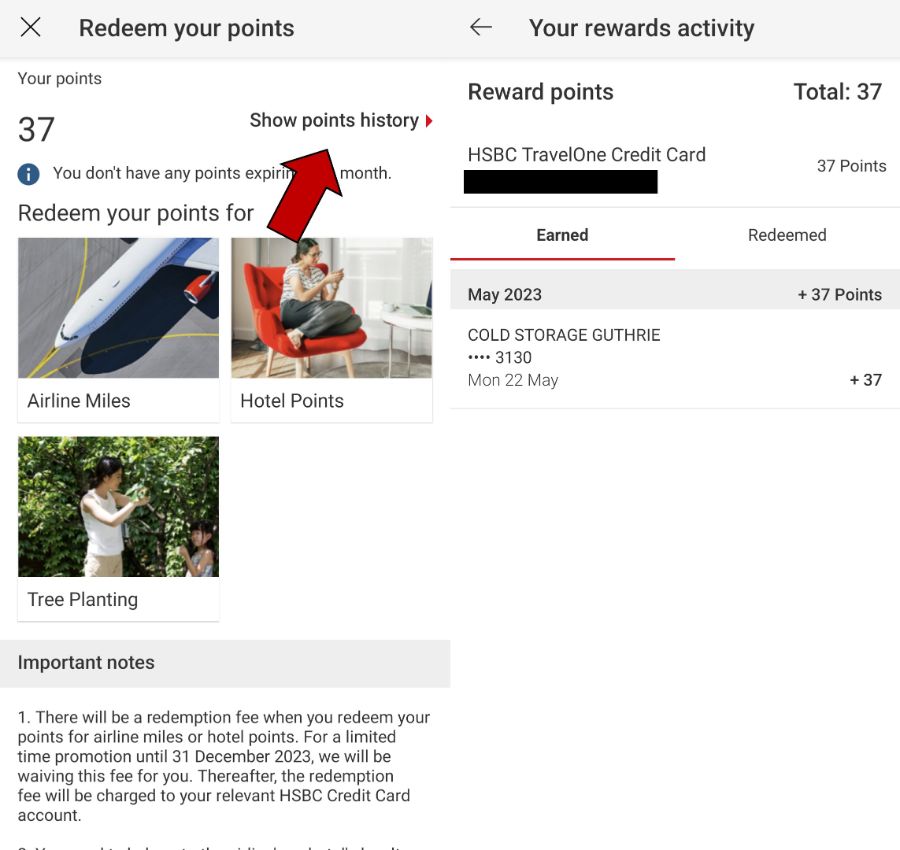

HSBC provides transaction-level points breakdowns, which can be found on the HSBC mobile app. To view this, log in to the HSBC mobile app and tap on your HSBC TravelOne Credit Card > Redeem Your Points

On the next screen, tap ‘Show points history’, and you’ll see a breakdown of points earned per transaction.

For the full list of formulas that banks use to calculate credit card points, do refer to these articles:

What transactions aren’t eligible for HSBC Rewards Points?

A full list of transactions that do not earn HSBC Points can be found in the T&Cs (at Point 3).

I’ve highlighted a few noteworthy categories below:

- Charitable Donations

- Education

- Government Services

- GrabPay top-ups

- Hospitals

- Insurance

- Professional services providers (e.g. Google & Facebook Ads, AWS)

- Real Estate Agents & Managers

- Utilities

HSBC also excludes CardUp, ipaymy and RentHero transactions from earning points. In a way, this does compound the problem of the lack of a bonus category, since you couldn’t even buy additional HSBC Points via these payments services if you were so inclined.

What do I need to know about HSBC Rewards Points?

| ❌ Expiry | ↔️ Pooling | 💰 Transfer Fee |

| 37 months | Yes | Free |

| ⬆️ Min. Transfer | ✈️ No. of Partners | ⏱️ Transfer Time |

| 10,000 miles (2 miles after) |

20 | Instant* |

| *For all partners except Hainan and JAL | ||

Expiry

All HSBC points expire at the end of a 37-month period which commences from the month subsequent to the month in which the points were earned.

