Well that was fun.

Yesterday morning, I wrote about LiquidPay 2.0, a new way of earning credit card rewards at QR code-only merchants, and basically the second coming of XNAP.

24 hours later, LiquidPay has stopped accepting credit cards, and — where domestic payments are concerned at least — has become little more than a glorified PayNow wrapper.

For those who missed the festivities, here’s my attempt at a post-mortem on what must have been a very long day for LiquidPay.

A long day for LiquidPay

Last week, Liquid Group launched LiquidPay 2.0, the second iteration of its platform offering cross-border payments, remittances, and interoperable QR code payments in Singapore and abroad.

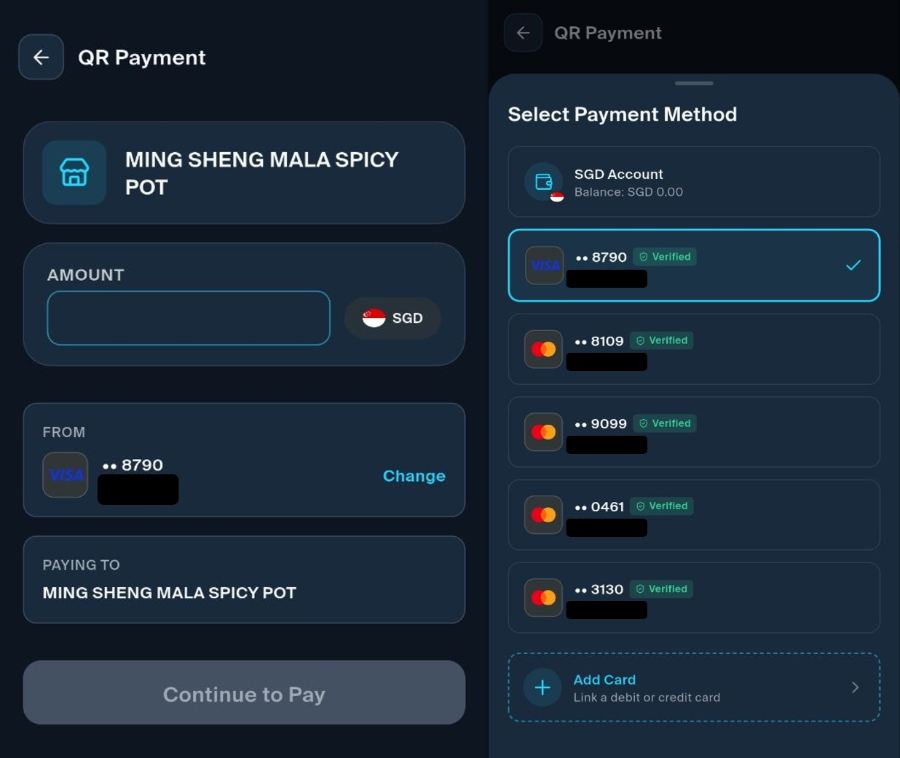

LiquidPay offered users two ways of paying:

- Cards

- Liquid Account

Card payments were only available at merchants participating in the LiquidPay (or legacy XNAP) scheme.

For all other merchants, users had to pay via their Liquid Account, by topping up their balance and making a PayNow transfer.

While the return of credit card rewards on QR payments was exciting, it was always living on borrowed time. The razor-thin margins on hawker and mom-and-pop transactions, combined with card network fees, made this an unsustainable, loss-making venture from the start.

But ironically, it was the Liquid Account feature that ended up causing so much pain for Liquid Group.

