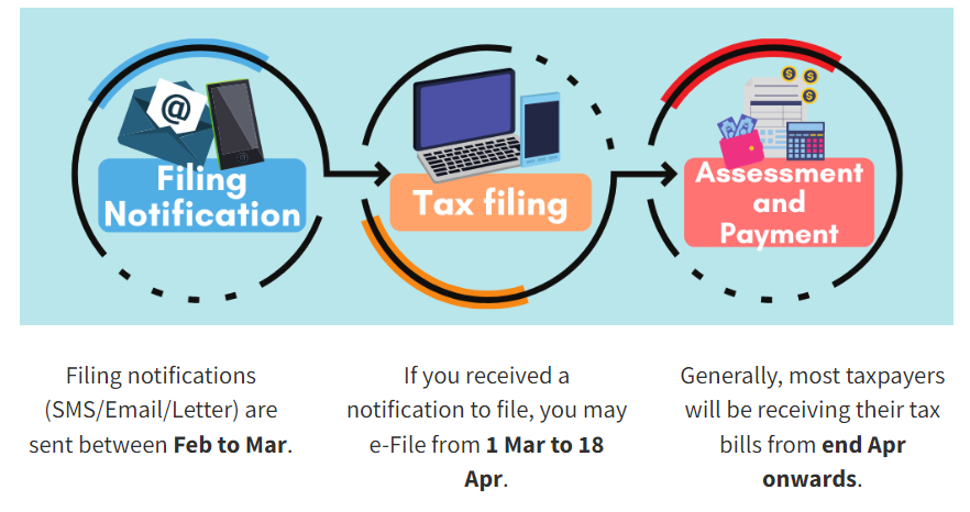

Income tax season is underway for YA 2024, and you probably know the drill by now. Individuals with income tax obligations will need to file their taxes by 18 April 2024. They’ll subsequently receive their tax bill (NOA) from the end of April onwards.

Few people relish paying taxes, but here’s the good news: if you don’t mind paying a small admin fee, it’s a great opportunity to earn some extra miles in the process.

|

| Tax Season 2024 |

| 💰 The MileLion’s Income Tax Guide 2024 |

How do I pay my income tax bill with a credit card?

IRAS doesn’t accept credit card payments. In their own words:

Credit card payments are not offered by IRAS directly because of the high transaction costs charged by the credit card service providers. This is to keep the cost of collection low to preserve public funds.

However, this doesn’t mean you can’t use your credit card to pay taxes. Banks and bill payment platforms offer tax payment facilities, which allow cardholders to earn rewards in exchange for a small fee.

I divide these into “indirect” and “direct”.

