Dear fellow influencers:

There is a long list of things in life which you’re perfectly at liberty to do, but might be somewhat unwise.

Filling up with rice at the buffet. Taking a bubble bath with your favourite toaster. Skipping BMT and basic close combat training, then showing up at an anime convention.

I share these words of wisdom because it’s come to my attention that many of you are promoting Citi’s Pay with Points option.

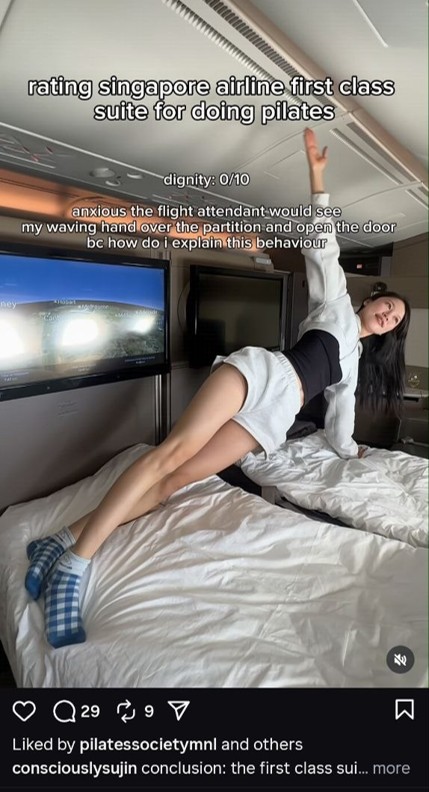

You see, the other night I was in the midst of a riveting doomscrolling session. The Instagram algorithm was on fine form, feeding me a never-ending stream of far-right conspiracy theories and flan recipes (I’m a man of eclectic tastes).

