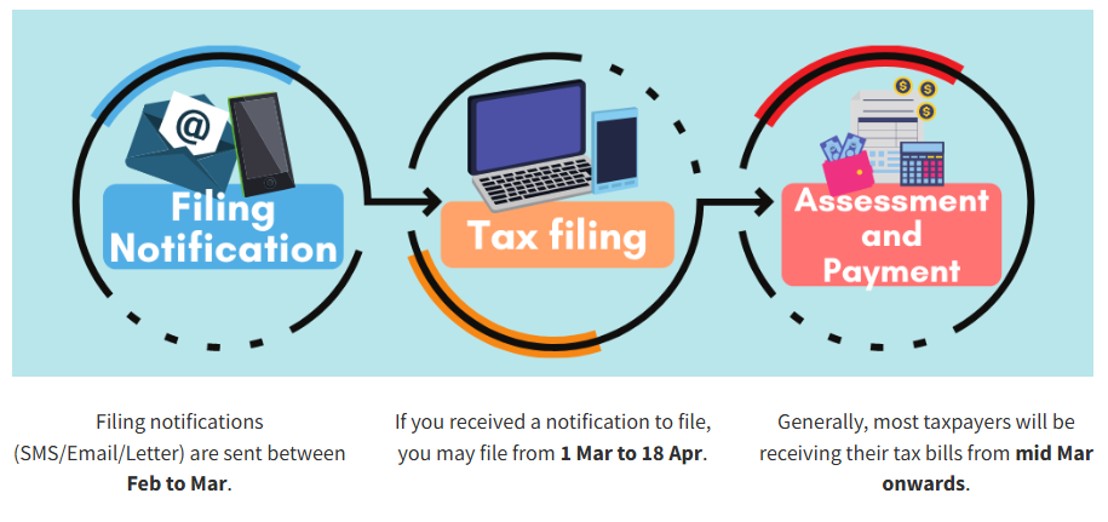

The YA 2026 income tax season is now underway, and individuals will need to file their taxes by 18 April 2026.

Tax bills, otherwise known as Notice of Assessments (NOAs), will then be sent in batches between mid-March and September 2026. If you haven’t received yours yet, don’t worry— I promise they haven’t forgotten about you!

While I don’t think anyone particularly relishes receiving their NOA, here’s the good news: if you don’t mind paying a small admin fee, tax season is a great opportunity to earn some extra miles.

In this guide, I’ll walk you through the various methods of doing so, as well as the all-important cost per mile.

|

| Tax Season 2026 |

| 💰 The MileLion’s Income Tax Guide 2026 |

How do I pay my income tax bill with a credit card?

IRAS does not accept credit card payments. In their own words:

Credit card payments are not offered by IRAS directly because of the high transaction costs charged by the credit card service providers. This is to keep the cost of collection low to preserve public funds.