| Indirect Payment Facilities | Direct Payment Facilities |

|

|

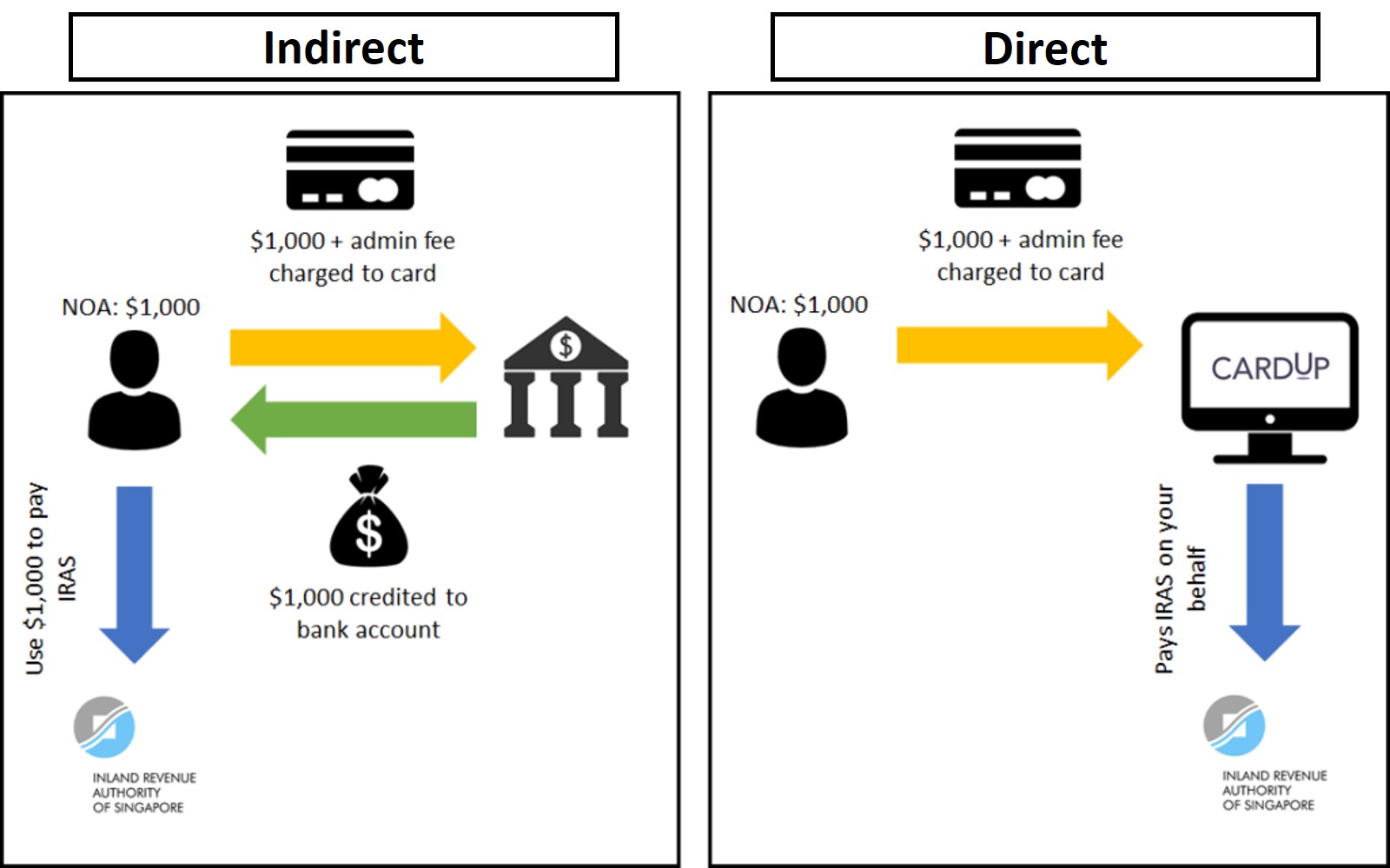

Both indirect and direct facilities work the same in the sense that your credit card is charged for the tax amount due plus an admin fee, earning miles in the process.

Where they differ is that:

- An indirect payment facility deposits the amount due into your designated bank account, in cash. You’re still responsible for paying IRAS

- A direct payment facility pays IRAS on your behalf

Whether it’s better to use an indirect or direct facility all boils down to the cost per mile: the admin fee, divided by the miles you earn.

What’s changed for YA2024?

Here’s a summary of the key changes that have taken place since last year’s article.

StanChart hikes tax facility admin fee to 1.9%

Effective 15 March 2024, Standard Chartered has hiked the cost of its Visa Infinite income tax payment facility from 1.6% to 1.9%.

This increases the lowest possible cost per mile from 1.14 cents to 1.36 cents– still good, but obviously not as good as before.

Citi PayAll hikes service fee to 2.6%

In April 2024, Citi PayAll hiked its service fee from 2.2% to 2.6% for all cards, which increases the cost per mile significantly.

That said, they’re also running a promotion that offers up to 2 mpd for income tax payments, but you’ll still be paying more per mile than you did in 2023.

