Today marks the start of a new era for American Express cardholders, with the Membership Rewards devaluation now in effect.

Transfer costs to all eight airline partners have increased by 22-25% (or 44-50% for Emirates Skywards), which not only reduces the value of your existing points, but also the value of future earnings, whether from regular spend or welcome bonuses denominated in Membership Rewards points.

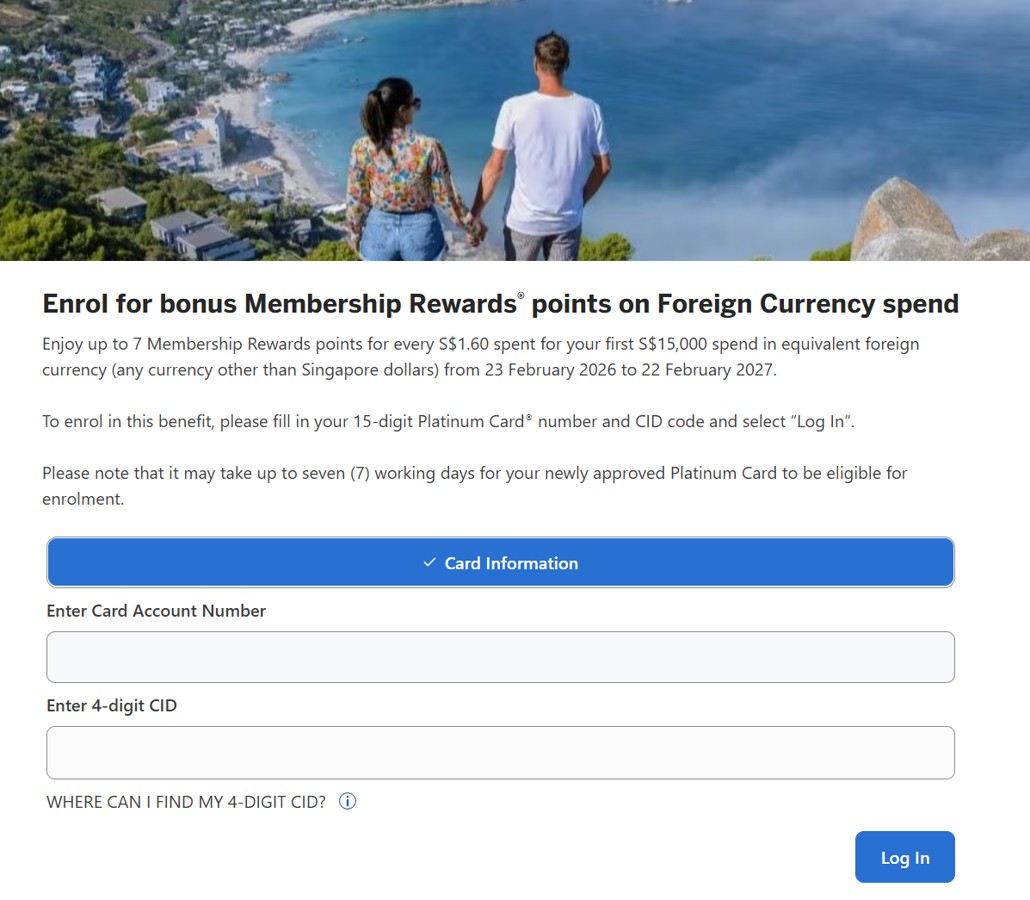

However, in an attempt to placate cardholders, the AMEX Platinum Charge has launched a foreign currency (FCY) spending promotion. This boosts the FCY earn rate from 0.69 mpd to 2.2 mpd, though only for a year, and capped at S$15,000 of spending (give chicken wing, take back etc. etc.).

The full details are now available, and frankly, nothing’s changed from my initial assessment. While there are some potential use cases for charitable donations, education and private hospitals, this is far from exciting, given that alternative cards offer up to 3.2 mpd on FCY spend— uncapped (did I mention they’re much cheaper too?).

AMEX Platinum Charge FCY spending promotion

AMEX Platinum Charge AMEX Platinum Charge |

||

| First S$15,000 | Beyond S$15,000 | |

| FCY Earn Rate | 2.19 mpd 7 MR points per S$1.60 |

0.63 mpd 2 MR points per S$1.60 |

| Note: Lower rates apply to Emirates Skywards | ||

From 23 February 2026 to 22 February 2027, AMEX Platinum Charge cardholders who spend on FCY transactions will earn 7 MR points per S$1.60 (2.2 mpd).