For the purpose of illustration:

| Points earned in the period of | Expiry date |

| 1-31 August 2023 | 30 September 2026 |

| 1-30 September 2023 | 31 October 2026 |

| 1-31 October 2023 | 30 November 2026 |

Pooling

In May 2024, HSBC added points pooling to its cards, bringing them all onto the same platform.

Therefore, if you have 10,000 HSBC Points on the HSBC TravelOne Card, and 15,000 HSBC Points on the HSBC Revolution Card, you can redeem a combined balance of 25,000 HSBC Points.

Do note that even though HSBC Points pool, you will lose any unutilised points if you cancel a card. Be sure to cash them out before cancelling.

Transfer Partners & Fees

The HSBC TravelOne Card launched with 12 airline and hotel partners, a number that has now increased to 20. This is by far the most programmes offered by any bank in Singapore.

| ✈️ HSBC TravelOne Airline Partners | |

| Frequent Flyer Programme | Conversion Ratio (HSBC Points : Partner) |

| 50,000 : 10,000 | |

| 35,000 : 10,000 | |

| 35,000 : 10,000 | |

| 35,000 : 10,000 | |

| 35,000 : 10,000 | |

| 35,000 : 10,000 | |

| 30,000 : 10,000 |

|

|

30,000 : 10,000 |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 |

|

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

|

25,000 : 10,000 |

| 🏨 HSBC TravelOne Hotel Partners | |

| Hotel Programme | Conversion Ratio (HSBC Points : Partner) |

|

30,000 : 10,000 |

| 25,000 : 5,000 | |

| 25,000 : 10,000 | |

| 25,000 : 10,000 | |

The catch is that not all partners share the same transfer ratios. With airlines, for instance, the ratio ranges from 25,000 – 50,000 points : 10,000 miles.

This is important, because the TravelOne Card’s advertised earn rates of 1.2/2.4 mpd only apply if you choose a partner with a 25,000 points : 10,000 miles ratio. The earn rates drop as the transfer ratio worsens, going as low as 0.6/1.2 mpd at the other end of the spectrum.

| Transfer Ratio (Points : Miles) |

HSBC T1 (Local)* |

HSBC T1 (FCY)^ |

| 25,000 : 10,000 (8x partners) |

1.2 mpd | 2.4 mpd |

| 30,000 : 10,000 (2x partners) |

1 mpd | 2 mpd |

| 35,000 : 10,000 (5x partners) |

0.86 mpd | 1.71 mpd |

| 50,000 : 10,000 (1x partner) |

0.75 mpd | 1.5 mpd |

| 50,000 : 10,000 | 0.6 mpd | 1.2 mpd |

| *3 points per S$1 on local spend ^6 points per S$1 on FCY spend |

||

It’s especially important to highlight that the transfer ratio for Singapore Airlines KrisFlyer was devalued to 30,000 points : 10,000 miles on 16 January 2025, which makes the HSBC TravelOne Card a 1/2 mpd card if KrisFlyer miles are your goal. Needless to say, you can do much better with other alternatives, and if you only want to earn KrisFlyer miles, this isn’t the card for you.

Cardholders will need to convert a minimum of 10,000 miles. However, the subsequent conversion block drops to just 2 miles after that, which means you could convert 10,002 miles, or 200,006 miles for instance. This is a great feature, because it helps avoid the problem of orphan miles. So long as you keep at least 10,000 miles in your account, you can cash out your entire balance with almost nothing left behind.

All conversion fees are waived until further notice.