AMEX HighFlyer Card no longer supports CardUp

![]()

While this isn’t strictly related to income tax, you should also know that the AMEX HighFlyer Card no longer works for CardUp transactions, which nerfs the highest-earning general spending option (1.8 mpd) at your disposal.

In case you’re wondering who to get mad at, the restriction is on the AMEX side.

What are the fees involved?

Here’s a list of the various payment facilities and the applicable fees.

| 🧾 List of Payment Facilities |

||

| Bank | Applicable Cards | Admin Fee |

Indirect |

SCB Visa Infinite | 1.9% |

Indirect |

UOB PRVI Miles, Visa Infinite Metal, Reserve | 1.7-2.2% |

Direct |

All cards except HSBC | 1.75-2.25% |

Indirect |

OCBC VOYAGE | 1.9% |

Link LinkDirect |

All SCB cards | 1.9% |

Link LinkDirect |

All Citi cards | 2.6% |

Direct |

All DBS cards | 2.5% |

| There is an additional option called ipaymy, but for reasons outlined in this post, I neither endorse nor comment on their services | ||

It may be tempting to compare options on the basis of admin fees, but that’s only half the story. You need to also consider the earn rate.

For example, the OCBC VOYAGE Payment Facility has an admin fee of 1.9%, but the earn rate is 1 mile per S$1 charged (instead of the usual 1.3 mpd). This means the cost per mile is 1.9 cents.

In contrast, Citi PayAll has a higher admin fee of 2.6%, but the Citi ULTIMA Card earns 1.6 miles per S$1 charged. This means the cost per mile is lower then VOYAGE, at 1.63 cents.

Keep in mind that banks may apply different earn rates for income tax payments as opposed to regular retail spend. For example:

- the UOB PRVI Miles Card normally earns 1.4 mpd, but awards 1 mpd for UOB Payment Facility transactions (you’ll earn 1.4 mpd via CardUp, though)

- all DBS cards earn a flat 1.5 mpd for income tax payment plans, instead of their usual rates.

If this is too complicated for you, the next section should make everything very clear.

What are my options for paying tax with a credit card?

CardUp

CardUp has announced their YA 2024 income tax payment promotion, which offers a 1.75% fee for Visa, and 1.99% fee for Mastercard.

| Visa | Mastercard | |

| Code | MLTAX24 | MCTAX24 |

| Admin Fee | 1.75% | 1.99% |

| Schedule by | 31 Aug 24 | 31 Aug 24 |

| Due by | 25 Mar 25 | 11 Sep 24 |

| Valid For | One-off or recurring | One-off |

Citi PayAll

|

| Citi PayAll Promo |

Citi PayAll’s promotion this year features:

- 2 mpd on all Citi PayAll tax transactions

- 1.6 mpd on all Citi PayAll non-tax transactions

This is subject to a minimum spend of S$5,000 on non-tax transactions on a single card, and capped at S$150,000 across all Citi PayAll categories.

I’ve written a detailed post covering the offer here.

Cost Per Mile

Shown below is the lowest possible price you can pay for miles with each card, denoted by CPM (cost per mile, in cents).

For the sake of brevity, I am not showing multiple options for each card, only the lowest. For example, Citi ULTIMA Visa cardholders could also pay income tax via Citi PayAll and buy miles from upwards of 1.3 cents, but the cheaper option would be to use CardUp, so that’s what’s mentioned in the table.

| 💰 Summary of Tax Payment Options |

|||

| Card | Pay Via | Fee (MPD) |

CPM |

Citi ULTIMA Visa Citi ULTIMA Visa |

CardUp | 1.75% (1.6 mpd) |

1.07¢ |

| Use CardUp with MLTAX24, valid till 31 Aug 24 | |||

DBS Insignia DBS Insignia |

CardUp | 1.75% (1.6 mpd) |

1.07¢ |

| Use CardUp with MLTAX24, valid till 31 Aug 24 |

|||

OCBC VOYAGE OCBC VOYAGE (Premier, PPC, BOS) |

CardUp | 1.75% (1.6 mpd) |

1.07¢ |

| Use CardUp with MLTAX24, valid till 31 Aug 24. New users use OCBC15 for 1.5% fee (0.92 cpm), valid till 31 Dec 24 |

