If you’re playing the miles game, chances are you’ll have more than one credit card from a given bank. In that case, points pooling is a highly desirable feature, since it minimises conversion fees and orphan miles, and makes card cancellations more frictionless.

In this post, we’ll take a closer look at which banks pool credit card points, and some of the finer details you should be aware of.

Why does points pooling matter?

Points pooling means that points earned on different cards are combined into one central account, instead of being held in individual silos.

Consider the following example. Let’s say I have a total of 27,000 miles with UOB (in the form of 13,500 UNI$) and 27,000 miles with Citibank (in the form of 67,500 TY points).

| 💳 UOB Cards (Points Pooled) |

||

| Card | Points | Total |

UOB Lady’s Card UOB Lady’s Card |

4,500 UNI$ | 13,500 UNI$ |

UOB Preferred Platinum Visa UOB Preferred Platinum Visa |

4,500 UNI$ | |

UOB Visa Signature UOB Visa Signature |

4,500 UNI$ | |

| 💳 Citi Cards (Points Not Pooled) |

||

| Card | Points | Total |

| 22,500 TY points | 22,500 TY points | |

| 22,500 TY points | 22,500 TY points | |

Citi Rewards Visa Citi Rewards Visa |

22,500 TY points | 22,500 TY points |

With UOB, points are pooled, so if I have three cards with 4,500 UNI$ each, I redeem my points from one central pool of 13,500 UNI$.

With Citi, points are not pooled, so if I have three cards with 22,500 ThankYou points, I redeem my points from three separate pools of 22,500 ThankYou points each.

Points pooling therefore offers three big advantages.

(1) Save on conversion fees

Points pooling allows cardholders to save on conversion fees when transferring credit card points to airline miles.

With UOB cards there’s only one central pool to draw from. No matter how many UOB cards I have, I will only pay a single conversion fee when transferring UNI$ to airline miles.

But with Citi cards, each card has its own “points silo” that doesn’t mix with the rest. Therefore, I will have to pay one conversion fee for each card.

(2) Avoid orphan miles

While pooling does not eliminate orphan miles altogether, spending with credit cards that pool points can help reduce the frequency and magnitude of the problem.

Both Citi and UOB have a minimum conversion block of 10,000 miles, but because of the different rules on pooling, you get two very different outcomes.

Here’s the situation with UOB:

| 💳 UOB Cards (Points Pooled) |

||

| Card | Points | Min. Block |

| UOB Lady’s Card |

4,500 UNI$ | 5,000 UNI$ |

| UOB Preferred Platinum Visa |

4,500 UNI$ | |

| UOB Visa Signature |

4,500 UNI$ | |

| Total Points | 13,500 UNI$ | |

| Total Conversion | 2x 5,000 UNI$ | |

| Orphan Points | 3,500 UNI$ | |

Since UOB pools points, I only need to deal with the minimum conversion block once, and that leaves me with 3,500 orphan UNI$.

Then consider Citi:

| 💳 Citi Cards (Points Not Pooled) |

||

| Card | Points | Min. Block |

| 22,500 TY points | 25,000 TY points | |

| 22,500 TY points | 25,000 TY points | |

| Citi Rewards Visa |

22,500 TY points | 25,000 TY points |

| Total Points | 67,500 TY points | |

| Total Conversion | Nothing! | |

| Orphan Points | 67,500 TY points | |

Since Citi does not pool points, I need to deal with the minimum conversion block three times, and since the block requires at least 25,000 ThankYou points, all my 67,500 ThankYou points are orphaned.

See how annoying that is? I have the same number of miles in my Citi and UOB accounts, but I can’t access the ones in my Citi account until each card has reached the minimum conversion block individually!

