The BOC Elite Miles Card has been a source of endless delight over the years, though most of the mirth was enjoyed by those who weren’t actually cardholders.

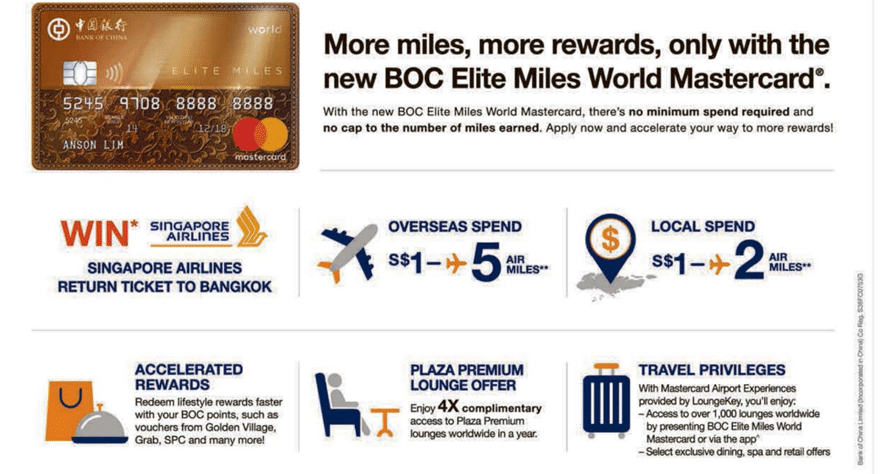

Mind you, this card hasn’t always been a punchline. When it first launched in 2018, this was the miles card to have, offering an uncapped 2 mpd on local spend and 5 mpd on foreign currency (FCY) spend, hardly any exclusion categories (not even YouTrip top-ups), and 4x Plaza Premium lounge visits. What a time to be alive!

That kind of generosity couldn’t last forever, but even at its regular rates of 1.5 mpd (local) and 3 mpd (FCY), the BOC Elite Miles Card was a force to be reckoned with

Yes, it came with its fair share of headaches—think paper application forms and having to visit a branch for the most basic of transactions—but the rewards were good enough to justify the hassle.

Until one day they weren’t.

In May 2020, BOC nerfed the Elite Miles Card by adding numerous rewards exclusion categories and slashing the earn rates. Even worse, the latter was achieved by devaluing the points to miles conversion ratio, rather than adjusting the earn rates directly. This not only reduced the number of points that cardholders would earn going forward, it also devalued the points they already had!

Since then, the BOC Elite Miles Card has faded into virtual irrelevance— give or take the odd insane promotion. But BOC is now looking to breathe new life into this card with a significant buff to its earn rates: 1.4 mpd on local spend and 2.8 mpd on FCY spend.

Of course, in true BOC fashion, this won’t be a straightforward process. Not only will existing cardholders see their current stash of points devalued (BOC is the only bank that can somehow “nerf to buff”), but Asia Miles conversions will be discontinued, and rewards for CardUp and ipaymy transactions will be removed.

BOC Elite Miles buffs earn rates to 1.4 mpd (local) and 2.4 mpd (FCY)

From 1 July 2025, the BOC Elite Miles Card will earn 1.4 mpd on local spend (up from 1 mpd) and 2.8 mpd on FCY spend (up from 2 mpd), without any minimum spend or cap.

| Till 30 Jun 2025 | From 1 Jul 2025 | |

| Local Spend | 1 mpd (4.5 pts per S$1) |

1.4 mpd (7 pts per S$1) |

| FCY Spend | 2 mpd (9 pts per S$1) |

2.8 mpd (14 pts per S$1) |

The above table may be puzzling if you scrutinize the points to miles ratio. If 4.5 points corresponds to 1 mpd today, why does 7 points (and not 6.3 points) correspond to 1.4 mpd from 1 July?

The answer is that BOC is nerfing its points, but buffing its earn rates.

| Till 30 Jun 2025 | From 1 Jul 2025 | |

| BOC Points : KrisFlyer | 45,000 pts = 10,000 miles | 50,000 pts = 10,000 miles |

Confused? Stay with me.