|||

UOB Reserve UOB Reserve |

CardUp | 1.75% (1.6 mpd) |

1.07¢ |

| Use CardUp with MLTAX24, valid till 31 Aug 24 | |||

| CardUp | 1.75% (1.5 mpd) |

1.15¢ | |

| Use CardUp with MLTAX24, valid till 31 Aug 24 | |||

Citi ULTIMA MC Citi ULTIMA MC |

CardUp | 1.99% (1.6 mpd) |

1.22¢ |

| Use CardUp with MCTAX24, valid till 31 Aug 24 | |||

UOB PRVI Miles Visa UOB PRVI Miles Visa |

CardUp | 1.75% (1.4 mpd) |

1.23¢ |

| Use CardUp with MLTAX24, valid till 31 Aug 24 | |||

UOB Visa Infinite Metal UOB Visa Infinite Metal |

CardUp | 1.75% (1.4 mpd) |

1.23¢ |

| Use CardUp with MLTAX24, valid till 31 Aug 24 | |||

StanChart Visa Infinite StanChart Visa Infinite |

CardUp | 1.75% (1.0/1.4 mpd) |

1.23¢ 1.72¢ |

| Use CardUp with MLTAX24, valid till 31 Aug 24 | |||

Citi Premier Miles Citi Premier Miles |

Citi PayAll | 2.6% (2 mpd) |

1.3¢ to 1.62¢ |

| Must pay at least S$5,000 in non-tax payments (@ 1.6 mpd), so your blended cpm will fall within the range of 1.3-1.62 cents. Valid till 31 Jul 24. Details here. | |||

Citi Prestige Citi Prestige |

Citi PayAll | 2.6% (2 mpd) |

1.3¢ to 1.62¢ |

| Must pay at least S$5,000 in non-tax payments (@ 1.6 mpd), so your blended cpm will fall within the range of 1.3-1.62 cents. Valid till 31 Jul 24. Details here. | |||

| Citi PayAll | 2.6% (2 mpd) |

1.3¢ to 1.62¢ |

|

| Must pay at least S$5,000 in non-tax payments (@ 1.6 mpd), so your blended cpm will fall within the range of 1.3-1.62 cents. Valid till 31 Jul 24. Details here. | |||

DBS Altitude Visa DBS Altitude Visa |

CardUp | 1.75% (1.3 mpd) |

1.32¢ |

| Use CardUp with MLTAX24, valid till 31 Aug 24 |

|||

OCBC 90°N Visa OCBC 90°N Visa |

CardUp | 1.75% (1.3 mpd) |

1.32¢ |

| Use CardUp with MLTAX24, valid till 31 Aug 24. New users use OCBC90N15 for 1.5% fee (1.14 cpm), valid till 31 Dec 24 | |||

OCBC VOYAGE OCBC VOYAGE |

CardUp | 1.75% (1.3 mpd) |

1.32¢ |

| Use CardUp with MLTAX24, valid till 31 Aug 24. New users use OCBC15 for 1.5% fee (1.14 cpm), valid till 31 Dec 24 | |||

OCBC Premier Visa Infinite OCBC Premier Visa Infinite |

CardUp | 1.75% (1.28 mpd) |

1.34¢ |

| Use CardUp with MLTAX24, valid till 31 Aug 24. New users use OCBC15 for 1.5% fee (1.15 cpm), valid till 31 Dec 24 | |||