(3) Simpler cancellations

With points pooling, cancelling cards becomes less troublesome because there’s no need to cash out the points on the cancelled card.

| 💳 UOB Cards (Points Pooled) |

|

| Card | Total |

| UOB Lady’s Card |

13,500 UNI$ (Pooled) |

| UOB Preferred Platinum Visa |

|

|

|

| 💳 Citi Cards (Points Not Pooled) |

|

| Card | Total |

| 22,500 TY points | |

| 22,500 TY points | |

| Citi Rewards Visa |

|

For example, if I were to cancel my UOB Visa Signature, I don’t lose the 4,500 UNI$ associated with the card. Those are already in the central pool, and are unaffected.

On the other hand, if I were to cancel my Citi Rewards Visa, I would lose the 22,500 ThankYou points associated with the card. Therefore I’ll need to cash them out before cancelling the card.

| ⚠️ Warning |

| The above does not apply to DBS, HSBC and Standard Chartered cards. These cards only pool points at the time of redemption, and if you want to cancel a card, you must transfer out all the points associated with it, or else forfeit them. |

Which banks pool points?

Here’s a summary of which banks do and don’t pool points.

| Bank | Pools Points? | Remarks |

|

✓ Yes | |

| ✕ No | ||

| ✕ No | ||

| ✓ Yes | ||

| ✓ Yes | ||

| ✓ Yes | ||

| ✓ ✕ Some |

OCBC has three rewards currencies. Only similar currencies pool | |

| ✓✕ Some |

StanChart has two tiers of cards. Only points from the same tier pool | |

| ✓ Yes |

There is some nuance to this, so be sure to read the details below.

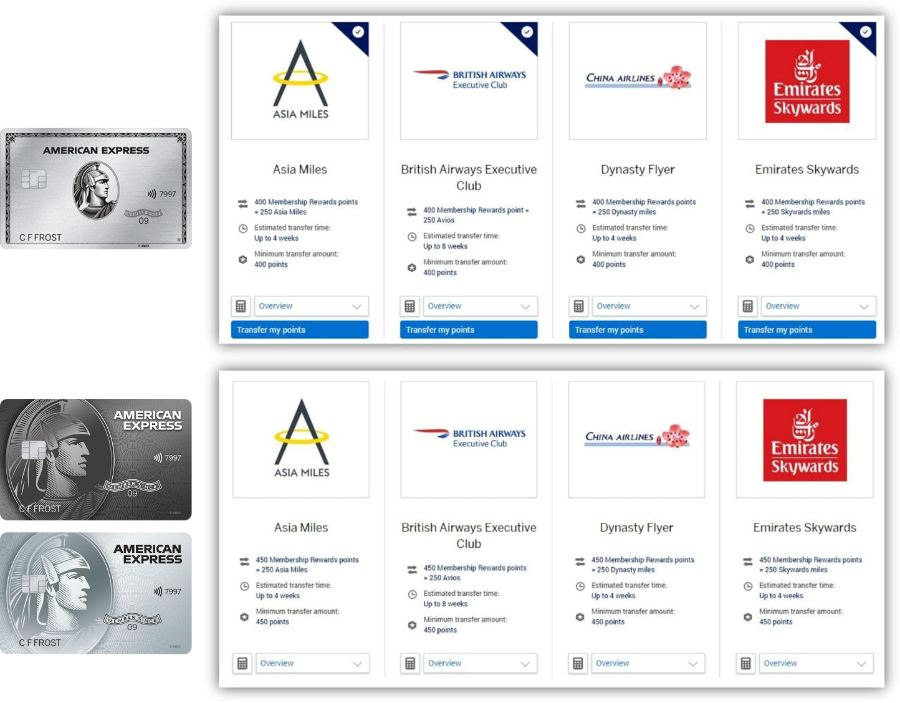

American Express

Membership Rewards points earned on the Platinum cards are pooled, but it’s slightly complicated.

AMEX Platinum Charge cardholders can convert Membership Rewards points to airline miles at a preferential rate of 400 points = 250 miles, versus 450 points = 250 miles for other AMEX cards.

If you hold an AMEX Platinum Charge and an AMEX Platinum Reserve or AMEX Platinum Credit Card, there are two possibilities.

