Here’s The MileLion’s review of the UOB Reserve Card, the bank’s flagship product, and available by invitation only to the wellest of the well-heeled.

While the card might never extinguish the memory of its infamous marketing typo, it has firmly established itself as one of Singapore’s most exclusive credit cards — one whose mere ownership already speaks volumes.

But while it’s lonely at the top, it’s certainly not solitary. And given the other elite cards that customers in this segment could easily obtain, does the UOB Reserve offer enough to be the card of choice?

|

|

| UOB Reserve Card | |

| 🦁 MileLion Verdict* | |

| The UOB Reserve Card feels somewhat underpowered for the elite segment it occupies, though it’s likely that the average cardholder won’t even notice it. |

|

| 👍 The good | 👎 The bad |

|

|

| *I won’t be assigning my usual Take It/Take It or Leave It/Leave It ratings to cards in the $500K segment, because the service experience, which is a huge factor in a segment like this, is unknown to me as a non-cardholder |

|

| 💳 Full List of Credit Card Reviews | |

Overview: UOB Reserve Card

| UOB Reserve Card |

|||

| Apply | |||

| Income Req. | S$500,000 p.a. | Points Validity | 2 years |

| Annual Fee | S$3,924 |

Min. Transfer |

5,000 UNI$ (10,000 miles) |

| Miles with Annual Fee |

100,000 | Transfer Partners |

3 |

| FCY Fee | 3.25% | Transfer Fee | Waived |

| Local Earn | 1.6 mpd | Points Pool? | Yes |

| FCY Earn | 2.4 mpd | Lounge Access? | Yes |

| Special Earn | 2 mpd on local luxury spend | Airport Limo? | Yes |

| Cardholder Terms and Conditions | |||

The UOB Reserve Card is made from Alpaca Silver which, contrary to popular belief, is not derived from smelting down alpacas. Instead, it’s an alloy of copper, nickel and zinc, and one of the priciest materials used in the manufacture of metal credit cards.

At 28 grams, it’s actually the heaviest credit card in all of Singapore (and makes the 14-gram AMEX Centurion look like a featherweight). Its bulk means that it may even have difficulty fitting into some of the more svelte card readers, and its pure metal construction also means it does not support contactless payments. Therefore, UOB also issues a plastic version, so you basically get two cards, each with their own card numbers and CVVs.

It’s also worth noting that there’s actually two kinds of Reserve Cards out there: the vanilla UOB Reserve, and the diamond-embellished UOB Reserve Diamond Card (because why wouldn’t you want a diamond on your credit card?).

The UOB Reserve Diamond Card has all the benefits of the UOB Reserve Card plus some extra perks, which I’ll touch on later in this review.

How much must I earn to qualify for a UOB Reserve Card?

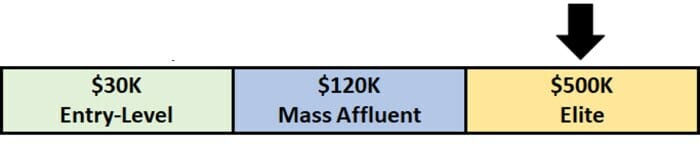

The UOB Reserve Card is strictly by invitation only. Applicants must earn at least S$500,000 p.a., though there may be some flexibility if you have a UOB Privilege Reserve (min. S$2M AUM) or UOB Private Banking (min S$5M AUM) relationship.

This puts it in direct competition with other elite credit cards such as the AMEX Centurion, Citi ULTIMA, DBS Insignia and HSBC Prive, commonly referred to as the “S$500K segment”.

The title is a bit of a misnomer, given that a S$500,000 income alone might not be sufficient for membership (particularly in the case of the AMEX Centurion Card). That said, it’s a useful shorthand for the kind of rarefied air we’re dealing with.

How much is the UOB Reserve Card’s annual fee?

| Principal Card | Supp. Card | |

| First Year | S$3,924 |

|

| Subsequent |

The UOB Reserve Card has an annual fee of S$3,924 for the principal cardholder.