Transfer Time

All HSBC Points transfers are processed instantly, with the exception of:

- Hainan Airlines Fortune Wings Club (5 working days)

- JAL Mileage Bank (10 working days)

Other card perks

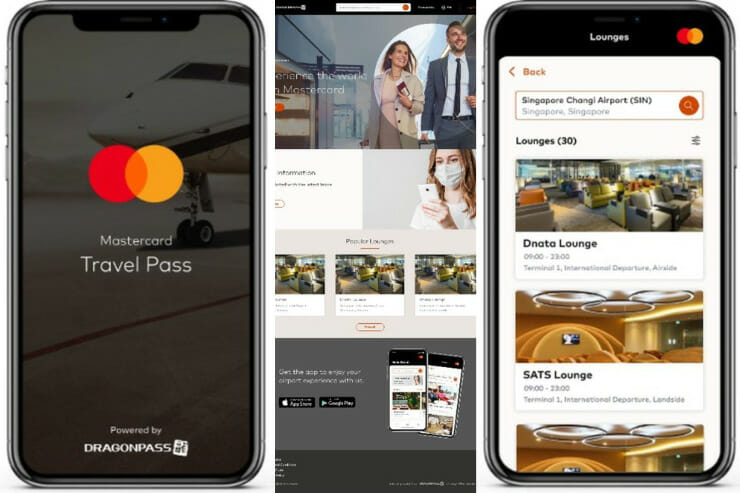

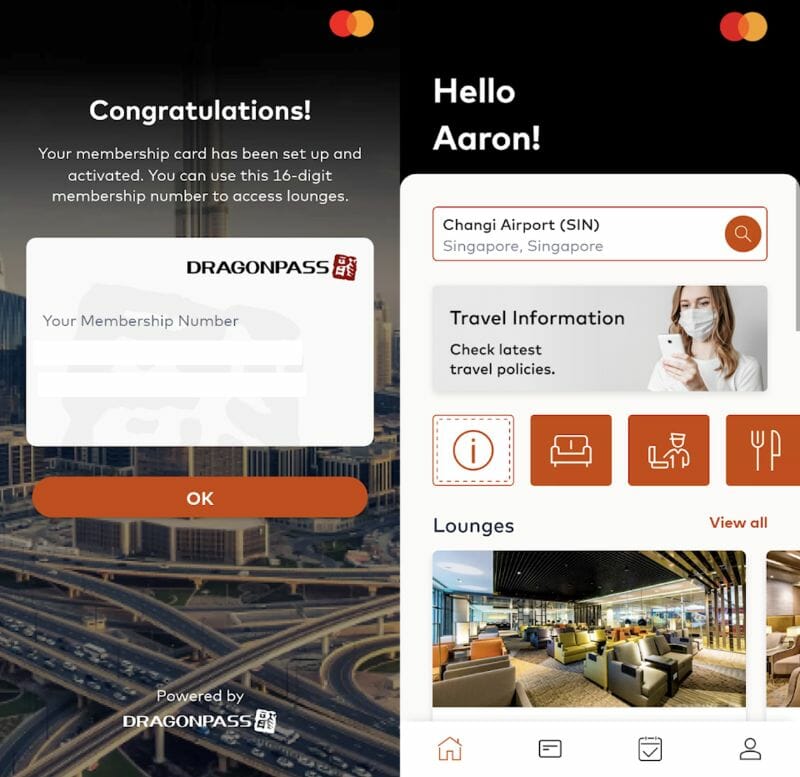

Four complimentary lounge visits

|

|

| Lounge Benefit T&Cs |

Principal HSBC TravelOne Cardholders enjoy four complimentary lounge visits per year, provided via DragonPass.

Effective 17 October 2024, lounge visits can be shared with a guest or guests. For example, a cardholder with one guest could visit two times, and a cardholder with three guests could visit one time.

Allowances are awarded by calendar year, which means you can enjoy up to eight visits in your first membership year. For example, if your card is approved in June 2025, you will be awarded:

- On date of approval: 4 visits (expires 31 December 2025)

- On 1 January 2026: 4 visits (expires 31 December 2026)

Allowances cannot be rolled over to the following year, so be sure to fully utilise your visits by the end of the calendar year.

