Effective today, Standard Chartered has cut the X Card’s 100,000 miles sign up bonus to 60,000 miles. To those who applied on or before 11.59 p.m on 31 July, relax- so long as your approval comes by 31 August, you’ll be eligible for 100,000 miles. For everyone else, 60,000 miles is the new reality.

We’ll talk more about the new offer in a moment, but let me begin by saying that the X Card launch appears to be a classic case in expectations mismanagement.

SCB certainly grabbed the headlines with the 100,000 miles sign up bonus, but the way in which they abruptly canned the offer just five days after launch (and a full month before it was originally set to expire) came off as panicky and disorganized, and attracted its fair share of ridicule from the public. More than that- after initially showing the market 100,000 miles, the revised 60,000 miles offer, generous though it may be, was always going to be viewed unfavorably.

What could have been done differently?

Well, I know that a 100,000 miles offer will be extremely attractive, and extremely expensive to fulfill. I (rightly) don’t want to do a UOB-style promotion that caps the bonus to “the first X customers who spend $Y”, yet I need to limit my maximum exposure.

So when the X Card launches, I’d openly advertise that the regular sign up bonus is 60,000 miles- but for the next 5 (or whatever) days, anyone who applies will be eligible for a 100,000 miles offer. That would create a sense of urgency, plus prewire the market to know that 60,000 miles is the business-as-usual offer, so it won’t come as a shock when the bonus reverts to that level.

If sign ups during the promo period go beyond my wildest expectations, then I grin and bear it, knowing that I’ve at least capped my damages to five days. If sign ups fall below, then I can play the good guy by saying “we’ve eXtended the 100,000 miles offer for a further (insert number) days, act now!” (yes, even in my hypothetical scenarios I think about marketing fluff)

This approach would help the bank hedge its bets, not to mention save face. By positioning 60,000 miles as the default offer and 100,000 miles as an upsized deal, no one can say you didn’t warn them. As it is, I can imagine there must be quite a few people who read about the X Card’s initial launch, saw that the 100,000 miles offer was valid till 31 August, and went away thinking they’d apply later. Assuming they don’t follow the news (and most people don’t track this kind of thing daily), they’re in for a rude shock, because it’s not like SCB sent a mass email alerting its customers to the early demise of the offer.

By setting an initial 31 August 2019 deadline, SCB created the expectation in the minds of the consumer (reasonable or not) that the offer would go on for a full 37 days. Of course it’s within the rights of the bank to pull the offer early- no one is disputing that. It just generates an unnecessary amount of ill will. Why play the bad guy by pulling a good offer early, when you can play the hero by extending it?

I’m going to caveat the above by saying I’m not privy to the inner workings of the launch. For all I know, that option was considered but abandoned for legal or other perfectly valid reason. All I’m saying is that optics aren’t good: SCB got everyone excited about 100,000 miles, then yanked the carpet abruptly.

Final point: I’ve seen some people comparing this X card launch to the Huawei $54 phone, and I think that’s the wrong comparison to make. There’s a subtle but important difference: with Huawei, the promotion was limited quantity. With SCB, the promotion was limited time. No matter how you feel about the limited time getting even more limited, if you sent in your application on or before 31 July, you’d still get your 100,000 miles. That is a crucial distinction to make, and we should recognise and commend banks for not resorting to UOB-style sign up promotions.

So, with all that said, what if you missed the boat?

How does the new sign up offer work?

The new X Card offer applies to anyone who submits an application from 1 August 2019 onwards. If your card is approved by 30 September 2019, and you spend S$6,000 in the first 60 days after approval and pay the S$695.50 annual fee, you’ll receive:

- 30,000 miles in the form of 75,000 360° Rewards Points within 30 days after card activation

- 30,000 miles in the form of 75,000 360° Rewards Points by 30 November 2019

Once the base miles are included, you’ll have a total of 67,200 miles, broken down as follows.