The supplementary cardholder arrangement is slightly confusing. UOB offers:

- One free metal supplementary card

- Two free plastic supplementary cards

This does not mean you can appoint three supplementary cardholders for free. Instead, you can appoint two supplementary cardholders for free, each of whom will receive a plastic card.

You can also request a metal card for one of your supplementary cardholders, but any additional metal cards beyond the first will cost S$654 each. Likewise, any additional plastic supplementary cards beyond the first two will cost S$381.50 each.

It is not possible to circumvent this by giving a plastic supplementary card to Persons A and B, and a metal supplementary card to Person C. Each supplementary cardholder must have a plastic card.

tl;dr: you get two supplementary cardholders free.

Annual fee waiver? What is this, the StanChart X Card? No. There’s no annual fee waiver. Not for you, not for the Prince of Nigeria, not for Lord Barrington. Everyone pays, simple as that.

Cardholders receive 50,000 UNI$ (100,000 miles) each year the annual fee is paid.

| Tier | Welcome Miles | Renewal Miles |

| Regular | 100,000 | 100,000 |

| Privilege Reserve Private Banking <S$5M AUM |

180,000 | 100,000 |

| Private Banking ≥S$5M AUM |

250,000 | 100,000 |

Privilege Reserve and Private Banking (<S$5M AUM) customers receive an extra 80,000 miles in the joining year, for a total of 180,000 miles.

Private Banking (≥S$5M AUM) customers receive an extra 150,000 miles in the joining year, for a total of 250,000 miles.

In terms of annual fees, the Reserve is the fourth most expensive card in the $500K segment, behind the AMEX Centurion, Citi ULTIMA and HSBC Prive.

| 💳 S$500K Cards Annual Fee (sorted from most to least expensive) |

||

| Cards | Annual Fee | Supp. Cards |

AMEX Centurion AMEX Centurion |

S$7,630* | 2x free^ |

HSBC Prive HSBC Prive |

S$5,327.92 | All free |

Citi ULTIMA Citi ULTIMA |

S$4,237.92 | 2x free |

| UOB Reserve |

S$3,924 | 2x free |

DBS Insignia DBS Insignia |

S$3,270 | 4x free |

| *Additional S$7,630 first-year initiation fee applies ^In addition to the two supplementary Centurion cards, a further two supplementary Platinum Charge cards are free |

||

How many miles do I earn?

| 🇸🇬 SGD Spending | 🌎 FCY Spending | ⭐ Bonus Spending |

| 1.6 mpd | 2.4 mpd | 2 mpd on luxury spend |

SGD/FCY Spending

UOB Reserve Cardmembers earn:

- 4 UNI$ for every S$5 spent in local currency (1.6 mpd)

- 6 UNI$ for every S$5 spent in foreign currency (2.4 mpd)

This makes the UOB Reserve Card the second highest-earning card in the $500K segment, even if its rounding policies are more punitive (more on that later, though my guess is that the average transaction size on these cards rather negates the effects of rounding).

| 💳 Earn Rates for S$500K Cards (Sorted by Sum of Local and FCY Earn Rates) |

||

| Cards | Local Spend | FCY Spend |

| HSBC Prive |

1.92 mpd | 2.4 mpd |

| UOB Reserve |

1.6 mpd | 2.4 mpd |

| Citi ULTIMA |

1.6 mpd | 2 mpd |

| DBS Insignia |

1.6 mpd | 2 mpd |

| AMEX Centurion |

0.78 mpd | 0.78 mpd |

Local Luxury Spend

UOB Reserve Cardholders earn 5 UNI$ per S$5 (2 mpd) on Local Luxury Spend, defined as local transactions at the following 96 merchants.

|

|

This is capped at the first S$20,000 per calendar month, and any spend above this amount will earn the usual 1.6 mpd.