-IRAS

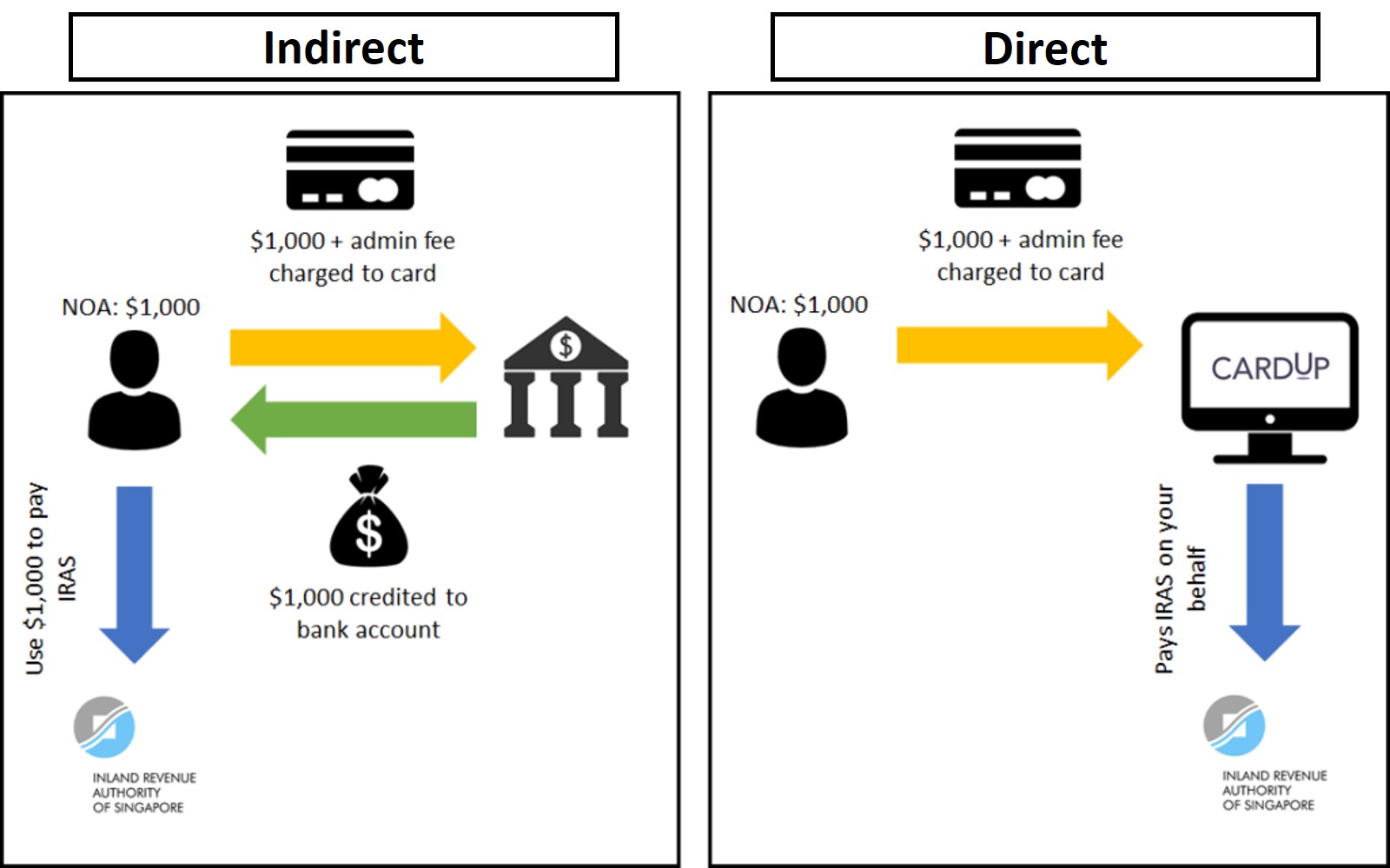

However, this doesn’t mean you can’t use your credit card to pay taxes. Banks and bill payment platforms offer tax payment facilities, which allow cardholders to earn rewards on taxes in exchange for a small fee.

I divide these into two categories: indirect and direct.

| Indirect Payment Facilities | Direct Payment Facilities |

|

|

|

|

Both indirect and direct facilities work the same in the sense that your credit card is charged for the tax amount plus an admin fee, earning miles in the process.

Where they differ is that:

- An indirect payment facility deposits the amount due into your designated bank account, in cash. You are still responsible for paying IRAS

- A direct payment facility pays IRAS on your behalf

Whether it’s better to use an indirect or direct facility all comes down to the cost per mile: the admin fee, divided by the miles earned.

What are the fees involved?

Here’s a list of the various payment facilities and the applicable fees.

| 🧾 List of Payment Facilities |

||

| Bank | Applicable Cards | Admin Fee |

Direct |

All cards except BOC, HSBC | 1.75% |

Link Indirect |

UOB PRVI Miles, Visa Infinite Metal, Reserve, KF UOB | 1.6-1.8% |

Link LinkDirect |

All StanChart cards | 1.9% |

Link Indirect |

StanChart Beyond, Visa Infinite | 1.9% |

MP3 for Income Tax Direct |

All DBS cards | 2.5% |

Link LinkDirect |

All Citi cards | 2.6% |

| There is an additional option called ipaymy, but for reasons outlined in this post, I neither endorse nor comment on their services. However, I’ll mention them in the cost per mile table later on to the extent it offers the lowest cost per mile for a given card. | ||

While I’ve sorted the table above on the basis of admin fees, that’s only half the story. A lower fee doesn’t necessarily mean cheaper miles; you need to also consider the earn rate.

This can be confusing, because banks may offer different earn rates for income tax payments as opposed to regular retail spend. For example:

- All UOB cards earn a flat 1 mpd for payments via the UOB Payment Facility, instead of their usual rates

- All DBS cards earn a flat 1.5 mpd for income tax payments, instead of their usual rates

To illustrate why it’s insufficient to compare options on the basis of admin fees alone, consider the following example:

| Method | Admin Fee | Earn Rate | CPM |

| DBS MP3 | 2.5% | 1.5 mpd | 1.67¢ |

| Citi PayAll |

2.6% | 1.6 mpd Ultima |

1.63¢ |

While Citi PayAll (2.6%) has a higher admin fee than DBS MP3 (2.5%), the cost per mile when paired with a Citi ULTIMA Card (1.63 cents) is lower than DBS MP3 (1.67 cents).