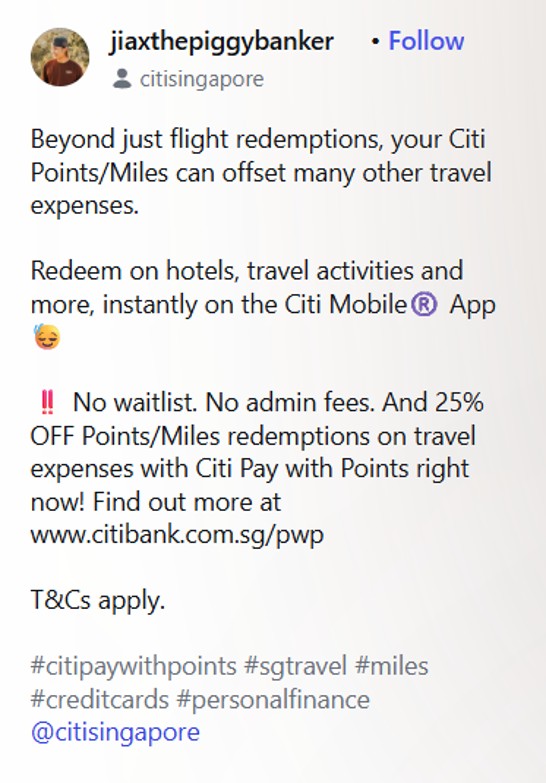

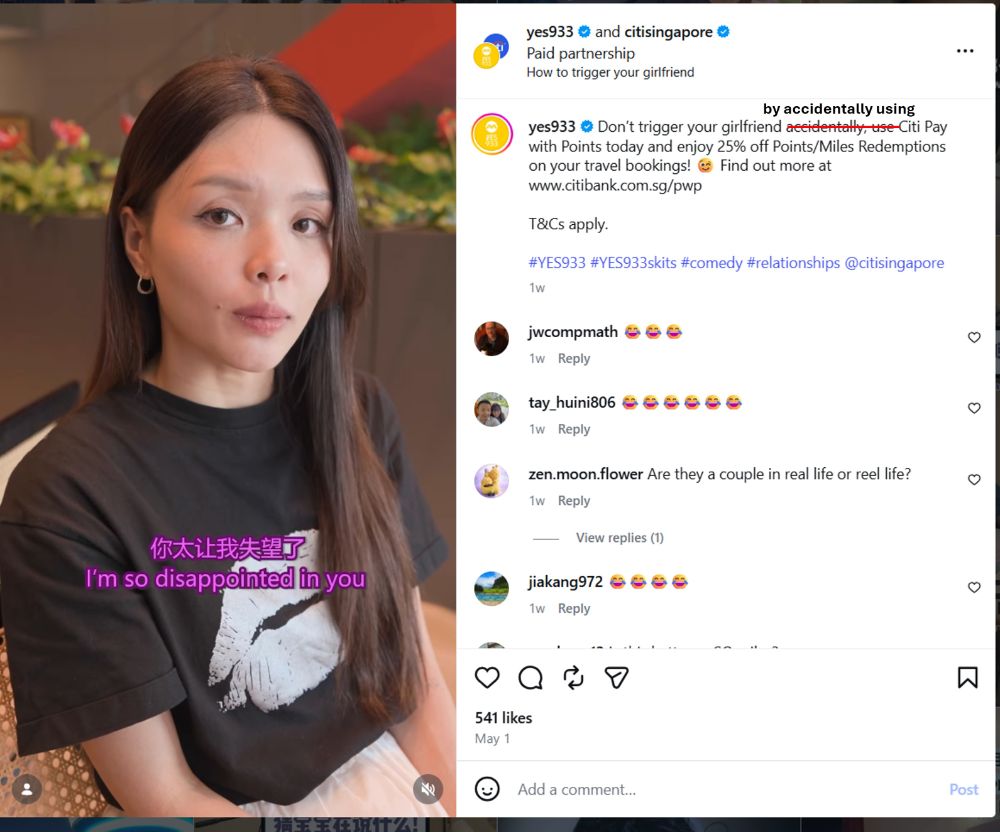

Then, all of a sudden, I stumbled upon this.

What’s this? I can redeem my Citi Miles and ThankYou Points for cash rebates? No waitlists? No admin fees? 25% off redemptions? And I can do it all on the Citi Mobile® App? (note to legal department: if you’re hiring influencers to sound authentic, maybe don’t insist they put registered trademark symbols?)