It’s worth noting that some of these luxury merchants are on the AMEX 10Xcelerator list, however, so if you have an AMEX Platinum Charge or Centurion, you could be earning 6.25 mpd or 6.41 mpd on up to S$16,000 of spend per calendar year.

What is the FCY transaction fee?

All FCY transactions are subject to a 3.25% fee, which is on par with the rest of the market.

| 💳 FCY Fees by Issuer and Card Network |

||

| Issuer | ↓ MC & Visa | AMEX |

| Standard Chartered | 3.5% | N/A |

| American Express | N/A | 3.25% |

| Citibank | 3.25% | N/A |

| DBS | 3.25% | 3.25% |

| HSBC | 3.25% | N/A |

| Maybank | 3.25% | N/A |

| OCBC | 3.25% | N/A |

| UOB | 3.25% | 3.25% |

| BOC | 3% | N/A |

| CIMB | 3% | N/A |

With a 2.4 mpd earn rate and a 3.25% FCY fee, using your UOB Reserve Card overseas represents buying miles at 1.35 cents apiece.

Transaction date or posting date?

UOB cards track spending by posting date, not transaction date.

For example, if you made a transaction on 30 September 2025 and it posts on 2 October 2025, that amount will count towards October 2025’s bonus cap for Local Luxury Spend. Therefore, you should exercise caution when spending towards the end of the calendar month, in case transactions “leak” into the following period.

Mind you, that might also be a good thing. If you’ve already fully utilised September 2025’s bonus cap, you might be able to start tapping the October 2025’s cap towards the last few days of the month (it’s a bit of a gamble of course, because transactions with some merchants do post on the same day).

Which cards track spending by transaction date vs posting date?

When are UNI$ credited?

Base UNI$ are credited when your transaction posts, which generally takes 1-3 working days.

The bonus UNI$ for Local Luxury Spend will be credited within seven days of the start of the following calendar month.

How are UNI$ calculated?

Here’s how you can work out the UNI$ earned on your UOB Reserve Card.

| Local Spend | Round down transaction to nearest S$5, then divide by 5 and multiply by 4. Round down to the nearest whole number |

| FCY Spend |

Round down transaction to nearest S$5, then divide by 5 and multiply by 6. Round down to the nearest whole number |

This means the minimum spend required to earn miles is S$5. Spend S$9.99, and you’ll earn the same points as someone who spent S$5. Spend S$4.99, and you’ll earn nothing at all!

This means that the UOB Reserve Card actually earns fewer points on smaller transactions than the Citi ULTIMA or DBS Insignia, despite all three ostensibly earning 1.6 mpd.

To illustrate:

| UOB Reserve 1.6 mpd |

Citi ULTIMA 1.6 mpd |

|

| S$5 | 8 miles | 8 miles |

| S$9.99 | 8 miles | 14.4 miles |

| S$15 | 24 miles | 24 miles |

| S$19.99 | 24 miles | 30.4 miles |

| S$25 | 40 miles | 40 miles |

| S$29.99 | 40 miles | 46.4 miles |

| S$35 | 56 miles | 56 miles |

| S$39.99 | 56 miles | 62.4 miles |

Of course, the question is what the average size of a transaction on such cards is. If you’re spending four-digit amounts, for example, the number of miles lost to rounding really is negligible.

If you’re an Excel geek, here are the formulas you need to calculate:

| Local Spend | =ROUNDDOWN (ROUNDDOWN (X/5,0) * 4,0) |

| FCY Spend |

=ROUNDDOWN (ROUNDDOWN (X/5,0) * 6,0) |

| Where X= Amount Spent |

|

For the full list of formulas that banks use to calculate credit card points, do refer to these articles:

What transactions aren’t eligible for UNI$?

A full list of transactions that do not earn UNI$ can be found in the T&Cs at Point 1.5.

