The Milelion is running a new series that aims to profile every credit card available in Singapore. Each week we will cover a different bank. The appendix below will be updated weekly with hyperlinks as more banks are added, allowing you to navigate between weeks seamlessly

Week 1- OCBC

Week 2- DBS

Week 3- UOB

Week 4- Citibank

Week 5- ANZ

Week 6- American Express

Week 7- HSBC

Week 8- Standard Chartered

Week 7: HSBC

“Why did I even start the omnibus”, I wondered to myself last weekend. “It’s long and tedious and the information there gets outdated very quickly and when people read the wrong thing they assume I got it wrong which then undermines my street cred with the cool kids on FT/HWZ which then messes with my own self-esteem and I really should be using this time to work on my MBA applications/garage boyband and also I still haven’t applied for my Citibank Rewards Mastercard which will let me do certain things with my bill payments which I promised whoever it was who told me about it that I wouldn’t tell about it and also I want muskmelon.”

And with that, I opened my laptop and started typing.

HSBC Revolution Credit Card

- Annual Fee: $150 (Two year fee waiver)

- Income Req: $30,000 (Singaporeans & PRs), $40,000 (Foreigners)

- Marketing Spiel: 2 miles per$1 on dining, online and entertainment

- The catch: $1=0.4 miles on everything else. There are better cards for the dining and online categories

HSBC positions its Revolution Card as a lifestyle card that rewards you for online, dining and entertainment transactions. This is an offering that a lot of other banks have in some form, the whole idea is to reward so called “discretionary transactions”.

Where online is concerned, HSBC helpfully defines this as including airline/movie/concert tickets/hotel/travel/taxi bookings/food orders/insurance premiums and online shopping sites. I thought the inclusion of “insurance premiums” was particularly interesting given that such payments are usually excluded under the T&C of other cards when it comes to points earning (because they’re typically not discretionary)

That said, you could get 4 miles per $1 on online with the DBS Woman’s World Card and the HSBC Advance Visa. But both of these have special requirements- the DBS Woman’s World Card needs a minimum annual income of $80,000 and the HSBC Advance needs you to put an initial deposit of $30,000 or a standing instruction to deposit $2,500 a month until you hit a $30,000 balance. If neither is feasible for you, then you might consider this (or the regular DBS Woman’s Card which has a $30,000 income requirement) for your online spending.

2 miles per $1 on dining is similarly not best in class, surpassed by the UOB Preferred Platinum AMEX (not dead, not dead!) and the HSBC Advance card with 4 miles per $1. Also note that HSBC only awards bonus spend (for the Advance and Revolution) on local dining transactions, whereas the UOB PPA does it for both local and overseas. Given how much spread banks earn on overseas credit card transactions, it’s surprising they don’t want to incentivize this more.

If you’re already building miles with HSBC then I think this is a decent enough card to add to your collection, but otherwise there are better options

Yay or Nay: For the entry level income requirement, it’s competitive with other offerings, but I’d rather try and get a UOB PPA and start a HSBC Advance account for other online spending.

HSBC Visa Infinite Credit Card

- Annual Fee: $488

- Income Req: Not explicitly stated, rumoured to be S$250,000 a year but this may have since been lowered

- Marketing Spiel: Unlimited lounge access, 30,000 miles with joining fee of $488, an earning rate that scales with how much you spend

- The catch: General spending rates are generally superseded by the UOB PRVI Miles card, you need to spend at least $5,000 a quarter to get the unlimited limo transfers

I briefly touched on the HSBC Visa Infinite card in my primer on ultra-exclusive credit cards but I’ll go into a bit more detail here.

The HSBC Visa Infinite is an invitation-only card that offers the cardholder 30,000 miles with the joining fee of $488. That represents a price of 1.6 cents per mile, easily one of the better mile buying opportunities out there.