| Old Offer (ends 31 July) | New Offer (ends 30 Sept) | |

| Miles from $695.50 Annual Fee | 30,000 | 30,000 |

| Spend $6K within first 60 days | 70,000 | 30,000 |

| Base miles earned on $6K spend @ 1.2 mpd | 7,200 | 7,200 |

| Total Miles | 107,200 | 67,200 |

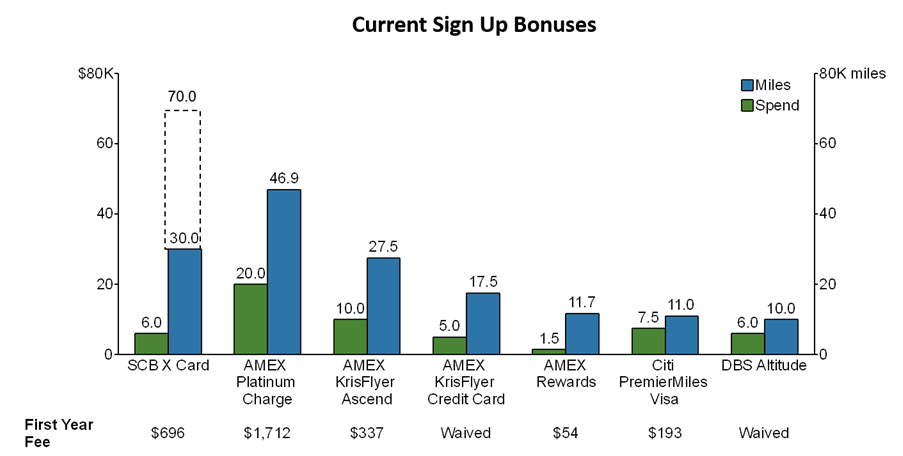

In the cold light of day, it’s still a good offer compared to what the rest of the market has. 100K was a phenomenal offer; but 60K is a good one.

Paying S$695.50 for the right to earn 60,000 miles is equivalent to paying 1.16 cents per mile (I don’t count the S$6,000 spending, because that should be spending you would needed to have done anyway).

You’ll of course want to adjust this for opportunity cost, given that you’re committing to spend S$6,000 at the X Card’s middling 1.2 mpd rate. The opportunity cost really depends on what you were planning to spend the S$6,000 on, and what your alternative card would have been:

| General Spending | Specialized Spending (e.g shopping, online) | |

| Alternative Choice | BOC Elite Miles World Mastercard (1.5 mpd) | Citi Rewards Visa/ Citi Rewards Mastercard/ UOB Lady’s Card/ DBS Woman’s World Card |

| Miles earned from spending $6K on alternative card | 9,000 | 24,000 |

| Miles earned from spending $6K on SCB X Card | 7,200 | 7,200 |

| Difference | 1,800 | 16,800 |

| X Card Adjusted Sign Up Bonus | 58,200 | 43,200 |

| Cost Per Mile, given S$695.50 fee | 1.2 cents | 1.6 cents |

It’s still good, but obviously not as good as before.

Put it another way: if you met a miles chaser who had no idea what happened over the past week and showed him the 60,000 miles offer, he would probably go for it. I realise it’s quite different for someone who knows they just took a 40% haircut, however.

I’m sure there must be some psychological study that deals with whether people will take a good offer, knowing a better one just slipped away, but I can’t recall it now (help me if you know).

New exclusion category: education

SCB has published a new set of T&Cs for the X Card. If you’re interested in the old T&Cs, you can find them here.