UOB PRVI Miles MC UOB PRVI Miles MC |

CardUp | 1.99% (1.4 mpd) |

1.39¢ |

| Use CardUp with MCTAX24, valid till 31 Aug 24 | |||

StanChart Journey StanChart Journey |

CardUp | 1.75% (1.2 mpd) |

1.43¢ |

| Use CardUp with MLTAX24, valid till 31 Aug 24 | |||

OCBC 90°N MC OCBC 90°N MC |

CardUp | 2% (1.3 mpd) |

1.51¢ |

| Use CardUp with OCBC90NMC, valid till 30 Jun 24. New users use OCBC90N15 for 1.5% fee (1.14 cpm), valid till 31 Dec 24 | |||

KrisFlyer UOB KrisFlyer UOB |

CardUp | 1.99% (1.2 mpd) |

1.63¢ |

| Use CardUp with MCTAX24, valid till 31 Aug 24 | |||

DBS Altitude AMEX DBS Altitude AMEX |

DBS | 2.5% (1.5 mpd) |

1.67¢ |

| Use DBS My Preferred Payment Plan for Income Tax Payment | |||

UOB PRVI Miles AMEX UOB PRVI Miles AMEX |

CardUp | 2.6% (1.4 mpd) |

1.81¢ |

| Use CardUp (no promo code) | |||

BOC Elite Miles BOC Elite Miles |

CardUp | 1.99% (1.2 mpd) |

1.95¢ |

| Use CardUp with MCTAX24, valid till 31 Aug 24 | |||

AMEX PPS Card AMEX PPS Card |

CardUp | 2.6% (1.3 mpd) |

1.95¢ |

| Use CardUp (no promo code) | |||

AMEX Solitaire PPS Card AMEX Solitaire PPS Card |

CardUp | 2.6% (1.3 mpd) |

1.95¢ |

| Use CardUp (no promo code) | |||

| CardUp | 2.6% (1.2 mpd) |

2.11¢ | |

| Use CardUp (no promo code) | |||

AMEX KrisFlyer Credit Card AMEX KrisFlyer Credit Card |

CardUp | 2.6% (1.1 mpd) |

2.30¢ |

| Use CardUp (no promo code) | |||

AMEX Centurion AMEX Centurion |

CardUp | 2.6% (0.98 mpd) |

2.59¢ |

| Use CardUp (no promo code) | |||

| CardUp | 2.6% (0.78 mpd) |

3.25¢ | |

| Use CardUp (no promo code) | |||

AMEX Platinum Credit Card AMEX Platinum Credit Card |

CardUp | 2.6% (0.69 mpd) |

3.67¢ |

| Use CardUp (no promo code) | |||

AMEX Platinum Reserve AMEX Platinum Reserve |

CardUp | 2.6% (0.69 mpd) |

3.67¢ |

| Use CardUp (no promo code) | |||

| ❓How is this calculated? |

|

For CardUp, both the admin fee and the tax payment earn miles, so a S$1,000 payment with a 1.75% fee placed on a 1.2 mpd card earns 1,221 miles (S$1,017.50 x 1.2 mpd, ignoring rounding). This works out to 1.43 cents per mile (S$17.50/1,221 miles) For bank facilities, only the tax payment earns miles, so a S$1,000 payment with a 1.75% fee placed on a 1.2 mpd card earns 1,200 miles. This works out to 1.46 cents per mile (S$17.50/1,200) |

| ❓ First CardUp payment? |

| If this is your first-ever CardUp payment, use the code MILELION to save S$30 off your first payment of any amount. You can subsequently use any other promo code for existing customers (e.g. MLTAX24) |

| ❓ Where’s my card? |

| If you don’t see your card mentioned above, e.g. HSBC Revolution or UOB Preferred Platinum Visa, there’s a good reason. These cards either don’t earn miles on tax payments (e.g. HSBC), or earn such a low rate that the cost per mile becomes prohibitive. |

Other important points

Apply for as many facilities as you want

If you hold more than one of the cards above, there’s nothing stopping you from applying for multiple tax payment facilities in order to buy more miles (otherwise known as churning).

For example, someone with a S$10,000 tax bill could apply for both the StanChart Visa Infinite tax payment facility and set up a payment arrangement with CardUp.