Currently, 45,000 BOC Points are equivalent to 10,000 KrisFlyer miles. From 1 July 2025, you will need to redeem 50,000 BOC Points (11% more) for the same 10,000 KrisFlyer miles. However, because the earn rate (in points) also increases by 56%, the overall earn rate (in miles) still improves by 40% overall.

Even so, this means that you should cash out any BOC Points you currently have, or else suffer a 11% loss in value come 1 July 2025.

You’re probably wondering: why not make things simple by keeping the conversion rates as-is, and increasing the earn rates even more? Well, you need to remember that this is BOC. Sneaking in a devaluation alongside a buff would be completely in character.

I find it particularly irksome for a bank to devalue its conversion rates, because it effectively penalises your past spending, but this is in fact the second time that BOC has done so. Prior to 15 June 2020, 30,000 BOC Points was equivalent to 10,000 KrisFlyer miles!

Convolutedness aside, these are objectively good earn rates, and perhaps the best you could expect for a general spending card with a minimum income requirement of S$30,000.

| 💳 Earn Rates for General Spending Cards (income req.: S$30K) |

||

| Cards | Local Spend | FCY Spend |

UOB PRVI Miles Card UOB PRVI Miles CardApply |

1.4 mpd | 3 mpd IDR, MYR, THB, VND 2.4 mpd All Others |

BOC Elite Miles Card BOC Elite Miles CardApply |

1.4 mpd | 2.8 mpd |

HSBC TravelOne Card HSBC TravelOne CardApply |

1.2 mpd | 2.4 mpd |

DBS Altitude Card DBS Altitude CardApply |

1.3 mpd | 2.2 mpd |

OCBC 90°N Card OCBC 90°N CardApply |

1.3 mpd | 2.1 mpd |

Apply |

1.2 mpd | 2.2 mpd |

StanChart Journey Card StanChart Journey CardApply |

1.2 mpd | 2 mpd |

Apply |

1.2 mpd | 1.2 mpd |

AMEX KrisFlyer Credit Card AMEX KrisFlyer Credit CardApply |

1.1 mpd | 1.1 mpd |

KrisFlyer UOB Credit Card KrisFlyer UOB Credit CardApply |

1.2 mpd | 1.2 mpd |

An uncapped 2.8 mpd for FCY spend is particularly attractive, because cards offering the same rates or better either come with minimum spend requirements, or higher minimum income requirements (or both).

| 💳 Cards with Uncapped FCY Earn Rates |

||

| Card |

Min. Income | FCY Earn Rate |

StanChart Beyond Card StanChart Beyond CardApply |

S$200K | 4 mpd (PP) 3.5 mpd (PB) 3 mpd (Regular) |

Maybank World Mastercard Maybank World MastercardApply |

S$80K | 3.2 mpd Min. S$4K |

Maybank Visa Infinite Maybank Visa InfiniteApply |

S$120K | 3.2 mpd Min. S$4K |

StanChart Visa Infinite StanChart Visa InfiniteApply |

S$150K | 3 mpd Min. S$2K |

Maybank Horizon Visa Signature Maybank Horizon Visa SignatureApply |

S$30K | 2.8 mpd Min. S$800 |

| BOC Elite Miles Card Apply |

S$30K | 2.8 mpd |

Furthermore, BOC’s FCY transaction fee of 3% is slightly below the market average of 3.25%, so using this card overseas represents buying miles at an attractive rate of 1.07 cents each.

| 💳 FCY Fees by Issuer and Card Network |

||

| Issuer | ↓ MC & Visa | AMEX |

| Standard Chartered | 3.5% | N/A |

| American Express | N/A | 3.25% |

| Citibank | 3.25% | N/A |

| DBS | 3.25% | 3% |

| HSBC | 3.25% | N/A |

| Maybank | 3.25% | N/A |

| OCBC | 3.25% | N/A |

| UOB | 3.25% | 3.25% |

| BOC | 3% | N/A |

| CIMB | 3% | N/A |

And finally, BOC has an extremely favourable rounding policy. Forget about S$5 earning blocks; BOC awards fractional points down to the very last cent.

