It’s probably not an exaggeration to say that in the miles game, everything revolves around the Merchant Category Code (MCC), the four-digit code that reflects a merchant’s principal business.

MCCs play a key role in determining how much a merchant pays to accept card payments, otherwise known as the interchange rate.

Certain MCCs qualify for lower interchange rates. For example, charities, educational institutions, and government agencies typically enjoy discounted fees — which is also why most credit cards exclude rewards for such transactions.

Conversely, certain MCCs attract higher interchange rates because they’re deemed “high-risk”. These categories may see higher volumes of refunds, chargebacks, and fraud claims, like pawn shops, money transfer services, and precious stone dealers. Others carry reputational or regulatory risk, like firearms, gambling and pornography.

On that note, there’s an interesting development that’s been brought to my attention. From September 2026, Visa and Mastercard will remove their preferential interchange rates for MCC 5814 Fast Food.

While this has the potential to increase costs across the board, it might also be good news for those using the HSBC Revolution or OCBC 365 Card…

Visa and Mastercard removing preferential interchange for MCC 5814 Fast Food

It may feel like every fast food restaurant accepts credit cards today, but it wasn’t always like this. In fact, operators have long been resistant to the idea, worried that the fees involved would eat into their already thin margins.

To drive adoption, Visa introduced its Fast Food Industry Fee Programme, which offered preferential rates for quick service restaurants. This scored a major win when McDonald’s Singapore started accepting Visa cards in December 2014, followed by Food Republic in January 2016.

Fast forward to today, and the programme appears to have been a resounding success — I can’t think of a single fast food chain that doesn’t accept cards. In fact, it may even have worked a little too well, because MCC 5814 often pops up in unexpected places, from bakeries to upscale sit-down restaurants (more on this later), suggesting that merchants have started to game the system.

This may explain why Visa and Mastercard have decided to end this preferential treatment from September 2026, per an update from payments processing company Qashier.

|

From 1 September 2026, both Visa and Mastercard will remove the preferential interchange treatment that applies to fast food and Quick Service Restaurant (QSR) merchants under MCC 5814 in Singapore. Visa is removing its Fast Food Industry Fee Programme interchange rate, and Mastercard is removing MCC 5814 (Fast Food Restaurants) from its Emerging Markets acceptor business segment. From that date, the standard applicable interchange rates will apply to these merchants instead of the preferential treatment. -Qashier |

To be clear: this doesn’t mean MCC 5814 will be removed. It just means that merchants under this MCC will no longer enjoy discounted interchange rates in Singapore. It effectively removes the incentive for a merchant to negotiate for a 5814 classification over, say, 5812 (Restaurants).

For what it’s worth, I don’t expect that most of the affected restaurants will stop accepting cards, because customers have become so accustomed to paying this way (which was probably the plan all along!). In all likelihood, restaurants will try to pass on the additional costs in the form of higher prices, which in turn affects everyone, regardless of payment method.

Good news for the HSBC Revolution Card?