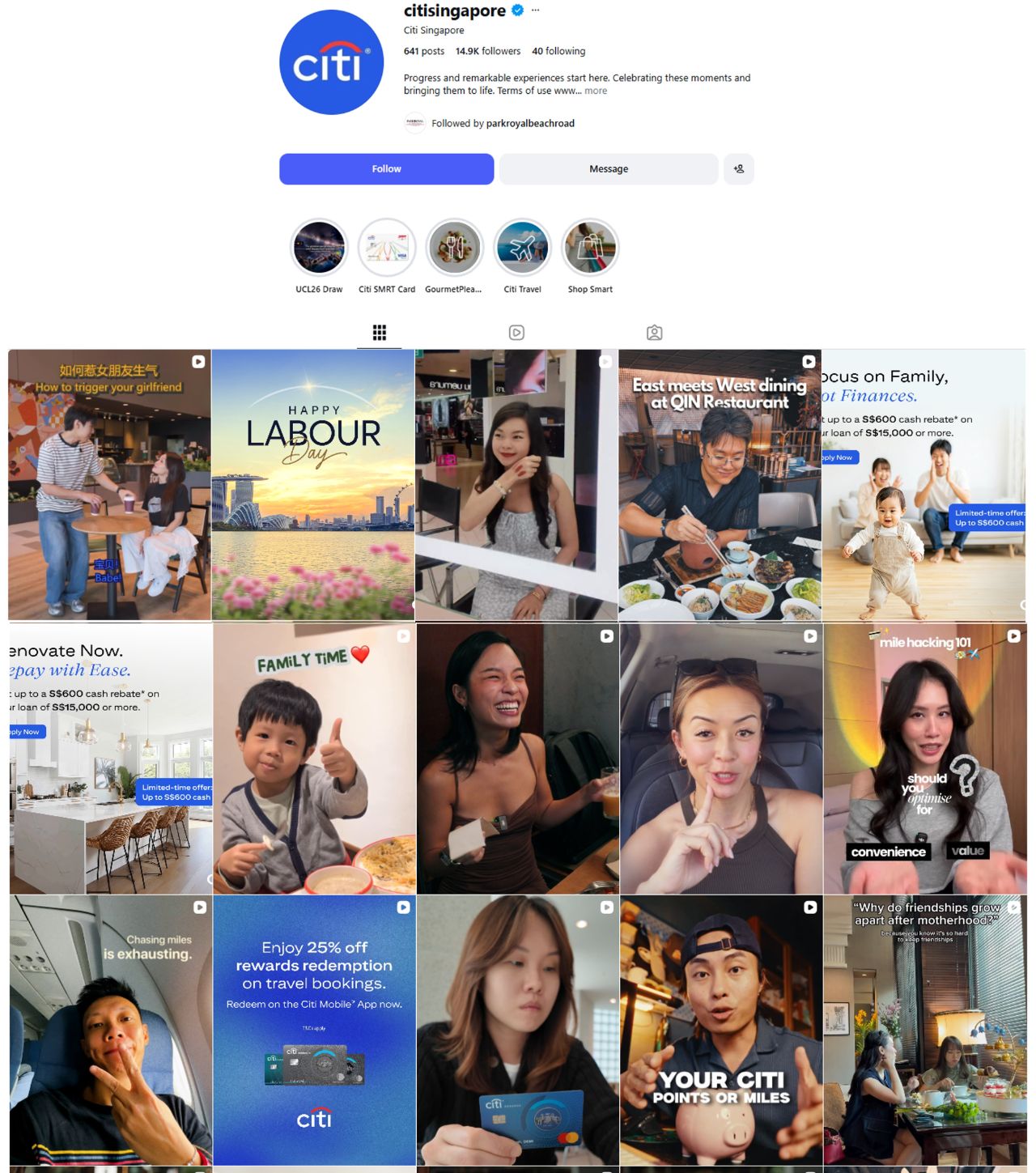

I was skeptical, but then I found another post, and then another, and then another. Indeed, a whole bunch of posts from individuals with better complexions, teeth, hairlines and personal hygiene than me had popped up in the past couple of weeks, singing the praises of this incredible option. A new travel hack! Send this to your miles-loving friends! Don’t wait!