As for regular mile earning rates, the amount of miles you earn depends on how long you’ve held the card and how much you spend on it. I’m not unduly impressed by the earning structure though, because in a best case scenario where you’ve held the card for 2 years or more AND spent at least $75,000 in the previous year, you earn 1.5 and 2.5 miles per S$1 respectively for local and overseas spend. In contrast, you could earn 1.4 and 2.4 miles per S$1 of local and overseas spend from the get-go with the UOB PRVI Miles card, without any minimum spend. Plus, if you spent $50,000 you’d get 20,000 bonus miles, which increases your average miles per dollar slightly.

| Year of card membership | Local spend | Overseas spend |

|---|---|---|

| Year 1 | S$1 = 1 air mile | S$1 = 2 air miles |

| Year 2 onwards (with yearly spend of more than S$50,000 in the previous year) |

S$1 = 1.25 air miles | S$1 = 2.25 air miles |

| Year 2 onwards (with yearly spend of more than S$75,000 in the previous year) |

S$1 = 1.5 air miles | S$1 = 2.5 air miles |

But people who get such cards aren’t just doing it for the miles earning, obviously. They’re looking at the special perks that come with the card.

And those perks are none to shabby. Frequent flyers can look forward to

(1) Complimentary one way airport transfers with a minimum

My reading of the T&C tells me that cardholders who spend a min of $5,000 per quarter can enjoy unlimited home to airport transfers and expedited immigration clearance. If you don’t meet the required minimum spend within a quarter you’ll be billed at the following rates

| International Airport VIP Services | Charge per service booked (service fee) |

| Airport Limousine service | S$45 (inclusive of 1 Cardholder and up to 2 other guests travelling together) |

| Expedited Immigration Clearance – For international airports |

US$65 – US$385 per person depending on location |

Airport transfers are pretty straightforward but what’s expedited immigration clearance? HSBC works with various local third parties to arrange meet and greet services for the primary cardholder and accompanying guests. This service is only available at “major airports within Asia”, you can get the list from the HSBC folks if you’re really interested. I can imagine this would save a good amount of time in countries where immigration queues can be quite schizophrenic and which don’t have special APEC lines.

If you fall in the category of individuals who spent more than $50,000 per year in the previous year, you do not need to meet this quarterly spend for the current year and can enjoy unlimited airport transfers and expedited immigration clearance.

(2) Unlimited lounge access for the principal and supplementary cardholders with Priority Pass and S$35 fee for guests.

This is much better than other so called premium cards which only give a number of complimentary visits per year, but not as good as the Citibank Prestige card which has unlimited visits for the principal cardholder + 1 guest. See the full comparison of lounge access through credit cards here.

Elsewhere, the regular range of Visa Infinite 50% dining deals are available (see CIMB’s here for example). You can get 50% off when dining with 1 guest at the following restaurants in the Marriott Tang Plaza Hotel- Marriott Cafe, Crossroads Cafe, Pool Grill, Wan Hao Chinese restaurant.

So there’s plenty to like about the benefits of this card, but I keep bringing myself back to my central question/thesis/struggle- is this the best card for earning miles? No, it’s not. Does that make it a bad card? No, but if earning miles the fastest is your primary goal, there are better ways

Yay or Nay: Yes if you think you can really maximise the limo and other VI benefits, no if your sole purpose is to earn miles as fast as possible

HSBC Advance Visa Platinum Credit Card

.png)

- Annual Fee: Free

- Income Req: Must be a HSBC Advance account holder

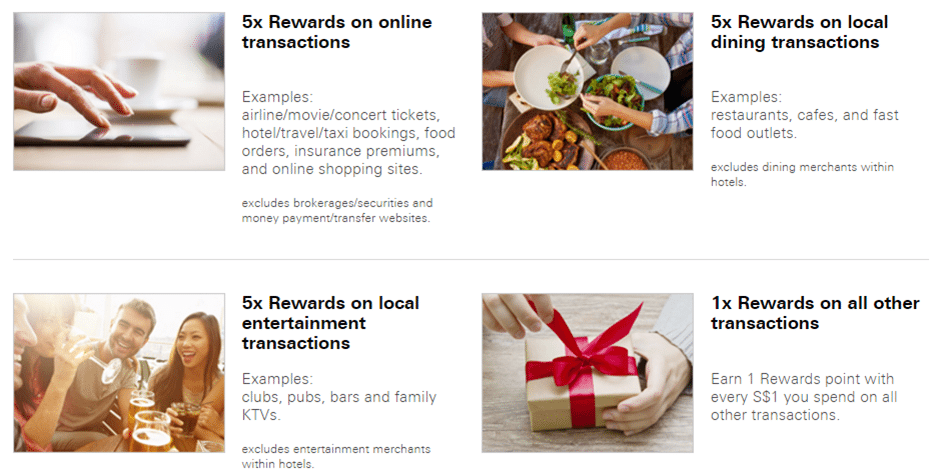

- Marketing Spiel: 10X points on local dining, local entertainment and online spending

- The catch: 10X points only till 31 Dec 16, not clear if program will be renewed after that

Ah, what to say about this card that has not already been said? My position on this card has slowly evolved- I think that if you’re in a position to get it you should. Over the course of a year, my spending on online and dining is likely to be high enough to offset the $40 fee involved of transferring miles over from another account.