I’ve highlighted a few noteworthy categories below:

- Charitable Donations

- Government Services

- Hospitals

- Insurance

- Prepaid account top-ups (e.g. GrabPay, YouTrip)

- Real Estate Agents & Managers

- Utilities

As a premium product, the UOB Reserve Card avoids UOB’s general exclusion for education, so paying school fees will still earn UNI$.

For avoidance of doubt, UNI$ will be awarded for CardUp transactions.

What do I need to know about UNI$?

| ❌ Expiry | ↔️ Pooling | ✈️ Transfer Fee |

| 2 years | Yes | Waived |

| ⬆️ Min. Transfer | ✈️ No. of Partners | ⏱️ Transfer Time |

| 5,000 UNI$ (10,000 miles) |

3 | 48 hours (KF) |

Expiry

Surprisingly enough, UOB does not offer non-expiring UNI$ for its UOB Reserve Cardholders. Their UNI$ will expire after two years, just like any other UOB card.

Non-expiring UNI$ are only offered to UOB Reserve Diamond Cardholders (see below for more details).

Pooling

UNI$ pool across cards. If you have 7,500 UNI$ on the UOB Reserve Card and 2,500 UNI$ on the UOB PRVI Miles Card, you can redeem 10,000 UNI$ in a single transaction.

It also means that you don’t need to transfer your UNI$ out before cancelling the UOB Reserve Card, assuming it’s not your last UNI$-earning card.

Partners and Transfer Fee

UNI$ transfer to KrisFlyer and Asia Miles at a 1:2 ratio, with a minimum transfer block of 5,000 UNI$ (let’s ignore AirAsia, because converting points there is like throwing them away):

| Frequent Flyer Programme | Conversion Ratio (UNI$: Partner) |

| 5,000 : 10,000 | |

| 5,000 : 10,000 | |

| 2,500 : 4,500 |

The usual S$27 conversion fee is waived for UOB Reserve Cardholders, and since UNI$ pool, you can use the UOB Reserve Card as a conduit to cash out UNI$ earned on other UOB cards for free.

Transfer Times

UOB transfers to KrisFlyer are typically completed within 48 hours. Do note that transfers to Asia Miles can take significantly longer; it’s good to budget up to 3 weeks.

If you need your KrisFlyer miles credited instantly, you can move them via Kris+ at a rate of 1,000 UNI$ = 1,700 KrisPay miles. KrisPay miles can then be instantly converted to KrisFlyer miles at a 1:1 ratio.

| S$5 for new Kris+ Users |

| Get S$5 (in the form of 500 KrisPay miles) when you sign-up with code W644363 and make your first transaction |

However, those 1,000 UNI$ would normally have earned you 2,000 KrisFlyer miles, so you effectively take a 15% haircut. Therefore I wouldn’t recommend taking this option, unless you need a small top-up to redeem a flight, or have an orphan UNI$ balance (<5,000 points).

If you choose to do so nonetheless, do remember that it’s a two-step process:

- Transfer UNI$ to KrisPay miles

- Transfer KrisPay miles to KrisFlyer miles

Do not forget the second step! If you wait more than 21 days, or spend any of the converted KrisPay miles via Kris+, the entire balance will be stuck in the Kris+ app. KrisPay miles expire after six months, and can only be spent at a poor ratio of 100 miles = S$1.

Other card perks

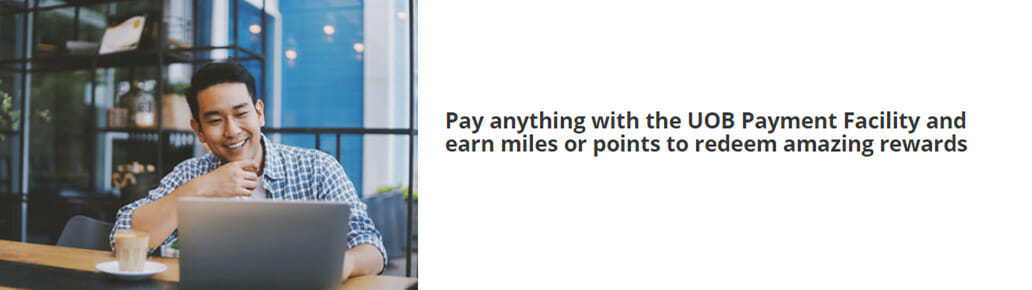

UOB Payment Facility

|

| UOB Payment Facility |

The UOB Payment Facility is a “no questions asked” bill payment facility that lets you buy as many miles as your credit limit allows.