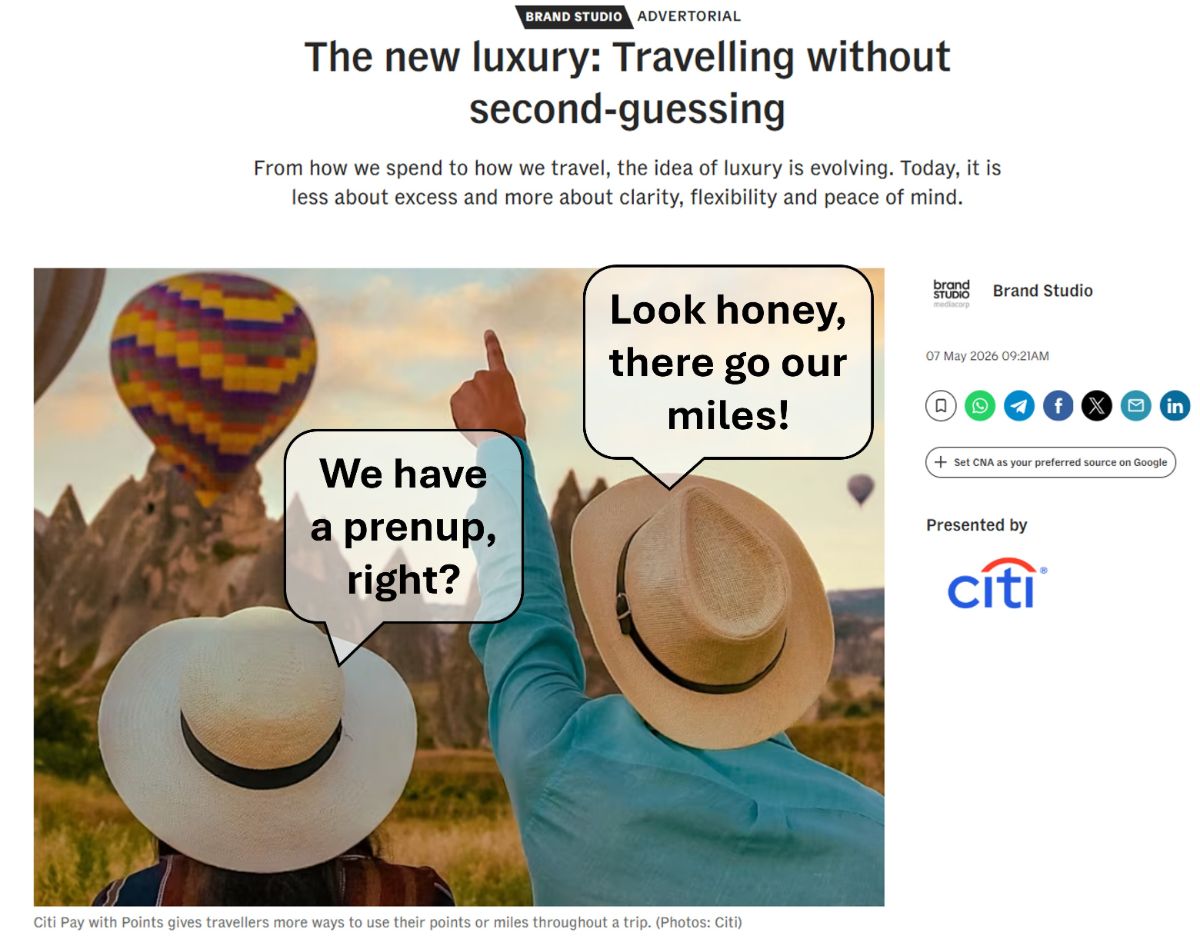

Even reputable news source CNA Lifestyle — the one which gave voice to the silent suffering we influencers endured having to learn TikTok during COVID — was proclaiming Pay with Points as “the new luxury”.

My world teetered on the brink of a Copernican shift, as I weighed the evidence before me. Had I been misleading everyone by advising them to redeem their Citi Miles and ThankYou Points for something as frivolous as *gasp* airline miles, while selfishly gatekeeping the true secret?

Well, here’s the thing. Having done some research (you know, the kind we should be doing before posting anything), I’m not entirely convinced that Pay with Points is as amazing as you’re making it sound.

Citi’s Pay with Points “deal”

Let’s briefly recap the details of Citi’s year-long Pay with Points (PwP) promotion, which runs from 19 March 2026 to 31 March 2027.

During this period, Citi cardholders can offset travel bookings with Citi Miles or ThankYou Points (TYP) at 25% off the usual rates.

|

|

| Points | Value |

-25% |

S$1 |

-25% |

S$1 |

| Terms & Conditions |

|

Travel bookings are defined as transactions with airlines, hotels and travel agencies, such as Singapore Airlines, Cathay Pacific, Westin, Klook and Trip.com. For example, a flight booking of S$800 could be offset with 98,400 Citi Miles, instead of the usual 132,000 Citi Miles.

Based on how enthusiastic you guys are about PwP, I’m concerned you might have missed three things.

First, this is even worse than last year’s “deal”, when the going rate was 100 Citi Miles per S$1.

Second, it’s not just quantitatively worse. It’s qualitatively worse too, because Citi is defining these categories much more narrowly this year.

| Category | 2025 | 2026 |

| Airlines | 3000, 3001, 3004-3018, 3020-3022, 3024-3026, 3028-3035, 3037-3040, 3042-3044, 3047-3052, 3054, 3056-3058, 3064-3066, 3068, 3069, 3072, 3075-3079, 3082- 3084, 3088-3090, 3098-3100, 3102, 3103, 3112, 3127, 3129, 3131, 3132, 3136, 3144, 3146, 3161, 3174, 3175, 3180-3184, 3187, 3191, 3193, 3196, 3206, 3211, 3217, 3219-3221, 3223, 3228, 3234, 3236, 3239, 3240, 3245- 3248, 3256, 3260, 3261, 3266, 3294-3299, 4511 | 3005, 3007, 3012, 3034, 3047, 3075, 3077, 3084, 3099, 3136, 3025, 3026, 3078, 3082, 3206 |