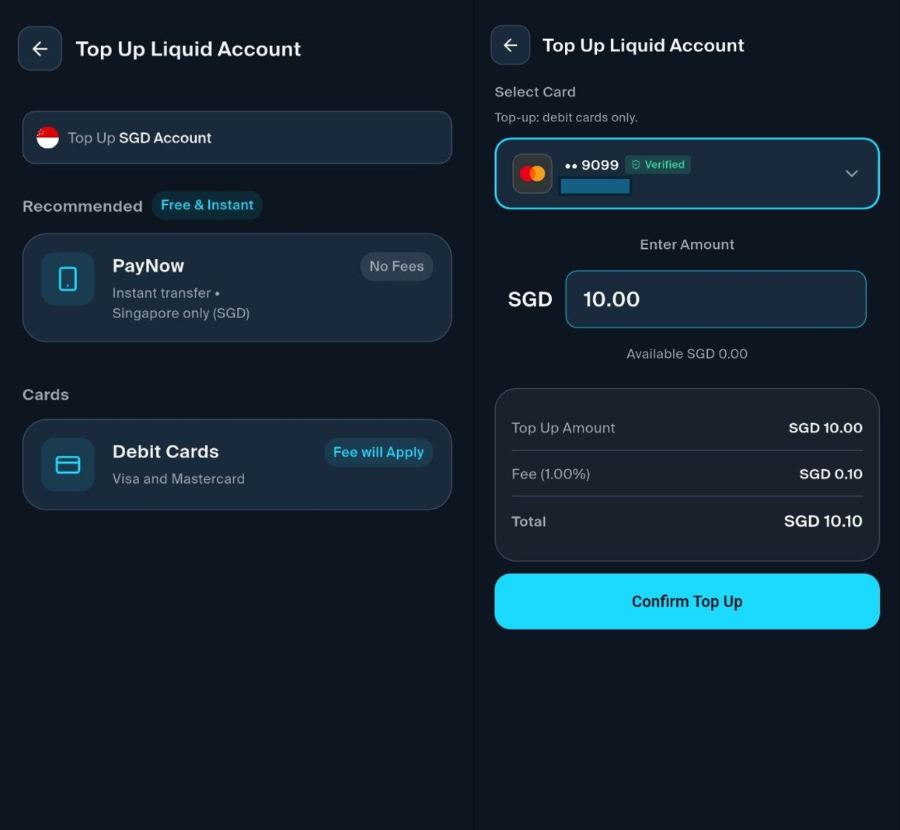

When I first played around with the app, I fully expected card payments and top-ups to code under different MCCs. To my surprise, LiquidPay used MCC 5399 for both. I mean, that’s just a staggering oversight. If GrabPay, SimplyGo and the various other sagas over the years have taught us anything, it’s that using non-6XXX MCCs for top-ups rarely ends well — for the company.

My guess is that Liquid Group assumed that because top-up methods were restricted to PayNow and debit cards — the latter carrying a 1% fee — the potential for abuse was limited.

How wrong they were.

One obvious workaround was the Amaze Card, which though technically a debit card, often serves as a pass-through for credit card spending. Users could:

- Pair it with the Citi Rewards or Maybank XL Rewards Card

- Earn 4 mpd on Liquid Account top-ups with a 2.01% fee (1% top-up fee from Liquid Group, and a further 1% domestic transaction fee from Amaze)

- Withdraw the funds via PayNow

That works out to a very reasonable 0.5 cents per mile — not free miles, but certainly a lot less than what you’d pay through other platforms like CardUp and Citi PayAll.

Alternatively, those with a Chocolate Visa Debit Card could:

- Earn 1 mpd on Liquid Account top-ups with a 1% fee

- Withdraw the funds via PayNow

1 Max Mile converts to 1 ALL Point (the rate will be devalued to 3:2 from July 2026), which in turn is worth 3 cents. Therefore, this was a “pay 1 cent get 3 cents” arbitrage opportunity. Even with the reduced earn rate of 0.4 Max Miles per S$1 after the first S$1,000, those who qualified for Chocolate’s Miles Multiplier feature could increase their earnings by up to 2x, keeping things sustainable beyond S$1,000.

Mind you, that’s just scratching the surface. I can imagine people using this to clock spend for high-yield savings accounts or sign-up bonuses, and long story short, it quickly became open season. The only real ceiling was the S$30,000 top-up limit per year, but even then, those who really wanted to could rope in family and friends for further churning.