The regular admin fee for UOB Reserve Cardholders is 1.9%, but this has been reduced to 1.6% until 31 August 2026 (and in all likelihood, will be further extended).

How it works is you specify how much you’d like to charge to the facility, e.g. S$5,000, and designate a bank account. UOB will then:

- Deposit S$5,000 into your designated bank account

- Charge S$5,090 to your credit card (S$5,000 + 1.6% admin fee)

- Awards UNI$ on the S$5,000 at a rate of UNI$2.5 per S$5 (the admin fee does not earn miles)

This gives you a total of 2,500 UNI$ (5,000 miles; the admin fee doesn’t earn miles). You take the S$5,000 UOB deposited to pay off your card bill, and your out of pocket cost is basically the admin fee. The miles divided by admin fee is the cost per mile (1.6 cents).

1.6 cents may not be the cheapest way of buying miles in Singapore; CardUp and Citi PayAll can often be cheaper. However, the main advantage of the UOB Payment Facility is that it’s “no questions asked”. You don’t need an NOA, tenancy agreement, invoice or other document; so long as you have the credit limit, you can buy the miles, simple as that.

Unlimited lounge visits

Principal UOB Reserve Cardholders receive unlimited Priority Pass visits, together with one guest.

Supplementary cardholders receive an unlimited-visit Priority Pass, without the guest allowance.

| 💳 Lounge Access for S$500K Cards (Sorted from Best to Worst) |

||

| Card | Free Visits (Per Year) |

|

| Principal | Supp. | |

| AMEX Centurion |

∞ + 1-2 guests | ∞ + 1-2 guests All supp. cards (2x free) |

| UOB Reserve |

∞ + 1 guest | ∞ All supp. cards (2x free) |

| HSBC Prive |

∞ | ∞ 3x supp. cards (3x free) |

| Citi ULTIMA |

∞ | ∞ 2x supp. cards (2x free) |

| DBS Insignia |

∞ | N/A 4x supp. cards (4x free) |

Of course, if you’re regularly travelling in First or Business Class (as most UOB Reserve Cardholders probably are), then a lounge membership may not be all that important.

Complimentary airport limo transfers

Principal UOB Reserve Cardholders are entitled to:

- 6x complimentary limo transfers per calendar year, if they are UOB Private Banking clients

- 4x complimentary limo transfers per calendar year, otherwise

These rides can be used for transfers to and from:

- Changi Airport

- Valencia Yachts reserved via UOB Reserve Concierge

- dinner reservations under Asia’s Finest Tables and Reserve Dining via the UOB Concierge

- cruises/staycations bookings made via the UOB Travel Concierge

All bookings and reservations must be charged to the UOB Reserve Card (e.g. you need to buy your air tickets with the card to qualify for an airport transfer).

Credit where it’s due, it’s good that UOB is offering airport limo rides beyond just the airport. At the same time, however, four rides is barely anything compared to the competition.

| Card | Limo Benefit | Remarks |

| AMEX Centurion |

Purchase First or Business Class ticket via Centurion Concierge | Round-trip transfer within Singapore, and on arrival at selected airports overseas |

| Citi ULTIMA |

Purchase First or Business Class ticket with card | One-way transfer in Singapore or overseas |

| HSBC Prive |

8x complimentary limo rides | Can be used in Singapore and on arrival at selected airports overseas |

| DBS Insignia |

No limo benefit | Limo rides offered through DBS Private Access programme, tied to AUM |

| UOB Reserve |

4-6x complimentary limo rides | Make dining, cruise, staycation or flight booking via UOB Travel Concierge |

Complimentary meet & greet services

Principal UOB Reserve Cardholders are entitled to two complimentary Meet & Assist or Fast Track Airport Immigration services per calendar year.