| Hotels | 3501-3521, 3523, 3524, 3526, 3528-3530, 3532, 3533, 3535-3545, 3548-3553, 3555, 3558, 3559, 3561-3565, 3567, 3569, 3570, 3572, 3573, 3575, 3577, 3579-3581, 3583, 3584, 3586, 3588-3592, 3595, 3596, 3598, 3602, 3604, 3607-3609, 3611- 3619, 3621, 3623, 3625, 3628, 3629, 3631, 3632, 3634-3645, 3647, 3649-3655, 3657-3665, 3667, 3668, 3670, 3672-3674, 3676-3681, 3684, 3685, 3687, 3688, 3690, 3692-3698, 3700, 3701, 3703, 3704, 3706, 3707-3710, 3714-3723, 3726-3728, 3730, 3731, 3734, 3736-3745, 3747, 3749-3752, 3754, 3755, 3757, 3760, 3763, 3765, 3769-3774, 3777-3780, 3782-3786, 3788-3791, 3793, 3795, 3796, 3798-3800, 3802, 3804, 3807, 3808, 3811-3814, 3816, 3818, 3819, 3822-3826, 3828-3832, 7011, 7012, 7033 |

3503, 3504, 3509, 3512, 3513 |

| Travel Agencies | 4722 | 4722 |

There’s a big gotcha lurking here, because it’s not hard to imagine a scenario where someone makes a purchase with Japan Airlines, Lufthansa, China Airlines, Scoot, Hyatt, or any of the hundreds of airlines and hotels that aren’t included, choosing PwP, only to receive the regular, non-discounted rate of 165 Citi Miles/440 TYP per S$1.

But never mind that. Third, and most crucially, PwP values your hard-earned Citi Miles and TYP at a jaw-droppingly poor figure of:

- 0.81 cents per mile, for Citi Miles

- 0.76 cents per mile, for TYP

That’s…not ideal.

Why Pay with Points makes no sense

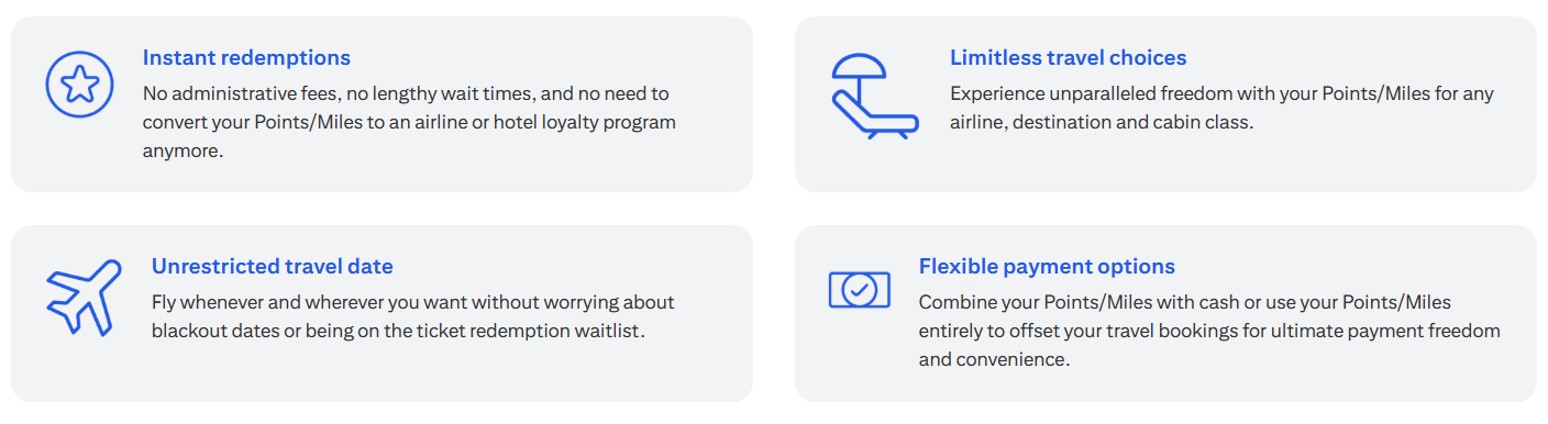

According to your videos, the case for using PwP is that it offers instant redemptions, unrestricted travel dates and destinations, partial payment options and ultimately more flexibility— sidestepping a lot of the usual headaches associated with airline miles.

And you know what? I’m onboard with that. Miles aren’t all pilates in Suites and fairy lights in Business. There are a lot of potential frustrations with waitlists, devaluations and unavailability during peak periods.