I don’t actually have the card yet. I’ve applied and they’re taking their own sweet time sending it over (HSBC’s customer service is on the lackluster side). I’m also aware that the 10X points on online, dining and entertainment is a temporary promotion, valid only till 31 Dec 2016. It may be extended, or it may not.

Here are the choice bits from the T&C-

- Online Transactions means retail transactions made via the internet and processed by the respective merchants/acquirers as an online transaction type through the Visa Worldwide networks. For the avoidance of doubt, transactions made on brokerage/securities and/or money payment/transfer websites are not classified as retail transactions and are expressly excluded. For Online Transactions which involve EZ-Link or Transitlink, 10x Rewards points are capped at 2,000 HSBC Rewards points per Account per calendar month (i.e. S$200 spend).

- Dining Transactions means retail transactions made at merchants located in Singapore which have their main business activities classified as “dining”, excluding dining merchants located within local hotels.

- Entertainment Transactions means retail transactions made at merchants located in Singapore which have their main business activities classified as “entertainment”, excluding entertainment merchants located within local hotels.

The fact that its a Visa also changes the equation significantly, given how the Amex traditionally has lower acceptance. I’ve said before that Amex has to give better rewards precisely for that reason- which is why the UOB PPA is/was one of the best dining cards out there. This does make me wonder how sustainable the 10X rewards program is though- UOB already realised that 10X on the PPA wasn’t sustainable, how much less so for a Visa card?

When I think about the thousands I must have been putting on online spending over the past couple of years, only to be capped at $2,000 per month on my DBS WWC, I feel slightly annoyed. But I suppose it’s better late than never.

Yay or Nay: Definitely get this card if you’re able to start a HSBC Advance account and pray they renew the 10X rewards after the end of this year.

HSBC Premier Mastercard Credit Card

- Annual Fee: Free

- Income Req: Must have a HSBC Premier relationship

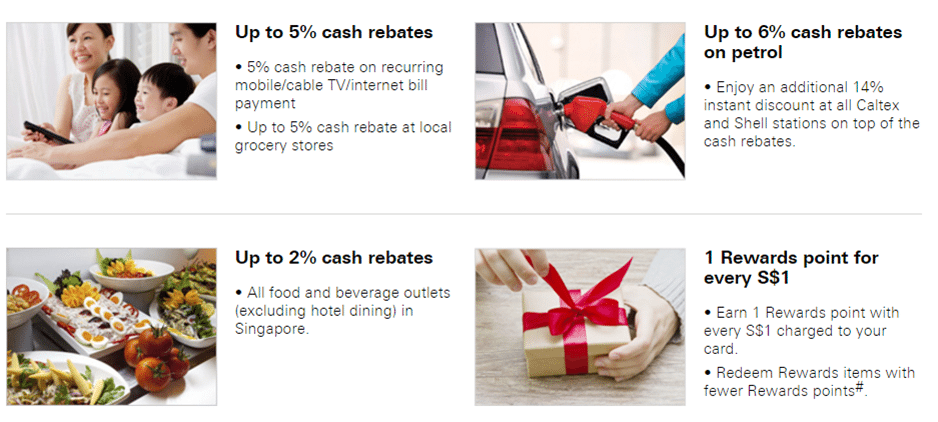

- Marketing Spiel: Rebates for recurring bill payments, petrol and dining, points for everything else

- The catch: General earning rate is $1=0.4 miles. It’s a very bad rebates card and an even worse points card