No minimum spend is required for this benefit. Cardholders will need to make bookings at least 72 hours before the desired pick-up time, and the principal cardholder must be one of the passengers. Guest fees are chargeable.

Golf perks

Principal UOB Reserve Cardholders are entitled to:

- 8x complimentary weekday green fees per calendar year, if they are UOB Private Banking clients

- 4x complimentary weekday green fees per calendar year, otherwise

This benefit is available at the Sentosa Golf Club and Tanah Merah Country Club, and excludes public holidays.

100,000 bonus miles

Principal UOB Reserve Cardholders who spend at least S$250,000 in a membership year will receive 100,000 bonus miles upon card renewal. S$250,000 is no small sum, though I assume the average cardholder might not find that much of an issue.

Keep in mind, this works out to just an incremental 0.4 mpd, so it’s not something you should go out of your way to achieve.

Complimentary travel insurance

| Coverage | Amount |

| Accidental Death | US$1,000,000 |

| Medical Benefits | N/A |

| Travel Inconvenience |

|

| Policy Wording | |

UOB Reserve Cardholders enjoy complimentary travel insurance when they charge their airfare to their card.

However, it’s surprisingly threadbare. While there’s US$1 million coverage for accidental death, and the standard travel inconvenience cover, there is no coverage at all for overseas medical expenses, emergency medical evacuation, trip cancellation or trip interruption.

Suffice to say: this should not be your primary source of travel insurance coverage.

Visa Infinite benefits

Principal and supplementary UOB Reserve Cardholders enjoy the following additional perks, provided by Visa.

| 🏨 Hotel Elite Status | |

| 🚗 Rental Car Elite Status | |

| 👍Other Perks |

For more information on how these perks work, refer to the post below.

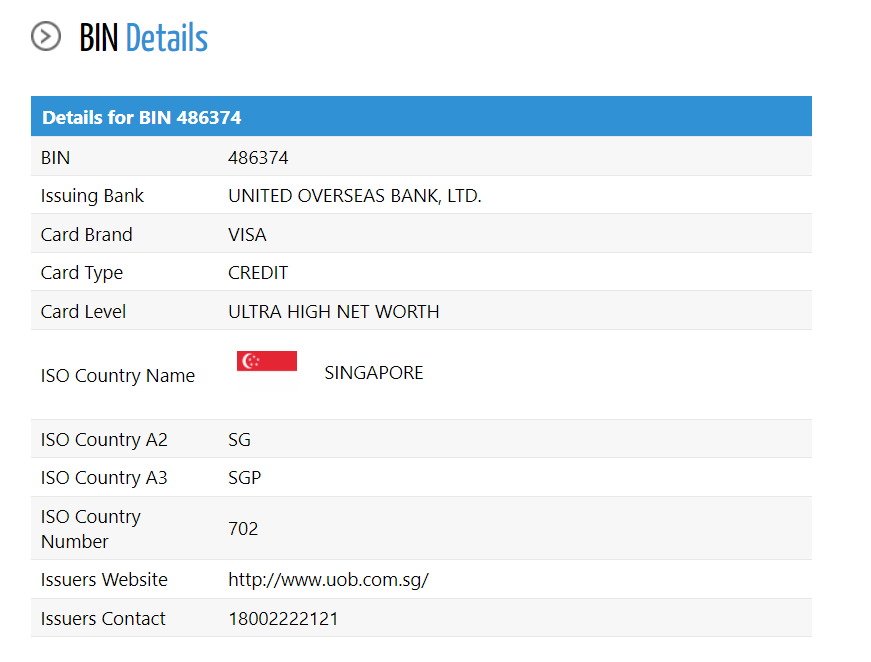

While the UOB Reserve Card’s card face says Visa Infinite, it’s actually part of the unpublished Visa Ultra High Net Worth tier. Don’t believe me? Run the card number through a BIN checker.