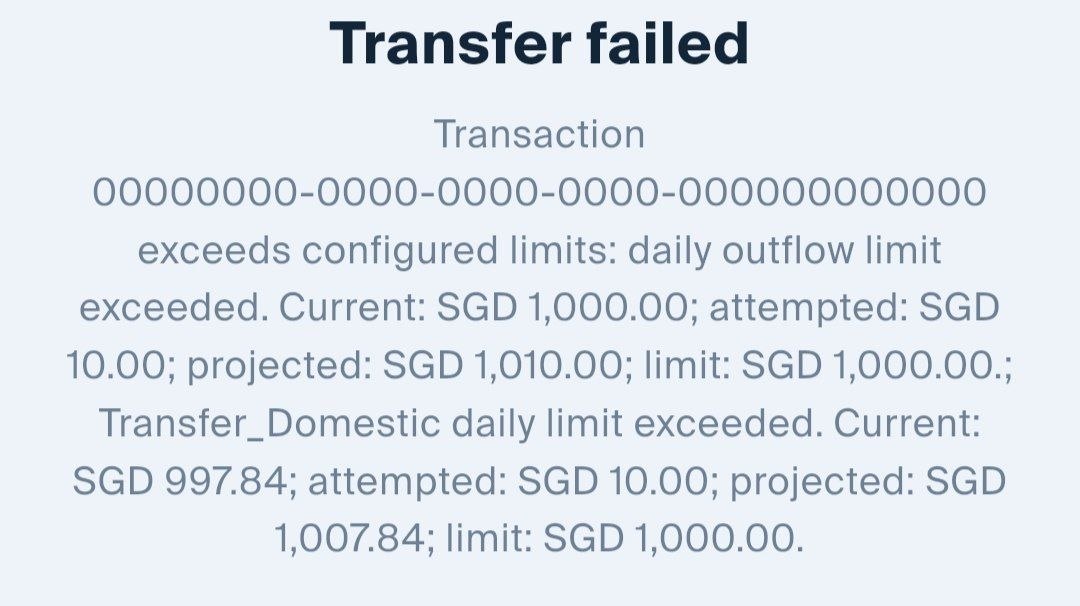

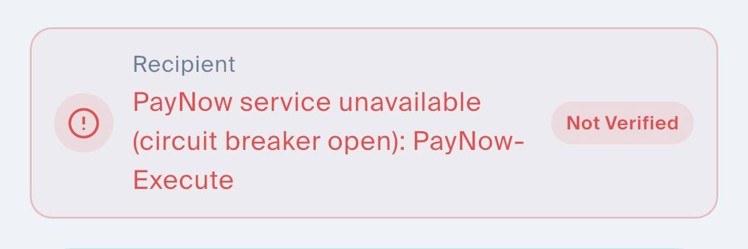

Therefore, it was only a matter of time before Liquid Group ran into liquidity issues.

You see, when you top-up a Liquid Account with a debit card, Liquid Group doesn’t receive the funds immediately. But when you cash out through PayNow, there’s an instant outflow from their coffers. As usage accelerated, reports started coming in of failed withdrawals due to a “circuit breaker” mechanism, presumably put in place to limit outflows in a “bank run” situation like this.

To stem the bleeding, Liquid Group made two changes:

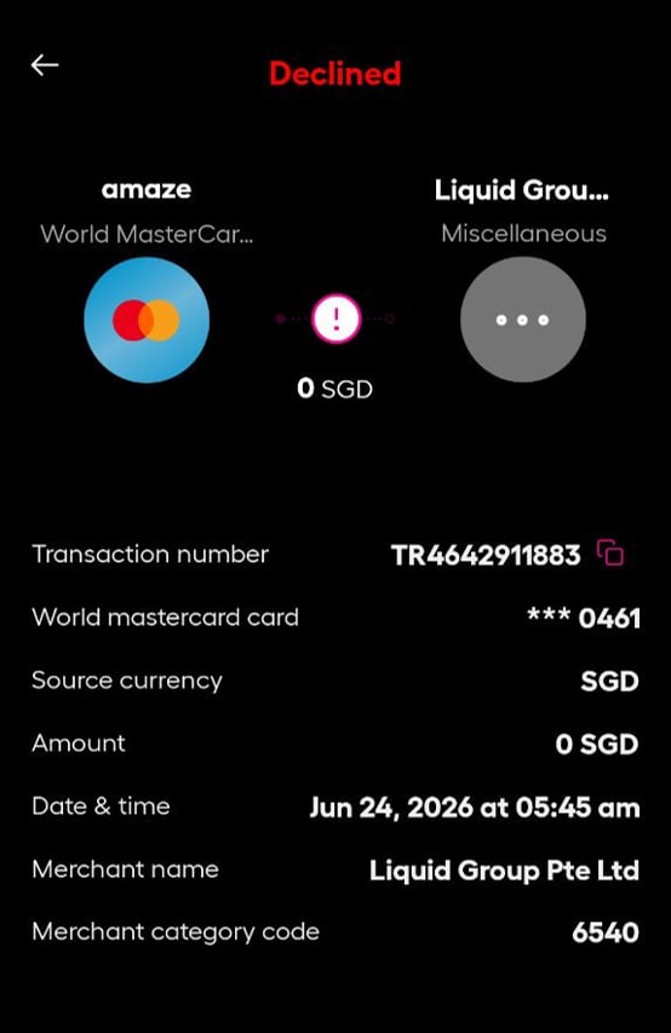

- It increased the fee for debit card top-ups to 3.5%

- It changed the MCC for top-ups to 6540 (though you have to wonder why they didn’t just do this in the first place!)

This effectively killed off the games that people were playing by increasing the cost, and removing the rewards. Come to think of it, the second change arguably makes the first unnecessary, but it might have been a stop-gap solution until they could get the MCC changed (unlike top-up fees, the MCC is not directly within the control of the merchant).

