Whenever someone asks me to write about manufactured spending, my answer is always the same: I have no idea what you’re talking about — and even if I did, doing so would probably not be worth the invective.

I don’t know about you, but I’m actually rather fond of walking around in public without people farting in my general direction, or telling me that my mother was a hamster, and my father smelled of elderberries.

That said, my assumption is that once a particular method has been nerfed, the omerta lifts, and I can discuss it publicly without fearing for my life.

Or at least I hope so, because I’m about to tell you the story of how, up until last week, the best card in the miles game (or cashback, for that matter) was actually the little-known EZ-Link Debit Mastercard.

The best card in the whole wide world

Back in March 2020, EZ-Link introduced the EZ-Link Wallet, an e-wallet for mobile phones that allowed users to scan and pay at participating merchants. In a market already saturated with e-wallet options, this was greeted with little more than a shrug — yet another app to install; yet another logo under the SGQR code.

But two years later, it partnered with Mastercard to create the EZ-Link Mastercard, a virtual debit card which allowed customers to pay with their EZ-Link Wallet balance anywhere Mastercard was accepted.

This created a manufactured spending opportunity — the ability to generate credit card rewards, without actually spending.

You see, EZ-Link top-ups were long excluded by banks, due to concerns about gaming. However, because these top-ups coded as MCC 4111 Local and Suburban Commuter Passenger Transportation, it wasn’t a simple matter of blacklisting the MCC entirely, as that would block rewards for “legitimate” transactions too (that didn’t stop OCBC though, which excluded the MCC wholesale in 2020).

Therefore, the exclusion was done on the basis of transaction description. Basically, banks told their systems not to reward any transaction that began with the description EZ-Link*.

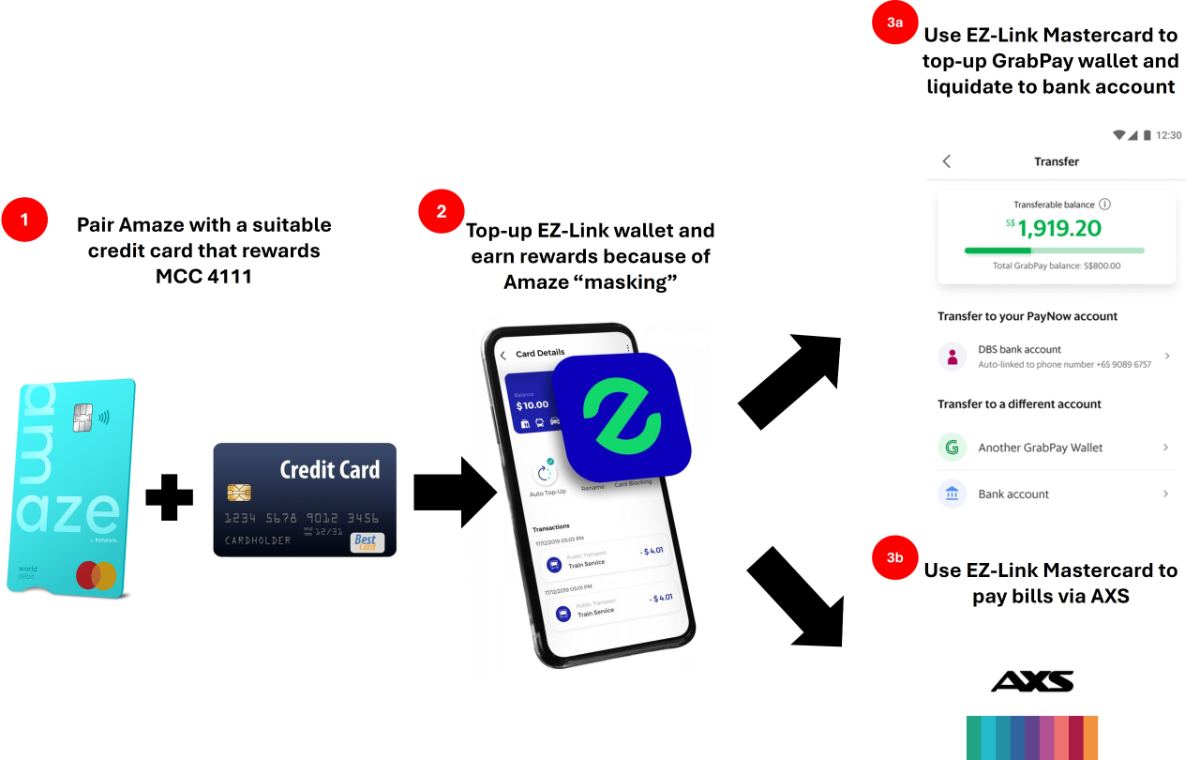

Remember though: Amaze modifies the transaction description into Amaze*Merchant. Therefore, if you were to top-up an EZ-Link wallet with an Amaze-paired card, the transaction description would become Amaze*EZ-Link under MCC 4111, therefore bypassing the exclusion. Hello rewards!