For example, a S$10.38 transaction in SGD will earn 72.66 BOC Points (based on the revised earn rate of 7 pts/S$1), with no rounding whatsoever. This means that you will never lose points to rounding, regardless of transaction size.

BOC will discontinue Asia Miles conversions

| Mileage Programme | Till 30 Jun 2025 | From 1 Jul 2025 |

| 45,000 : 10,000 |

50,000 : 10,000 |

|

| 27,000 : 6,000 |

N/A |

BOC Points can currently be converted to both Singapore Airlines KrisFlyer and Cathay Pacific Asia Miles.

From 1 July 2025, Asia Miles will no longer be offered, giving BOC the dubious distinction of being the only bank in Singapore not to support transfers to this programme. You can still convert 27,000 BOC Points into 6,000 Asia Miles until 30 June 2025.

With only one conversion partner, the fate of your BOC Points will be inextricably tied to KrisFlyer. If When KrisFlyer eventually devalues its award charts again, you’ll usually have one month to redeem awards at the existing prices. Given that BOC requires 14-21 working days to complete conversions (and based on real-world data points, that’s an actual timeline and not a case of underpromise and overdeliver), there might not be enough time to convert your BOC Points into miles.

New exclusions for CardUp and ipaymy

From 1 July 2025, BOC will add new categories to its rewards exclusion list, including both CardUp and ipaymy.

| MCC | Description |

| 4829 | Payment of funds for money transfers and remittance services |

| 4900 | Utilities – electric, gas, water and sanitary |

| 5199 New |

Non-durable goods (not elsewhere classified) |

| 5960 | Direct Marketing – Insurance Services, Insurance Sales, Underwriting and Premiums |

| 5965 New |

Direct Marketing – Combination Catalog and Retail Merchants |

| 5993 New |

Cigar Stores and Stands |

| 6010, 6011, 6012, 6050, 6051, 6211 | Payments to financial institutions (including banks and brokerages) for financial services |

| 6300, 6399 6381 New |

Insurance Payments |

| 6513 | Real Estate agents and managers |

| 6540 6529, 6530, 6534 New |

Payments of funds to prepaid accounts and/or merchants categorised as “payment service providers” |

| 7349 New |

Cleaning, Maintenance and Janitorial Services |

| 7511 New |

Quasi Cash – Truck Stop Transactions |

| 7523 New |

Parking lots and garages |

| 7995 | Betting, including lottery tickets, casino gaming chips, offtrack betting and wagers at race tracks |

| 8062 | Hospitals |

| 8211, 8220, 8241, 8244, 8249, 8299 | Schools and Educational Services |

| 8398 | Charitable and Social Service Organisations |

| 8661 8651, 8699, 8999 New |

Political Organisations, Religious Organisations, and Membership Organisations (not elsewhere classified) |

| 9211 | Court Costs including Alimony and Child Support |

| 9222 | Fines |

| 9223 | Bail and Bond Payments |

| 9311 | Tax Payment |

| 9399 | Government Services – not elsewhere classified |

| 9402 | Postal Services – Government Only |

| 9405 | Intra-Government Purchases – Government only |

Do note that BOC has not explicitly excluded CardUp’s MCC (7399), but mentions CardUp as a specific example in its T&Cs under “Financial Institutions for Financial Services”.

| Category | Examples |

|---|---|

| Cleaning, Maintenance, and Janitorial Services | Helpling, Sendhelper |

| Educational Institutions | Institute of Technical Education (ITE), NTU, NUS, SIM, SIT, SMU, SUSS, SUTD |

| Financial Institutions for Financial Services | AxiTrader, BANC DE BINARY, BANCDEBINARY.COM, CardUp, City Index, FOREX.COM, MONEYBOOKERS.COM, IC Markets, IG Asia, IGMarkets.com.sg, ipaymy, OANDA, Peppersone (sic), Plus500, Revolut, Saxo Capital Markets/Saxo Cap Mkts Pte Ltd, SKRSKRILL.COM, SKRxglobalmarkets.com, SKYFX.COM |