This comprises of:

- The base reward of 2 MR points, and

- A bonus reward of 5 MR points (awarded in blocks of 25 MR points per S$8 in FCY spend)

Do note the S$8 spending block required for the bonus reward. If you spend S$23, for example, you will be awarded bonus points based on S$16 of spending (and you thought UOB’s S$5 blocks were bad…)

The bonus reward is capped at a maximum of S$15,000 for the entire promotion period. Any spending beyond this threshold will earn the usual 2 MR points per S$1.60 (0.63 mpd).

Enrolment is required, and can be done on this page. If your AMEX Platinum Charge was recently approved, it may take up to seven working days before it’s eligible for enrolment.

Supplementary cardholder spending will be combined with the principal cardholder’s in awarding bonus points.

When will bonus points be credited?

What’s slightly odd about this promotion is that the T&Cs state the following:

The Membership Rewards points earned under this Benefit (including the Bonus Earn Rate) will be credited to your Membership Rewards Programme Account around twelve (12) weeks after the eligible transaction is made. No requests to expedite will be entertained.

This suggests that even the base reward of 2 MR points per S$1.60 will only be credited 12 weeks after the transaction is made.

I find this hard to believe. I think it’s much more likely that:

- the base points will be awarded when the transaction posts, with the bonus points credited within 12 weeks, or

- the base and bonus points will be awarded together with the transaction (AMEX is fond of using CYA language that stipulates much longer timelines than are actually necessary)

We’ll find out soon enough, I suppose.

What counts as qualifying spend?

All online and offline FCY spending will be eligible for this promotion, with the exception of American Express’ usual reward exclusions.

| ❌ Qualifying Spend Exclusions |

|

a) Charges processed and billed prior to the Enrolment Date or charges prepaid on any Card Account prior to the first billing statement for that Card Account following the Enrolment Date; |

It’s worth noting that charitable donations, education and private hospitals are still eligible to earn rewards with the AMEX Platinum Charge, so that is one potential use case for this promotion.

Charitable donations are now a universal exclusion among banks in Singapore, so if you’re giving to an overseas charity, then the AMEX Platinum Charge at 2.2 mpd would be the best option by far.

It’s also a good option for paying overseas tuition fees, though you can earn up to an uncapped 3.2 mpd with the Maybank World Mastercard or Maybank Visa Infinite for such transactions.

Terms & Conditions

The terms & conditions for the FCY spending promotion can be found here.

What can you do with Membership Rewards points?

Membership Rewards points can be transferred to eight airline and two hotel partners, at the ratios shown below.

| Programme | Conversion Ratio (AMEX: Partner) |

|

| Plat Charge Centurion |

Others | |

| 500 : 250 | 550 : 250 | |

| 500 : 250 | 550 : 250 | |

| 500 : 250 | 550 : 250 | |

| 600 : 250 | 650 : 250 | |

|

500 : 250 | 550 : 250 |

|

500 : 250 | 550 : 250 |

| 500 : 250 | 550 : 250 | |

|

500 : 250 | 550 : 250 |

| 1,000 : 1,000 | 1,000 : 1,000 | |

| 1,000 : 1,250 | 1,000 : 1,250 | |

As mentioned, the cost of transfers to airline miles has now increased, though transfers to hotel points remain unchanged.

Membership Rewards points can also be redeemed for statement credit under the Pay with Points and Pay with Points+ programmes. However, this represents relatively poor value compared to redemptions for airline miles.

| Implicit Value per Mile | ||

| Plat Charge Centurion |

Others | |

| Pay with Points 1,000 MR points = S$4.80 |

0.96¢ |

1.06¢ |

| Pay with Points+ 1,000 MR points = S$6 |

1.2¢ | 1.32¢ |

| For example, if you choose Pay with Points as an AMEX Platinum Charge cardholder, you are implicitly accepting a value of 0.96 cents per mile (based on the miles that could have been redeemed instead with those points). | ||

What other cards can you use for FCY spend?

An earn rate of 2.2 mpd may be impressive by the AMEX Platinum Charge’s standards — it’s 3.5x the usual, after all — but compared to the rest of the market, it’s actually very poor.