If you don’t have wriggle room in your travel dates, if you want the certainty of visiting a particular destination, if you need to be on a specific flight, then nothing beats the flexibility of booking a commercial ticket with cash.

But if that’s the case, you really should be earning cashback, not miles. And you know what’s a good way of earning cashback? Hint: it’s not a miles card!

To illustrate, here’s the effective rebate with PwP on the Citi PremierMiles Card and Citi Prestige Card.

| Card | Earn Rate | Effective Rebate via PwP |

Citi PremierMiles Card Citi PremierMiles Card |

1.2 Citi Miles per S$1 SGD 2.2 Citi Miles per S$1 FCY |

0.98% SGD -1.46% FCY |

| 3.25 TYP per S$1 SGD 5 TYP per S$1 FCY |

0.98% SGD -1.73% FCY |

|

| FCY rebate is nett of a 3.25% FCY fee |

||

Citi PremierMiles Cardholders earn 1.2 Citi Miles per S$1 on local spend. If you redeem those points at the PwP rate of 123 Citi Miles per S$1, your effective rebate is just under 1%.

It’s even worse if you spend overseas, because that 2.2 Citi Miles per S$1 comes with an FCY transaction fee of 3.25%. If you cash out your points at the PwP rate, you’re actually losing money! The math, as the youngsters say, is not mathing.

Instead, why not earn an uncapped 1.5-1.7% cashback with the various cashback cards on the market, which you could then use for the “unparalleled freedom” and “unrestricted travel dates” that PwP supposedly offers?

| 💳 General Spending Cashback Cards (Without Min. Spends or Caps) |

||

| Annual Fee | Cashback | |

UOB Absolute Cashback UOB Absolute Cashback |

S$196.20 (FYF) |

1.7% |

BOC Visa Infinite BOC Visa Infinite |

S$381.50 (FYF) |

1.6% |

Citi Cash Back+ Card Citi Cash Back+ Card |

S$196.20 (FYF) |

1.6% |

OCBC Infinity Cashback OCBC Infinity Cashback |

S$196.20 (FYF) |

1.6% |

ICBC Chinese Zodiac Card ICBC Chinese Zodiac Card |

S$150 (F3YF) |

1.6% |

Maybank FC Barcelona Card Maybank FC Barcelona Card |

S$130.80 (F2YF) |

1.6% |

Mari Credit Card Mari Credit Card |

N/A | 1.5% |

AMEX True Cashback Card AMEX True Cashback Card |

S$174.40 (FYF) |

1.5% |

SC Simply Cash Card SC Simply Cash Card |

S$196.20 (FYF) |

1.5% |

| FYF= First Year Free, F2YF= First 2 Years Free, F3YF= First 3 Years Free |

||

I mean, I can’t say I’m the biggest advocate of cashback cards. But if you want to use your points as cashback, you might as well have spent on a cashback card in the first place.

Wait a minute, you say. You’re just cherry-picking your examples. What about the Citi Rewards Card? With its bonus rate of 10 TYP per S$1, PwP is equivalent to a 3% cash rebate. Considering there’s no minimum spend necessary, that beats any cashback card, right?

Um, no. Remember, this PwP promotion is only valid for offsetting travel bookings. When you charge travel bookings to the Citi Rewards Card, you earn just 1 TYP per S$1, because of its travel-related blacklist. In other words, your actual rebate is — wait for it — 0.3%.

But I’m past that stage already! I can’t go back in time and use a cashback card, and now I have all these Citi Miles and TYP. Surely cashing them out via PwP would be better than letting them go to waste?

Not so fast. If you’ve decided to ragequit the miles game, then cashing out via Kris+ would still be better value. Kris+ offers instant, fee-free conversions from Citi points to KrisPay miles at the following ratios:

| Citi Miles/ TYP | KrisPay Miles | |

| 4,000 Citi Miles | ⇒ | 3,400 miles |

| 10,000 TYP | 3,400 miles |

|

You can then spend those KrisPay miles at 1 cent each across nearly 600 dining and retail outlets including NTUC FairPrice, Paradise Dynasty, Challenger, iStudio and Esso. You could use them for KrisShop, Pelago, even transfer them to KrisFlyer to pay for Singapore Airlines or Scoot flights.

