| Update (8-Oct): BOC has investigated the matter and claims to have refunded the interest costs to all affected customers. Going forward, they say they will proactively identify and reverse such charges, without the need for customers to call in. From what I gather, the process will still be a manual reconciliation, so I’d advise you to keep checking anyway. |

I think it’s safe to say that in general, miles chasers have a very high tolerance for pain.

We don’t mind applying for and keeping track of 10+ credit cards. We’ll trek to an out-of-the-way clinic if they have Paywave. We’ll position ourselves, the wife and the baby to Vietnam just to capitalize on a mistake fare. There’s even a legendary story about someone who, during the Citibank Apple Pay 8 mpd promotion, spent hours tapping his phone multiple times at the same terminal to circumvent the $100 transaction limit.

But yet, everyone has their limits. And BOC seems to like to test them.

BOC’s mysterious interest charges

![]()

When looking through my monthly card statement, I spotted that I’d been charged interest. This was weird, because I always pay in full, via GIRO. There was no shortage of funds in my account, so there’s no reason why the amount shouldn’t have been settled in full.

I called up customer service and learned the following:

- My amount due for the previous month was $4,007.06

- In the current month, I had a refund of $593.86 credited to my card

- The amount deducted from GIRO was therefore $3,413.20

- However, because the system saw that the payment of $3,413.20 was less than the $4,007.06 owed, it charged interest on the $593.86 “outstanding”!

I was astounded that their system wasn’t smart enough to recognise a refund as a partial “payment” of the amount due, but the CSO assured me she would reverse the interest charges and I’d see it on my next statement.

“So what if I didn’t call in?” I asked.

There was a pause.

“Just call in and we’ll waive it for you,” she said again.

I had a separate discussion with a customer service manager, who clarified that BOC’s system sees merchant refunds as a credit balance, but not a payment of the amount outstanding. He said that this “might” lead to situations where customers get charged with interest when they have merchant refunds and GIRO arrangements.

I highlighted the same point again: that customers have the reasonable expectation that a bank’s systems will properly calculate and charge interest, and that it concerned me the bank had no automated way of flagging and reversing such erroneous interest charges. He said he’d pass the message on.

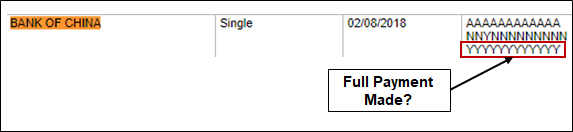

He went on to say he “didn’t believe” it affected CBS credit scores, and based on my latest credit report, that at least seems to be correct. My BOC payment history shows that full payment has been consistently made.

That said, I’d advise anyone in a similar situation to check their score for themselves, because this is something you don’t want to mess around with.

| Update: A few people have reached out to tell me this did affect their CBS score, so you should definitely take a look at your report and get it rectified if necessary |

Now I’m no lawyer, so I can’t speak to the implications of charging interest when it’s not actually due. But from any rational point of view, surely it’s not right to expect the customers to have to spot such things?

Delayed cards, transfer caps and last-century tech

This isn’t the first annoyance I’ve encountered with BOC.

The Milelioness lost her card on 3 July, and reported it the same day. Most banks replace lost cards in 2-3 working days, but most banks aren’t BOC. Days turned to weeks, weeks to months. Calling the bank didn’t help- various CSOs promised me they would “expedite it”, but nothing happened. Finally, the replacement card arrived on 26 August, 36 working days after it was reported lost.

Whatever the reasons for the delay, I think most people would agree that waiting 36 working days for a replacement is just not normal. I mean, the X Card may run out of metal, but have you ever heard of a bank running out of plastic? [Edit: BOC is saying that the reason for the delay was not cardstock shortage, but rather a system switchover. Card replacements should take 7 working days now. Let’s hope so, because 36 working days is insane]

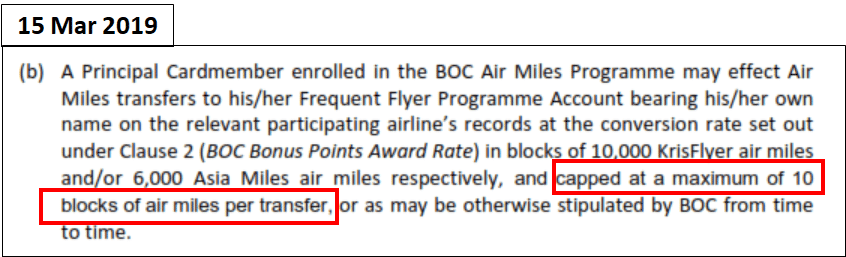

Then there’s the transfer cap that BOC imposed back in March 2019, which makes BOC unique among banks in Singapore in that it caps the maximum number of points you can transfer at one go to 10 blocks, i.e. 60,000 Asia Miles or 100,000 KrisFlyer miles.

If it feels like an arbitrary restriction, that’s because it is. There’s no good reason to cap the number of points that people can transfer at one go (it’s certainly not an IT limitation), and it comes off as an attempt to generate more from transfer fees. At a time when some banks are introducing no-fee transfers on mass market cards, BOC is going in completely the wrong direction.