Here’s how to start enjoying the benefit:

- Step 1: Download Mastercard Travel Pass app (Android | iOS)

- Step 2: Select ‘Sign up’ to register for the programme, or log on to your account if you’re already a member

- Step 3: Enter your HSBC TravelOne Card details for a one-time verification

- Step 4: Complete your personal details for Mastercard Travel Pass account registration (enter your name as shown in your passport)

- Step 5: Set your account password

Four visits is relatively generous for an entry-level credit card.

| 💳 Credit Cards with Airport Lounge Access (Income Req.: S$30K p.a.) |

||

| Card | Network | Free Lounge Visits (per year) |

| HSBC TravelOne Card Apply |

DragonPass | 4 CY Share |

| UOB PRVI Miles Card Apply |

Priority Pass | 4 CY No Share |

Apply |

Priority Pass | 2 CY Share |

DBS Altitude Visa DBS Altitude VisaApply |

Priority Pass | 2 MY Share |

| StanChart Journey Card Apply |

Priority Pass | 2 MY Share |

| Legend | ||

| Whether visits are tracked by calendar year CY or membership year MY Whether lounge visits can or can’t be shared with guests Share No Share |

||

Entertainer with HSBC

|

| ENTERTAINER with HSBC |

Principal HSBC TravelOne Cardholders receive a complimentary ENTERTAINER with HSBC app membership, which includes:

- 1-for-1 dine-in offers at more than 150 merchants across Singapore, including Sushi Jiro @ PARKROYAL COLLECTION, Bangkok Jam, Paul Bakery and more

- 1-for-1 takeaway offers at more than 50 merchants including Canadian 2 For 1 Pizza, Andersen’s of Denmark and more

- Up to 50% off leisure, attraction and wellness offers at BOUNCE Singapore, Spa Infinity, Virtual Room and more

- 1-for-1 stays in rooms at over 175 hotels around the world

You’ll need an activation key to start using your ENTERTAINER membership. This should have been emailed to you; if not you’ll need to call 1800 4722 669 to get it from customer service.

Complimentary travel insurance

| Accidental Death | S$75,000 |

| Medical Expenses | S$150,000 |

| Travel Inconvenience | Flight Delay: S$150 Baggage Delay: S$1,500 Lost Baggage: S$1,500 |

| Policy Wording | |

Principal and supplementary HSBC TravelOne Cardholders receive complimentary travel insurance when they:

- Use their TravelOne Card to purchase air tickets, or

- Use their TravelOne Card to pay for the taxes and surcharges on a ticket redeemed with airline miles

This provides coverage of S$75,000 for accidental death, S$150,000 for overseas medical expenses, S$1 million for emergency medical evacuation, as well as coverage for travel inconveniences like flight delays and lost luggage.

Do note that there is no coverage for personal liability or rental vehicle excess, so you may need to purchase supplementary coverage if this is important to you.

Summary Review: HSBC TravelOne Card

|

|

| Apply | |

| 🦁 MileLion Verdict | |

| First Year | Recurring |

| ☑ Take It ☐ Take It Or Leave It ☐ Leave It |

☐ Take It ☑Take It Or Leave It ☐ Leave It |

| What do these ratings mean? |

|

The HSBC TravelOne Card is a solid general spending option, offering a decent welcome bonus and up to eight lounge visits in the first membership year— more than enough to cover the S$196.20 annual fee. What’s more, with 20 airline and hotel partners, free and instant conversions, and conversion blocks as small as two miles, HSBC Points are extremely versatile.

From the second year onwards it’s a bit more marginal, but the 30,000 HSBC points received for paying the annual fee are worth 6,000 Accor points, or €120 (~S$177). Together with four additional lounge visits, it might still be worthwhile.

The key weaknesses of this card are its relatively low earn rate for local spending, with no bonus categories or miles purchase facility to accelerate your earnings. Also, this is not the card to use if you want to earn KrisFlyer miles, following the devaluation to the transfer ratio in early 2025.

What do you make of the HSBC TravelOne Card?

anyone know if AXS pay+earn also contributes to the $800 spend offer?