Take particular care if you’re applying for two direct payment facilities, however, because overpaying your tax bill will trigger a refund from IRAS, and a possible clawing back of the miles by the bank.

|

“Where we have determined in our discretion exercised reasonably that your Payment(s) to IRAS exceed the amount of taxes which you are required to pay to IRAS, we shall be entitled to claw back any rewards credited to your card account in connection with any amount so overpaid to IRAS using the Service. In such an event, we will refund the relevant portion of Fee in respect of such overpaid amount.” |

There’s no chance of this happening with indirect payment facilities, because the onus is on you to pay IRAS. What you do with the cash after it’s deposited into your account is your own business.

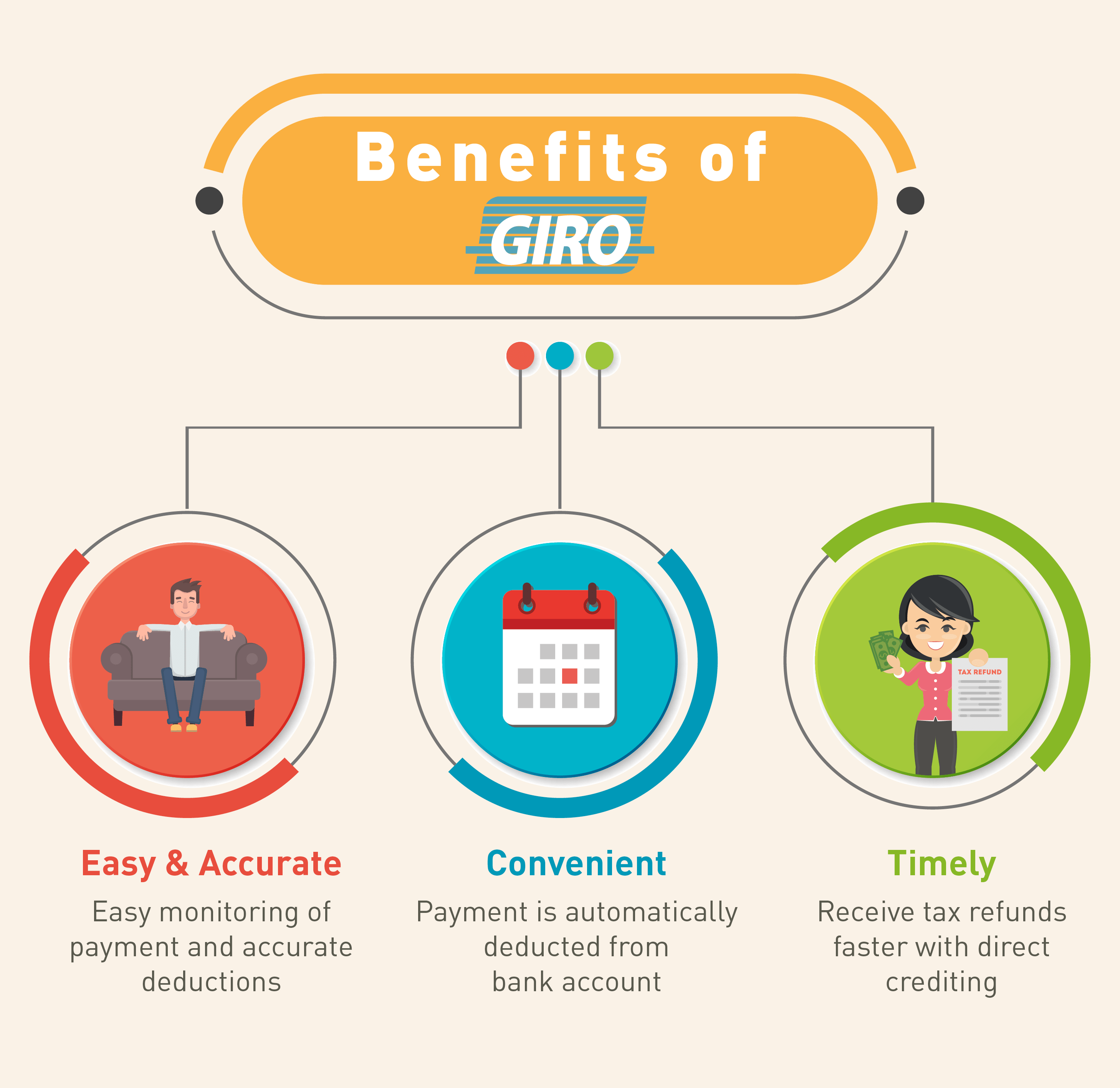

You can still use GIRO

IRAS allows taxpayers to split their payment into 12 interest-free instalments via GIRO. This is great for maximizing your cashflow, and something I opt for each year.

Setting up GIRO for income tax can be done via the following methods:

- Instant

- myTax portal (DBS/POSB and OCBC customers)

- Internet banking (DBS/POSB, OCBC and UOB customers)

- AXS stations (DBS/POSB customers)

- 3 weeks processing

- GIRO application form (all bank customers)

Once your GIRO arrangement has been approved, you can view the monthly instalment by logging to myTax Portal, selecting Account > View Payment Plan > View Plan.

There are no issues using GIRO if you opt for an indirect payment facility, as the bank simply credits the cash to your account, and how you go about paying IRAS after that is up to you.

It’s also possible to use GIRO when you’re paying via a direct payment facilities, though you’ll want to make manual payments well in advance of each month’s scheduled deduction (on the 6th of each month) to avoid double payment.

To illustrate, suppose your tax bill is S$12,000 and you opt for GIRO. IRAS will split your tax bill such that S$1,000 comes due each month.

| Month | Manual Payment | GIRO | Total Paid |