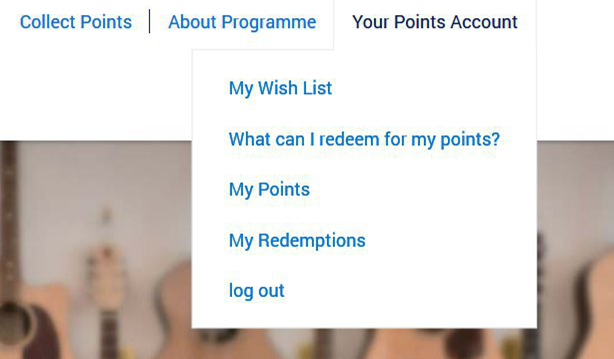

(1) Some people will see their points pooled automatically on the back end, all convertible at the more advantageous 400:250 rate. If you’re in this situation, the drop down menu for “Your Points Account” will look like this.

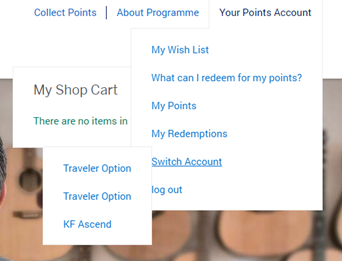

(2) Some people will not see their points pooled on the back end. Instead, they’ll have one points account for their AMEX Platinum Charge, and another points account for their AMEX Platinum Reserve/Platinum Credit Card. If you’re in this situation, the drop down menu for “Your Points Account” will have a “Switch Account” button to toggle between points balances.

In this case, you can call up customer service to get your points manually combined and transferred at the more advantageous 400:250 rate.

The points pooling concept is irrelevant for the American Express KrisFlyer cobrand cards, because miles are automatically credited to the linked KrisFlyer account with no transfer fees (plus, you can’t own more than one KrisFlyer cobrand card anyway).

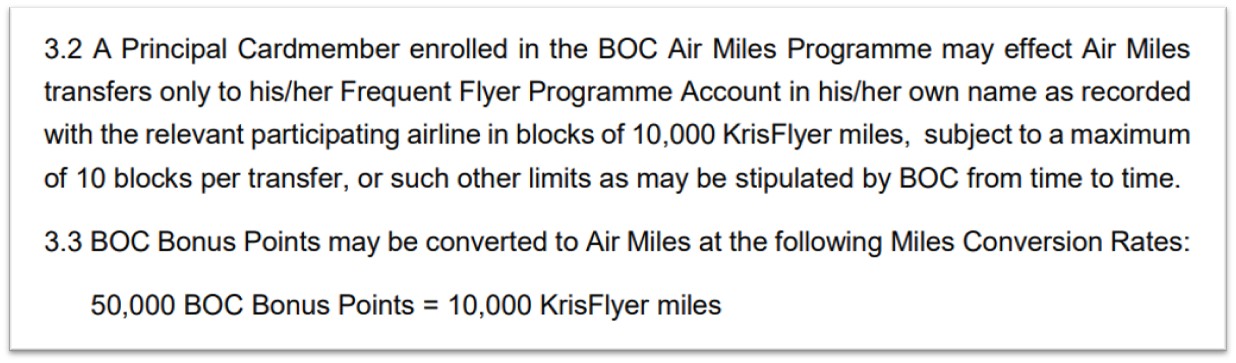

Bank of China

While Bank of China only has one miles card in their entire portfolio, you may still end up paying multiple conversion fees anyway!

That’s because in March 2019, BOC capped the maximum number of points that can be converted in a single transaction at 10 blocks. This works out to 100,000 KrisFlyer miles, and means that if you want to convert, say, 250,000 KrisFlyer miles, you’d pay $30.56 x 3 =$91.68 of conversion fees.

It’s a very silly and arbitrary rule, but it wouldn’t be BOC if it wasn’t.

Citibank

![]()

Citi has two different points currencies:

- Citi Miles (earned by the Citi PremierMiles Card)

- ThankYou points (earned by the Citi Prestige, Citi Rewards and Citi ULTIMA Cards)

Sadly, points are not pooled — not even within the same currency type — so you’ll pay as many conversion fees as you have cards.