What’s more, because the EZ-Link Mastercard is a debit card, you could create a “clean loop” by topping up an EZ-Link Wallet with an Amaze-paired Citi PremierMiles Card (for example), earning 1.2 mpd, then topping up a GrabPay Wallet before cashing out the balance to a bank account.

This lasted until EZ-Link blocked e-wallet top-ups altogether in August 2022, thereby removing the possibility of encashing your balance (step 3a in the diagram above).

However, using the EZ-Link Mastercard to pay bills via AXS (step 3b) was still a viable option, at least until Amaze added a 2% fee on e-wallet top-ups in February 2023. This introduced a cost into the process at step 2, which made it significantly less worthwhile (e.g. with the Citi PremierMiles Card you were now paying 2% to earn 1.2 mpd, or 1.67 cpm, and in any case, Citi would later add Amaze*EZ-Link as a rewards exclusion in July 2023).

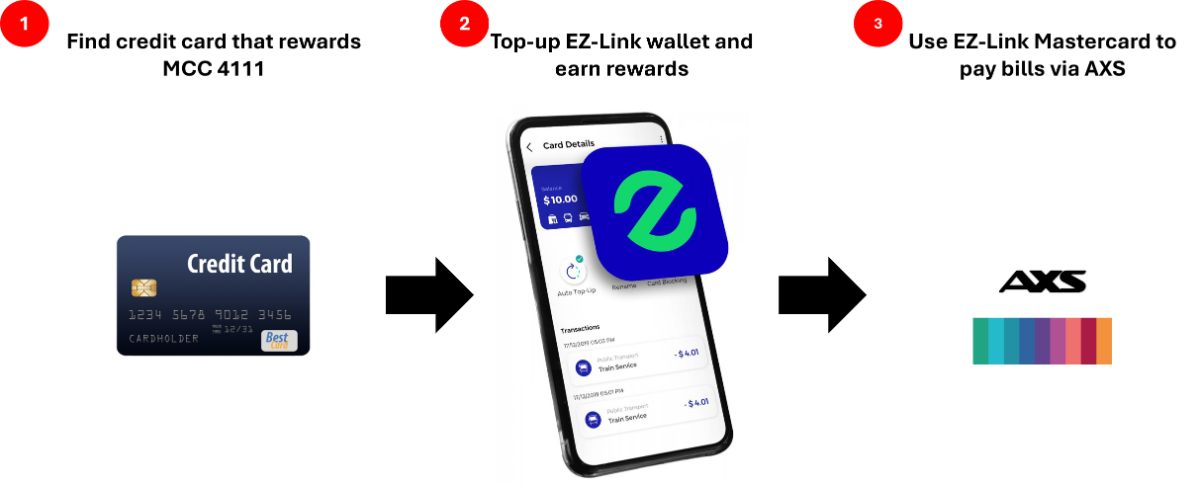

But things got interesting again in September 2024, when EZ-Link and TransitLink were merged into a single entity called SimplyGo. This led to a change in the merchant name, such that EZ-Link top-ups now used the transaction description SimplyGo (assuming you made the top-up with the SimplyGo app, and not the EZ-Link app).

And because most banks had no exclusion for SimplyGo, you didn’t need Amaze anymore. You could top-up the EZ-Link Wallet with any card that rewarded MCC 4111 — earning 6 mpd with the UOB Lady’s Cards with Transport as a bonus category, or clocking minimum spend for high yield savings accounts or upsized cashback rebates — then use the EZ-Link Mastercard to pay bills via AXS.

Those are just the ones I know of, mind you. I’m sure the hive mind found far more creative ways, and modesty forbids me from repeating some of the other stories I’ve heard. This was basically a return to the golden days of the GrabPay Mastercard.

Now, at this juncture I should emphasise that bill payments aren’t manufactured spending in the strictest sense. With manufactured spending, the goal is to convert card spend into cash or cash-like value. As far as I know, that possibility ended in August 2022, when EZ-Link blocked top-ups to e-wallets.