| May 2024 | – | S$1,000 | S$1,000 |

| Jun 20224 | – | S$1,000 | S$2,000 |

| Jul 2024 | S$400 | S$600 | S$3,000 |

| Aug 2024 | – | S$1,000 | S$4,000 |

| Sep 2024 | S$1,500 | – | S$5,500 |

| Oct 2024 | – | S$500 | S$6,000 |

| Nov 2024 | – | S$1,000 | S$7,000 |

| Dec 2024 | – | S$1,000 | S$8,000 |

| Jan 2025 | – | S$1,000 | S$9,000 |

| Feb 2025 | – | S$1,000 | S$10,000 |

| Mar 2025 | – | S$1,000 | S$11,000 |

| Apr 2025 | – | S$1,000 | S$12,000 |

Suppose you make a manual payment of S$400 in July 2024. According to your payment schedule, you were supposed to pay S$1,000 in July, so GIRO will automatically adjust to deduct S$600 instead of S$1,000 for that month.

Then suppose you make a manual payment of S$1,500 in September 2024. According to your payment schedule, you only needed to pay S$1,000 in September, so GIRO won’t take any deduction for this month.

When October 2024 comes round, assuming you make no further manual payment, GIRO will deduct S$500 to put you “back on schedule” with S$6,000 paid off by the end of October 2024.

Now, it’s important to keep in mind that IRAS GIRO deductions take place on the 6th of the month the tax is due (or the next working day if that happens to be a weekend or public holiday). If your manual payment is made close to this date, it’s possible the regular GIRO deduction will still take place.

Per my understanding, the cut-off is the last day of the month before, so if you make a manual payment on 1 April, the reduction will be in effect for May’s taxes (and not April). In any case, the CardUp system won’t let you schedule payments during the last few and first few days of each month.

For more instructions on how to setup a recurring income tax payment series with CardUp, refer to this link.

When miles will be credited?

If you’re using CardUp, you can expect your credit card points to be awarded once the transaction posts.

However, if you’re using Citi PayAll, only the base points will be posted with the transaction. You’ll need to wait until 20 November 2024 to receive the bonus component.