DBS Bank

![]()

DBS Points are kept separate on the back end, but pooled together at the time of redemption.

However, outside of redemptions, DBS Points are kept separate. This means that if you cancel a given DBS card, you’ll forfeit all points earned on that card. Cash them out before cancelling!

| ⚠️Complication |

|

When redeeming DBS Points, the DBS system will deduct those with the earliest expiry first. As a reminder:

This is usually a good thing, but it can create a problem when you’re trying to cancel a card lower down the redemption priority. For example, if I want to cancel my DBS Altitude Card, I must redeem all the DBS Points on my DBS Woman’s World Card first, before I can cash out the DBS Points on the DBS Altitude Card. If you have two cards which both earn non-expiring points, the points on the card with the smaller card number will be deducted first. |

HSBC

![]()

HSBC Rewards Points are kept separate on the back end, but pooled together at the time of redemption.

However, outside of redemptions, HSBC Rewards Points are kept separate. This means that if you cancel a given HSBC card, you’ll forfeit all points earned on that card. Cash them out before cancelling!

| ⚠️Complication |

|

Just like DBS cards, there is a potential complication when cancelling HSBC cards. When redeeming HSBC Rewards Points, the system will deduct those with the earliest expiry first. While all HSBC Rewards Points have a standard validity of 37 months, a problem can arise when you are cancelling a “younger vintage” card. For example, suppose you got a HSBC Revolution Card three years ago, and a HSBC TravelOne Card one year ago, and plan to cancel the latter. You will need to transfer out the older points on the Revolution first before you can get to the younger points on the TravelOne. |

Maybank

Maybank TREATS Points are pooled across all cards.

If you have a Rewards Infinite membership (earned by spending at least S$24,000 in a membership year, or holding a Maybank Visa Infinite or Maybank World Mastercard), the benefit of non-expiring points extends to your entire TREATS balance.

OCBC Bank

![]()

OCBC has three different points currencies:

- 90°N Miles (OCBC 90°N Mastercard, OCBC 90°N Visa)

- OCBC$ (OCBC Rewards, OCBC Premier Visa Infinite)

- VOYAGE Miles (OCBC VOYAGE)

Similar points currencies will be pooled, but different points currencies will not.

For example, any OCBC$ I earn on the OCBC Rewards Card can be pooled with OCBC$ earned on the OCBC Premier Visa Infinite. However, OCBC$ I earn on the OCBC Rewards Card cannot be pooled with 90°N Miles earned on the OCBC 90°N Mastercard/Visa.

Standard Chartered Bank

![]()

Standard Chartered has two different tiers of cards

- Tier 1: Beyond, Journey, Priority Visa Infinite, Visa Infinite

- Tier 2: All other cards

| Tier 1 Points | Tier 2 Points | |

| Conversion Fee | S$27.25 per conversion |

|

| Expiry? | No expiry | Up to 3 years |

| Conversion Rate |

25,000 pts = 10,000 miles | 34,500 pts = 10,000 miles |

Points are pooled within tiers, but not across tiers (so you can’t combine Tier 1 and 2 points in a single redemption, for example).

Like DBS and HSBC, Standard Chartered only pools points for the purposes of redemptions. You must convert all your points before cancelling a card, or else forfeit them.

UOB

![]()

UOB UNI$ are pooled across all cards.

UOB Privilege Banking Visa Infinite, UOB Reserve, UOB Visa Infinite and UOB Visa Infinite Metal Card members enjoy complimentary conversions, so if you have one of these cards, you could use it as a conduit to convert points earned on other UOB cards for free!

Do note that the KrisFlyer UOB Credit Card is a cobrand card that does not earn UNI$; instead, KrisFlyer miles earned are deposited directly into your KrisFlyer account once a month.

Conclusion

Not pooling points is a very customer-unfriendly decision, but my guess is that banks which don’t allow it aren’t doing so deliberately. More likely than not, it’s a hangover from an outdated IT system where points were kept in silos, which no one dares to touch.