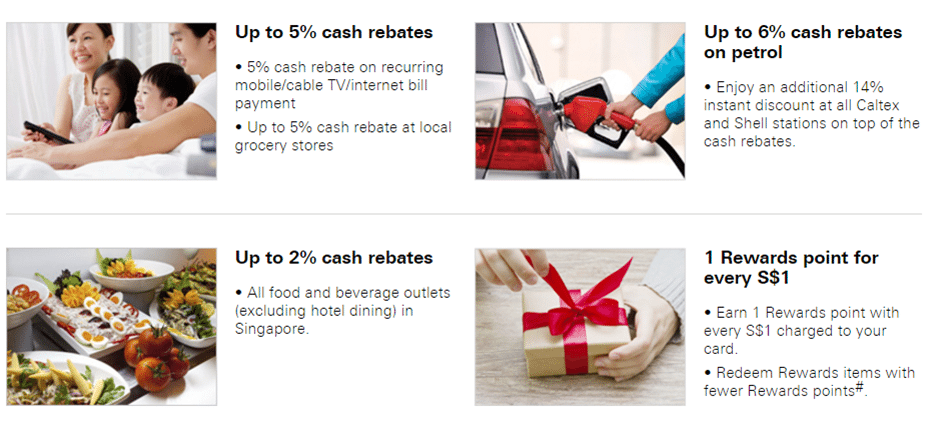

The HSBC Premier card is offered to HSBC’s premier banking customers (i.e those who have a min $200,000 total relationship balance with the bank).

It’s a bit of a strange card in that it offers cash rebates on some categories, miles on others. To enjoy any cashback at all, you need to spend at least S$400 a month for 3 months in a quarter. The higher cashback rate is enjoyed with a minimum S$800 a month for 3 months in a quarter. Or to summarize-

| Spend tier | Min. S$400 spend/month for all 3 months in a calendar quarter | Min. S$800 spend/month for all 3 months in a calendar quarter |

|---|---|---|

|

Recurring Mobile / CableTV / Internet Bill Payment^

|

5% cash rebate | 5% cash rebate |

|

Groceries

|

3% cash rebate | 5% cash rebate |

|

Petrol (Caltex & Shell)

|

14% instant discount + 3% cash rebate |

14% instant discount + 6% cash rebate (Shell) |

| 14% instant discount + 5% cash rebate (Caltex) |

||

|

Dining

|

1% cash rebate | 2% cash rebate |

|

Max Rebate per Quarter

|

S$60 | S$120 |

The cash rebates are nothing to shout about- you would be able to get rates just as good if not better with other dedicated cashback cards which don’t have a minimum spend requirement. And a $60 per quarter cap means whatever upside to you is limited.

Other spending that doesn’t fall into these categories earns the equivalent of 0.4 miles per S$1. I’m really struggling to see what the benefits of this card are. It is a World Mastercard, and therefore you can enjoy some of the special benefits accruing to World Mastercard holders (eg SPG Gold status with a single stay), but there’s no reason you can’t get a World Mastercard elsewhere (eg the Citibank Rewards card).

So if this card is meant to reward loyal premier banking HSBC customers I’m at a loss to understand how.

Yay or Nay: Nay. If you’re a HSBC Premier customer you should be nudging them to offer you the HSBC VI

HSBC Visa Platinum Credit Card

- Annual Fee: S$192.60 (2 year fee waiver)

- Income Req: S$30,000 (Singaporeans/PRs), S$40,000 (Foreigners)

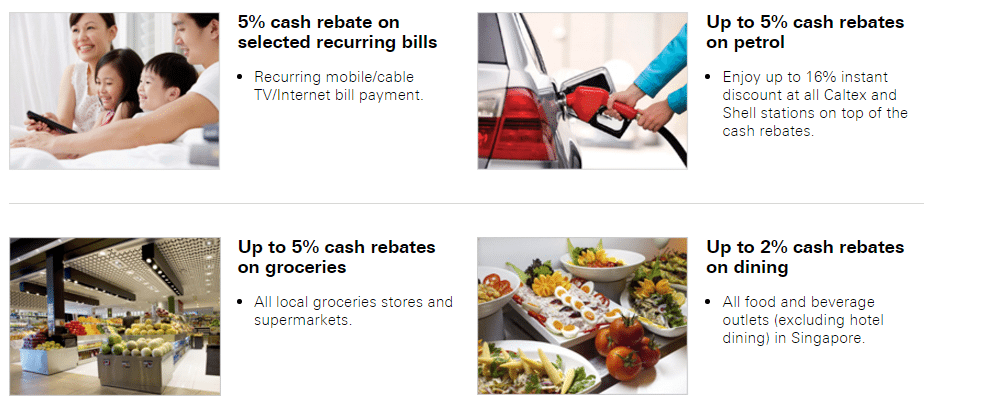

- Marketing Spiel: 5% rebate on recurring mobile/TV/internet bills, 5% rebate on groceries, 5% rebate on petrol, 2% rebate on dining

- The catch: Highest tier of cashback requires min S$800 spending per month for 3 months, everything else earns 0.4 miles per S$1

Woah. Dejavu? The benefits of this card look almost the same as those of the HSBC Premier.