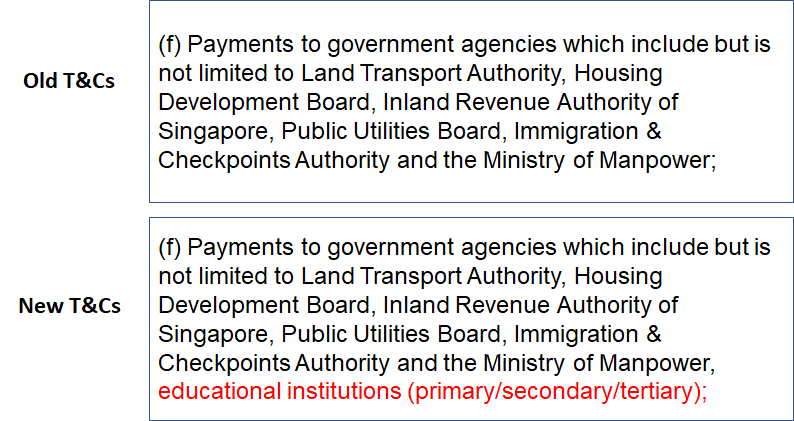

I ran the T&Cs through a comparison checker, and apart from the change to the sign up bonus, most of the fixes were typos. There is an important change to the exclusion categories that will not count towards the S$6,000 spending, however:

In the new T&Cs, education institution payments are now excluded. Based on how the sentence is structured, I’m assuming this refers to educational institutions which are affiliated with the government, not all education institutions in general (because it’d make more sense to put that as a separate bullet point).

If you’ve already made a big payment to an education institution, you really should get on the phone and clarify with customer service what this means for you. Private institutions should be fine, but I’d be a bit worried if I made a payment to a government-affiliated one. Remember to get whatever response they provide in writing, because you don’t want to be riding on a single big tuition fee payment to get your 100,000 miles only to end up disappointed later.

It’s noteworthy that the “education institutions” exclusion only appears in point 57 of the T&Cs where it’s addressing what doesn’t count towards the S$6,000 spending. It does not appear in point 26 where it’s addressing what doesn’t earn points, full stop. So my guess is that education payment fall in the same category as CardUp/ ipaymy/ RentHero- they earn base miles, but they won’t count towards the sign up bonus.

Conclusion

Despite four applications and a last minute appeal to my RM, I didn’t get the X Card. It’s certainly not an income requirement thing, and I’ve got a credit score of AA, so I’ll attribute this to Russian interference cosmic randomness.

| Edit: My RM contacted me on 2 August and told me he managed to get the card approved, plus the 100,000 miles sign up bonus. It seems like they do have some flexibility for Priority Banking customers, so if you’re one and got rejected on or before 31 July, it’s worth seeing what he/she can do |

To those of you who got in on the 100,000 miles offer, congratulations! We’re not going to see something like this again for a long, long time, and I hope you’re well on your way to hitting the S$6,000 spending requirement. Check out this article if you need some ideas on where to transfer your sign up bonus.

This is gimmicks.make lots of pre launch attention but subsequently reduce benefit.

thanks captain obvious

Hi Aaron, for the sign up qualifying transactions, what does it mean of this clause? The following transactions charged to a principal X Card or supplementary X card will not be considered as a X Card Sign Up Gift Qualifying Transaction for the purposes of the X Card Sign Up Gift Promotion: (b) Bill payments (Examples of bill payment merchants include but are not limited to Telecommunications and utilities providers such as Starhub, Singtel and M1, Singapore Power); include but not limited to Telecommunications and utilities providers, is that mean i can pay my starhub and M1 bill and it… Read more »

No it means that any form of bill payment to telco and utilities provider aren’t included for the $6,000 spend.

How much does it actually cost SCB? How much do banks buy miles for? I can’t imagine they pay more than 1c per mile – in fact I’d expect it to be a lot less. In Australia there are ongoing campaigns to earn 100,000 miles on credit card sign ups with $6000 spend and similar annual fees. In the USA the sign up bonuses are even more attractive. The credit cards in these other countries transfer to many of the same airlines available from SCB so I expect the cost to the banks per mile from these FF programs to… Read more »

Great sense of humour, Aaron. May also be worth sharing that those (and I assume you as well) who received the A05 error message during their application are actually unsuccessful / rejected applicants, as it is not abundantly clear unless you follow up with SCB for an explanation as to what it means (which I did). Another PR / comms failure on their part, might I add.

Hi Aaron, I understand your frustrations in missing out on the promotion. I met the annual income requirement based on last 6 months of CPF contribution and have a AA score (1,972) on my credit scoring, and have been a SCB cardholder for more than 10 years but was rejected for 3 times as well. It’s even tougher to justify your rejection since you are a priority banking client….