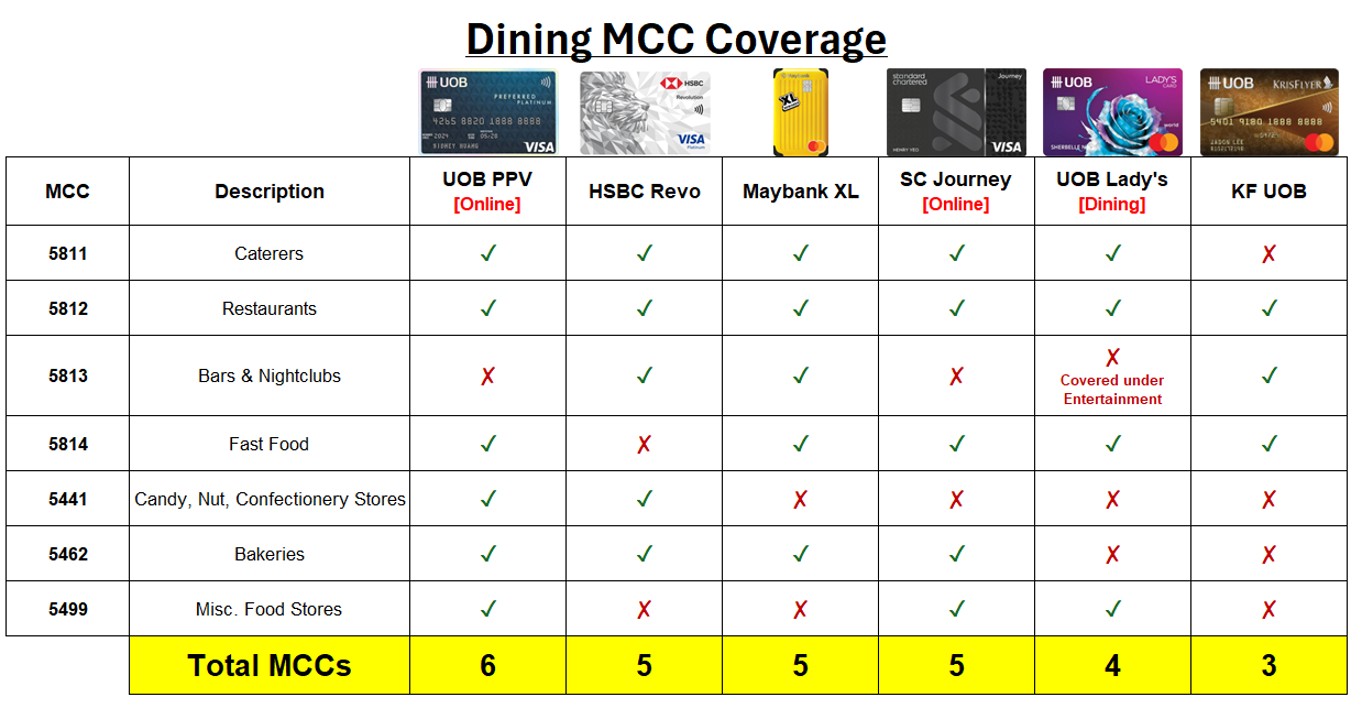

One of the biggest pain points for HSBC Revolution Cardholders is the “5814 gotcha”.

While the card prominently markets dining as a bonus category, HSBC actually excluded MCC 5814 from its whitelist back in May 2024, making it the only dining card on the market to do so (though you might recall that the DBS Vantage used to offer 4 mpd on dining when it first launched — except for 5814).

| ⚠️ Affects OCBC 365 Cardholders too |

|

If you’re a cashback user, it’s worth knowing that the OCBC 365 Card removed MCC 5814 from its dining bonus category in September 2023 (though it continues to explicitly whitelist Foodpanda and GrabFood). |

Some people call this a weird oversight, but I doubt it’s an oversight at all. If 5814 has lower interchange, then 5814 transactions are less profitable for the bank, and HSBC has made a deliberate decision not to bonus such spending.

This exclusion makes it a risky choice for dining, because the historically preferential rates for MCC 5814 have resulted in its widespread adoption, even at merchants that are far removed from what most people would consider fast food.

5814 has been reported at restaurants with table service such as Shin Katsu, PS Cafe, Beyond the Dough, Tipo Pasta, Cafe Nesuto, or bakeries like Noci Bakehouse, Paris Baguette and Polar (at least if you pay through Kris+). Moreover, Grab Dine Out, Grab Delivery and Foodpanda also code as MCC 5814, even if you’re ordering from a fine dining restaurant. The community is full of complaints from cardholders who learned the hard way that their meal only earned 0.4 mpd because it coded the “wrong” way!

Now that card networks are eliminating preferential rates for 5814, the incentive for restaurants to bend over backwards to be classified as fast food should also be removed. To be clear, I don’t expect every restaurant under 5814 to switch to 5812 overnight — many may never switch due to sheer inertia —but it would limit the number of newly-opened establishments pursuing a 5814 classification.

In time, hopefully these nasty surprises will get less common (or HSBC could just stop being weird about it and add 5814 to its whitelist, since it’s more profitable now).

Conclusion

From September 2026, Visa and Mastercard will remove their preferential interchange for MCC 5814 Fast Food. This will result in an increase in processing costs, and possibly higher prices for consumers, to the extent that merchants try to pass on the increases.

While this may seem like a mundane B2B decision, it could have implications for credit card rewards, and who knows — maybe 5814 might be restored to the whitelists of the HSBC Revolution and OCBC 365 Card.

I totally agree with this move. MCC5814 has been abused by many established restaurants. Frustrating because many my dining spending got excluded by HSBC revolution because the restaurant unexpectedly use MCC5814

you’ve enlightened why so many dining establishments code as -14! I’ve been wondering and thought it was just an issuer error

“HSBC has made a deliberate decision not to bonus such spending”: Grammar Nazi alert, Aaron!

5814 is also an issue with online QR table order portals that some non-fastfood restaurants use.

Further restaurants to add to the 5814 list: Temper and Nomada. Total scam.

wait, NOMADA? seriously? i just ate there a few weeks ago (didnt use revo, phew!). How on earth is that even close.