If this is too complicated for you, I’ve done the calculations later on in this article for every major miles-earning card.

What’s changed for YA 2026?

Here’s a summary of the key changes that have taken place since last year’s article.

BOC: No more miles for CardUp/ipaymy

On 1 July 2025, the BOC Elite Miles Card was overhauled to offer 1.4 mpd on local spend (up from 1 mpd) and 2.8 mpd on FCY spend (up from 2 mpd), without any minimum spend or cap.

Unfortunately, this came at the expense of CardUp and ipaymy, both of which were added to the exclusion list on the same day.

CardUp: No more points for DBS/UOB-issued AMEX cards

![]()

From 1 April 2026, DBS- and UOB-issued AMEX cards no longer earn rewards with CardUp.

It’s worth noting that this is not a bank-initiated nerf. You won’t find any announcement about it on the DBS or UOB websites. Rather, it’s a network-initiated restriction, one that I imagine CardUp doesn’t like, but has little choice but to abide by.

This removes the possibility of using CardUp with the DBS Altitude AMEX, DBS Treasures Black Elite AMEX and UOB PRVI Miles AMEX.

OCBC VOYAGE Payment Facility: Retired

Last year, OCBC officially retired the VOYAGE Payment Facility. This “pay anything” facility allowed OCBC VOYAGE Cardholders to purchase miles from 1.9 to 1.95 cents each, no questions asked (similar to the UOB Payment Facility).

It’s been clear for several years now that OCBC has been pivoting towards CardUp as a bill payment solution, so it’s unsurprising that the VOYAGE Payment Facility has been sunset. It’s no big loss, if you ask me, given the relatively high cost per mile and the devaluation of VOYAGE Miles for airfare offsets.

SC EasyBill: One payment per category per month

In December 2025, Standard Chartered quietly nerfed its SC EasyBill payment service by capping customers at one bill payment per category, per month.

| Category | Examples |

| Tax Payments |

|

| Education |

|

| Insurance |

|

| Rent |

|

This means you can no longer use SC EasyBill to pay both personal income tax and property tax in the same month, or personal income tax and corporate income tax (for those who own a company and pay themselves a salary).

This usage cap will be particularly significant for StanChart Beyond Cardholders, as one of the card’s key attractions is the ability to buy miles at 0.95 cents each via SC EasyBill (1.9% fee, 2 mpd for Priority Banking and Priority Private clients). Moreover, SC EasyBill transactions count towards the S$20,000 minimum spend for the 100,000 miles welcome offer.

What promotions are available?

CardUp

| Code | MLTAX26R |

| Limit | 2x redemptions per user; no overall redemption cap |

| Admin Fee | 1.75% |

| Min. Spend | None |

| Cap | None |

| Schedule By | 12 June 2026, 6 p.m (SGT) |

| Due Date | 7 May to 17 June 2026 |

| Eligible Cards | Visa, UnionPay |

| Eligibility | New & Existing users |

| MLTAX26R T&Cs | |

New and existing CardUp customers can use the promo code MLTAX26R to enjoy a 1.75% fee for recurring income tax payments.

This code is valid for up to two redemptions per user, for payments that are:

- Scheduled by 12 June 2026, before 6 p.m

- With due dates between 7 May and 17 June 2026

The second bullet point isn’t a typo— while this is described as a promotion for recurring payments, it really covers only two payments: one in May (for June 2026’s instalment), and one in June (for July 2026’s instalment).

CardUp will roll out another offer after June for users who want to continue with recurring income tax payments. So for now, you can just schedule recurring payments for May and June, and reassess the situation when the new promo code is unveiled.

If you have a tax payment that is S$40,000 or larger, you can contact CardUp at hello@cardup.co for special pricing.

| 💳 Targeted 1.7% offer |

| In addition to the public offer, CardUp has sent out emails offering targeted customers a 1.7% admin fee on a one-off tax payment with the code 170TAX2026. Check your inbox to see if you were selected to participate. |

Citi PayAll

Citi PayAll has yet to launch its income tax promotion for 2026.

In 2025, Citi PayAll offered 1.8 mpd on tax payments, though customers also had to spend a minimum of S$6,000 on non-tax payments at 1.6 mpd. Depending on the overall mix of tax and non-tax payments, the cost per mile ranged from 1.44 to 1.63 cents.