Can we form a “X-card rejects” club, and lodge a complaint with MAS or CASE on this? SCB rejects our card application with no clear reason, even though we qualify to the dot…

Anyone?

It’s a private bank. They can choose to do business with anyone they want. Apparently that did not include you and many others.

I’d just move on and not waste my time here.

Would you form a “employee rejects” club for people who have not been offered a job after interview, and say that the employer rejected their applications with no clear reason even though the applicants are totally qualified?

There’s your answer.

Like what Dave said, it’s all their discretion on acceptance of business… sadly, nothing much we can do, but I do believe that they prefers new to SCB clients than existing clients in this campaign.

Will be canceling my current SCB card soon after this treatment…

I tried to apply last night about 10pm. It kept giving me a “transaction error, please try again” message, which persist till about 1150pm, by then they had already changed the wording to reflect the lower miles.

So it seems they pulled the plug way before midnight. Either that or the server simply died under the increased load. Again, poor management from scb.

How about private hospital / clinic payment?

Is it excluded?

You are a saviour!! I made a tuition fee payment on the X card a couple of days back. I just read about the new exclusion for tuition fee payments here and immediately called up the bank to check if my transaction can be counted as a qualifying transaction since i made the payment before the new T&C were uploaded. The CSO was still referring to the old terms and had no clue that the T&Cs have been updated and I had to ask her to open the updated terms on the bank’s website. I’ve been told to expect a… Read more »

My experience with CSOs is that they don’t always know what they are saying. Yesterday I asked a UOB CSO a question about the 12 free rides UOB promotion for simply go, and I ended up explaining to her $40 is the minimum spend in a calendar month, $15 is the rebate cap and 25% is the rate at which they calculate the rebate. She gave me a hesitant answer about “winners” will be notified at the end of the promotion (seems like not everyone who signs up will get the reward, true to UOB style). It’s better to get… Read more »

Wouldn’t education instruction have the same MCC whether government or private?

“…someone who knows they just took a 40% haircut, however.” I’m that someone and despite 60k miles still being a good deal, I’m Not going to take the bait.

Feeling salty and it leaves a bitter aftertaste about SCB.

There are certainly more similarities than differences between the two campaigns. Both left people with less favorable impression of the brand. When you run such campaigns, you want people to be talking about the brand in a more positive manner. This is a miles card. You want to capture more (and not less) of the miles community. You want them to use your card over other miles card. With a separate T&C (with further enhanced exclusions) for this x card, i will use sc cards for even LESS spending categories, that in order not to confuse myself on the huge… Read more »

Agree wholeheartedly. SCB is now known as the brand that didn’t think through its X-Card launch and can’t deal with it so had to roll back just after just 5 days. Huawei is now known as unable to honor cheap phone promo. UOB is known for its intransparent promos that people don’t now bother. BOC is the card with slow and archaic service on just about everything!

I managed to get my X card approved (can be seen on internet banking account) on the 1st August, despite applying on the late evening on 31 July 2019. Alas, the physical card is nowhere in sight. I called CSO who said they ran out of cards. Anyone got better luck??

And I am still waiting for it to charge my EVA tickets from SIN-SEA. I pray the tickets and upgrade awards don’t get filled up by the time the card comes.

Haven’t got mines either. Checked with a few people who I know that applied, no luck in getting the card either.

Oh, I am losing my patience. Called CSO who told me that my card has been sent to Singpost since Monday. Singapore can’t be that big right? Anyway, no card yet. If I don’t get it by tmrw, I will go ahead and book my air tickets. Upset +++. In fact, my experience with BOC was much better. Seems like I have to buy $6000 worth of NTUC vouchers then… grrrrr

Mine’s arrived today, no fancy box, just a plain envelope. There is a letter inside explaining they ran out of boxes due to the demand for the card.

Do you know if TOP up to YouTrip is eligible spend as part of the $6,000?