Hi Milelion! Thanks for the solid write-up.

By the way, in the above section “What sign-up bonus or gifts are available?”, the minimum qualifying spend seems to have increased to SGD1,000, from SGD800. As it is mentioned in HSBC’s “Terms and Conditions for the HSBC TravelOne Credit Card Sign up Promotion for 1 September 2023 to 31 December 2023”.

Raising this up to prevent confusion among readers.

Cheers~

thanks! will get that updated.

When will the TravelOne card annual fee for the bonus points be charged? I don’t see the annual fee showing on my statement yet after 2 months. If so how do I qualified for the bonus points? Any Idea?

Same question though different promo! 🙂 I just applied and spent the $500 needed. When will I need to pay for the annual fee to get the 30k miles?

usually charged about 2-3 months after approval

hi Milelion, would u be in the know on whether the pooling would still happen by year end (aka 123123)?

i don’t have any info on this at the moment.

Hi Aaron,

this is a great article! Quick questions for the EGA cashback eligibility, referring to HSBC EGA T&C art 5a (i)

From above T&C, it seems only transactions in SGD are eligible for 1% cashback, not the FCY transactions. Kindly advise. Thank you!

Aaron, I think there’s something missing from your review: HSBC T1 is, in a vacuum, technically, the best non-SGD general spend card in the market, because it earns the same non-SGD rate as UOB PRVI Miles and it has much better rounding. This is currently irrelevant because you only get orphan miles, but it would become useful if T1 and Revolution miles suddenly pool. If you took Milelion advice and got T1 for the signup bonus miles, should you cancel the card then consider reapplying if pooling is implemented? In practice, most people will still get UOB PRVI Miles because… Read more »

So is there any reason to use the T1 (assuming you get a fee waiver from heavy Revolution use) instead of the UOB PRVI Miles or Citi Premier Miles as your general spend card given the better transfer partners and pooling with Revolution?

Probably moot if your CardUp spend gets you a DBS Vantage fee waiver

Actually, need to consider if T1 is the better overseas general spend card

Why bother & the fuss about annual fee waiver when you can afford? 🙄

Why bother using a credit card when you can afford to pay off your flight tickets using cash?

Understand from Mile Lion that the 2nd year fee waiver is near impossible to waive, same experience when I called HSBC as well. Any lucky few managed to waive 2nd year annual fee and what reason did you give? HSBC told me needed to spend 25k in one year to get it waive.

The table at the top of the article still says points don’t pool – needs to be updated!

yes, that will be updated in the 2024 version.

Surprisingly, I’m still receiving the 1% Everyday+ Cashback of all my HSBC CC spending after 2 May. Is that a lucky bug?

yes. enjoy it while it lasts.

AirAsia conversion seems to be 12500:10000, worth it to convert?

In order to be eligible for the welcome bonus, do we need to click all at the marketing consent? what if i opt out the call option but click the rest?

I just called for fee waiver and they offered me 25k points for paying the fee. I declined as I have exhaused the 4 lounge visits in 2024 & have to wait for 2025 to reset.

can i use cardup for the min spend needed for the welcome bonus?

can I ask if supplementary card holder is able to enjoy the lounge as well?

Hi Milelion, thanks for the write up! (: super helpful. Can i ask if you’re aware when the bonus miles will be credited upon making the qualifying spending?

Tried to get a fee waiver today but got rejected, call services staff mentioned that for HSBC TravelOne, the annual fee is STRICTLY not waivable 🙁

I applied this card this year July and was charged the membership in Oct. I tried to waive but was rejected as well. what happened to the 1st year free waiver mentioned in this article?

Hi can I use it with Amaze and still earn points?

Article needs a tiny update : UOB Prvimiles now has 4 Priority Pass visits per year 🙂

I made sure I cancelled it 2 months before annual fee due so that I dont get that problem of being forced to pay annual fee.

Any idea for the welcome bonus, will FCY fees be counted in the $1000 spending required?