That said, the lack of points pooling may not necessarily be a deal-breaker. I’d argue that it’s still worth using Citi cards, for example, thanks to the sheer variety of transfer partners and the opportunity to earn 4 mpd on online transactions with the Citi Rewards Card.

How important is points pooling to you?

do points earned from supplementary cards of these banks count and pool to the main card?

Yes, pool to main card

“SC x-card – if you got the 100,000 miles bonus from $6,000 of local spending”

It’s any spending isn’t it? Not just local spending.

I mean if you earned the 100k miles via 6k of local spending your total haul would be 107.2k.

You describe the nuances of these banks and their respective cards well. Thank you!

Just a minor point, I don’t think you will lose all the uni$ with uob even after you cancel your last mile earning card. The balance will still be the same after you next reapply another uob miles earning card. I had an experience where I had a negative balance (long story) and it was there even after I cancelled all my cards.

How did you manage to get negative points? Is it a corner case or something people can easily fall into?

Interesting! But if you close all your card accounts, you’re saying they still have a “memory” of you?

yup, i charged hospitalisation bill and got uni$ and then redeemed it. then the insurance refunded the money and they had to deduct the points. i then cancelled all my cards in boycott but when i reapplied in future, the “debt” is still there. apparently the memory is for life.

But don’t UNI$s have an expiry? Surely they won’t show up if they have expired. Maybe this only applies to negative balances. A rather confusing issue, if UOB deducts my UNI$s for annual “fee”, and wouldn’t waive it, and I cancel my card, but my UNI$s were to expire in March 2020, would they refund the UNI$s – and with what expiry date? (Assuming I have another card)

https://pib.uob.com.sg/assets/images/web/rewards/rewardsplus_tnc.pdf 1.5 If the Principal Cardmember’s Credit Card account is terminated at any time for any reason, whether by the Principal Cardmember or UOB, the Principal Cardmember and the Supplementary Cardmember shall be disqualified from participating in the Programme and ***> all unused UNI$ then accrued shall automatically be cancelled and no longer be available for use <*** by the Cardmember. Such UNI$ shall not be transferable to any other Account of the Cardmember. There are plenty of other T&Cs which give UOB the right to cancel, claw back, exclude and deduct uni$ without any recourse by the customer. I… Read more »

It seems then it’s not possible to transfer UNI$ from a cancelled account to an active one. But the article above says “Since UOB points pool, cancelling a given card has no impact on my total points balance, assuming it’s not my last points-earning card with the bank.”? So who’s correct 😱

The insurance refunded back to your card?

Or rather insurance paid hospital and hospital refunded back to your card?

Otherwise how will UOB know?

But wouldn’t u then have a credit balance on your card and subsequently when u spend using that u would have earned back the equivalent uni$ back and bring things back to status quo?

Or (gasp!) did u forfeit the credit when u cancelled the cards?

Hi Aaron!

Does it mean that if I have both the pink and blue titanium cards and I cancel one, the points of the cancelled one will not be forfeited?

What about for scb vi and x vi?

You wrote the points from these 2 cards are pooled for redemption but technically they are still kept in separate pools and cancelling one will mean a forfeiture of the points?

yes, so long as you have one ocbc$ earning card, you will retain the points from both cards

for scb vi and scb x, cancelling one will lead to forefeiture of points. points are only pooled for the purposes of redemption.

confusing, isn’t it?

Thanks for the reply Aaron!

Especially on a topic u wrote a year ago

It’s only confusing because each bank has its own system, I actually find the dbs/scb more logical though uob/ocbc is certainly more friendly

Annoying thing with the way DBS does it is that you’d have to redeem all points to cancel an Altitude card without losing the miles collected on it.

Redemptions would otherwise be first deducted from the WWMC balance as these expire earlier.

Can we pool points from different bank CCs into 1 common account like Krisflyer? Thanks

What about the situation when one holds a Amex corporate card, and also personal Amex platinum card? Can the points from those two cards pool?