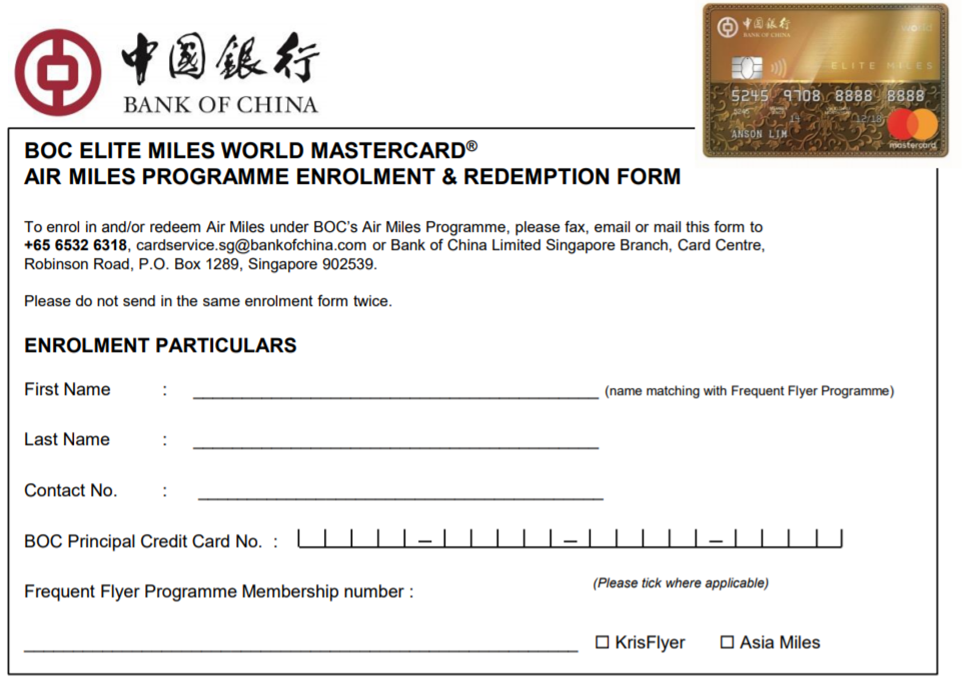

All this set against the backdrop of BOC’s hopelessly antiquated IT. Let’s face it, we knew from the start that banking with BOC wouldn’t be a walk in the park. Linking your credit card to ibanking requires a trip to a BOC branch. BOC ibanking doesn’t support recurring fund transfers. There’s no online rewards portal, so you need to fill up a form to convert credit card points (at least said form is accepted via email!)

There’s even some concerning security flaws in BOC’s ibanking website. Where other ibanking portals are concerned, closing the browser window and attempting to reload it (control-shift-T on Chrome) will give you an error message and require you to log in again. Doing the same with BOC re-opens your currently active banking session, with full access to your account. Yes, it’s best practice to log out when you’re done with your business, but isn’t the hallmark of a good system that it protects people from themselves?

In light of all this, it’s somewhat apt that more than a year after the BOC Elite Miles card was launched, it still doesn’t appear on BOC’s website.

Why don’t I switch?

Like I said at the start, miles chasers can be very forgiving if you ply them with miles. And since the BOC Elite Miles’ earn rate of 1.5/3 mpd on local/overseas spend is among the best in the market, many would-be switchers find themselves stuck with golden handcuffs.

But that’s not what’s stopping me from switching. Sure, I’d have to go from 1.5 to 1.4 mpd on local spending if I switched from BOC Elite Miles to UOB PRVI Miles, but remember: some of that incremental is offset because I’m spending more on conversion fees with BOC thanks to their transfer cap.

Moreover, now that the OCBC 90°N Card is on the market, I can get 4 mpd on all my overseas spending until 29 Feb 2020, 33% better than the BOC. The OCBC 90°N Card also has no geographic restrictions on payment processing- as long as it’s foreign currency, you’ll earn 4 mpd. In contrast, BOC requires that the transaction is processed outside Singapore.

| For all its flaws, the BOC Elite Miles is still one of the few cards that gives miles for insurance payments. Badly-trained BOC CSOs keep sparking panic by telling customers that points for insurance are not being awarded/getting clawed back, but mine have been crediting fine every month. You could, however, instead use the HSBC Revolution to get 2 mpd on insurance payments. |

What is stopping me from switching is the fact I’m using the BOC Smart Saver account.

Unlike most other hurdle accounts, the BOC Smart Saver doesn’t require you to buy any of the bank’s investment products. As someone who prefers to do his own investment, this is a huge plus.

I’m currently earning a very impressive 3.55% p.a on the first S$60,000 of my BOC Smart Saver balance:

- 1.6% from spending >S$1,500 on my BOC Elite Miles card

- 1.2% for crediting a salary of at least S$6,000

- 0.35% for making at least 3 GIRO payments

- 0.4% base interest

The next best alternative, given my circumstances, is to earn:

- 2.4% with DBS Multiplier

- 2.5% with Citi Maxigain (but I can’t withdraw the money without incurring an interest penalty)

- 2.55% with OCBC 360

Giving up my BOC Elite Miles and switching to another bank account basically means forgoing about S$50 a month in interest, or S$600 a year. That’s not even talking about the hassle of updating every one of my GIRO arrangements, so even though I’m tempted to just give up on my BOC Elite Miles card, I can’t do so until I find a better alternative on the bank account side.