Bill payments, on the other hand, are genuine transactions to a third party with real economic substance behind them. Therefore, the EZ-Link Mastercard-AXS combo would be more accurately described as a way of earning rewards on expenses that would normally be ineligible.

Still, most people have plenty of bills to pay — income tax, GST, hospital bills, education, government agencies, insurance premiums, MCST fees, season parking, utilities — and you could always pay bills on behalf of friends and family.

With this in the picture, other payment platforms became virtually irrelevant. Underwhelming Citi PayAll promotion? Yawn. SC EasyBill adding monthly usage cap? Boring! CardUp hiking fees? Who cares? So long as the SimplyGo gravy train kept running, there was no reason to ever do something as silly as — gasp — paying a fee to earn miles.

| 💳 Not credit card bills though |

|

You couldn’t use the EZ-Link Mastercard to pay credit card bills, because on the AXS backend, the EZ-Link Mastercard was classified as a credit card (despite actually being a debit card). I distinctly remember that the GrabPay Mastercard was treated the same way. Presumably, AXS knew about some of these shenanigans and pre-emptively took steps to prevent people from creating an infinite rewards loop. |

The only limitation here was the annual spending cap on the EZ-Link Wallet — unlike YouTrip and Revolut, which have received approval to increase their annual spending limit to S$100,000, the EZ-Link Wallet was still stuck on the old S$30,000 system. But again, you could always recruit friends and family and use their EZ-Link Wallets, since the cap applied on an individual level.

For obvious reasons, this was discussed in hushed tones. Over the years, I recall seeing a couple of messages about this in the Telegram communities (some of which quickly vanished, which I can only surmise was the result of a vigorous rebuke via PM), and heard about a couple of self-proclaimed financial gurus attempting to “sell” this trick as part of their paid-for classes.

Frankly, I’m amazed (pun?) that this lasted as long as it did, but there were already signs that banks were starting to catch on. Citi excluded SimplyGo in mid-2024, and Maybank followed in December 2025 (note: excluding SimplyGo is not the same as excluding bus and MRT rides, since the transaction description for these is Bus/MRT).

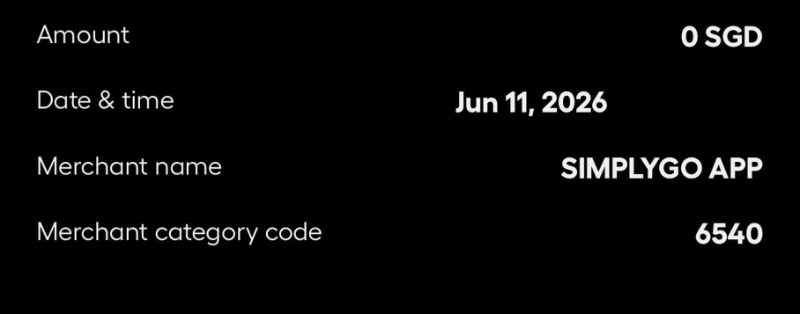

But what ultimately killed this wasn’t the banks — it was the payment processor. From what I understand, SimplyGo used to use Stripe, but when it changed to a different payment processor (on or around 10 June), the MCC was recategorised to 6540, and the merchant description changed to SimplyGo App.

And that, in so many words, was game over. Unless you can find a card which earns rewards for MCC 6540, the EZ-Link Wallet is now a dead-end for miles. But what a ride it was!

I’m sure there will now be tears, recriminations, and the usual vitriol against those who can’t keep their mouths shut, though at the end of the day, that’s the circle of life in the miles game. This won’t be the first hack to be killed, and it certainly won’t be the last.

Make hay.

Conclusion

EZ-Link Wallet top-ups via the SimplyGo app now code as MCC 6540, which brings an end to one of the more enchanted periods in the miles game.

If you want to earn miles on income taxes or other types of bills, you’ll now have to resort to CardUp, Citi PayAll and other bill payment platforms instead, and pay an admin fee for the privilege.

Are there workarounds, you ask?

I have no idea what you’re talking about.

“Snitches get stitches”😂

or, in the case of some gurus, snitches get riches

There would be some that wouldn’t want to see posts like these. It can act as inspiration for future opportunities.

I have only just joined the game, then I saw this …

Damn that was a good run though. Wonder if DBS also noticed people just throwing $1,000 from the Womens World card at SimplyGo every month and not buying anything else…:-p.

And multiple $500 cap on the vantage 🤣

I had a friend that was questioned by his bank as they flagged the top up to simplygo as suspicious. Thankfully didnt happen to me. Sad to see this go – once it’s posted like this means gg

love the last two lines in your conclusion 😀