The question then becomes: what does the Visa Ultra High Net Worth tier offer? Honestly, I don’t know. So far I’ve only been able to find a special golfing programme where availability is much better compared to regular Visa Infinite (probably because there’s less competition for slots), but that’s about it.

UOB Reserve Diamond Card

Like every monied club, there’s always a higher tier of exclusivity, a secret level where the super elite can look down their noses at the regular elite.

That comes in the form of the UOB Reserve Diamond Card, which UOB Reserve Cardholders will be upgraded to upon spending at least:

- S$1 million a year on the UOB Reserve Card

- S$10 million a year on the UOB Payment Facility (which would cost S$160,000 in fees, based on the current rates)

Those are frightening sums (at least for me), but the reward takes bling to the next level: a card with an actual diamond embedded into it. How much does it cost to make? Well, if you want an additional supplementary card, each will cost you S$1,090 (and you’re limited to two).

Thankfully, it’s not a mere cosmetic upgrade. UOB Reserve Diamond Cardholders receive additional privileges, as summarised below:

|

|

|

| UOB Reserve | UOB Reserve Diamond | |

| Earn Rate |

|

|

| UNI$ Expiry | 2 years | None |

| Lounge Access | Principal: Unlimited Priority Pass (+1 guest) Supplementary: Unlimited Priority Pass |

|

| Limo Transfers | 4 per year | |

| Meet & Assist | 2 per year | 8 per year |

| Golf Games | 4 per year | 6 per year |

| Free 2nd Hotel Night | N/A | Once per quarter |

| Meal On Us | N/A | Once per quarter |

| Birthday Treat | N/A | Once per year |

| The physical Diamond Card has a validity of five years, but Diamond-tier privileges will be rescinded if the customer does not meet the qualifying spend in the subsequent 12-month membership period. In other words, you might have a physical UOB Reserve Diamond Card, but the features of a regular UOB Reserve Card. | ||

UOB Reserve Diamond Cardholders enjoy non-expiring points (why that’s a perk reserved only for those who spend S$1M a year, I do not understand), extra meet & assist usages, and extra golf games.

There are also three additional perks that UOB Reserve Cardholders don’t get:

- Free 2nd hotel night

- Meal on Us

- Birthday treat

Free 2nd hotel night

Principal UOB Reserve Diamond Cardholders are entitled to one complimentary hotel night when they book two consecutive nights at any hotel worldwide with UOB Travel Planners.

Unfortunately, the terms governing this perk are very strict:

- Maximum one redemption per calendar quarter

- Capped at S$400 per night

- Upfront payment required, and free night is forfeited if the reservation is changed or cancelled

It just seems incredibly stingy, given that the Citi ULTIMA Card offers the 2nd night free as a regular perk, with no limitation on usage or rebate amount. If a cardholder is spending S$1M with you each year, you’d think you could offer something better than a 0.16% rebate!

Meal on Us

Principal UOB Reserve Diamond Cardholders receive a complimentary meal for two persons, once per calendar quarter.

A redemption letter will be sent by the 30th/31st of each calendar quarter via mail. I would assume these are at suitably high-end restaurants, perhaps the ones under the Reserve Dining programme.

Birthday treat

Principal UOB Reserve Diamond Cardholders receive a special “birthday treat” during their birthday month.

Each principal Diamond Cardmember will be greeted via a call by UOB Reserve Concierge during his/her birthday month, based on the Cardmember’s last known contact number in the Bank’s records. UOB Reserve Concierge will then reveal the Gift via the call, and facilitate the Diamond Cardmember’s redemption.

I would hope this is much more than just a cake and some balloons, so if anyone’s experienced it before, please tell us!