Standard Chartered Payment Facility & EasyBill

From 1 April to 30 June 2026, the Standard Chartered Income Tax Payment Facility is offering a 100% rebate of the administrative fee for Beyond and Visa Infinite cardholders, capped at S$200 per cardholder. This is equivalent to free miles on a tax payment of up to S$10,526.

However, this is capped at just 25 participants per month, so you’ll want to apply as early in the month as possible, preferably just after midnight on the 1st of each month. Honestly, it’s a gamble more than anything.

Standard Chartered offering S$200 cashback on income tax payments for Beyond and Visa Infinite

We have yet to see an offer for SC EasyBill so far. 2025’s offer featured a 100% rebate of the administrative fee for tax payments, capped at S$200 per cardholder for the first 50 applicants each month.

UOB GIRO promotion

While you can’t earn miles this way, it’s still worth noting that from 1 April 2026 to 31 March 2027, UOB customers can enjoy a 6% rebate tax and other bill payments made through GIRO.

| Category | Eligible Merchants |

| Tax |

|

| Insurance |

|

| Utilities |

|

| Telco |

|

To earn this rebate, customers will need to complete the following three steps:

- Register their mobile number for PayNow on UOB TMRW

- Activate Money Lock on UOB TMRW (minimum S$1 lock amount)

- Apply for the GIRO monthly payment plan through the relevant organisation, selecting an eligible account for deduction

Eligible accounts are defined as the following:

- KrisFlyer UOB Account

- UOB One Account

- UOB Lady’s Savings Account

- UOB Uniplus Account

If these criteria are met, customers will receive a 6% rebate on the deducted GIRO amount, with the monthly cap determined by the MAB in the account.

| Account MAB | Rebate | Monthly Cap |

| ≥S$30K and <S$75K | 6% | S$10 |

| ≥S$75K and <S$150K | 6% | S$25 |

| ≥S$150K | 6% | S$50 |

For example, if a UOB One Accountholder with a MAB of S$150,000 pays an eligible GIRO bill worth S$800, he can expect to receive a S$48 cash rebate.

If you have multiple eligible accounts, you are entitled to earn multiple payment rebates, subject to each account satisfying its own eligibility conditions.

UOB offering 6% rebate for taxes, utilities, telco and insurance bills paid via GIRO

UOB Payment Facility

![]()

From 1 March to 31 May 2026, the UOB Payment Facility is running a promotion that allows cardholders to purchase unlimited miles from 1.6 to 1.8 cents each, depending on card. As this is a “pay anything” facility, however, UOB doesn’t really care what you use the funds for, and it doesn’t matter what size your tax bill is.

Think of this as a way of topping up your account further, after you’ve exhausted the cheaper options.

UOB Payment Facility offering unlimited miles at 1.6-1.8 cents each

What’s the cost per mile?

In the table below, I’ve ranked credit cards by the lowest possible price you can pay for miles, denoted by CPM (cost per mile, in cents).

I’m not displaying any AMEX options at the moment (except the UOB PRVI Miles AMEX), as there are no ongoing offers for tax payments.