Closer inspection reveals that there are some differences, however slight. The HSBC Premier Mastercard gets a 14% instant discount on petrol vs 16% for the HSBC Visa Platinum. Which is weird because I’d have thought all HSBC cards enjoy the same tier of discounts.

| Spend tier | Min. S$400 spend/month for all 3 months in a calendar quarter | Min. S$800 spend/month for all 3 months in a calendar quarter |

|---|---|---|

| Recurring Mobile/Cable TV/Internet Bill Payment | 5% rebate | 5% rebate |

| Groceries | 3% rebate | 5% rebate |

| Petrol (Caltex and Shell) | up to 16% instant discount + 3% rebate |

up to 16% instant discount + 5% rebate |

| Dining | 1% rebate | 2% rebate |

And if you look at the graphics on both pages you can see some differences. Go on, spot them!

I am Jack’s complete lack of enthusiasm.

Yay or Nay: If the HSBC Premier card was bad, this isn’t much better. At least you don’t have to park S$200,000 with the bank to get it though.

One more instalment to go and the Omnibus is complete!

thanks for your sharing! really appreciate it. am gonna get the hsbc advance card now.

i have been using anz optimum to get 5% cashback on my hotel expenses & the stanchart singpost to get 7% cashback on line airfare bookings but since i do use miles for biz class redemption, makes more sense i consolidate everything onto the hsbc advance.

for spending not covered by hsbc advance e.g. overseas dining, hotel expenses offline etc… which card would you suggest?

Thank you for your thoughts 🙂

Thanks for sharing this information!

Does insurance premiums qualify for miles on HSBC Advance?

i just got my hsbc advance card so i can’t say. other people have reported success but don’t quote me on that.

Aaron, do you have contacts for Advance management? And not just RM, but higher?

I opened Advance account in begining of April and signed for Advance Visa card. It has been 5 month already, no word about the card, RM does not answer emails.

nope, I’m not that well connected (yet!). I waited about a month for my card.

Just had a letter from HSBC, the Visa Infinite package is being “enhanced” from 1 Jan 2017 – basically mile earn rate has been reduced, annual fee going up (for non Premier customers) and capping the number of free airport rides. Not sure its worth the fee now…

oh yeah i just read about that on HWZ. HSBC is going to have a lot of angry customers soon…

Hi Aaron, the bonus points for HSBC, for local dining/entertainment/online spend, may take up to 2 months to be posted, and it is always lumped together in the monthly statement. Do you actually call them up every month to verify which transactions are those bonus points for?

i did for one month then got lazy. since i know i only use that card for online + dining, i look at my bill and times 4 to eyeball the numbers and see if they’re in order.

Advance card 10x points extended to 31 Mar 17:

https://www.hsbc.com.sg/1/PA_ES_Content_Mgmt/content/singapore/personal/cards/09/hsbc-advance-visa-platinum/tnc.html#B

you beautiful, beautiful man. best news i’ve got all week. will write something on this shortly.

And your article on this was the best thing I read this week! Thanks both, for making my day!

Can the rewards points be consolidated across all HSBC cards for redemption?

Called CSO, revolution visa and advance visa all different pool

hi aaron,

fantastic work on the omnibus! this is THE definitive guide for credit cards in Singapore. makes research so much easier than the noise on HQZ.

carry on the omnibus with Stanchart please!

Actually, putting aside the debate on rebate vs miles card. I feel that the premier card is a good rebate card, it seems like the only one that 1) Gives you 5% on all groceries 2) Gives you 5% on all Phone bills 3) gives you 0.4miles over and above that. ( if 1 mile is worth 4 cents, 0.4 miles = 1.6 cents, which means is another 1.6% back) 4) 0.5% fee for taxes to get 0.4 miles. I think its a good card that compliments the miles and it helps the cashflow. (Nice to see a rebate to… Read more »

Just received a letter from HSBC. The 10x points for the Advance card will not be renewed beyond 31.5.17. From 1 June 2017 it will become a cash back card.