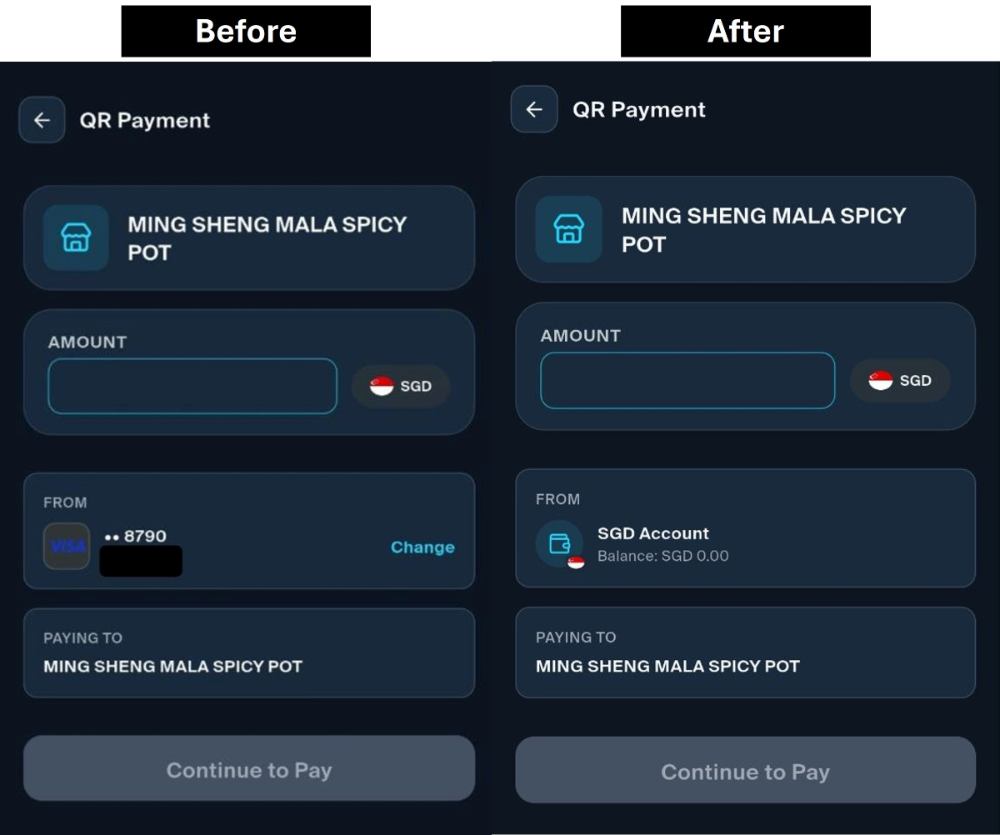

Oh, and one more thing. There was further collateral damage, because late last night, LiquidPay disabled credit card payments altogether. Regardless of merchant, the only payment option that users now have is their Liquid Account.

This basically turns LiquidPay into a glorified PayNow wrapper — why go through the trouble of topping up an account and then paying the merchant, instead of just paying the merchant directly?

Anyway, it looks like the dust has settled for now. As of this morning, LiquidPay’s website carries the following message:

|

Thank You for the Amazing Response!

We are grateful for the overwhelming support received since the launch of our introductory 1.0% debit card top-up promotion. As the promotional period comes to an end, debit card top-ups to your Liquid Account will be subject to a revised fee of 3.50%, effective 23 June 2026.

You may continue enjoying all LiquidPay services, including local payments, overseas QR payments, PayNow transfers and remittances.

Thank you for your continued support as we enhance the LiquidPay experience.

|

Amazing response indeed.

Conclusion

For those who are new to all this, congrats. You’ve just witnessed an entire manufactured spending saga compressed into 24 hours — greed and guilt, hype and hush, and the predictable online drama between those for and against sharing (which I don’t see much point getting drawn into, because we’re never going to come to an agreement on this).

Say what you will about the miles game, but it’s never boring…

Ok. time to uninstall the app and give it a one star lol

Hokay, app uninstalled, prolly the shortest duration for an app staying in phone

No wonder credit card options didn’t appear when I scanned the Qr code at hawker. Thanks for the update. You’re the best.

This company is hot trash

App turned useless in a day lol

And to add, the app look so much like a product of AI vibe coding

shutdown in 24 hrs.. so much more difficult to manufacture spend. i missed the old days of YT

The layout and also error messages are clear sign of a vibe-coded app and backend. Would definitely not trust with my information