There are many, many other cards which outperform this comfortably, as the table below shows.

| Card FCY Fee |

FCY Earn | Cost Per Mile |

DCS Imperium Card DCS Imperium Card3.25% Apply |

4 mpd No cap Min. spend S$4K per c. month |

0.81¢ |

Maybank XL Rewards Card Maybank XL Rewards Card3.25% Apply |

4 mpd Max S$1K per c. month |

0.81¢ |

UOB Preferred Platinum Visa UOB Preferred Platinum Visa3.25% Apply |

4 mpd Max S$600 per c. month, must use contactless |

0.81¢ |

3.25% Apply |

4 mpd Online Max S$1K per s. month |

0.81¢ |

3.25% Apply |

4 mpd Online Max S$1K per c. month |

0.81¢ |

UOB Visa Signature UOB Visa Signature3.25% Apply |

4 mpd Min. S$1K, max S$1.2K per s. month |

0.81¢ |

StanChart Beyond Card StanChart Beyond Card3.5% Apply |

PP: 4 mpd PB: 3.5 mpd Regular: 3 mpd No cap |

PP: 0.88¢ PB: 1¢ Regular: 1.17¢ |

Maybank World Mastercard Maybank World Mastercard3.25% Apply |

3.2 mpd No cap Min. spend S$4K per c. month |

1.02¢ |

Maybank Visa Infinite Maybank Visa Infinite3.25% Apply |

3.2 mpd No cap Min. spend S$4K per c. month |

1.02¢ |

BOC Elite Miles Card BOC Elite Miles Card3% Apply |

2.8 mpd No cap |

1.07¢ |

Maybank Horizon Visa Signature Maybank Horizon Visa Signature3.25% Apply |

2.8 mpd No cap Min. spend S$800 per c. month |

1.16¢ |

StanChart Visa Infinite StanChart Visa Infinite3.5% Apply |

3 mpd No cap Min. spend S$2K per s. month, else 1 mpd |

1.17¢ |

HSBC Premier Mastercard HSBC Premier Mastercard3.25% Apply |

2.76 mpd No cap |

1.18¢ |

StanChart Rewards+ StanChart Rewards+3.5% Apply |

2.9 mpd Capped at S$2.2K per m. year |

1.21¢ |

DBS Treasures Black Elite DBS Treasures Black Elite3% |

2.4 mpd No cap |

1.25¢ |

HSBC TravelOne Card HSBC TravelOne Card3.25% Apply |

2.4 mpd No cap |

1.35¢ |

UOB PRVI Miles Card UOB PRVI Miles Card3.25% Apply |

3 mpd (IDR, MYR, THB, VND) 2.4 mpd No cap |

1.08¢ (IDR, MYR, THB, VND) 1.35¢ |

UOB Visa Infinite Metal Card UOB Visa Infinite Metal Card3.25% Apply |

2.4 mpd No cap |

1.35¢ |

DBS Altitude AMEX DBS Altitude AMEX3% Apply |

2.2 mpd No cap |

1.36¢ |

OCBC VOYAGE (Premier, PPC, BOS) OCBC VOYAGE (Premier, PPC, BOS)3.25% |

2.3 mpd No cap |

1.41¢ |

OCBC Premier Visa Infinite OCBC Premier Visa Infinite3.25% |

2.24 mpd No cap |

1.45¢ |

| AMEX Platinum Charge 3.25% Apply |

2.2 mpd Max S$15K for promo period |

1.48¢ |

3.25% Apply |

2.2 mpd No cap |

1.48¢ |

DBS Altitude Visa DBS Altitude Visa3.25% Apply |

2.2 mpd No cap |

1.48¢ |

OCBC VOYAGE OCBC VOYAGE3.25% Apply |

2.2 mpd No cap |

1.48¢ |

3.25% Apply |

2.2 mpd No cap |

1.48¢ |

Granted, Membership Rewards points are inherently more valuable thanks to their numerous transfer partners, smaller conversion blocks and free conversions (which are instant for KrisFlyer and Qantas Frequent Flyer), so if we’re comparing 2.2 mpd on the AMEX Platinum Charge to 2.2 mpd on the DBS Altitude Visa or Citi PremierMiles Card, the AMEX is the clear winner.

But how much of haircut are you willing to take for that? Compared to a 3.2 mpd card, you’re giving up 30% in quantity for the added “quality”. I guess it’s up to the individual, though if you primarily stick to KrisFlyer, you should definitely go with the higher-earning alternative cards.

Refer to the article below for more on the best cards for overseas spend.

Conclusion

The AMEX Platinum Charge has launched a year-long FCY spending promotion, which offers cardholders 3.5x the usual earn rate on all FCY transactions until 22 February 2027.

Sadly, this amounts to just 2.2 mpd, and with a S$15,000 spending cap, it falls well short of what the competition has to offer. You might be able to get some value out of this by making charitable donations or paying overseas school fees or hospital bills, but otherwise I’d prefer to stick to other cards.

What do you make of the AMEX FCY spending promotion?

Agreed with the analysis! I was all ready to sign up for the Amex plat charge until i saw their huge devaluation of MR points for miles trasfer.

Imo this card is very poor value and i’ll be sticking with other non-amex cards

Was about to sign up the Charge card again this month… after terminating it last year

Unfortunately, MR points devalued. Too bad….