Terms & Conditions

Conclusion

Is the UOB Reserve Card worth its S$3,924 annual fee?

In one sense, no.

The lounge, limo, meet & greet and golf benefits are matched or exceeded by cards at a lower price point and the complimentary travel insurance is bare bones. It’s not like the picture improves all that much for UOB Reserve Diamond Cardholders, who basically get four free meals, a S$400 quarterly hotel rebate and a birthday treat as a thank you for spending S$1 million annually — levels of spending that should, in theory, put you in the running for the much superior AMEX Centurion Card (though to be fair, that card carries double the annual fee).

But assuming you spend at least S$250,000 each year, then the 200,000 miles you receive (100,000 miles renewal + 100,000 miles spending bonus) would cover at least S$3,000 of the annual fee, or possibly even more, given that wealthier individuals tend to have higher miles valuations (since they might have paid for Business Class travel out of pocket otherwise).

Sure, there’d be a lot of opportunity cost in putting so much spending on a general spending card, but again, the typical customer profile for this card has better things to do than min-max 4 mpd cards each month (not to mention their bonus caps would be a distant memory at such levels of spending).

Which brings me to my next point: perhaps I’m coming at this from completely the wrong angle. If the S$3,924 annual fee is nothing but a rounding error to you — and I think that’s the target clientele for this card — then it’s not so much about making sure every dollar of annual fee is accounted for. It’s more about the less tangible benefits like service and access, and the overcompensatory joy of whipping out a Diamond-studded credit card.

And can you really put a price on that?

looking at the benefits made me laugh, do they really understand the customer whose annual income exceeding half a million. Can’t imagine who’d like to pay $3,852 for the membership fee would take the economy class and need a PP for the lounge. Very funny…

+1

Agree. Even for mass affluence, I really don’t understand positioning PP as status. Almost everyone gets it, what’s the big deal?

Other than the cachet of the Centurion, Ultima seems sensible

Before i open fd account and trust UOB with my pension i was solvent.

Today refusesal to play fair trader and refund my losses u o b leaving me hand to month preventing me to return home insolvent while keeps on boasting Bilions illgots profits.

Public should be warned. Without prejudice.

Jm. Uk expat.

Other than Amex centurion, out of $500k card only UOB has hotel elite status?

UOB reserve gets you free GHA titanium status upgrade

For the 200k spend qualification criteria, does this all have to be on a single UOB card or can it be spread across multiple UOB cards in the same 12 month window?

Multiple is ok

On the contrary, rich people are actually huge misers and the 3.8k+ IS going to matter to them as they scrutinise hard for value.

UOB Reserve gives the principal a complimentary birthday cake from Fullerton Hotel Cake Boutique yearly and also free upgrade to GHA Discovery Titanium status. Another point to note is spending $250k a year on the card will get you another bonus 100,000 miles upon renewal of card. So you will get 200,000 miles a year for the annual fee of $3888 which is a much better value for paying the annual fee.

Thanks Aaron for the detailed comparison, can you advise other than this card which other credit card allows us to buy krisflyer points?

Had it for some years and yup it’s useless. It’s so heavy and the paywave function of the card doesn’t work well. The card also does not work well on some overseas terminal slots. They give a plastic card for backup. The concierge service is so useless and probably outsourced.

Thanks for the information. Especially the lousy concierge – that’s the main reason to stay with one of these cards. Someone I met at a card-promotion dinner was waxing lyrical about their Reserve card. They loved the dining program and used it to buy miles at 1.6 cpm. Color me a skeptic. With only 2 restaurants per city in the program every season, it seems thin. Zen and Na-Oh I can get in myself. I hardly buy miles but if I had to I’d use the Beyond. Same transfer partners. Spending to get the diamond would net at least another… Read more »

They also offer a buy 1 get 1 free item at Club 21 as a birthday perk. I’m not sure whether it is still worthwhile for the fees. There are other cards more worthwhile that offers a 100k mile upon sign up like Standchart with a lower fee.