Kris+ values 1 Citi Mile at 0.85 cents each. Is it terrible? Yes. Is it as terrible as PwP? No.

“It’s just an option!”

Therefore, fellow influencers, I fear we may be leading our audiences astray with our well-intentioned but ultimately flawed advice.

It’s easy to dodge the criticism by saying something along the lines of “We’re not telling people they should be using PwP, we’re just presenting it as an alternative option.”

But that’s the thing. At its current value, PwP should not even be an option, period.*

*Unless you have <4,000 Citi Miles or <10,000 TYP and no plans to earn more. And even then, you need to be careful about what travel bookings you make because of the limited MCC coverage. And of course, you might as well have spent on a cashback card instead. But I imagine all those caveats don’t make for a very good Instagram reel.

When we treat PwP as an equally valid choice, and wax lyrical about its convenience and flexibility while saying nothing about its biggest flaw — the terrible value — we’re abdicating, not educating.

At the very least, we should make it clear to people that they’re trading convenience for significant value loss, instead of nudging them towards a suboptimal decision by omitting the crucial facts.

But don’t worry, the situation is salvageable. With just a few simple edits, we can correct these posts. Look— you don’t even need to change the video!

So in conclusion, my friends, please don’t use Citi’s Pay with Points, because:

- the value is abysmally poor

- you might as well have used a cashback card in the first place

- cashing out points via Kris+ gives you better value (mind you, “better” is relative!)

I mean, I assume you’re using Pay with Points yourself.

Because otherwise, why would you be posting about it?

Hahaha the burn in this!

I missed the “For Great Justice” section so much.

love this

Let them burn their points!

love this, they should be shamed.

They must be paid by the airlines to promote this .

On the flipside, the more people who burn their points this way, the better for us

(un)natural selection 🙂

Honestly, if they want to be lazy, let them. better for the rest of us 😛 sshhhh

Yes more redemption tickets on travel for us! Thanks to them!

well. Influencers will just about promote anything as long as it fills their wallets. No matter if it benefits their viewers or not. Thats why you are different.

This is the exact reason why I don’t listen to SG influenzas. Most have little to no knowledge about the product they are promoting and follow the script provided by the product’s company. Heck I bet these influenzas are the ones putting all spend on a 1.2 mpd general spend credit card. Say it with me: influenzas do not have your best interests at heart. Thank you Milelion for doing the Lord’s work.

Thank you Aaron, where would be if not for your far right conspiracy theory doom-scrolling! At least someone was making beneficial content!

Thank you for the transparency! Keep up the honesty and integrity!

was thinking nothing to take away from this post, but got to see your cashback cards comparison “)

always nuggets from your post, you’re the best reviewer of credit cards in Singapore, hands down

we must make sure this article doesn’t see the light of day. Let the uninformed burn their points. Mwahahahaha

Aaron, I went through the list of posts you tagged and I don’t think it’s fair as some of the posts there are promoting Citi cash back not pay with points.

Which post are you talking about specifically? All the posts I linked to are for pwp.

the citi Singapore instagram page which you took a screenshot of includes posts which are not all PWP.

Understand the confusion, and I’m aware they’re not all PWP- for more on the decision to use a screenshot of the overall page instead of the specific posts (which was the original case), you might want to refer to this thread (be sure to read the full replies): https://t.me/milelion/1253351

I think this is a classic example of “can’t please all the people all of the time”.

also when you linked the words ‘whole bunch of posts’ to the citi singapore page, not all of them are promoting PWP what.

regarding this- I would hope people realise “whole bunch of posts” does not mean “literally every single post you see on the Citi Instagram page”. I mean, there’s a happy labour day post too!

Nowadays influencers should have responsible for what they are promoting! They cant just simply advertise or talk something that is not true. Well, I also wondering how many of them actually do the survey or calculation before they take the money and just blindly promoting all these…

In Aaron We Trust

This is actually very well written professionally. And really, why do we even need pay with points.

love the subheader! this is Shady indeed xD

Yes, totally agreed!

This is why we love you Aaron.

You are amazing. Absolutely respect the integrity of your work, even if it might put a potential “paid partnership” with Citi at risk. Thank you for your intellectual honesty.