| 💰 Summary of Tax Payment Options |

|||

| Card | Pay Via | Fee (MPD) |

CPM |

StanChart Beyond StanChart Beyond(PB/PP) Apply |

SCB | 1.9% 2 mpd |

0.95¢ |

Citi ULTIMA Visa Citi ULTIMA VisaApply |

CardUp | 1.75% 1.6 mpd |

1.07¢ |

DBS Insignia DBS InsigniaApply |

CardUp | 1.75% 1.6 mpd |

1.07¢ |

OCBC VOYAGE OCBC VOYAGE Premier, PPC, BOS Apply |

CardUp | 1.75% 1.6 mpd |

1.07¢ |

UOB Reserve UOB ReserveApply |

CardUp | 1.75% 1.6 mpd |

1.07¢ |

Apply |

CardUp | 1.75% 1.5 mpd |

1.15¢ |

Citi ULTIMA MC Citi ULTIMA MCApply |

IPM | 1.99% 1.6 mpd |

1.22¢ |

UOB PRVI Miles Visa UOB PRVI Miles VisaApply |

CardUp | 1.75% 1.4 mpd |

1.23¢ |

UOB Visa Infinite Metal UOB Visa Infinite MetalApply |

CardUp | 1.75% 1.4 mpd |

1.23¢ |

StanChart Visa Infinite StanChart Visa InfiniteApply |

CardUp | 1.75% 1.4 mpd* |

1.23¢ |

| StanChart Beyond Card (Regular) Apply |

SCB | 1.9% 1.5 mpd |

1.26¢ |

DBS Altitude Visa DBS Altitude VisaApply |

CardUp | 1.75% 1.3 mpd |

1.32¢ |

OCBC VOYAGE OCBC VOYAGEApply |

CardUp | 1.75% 1.3 mpd |

1.32¢ |

OCBC 90°N MC OCBC 90°N MCApply |

CardUp | 1.75% 1.3 mpd |

1.32¢ |

OCBC 90°N Visa OCBC 90°N VisaApply |

CardUp | 1.75% 1.3 mpd |

1.32¢ |

OCBC Premier Visa Infinite OCBC Premier Visa InfiniteApply |

CardUp | 1.75% 1.28 mpd |

1.34¢ |

UOB PRVI Miles MC UOB PRVI Miles MCApply |

IPM | 1.99% 1.4 mpd |

1.40¢ |

Citi Premier Miles Visa Citi Premier Miles Visa |

CardUp | 1.75% 1.2 mpd |

1.43¢ |

Maybank Visa Infinite Maybank Visa InfiniteApply |

CardUp | 1.75% 1.2 mpd |

1.43¢ |

StanChart Journey StanChart JourneyApply |

CardUp | 1.75% 1.2 mpd |

1.43¢ |

Citi Prestige Citi PrestigeApply |

IPM | 1.99% 1.3 mpd |

1.50¢ |

KrisFlyer UOB KrisFlyer UOBApply |

IPM | 1.99% 1.2 mpd |

1.63¢ |

Citi Premier Miles MC Citi Premier Miles MCApply |

IPM | 1.99% 1.2 mpd |

1.63¢ |

UOB PRVI Miles AMEX UOB PRVI Miles AMEXApply |

UOB | 1.8% 1 mpd |

1.80¢ |

| *With a minimum spend of S$2,000 in a statement month. Minimum spend includes CardUp payments (and SC EasyBill/StanChart Tax Payment Facility for that matter). | |||

| ❓How is this calculated? |

|

For CardUp, both the admin fee and the tax payment earn miles, so a S$1,000 payment with a 1.75% fee placed on a 1.2 mpd card earns 1,221 miles (S$1,017.50 x 1.2 mpd, ignoring rounding). This works out to 1.43 cents per mile (S$17.50/1,221 miles) For bank facilities, only the tax payment earns miles, so a S$1,000 payment with a 1.75% fee placed on a 1.2 mpd card earns 1,200 miles. This works out to 1.46 cents per mile (S$17.50/1,200) |

| ❓ Where’s my card? |

| If you don’t see your card mentioned above, e.g. HSBC Revolution or UOB Preferred Platinum Visa, there’s a good reason. These cards either don’t earn miles on tax payments (e.g. HSBC), or earn such a low rate that the cost per mile becomes prohibitive. |

Of course, the lower the cost per mile the better, but everyone will have to decide for themselves what “ceiling price” they’re willing to pay, based on their personal mile valuation.

Other important points

Apply for as many facilities as you want

There’s nothing stopping you from applying for multiple tax payment facilities in order to buy more miles (otherwise known as churning).

For example, someone with a S$24,000 tax bill and a StanChart Visa Infinite Card could set up an arrangement with both the Standard Chartered Income Tax Payment Facility and CardUp.

- With the Standard Chartered Income Tax Payment Facility, he could earn 33,600 miles (S$24,000 x 1.4 mpd) at a cost of S$456 (1.9% x S$24,000).

- With CardUp, he could pay his taxes in 12-month installments of S$2,000 each, earning 2,849 miles per month (S$2,000 x 1.0175 x 1.4 mpd) at a cost of S$35 (1.75% x S$2,000).

There is no interaction between the two here, because the Standard Chartered Income Tax Payment Facility is indirect, and CardUp is direct.

However, take care if you’re applying for two or more direct payment facilities, because overpaying your tax bill can create issues. Over the years, there have been many people who overpaid their taxes to buy additional miles, in the knowledge that IRAS will refund the excess anyway. However, this creates additional administrative work, and IRAS has made its displeasure at such activity known.

|

“Where we have determined in our discretion exercised reasonably that your Payment(s) to IRAS exceed the amount of taxes which you are required to pay to IRAS, we shall be entitled to claw back any rewards credited to your card account in connection with any amount so overpaid to IRAS using the Service. In such an event, we will refund the relevant portion of Fee in respect of such overpaid amount.” |

You can still use GIRO

IRAS allows taxpayers to split their payment into 12 interest-free instalments via GIRO. This is great for maximising your cashflow, and something I opt for each year.