| Government Services | ACRA, CPF, HDB Season Parking, ICA, IRAS, LTA, MOM, Town Council, URA |

| Hospitals | Farrer Park Hospital, Gleneagles Hospital, KK Women’s and Children’s Hospital, Mount Alvernia Hospital, Mount Elizabeth Hospital, National University Hospital, Parkway Shenton Hospital, Singapore General Hospital, Tan Tock Seng Hospital |

| Insurance Payments | AIA Insurance, AIG, AVIVA, AXA, Great Eastern, Manulife, MSIG Insurance, NTUC Income, Prudential, QBE Insurance, Sompo Insurance, TM Life Insurance |

| Money Transfer and Remittance Services | MoneyGram, Swiss Money Transfer, Western Union, Wise, WorldRemit |

| Prepaid Accounts and Payment Service Providers | AXS, EZ Link/EZ-Link/EZLINK, eNETS, HelloPay, MatchMove Pay, NETS FlashPay, SAM, SingTel Dash, Transit/TransitLink, Youtrip, Grab wallet top-ups, ShopeePay wallet top-ups |

| Real Estate Agents and Managers | ERA Singapore, MCST, RentHero |

| Utility Bill Payments / Other Payments | AXS, SAM payments, SP Services |

It’s unfortunate, because an earn rate of 1.4 mpd would have made the BOC Elite Miles one of the best cards to use with CardUp, particularly at the S$30,000 income level.

BOC Points remain valid for 1-2 years

BOC’s announcement mentions an update to the “rewards period”, but really, nothing has changed here.

BOC Points continue to be valid for 12-24 months, depending on when they were earned.

| Earned | Expiry |

| 1 Jul 2024- 30 Jun 2025 | 30 Jun 2026 |

| 1 Jul 2025- 30 Jun 2026 | 30 Jun 2027 |

| 1 Jul 2026-30 Jun 2027 | 30 Jun 2028 |

Points expiry takes place on 30 June each year, which means that in a worst case scenario, points could be valid for as little as 12 months (if they were earned on 30 June). On the flip side, however, points could be valid for as much as 24 months (if they were earned on 1 July).

BOC is not for the faint of heart!

If you want to apply for a BOC Elite Miles Card, it’s important that you go in with both eyes open. This is not a bank for the faint of heart, with its antiquated processes, nonsensical rules and endless shenanigans.

- You’ll need to visit a physical BOC branch to set up ibanking, or to link your BOC credit card to your ibanking account

- BOC still uses paper forms for points conversions, which take 14-21 working days to be processed

- BOC charges a conversion fee of S$30.56 that covers up to 10 “blocks” of air miles, equivalent to 100,000 KrisFlyer miles or 60,000 Asia Miles. You must pay another conversion fee if you wish to convert more than this amount

- BOC does not recognise refunds as credits to amounts outstanding, which has resulted in cardholders being charged unexpected interest in the past

- BOC’s idea of an annual fee waiver is to reverse the amount outstanding…then deducting your points instead

I’ve jested about how feels like you need to be constantly on your guard when dealing with UOB cards, but BOC takes it to the next level.

Conclusion

The BOC Elite Miles Card will get a major buff to its earn rates on 1 July 2025, when local and FCY spend start earning 1.4 mpd and 2.4 mpd respectively.

However, BOC will also sneak in a devaluation of existing points via an adjustment to its conversion rates, which means that existing cardholders should aim to cash out their entire stash ahead of this date.

Asia Miles conversions will be removed, leaving KrisFlyer as the only transfer partner, and rewards will no longer be offered for CardUp and ipaymy.

I’m not going to deny the obvious: this is now a competitive miles card once again. The key question is whether BOC’s processes have improved commensurately, to make dealing with the bank less migraine-inducing.

Will you be returning to BOC Elite Miles Card?

Does the Cardup exclusion applies to other BOC cards as well? E.g. cashback for BOC family card.