So if you’re hoping to use your miles for a trip in the near future, that’s something you need to factor in too.

What type of points are you earning?

When evaluating two cards with similar cost per mile figures, it’s helpful to think of qualitative factors as well”

- Do points expire?

- Do points pool?

- How many transfer partners are available?

- Is there a fee for transferring points?

For example, Citi Miles would be superior to DBS Points or UOB UNI$, thanks to the sheer number of transfer partners available. Likewise, non-expiring Citi Miles and 90°N Miles would be more useful than expiring UNI$ or HSBC Rewards Points.

Conclusion

Income Tax Season 2024 has begun, and we’re starting to see the promotions roll out. The current lowest cost per mile starts from 1.07 cents, which can be attractive especially for those looking to redeem First and Business Class tickets.

I’ll be updating this article as new tax payment promotions are announced, so be sure to bookmark it for future reference.

Anyway to use HSBC to pay ?

No. Hsbc ended its own tax payment facility in 2023, and excludes cardup and ipaymy from earning points

Say if I were to use the UOB Payment facility with UOB Visa Infinite Metal card, would it then be about 1.4 cents per mile ? Is my calculations correct?

Would it be possible to have a separate table without Cardup as the primary payment facility ?

churning? I don’t think that word means what you think it means.

Many will tap on this opportunity to meet the credit card sign-up gift requirement (500/1000/1500 or Citi Prestige 2000 for 2 months), do you want to include a section on this?

How should I go about doing this if I’m making monthly payments on my income tax? Do I need to set up a 1 one-time payment with the first promo for the first month’s payment, and then set up the remaining balance as a separate recurring payment with the second promo?

yup that’s right!

Hi, what if i am making a first time lump sum payment? I can only use the $30 off, and can’t stack the 2 promos? Thank you!

Hi Aaron, could you please confirm if we are able/unable to stack the 2 promos together in separate payments for the same tax NOA? Thanks!

Any idea if Amex (plat) would ever be added to the promo bucket?

cardup has amex promo codes from time to time. i think there’s a decent chance, though the timeline may not be so soon.

The summary table shows 1.3mile per $ for DBS Altitude Visa whereas the information above it states 1.5mile per $ for ALL DBS cards. Which is correct?

keep in mind the earn rates are different depending on what method you use. you earn 1.3 mpd via cardup, 1.5 mpd via dbs own payment scheme.

UOB PP card is not on the list?

The Standard Chartered Visa Infinite Income Tax Payment Facility states a cashback capped at $300, and first 50 applications per calendar month. The example SC showed was Tax of $80,000 at 1.9% fee ($1520) and get cashback of $300. It is not clear if one still earn the points

thanks for the heads up! will take a look at that.

I already have Giro set up to pay my taxes monthly. So if I were to keep that arrangement, I can only do “indirect” payment right? If yes, my only options is UOB, Standchart or OCBC. of the 3, which card gives the best CPM? I would also want to use that same card for daily use to increase the rate of earning the miles. thanks in advance.

Hi Aaron,

I still have my Citibank Premiermiles VISA card. What would the earn rate be?

Hi Aaron, if i want to pay with CardUp monthly, do i need to apply for GIRO on IRAS first? Because i see that the full amount is payble by May. And if i apply for GIRO, it will deduct from my POSB bank account. How do i then use card up to pay?

Ocbc tax payment facility only available for the one time payment with 1.9% fee. They discontinued the other repayment option of 12 monthly installments with 2.85% fee.

for Citi cards, what would the CPM be like if unable to hit the 5k spending for Citi PayAll? Would CardUp be a better option in this case?

Should also factor in the interest that you would have earned for the “direct” facility. Had you paid by installment (interest free), you could have earned at least 3% interest pa for amounts that would have still been in your bank account but now went to re-payment. This could come up to over $100 depending on the NOA amount. So, amount that you are “purchasing” the miles = processing fee + interest that you could have earned.