Setting up GIRO for income tax can be done instantly via myTax Portal for the following banks:

- Bank of China

- Citibank

- DBS/POSB

- HSBC

- ICBC

- Maribank

- Maybank

- OCBC

- Standard Chartered

- UOB

Otherwise, you’ll need to submit a request for a manual GIRO form, which will take up to three weeks to process.

Once your GIRO arrangement has been approved, you can view the monthly instalment by logging in to myTax Portal, selecting Account > View Payment Plan > View Plan.

There are no issues using GIRO if you opt for an indirect payment facility, as the bank simply credits the cash to your account, and how you go about paying IRAS after that is up to you.

It’s also possible to use GIRO when you’re paying via a direct payment facility, though you’ll want to make manual payments well in advance of each month’s scheduled deduction (on the 6th of each month) to avoid double payment.

To illustrate, suppose your tax bill is S$12,000 and you opt for GIRO. IRAS will split your tax bill such that S$1,000 comes due each month.

| Month | Manual Payment | GIRO | Total Paid |

| May 2026 | – | S$1,000 | S$1,000 |

| Jun 2026 | – | S$1,000 | S$2,000 |

| Jul 2026 | S$400 | S$600 | S$3,000 |

| Aug 2026 | – | S$1,000 | S$4,000 |

| Sep 2026 | S$1,500 | – | S$5,500 |

| Oct 2026 | – | S$500 | S$6,000 |

| Nov 2026 | – | S$1,000 | S$7,000 |

| Dec 2026 | – | S$1,000 | S$8,000 |

| Jan 2027 | – | S$1,000 | S$9,000 |

| Feb 2027 | – | S$1,000 | S$10,000 |

| Mar 2027 | – | S$1,000 | S$11,000 |

| Apr 2027 | – | S$1,000 | S$12,000 |

Suppose you make a manual payment of S$400 in respect of July 2026. According to your payment schedule, you were supposed to pay S$1,000 in July, so GIRO will automatically adjust to deduct S$600 instead of S$1,000 for that month.

Then suppose you make a manual payment of S$1,500 in respect of September 2026. According to your payment schedule, you only needed to pay S$1,000 in September, so GIRO won’t take any deduction for this month.

When October 2026 comes round, assuming you make no further manual payment, GIRO will deduct S$500 to put you “back on schedule” with S$6,000 paid off by the end of October 2026.

Now, it’s important to keep in mind that IRAS GIRO deductions take place on the 6th of the month the tax is due (or the next working day if that happens to be a weekend or public holiday). If your manual payment is made too close to this date, it’s possible the full GIRO deduction will still take place.

Therefore, I would recommend making all manual payments at least two weeks in advance to avoid a double deduction (but if a double deduction happens it’s not the end of the world, since that amount goes towards offsetting the following month’s payment). In any case, the CardUp system won’t let you schedule tax payments during the last few and first few days of each month.

For more instructions on how to set up a recurring income tax payment series with CardUp, refer to this link.

What type of points are you earning?

When evaluating two cards with similar cost per mile figures, it’s helpful to think of qualitative factors as well.

| 💳 Comparing Points Currencies | |

| Expiry |

|

| Minimum Conversion |

|

| Pooling |

|

| Transfer Partners |

|

| Transfer Fees |

|

| Transfer Speed |

|

For example, Citi Miles would be superior to DBS Points or UOB UNI$, thanks to the sheer number of transfer partners available. Likewise, non-expiring Citi Miles and 90°N Miles would be more useful than expiring UNI$ or HSBC Rewards Points.

For the full analysis, refer to my guide below.

Conclusion

Income tax season presents an opportunity to buy miles at attractive rates, especially if you plan to redeem First or Business Class flights.

The all-important cost per mile, which I’ve highlighted for every major card with an ongoing promotion, boils down to the admin fee and earn rate available to you. Needless to say, we want to minimise fees and maximise earn rates, but don’t forget about qualitative factors like the range of transfer partners, points expiry and transfer times.

I’ll be updating this article as new tax payment promotions are announced, so be sure to bookmark it for future reference!

Any data point about conflicts on using the same credit card to pay tax via 2 different facilities? Ie using SC Beyond card via SC EasyBill, and then subsequently using the same card via CardUp for the same tax payment?