Conclusion

If you’ve got a BOC Elite Miles World Mastercard, you should absolutely monitor your monthly statement and ensure you’re not paying interest when you shouldn’t be.

I’m aware that quite a few otherwise hardcore miles chasers have thrown in the towel on BOC already, either because of frustrations with IT, having to wait inordinate periods of time for a replacement card, or points clawbacks. I can’t speak to individual cases, but I suppose if nothing else this experience helps people answer the question: just how much would you endure for miles?

Can this be reported to MAS? I mean, who knows how much they have swindled off people who are less vigilant.

I have a feeling, quite a few. I first saw those interest anomalies in March and it’s still happening. They still haven’t applied a fix clearly.

Fill up hard copy form to convert points to miles.

And this a big China owned bank. Unbelievable….

What makes you think that a big China owned bank should be conforming the to the latest generally accepted best practices in the banking industry? It conforms to whatever the Chinese Communist Party wants. Nothing else. If the CCP wants BOC to have the best banking practice, it’ll happen overnight. If not, don’t even dream about it.

this is the reason why people are protesting in Hong Kong against China

I raise both feet on your comment, always a nightmare when I recall my experience with BOC from the lovely China

It’s probably untrue that the interest was a result of your refund – the CSO might not know the actual reason. I haven’t had a single refund for the past two months, but I have been consistently incurring an “Interest in the Period” of $3.00. Thanks for raising this, because I was still doubting myself if my bill payments didn’t go through on time.

The Gods know what the CSO are for, they are like your worst nemesis! They never do one single thing they promised on their hotline!

Aaron, I wrote to you in March and gave you a heads up about this..

What’s more worrying is that I have to call up every month to get them to reverse. I asked the BOC person on the phone if other customers are being affected by this glitch. She said no and that I was an isolated incident and that it will not happen again. Clearly BS. I have a feeling it’s going to happen again next month…

i just re-read your email, but i never connected the dots until now! i was only able to replicate the problem in july this year, i think it’s because i only set up giro then. previously i was paying on AXS, and i paid whatever the full amount due was regardless of whether i had refunds or not. therefore i never got hit by this before.

I’ve had this problem since 2017 (maybe early 2018), when the BOC Family card was still giving SGD100/month cash rebates. The story they gave me was consistent with yours – bug caused by reversal of charges (the foreign vendors loved to charge me in SGD despite my clear indication for local currency).

Buckle up – I think this issue is here to stay.

thanks for the post. hope BOC fixes it for good, got a few refunds coming in, will watch out.

i lost my card in May… received the replacement yesterday…..

same thing happened to my wife, may lost card in London, new card only arrives last week, saying they are upgrading to paypass card so took longer

It must’ve been a blessing in disguise that I got my cc application rejected… I don’t want all these unnecessary problems to add to my (already arguably) complicated mileslife.

I had a fraud transaction on my BOC card on 1/7/19 and I immediately called in to report it (I got thru after waiting on the phone for 20 minutes!). 2 days later, I called them for a follow up and was told that the investigation process may take up to 3 months! They did not tell me what they will do with the ‘fraud transaction’ and it is after I pressed them to say that it is unfair for me to fork out the payment first while waiting for BOC to do their investigation that they finally offer to… Read more »

Thanks for this article – pretty much sums up the love (and lots of) hate i have with the BOC card/account. Everyday I dream and hope that BOC was as advanced as their WeChat/Alibaba counterparts. I was hit by a fraud attack after a trip to France in September 2018, and I was hit by these interest charges for the likes of 4-5 months while the investigations were going on. Same thing, call every month to have it waived. And lets not even go to the unpleasant tone that most of their CSOs have when you talk to them over… Read more »

I feel you brother…BOC CSO…a new level of “customer service” – Attitude, professionalism, Ethics – All downright bottom

Even cancelling the card takes 2 weeks to complete.

Beware. “Interest in the period” is also charged if your GIRO date happens to fall on a public holiday or weekend. When that happens BOC executes the GIRO on the business day after, and charges you for a number of days interest. Personal experience.

BOC has tried to swindle me off with epic fail dispute resolution refunds, causing merchant banks to be late, had to chase them down via Small Tribunal in order to get it sorted (almost a whole year of settlement back and forth – nvr used them again, too much fraud internally in their operations). MAS is completely useless, their job is to redirect you to banks customer service (which is where the banks fail most). So good luck with anyone continuing their miles game with BOC, you are at HIGH risk for your not-so-high return, meh

Thank you Aaron for educating the public on our “beloved” Bank of China! It’s heartwarming to see that I do not face their atrocities alone, yet its saddening to see many of us going through their banking atrocities

Gotta be wary about these chinese banks..

who knows what they are doing behind the scenes..