Here’s The MileLion’s review of the AMEX Solitaire PPS Credit Card, exclusively reserved for Singapore Airlines’ most valuable customers.

The publicity materials would have you believe that this card is the ultimate miles machine, with its complimentary upgrades to Suites or First Class, discounts on award flights, and earn rates of up to 1.5 mpd in Singapore and 2.4 mpd overseas.

In reality, however, it’s actually a very underwhelming card, and a good reminder of how easy it is to pass off mediocrity as exclusivity.

AMEX Solitaire PPS Credit Card AMEX Solitaire PPS Credit Card |

|

| 🦁 MileLion Verdict | |

| ☐ Take It ☐ Take It Or Leave It ☑ Leave It |

|

| What do these ratings mean? |

|

| While it may be targeted at Singapore Airlines’ top dogs, the AMEX Solitaire PPS Credit Card’s earn rates place it at the bottom of the food chain. | |

| 👍 The good | 👎 The bad |

|

|

Overview: AMEX Solitaire PPS Credit Card

Let’s start this review by looking at the key features of the AMEX Solitaire PPS Credit Card.

|

|||

| Apply | |||

| Income Req. | N/A* | Points Validity | 3 years |

| Annual Fee | S$561.35 (FYF) |

Min. Transfer |

N/A |

| Miles with Annual Fee |

N/A |

Transfer Partners |

1 |

| FCY Fee | 3.25% | Transfer Fee | N/A |

| Local Earn | ≤S$3.8K: 1.3 mpd >S$3.8K: 1.5 mpd |

Points Pool? | N/A |

| FCY Earn | ≤S$3.8K: 1.3 mpd >S$3.8K: 2.4 mpd |

Lounge Access? | No |

| Special Earn | 2 mpd on SIA, Scoot, KrisShop, Pelago | Airport Limo? | No |

| Cardholder Terms and Conditions | |||

| *AMEX no longer publishes an official income requirement for this card; the last documented requirement was S$30,000 p.a. | |||

For context, Singapore Airlines has a total of four Singapore Airlines AMEX cobrand cards, each targeted at a different section of the member base.

The AMEX Solitaire PPS Credit Card sits at the top of the hierarchy, and is exclusively for Solitaire PPS Club members. Just below it is the AMEX PPS Credit Card for regular PPS Club members, followed by the AMEX KrisFlyer Ascend and AMEX KrisFlyer Credit Card, which are open to all KrisFlyer members.

| Card | Eligibility | Annual Fee |

| AMEX Solitaire PPS Credit Card |

Solitaire PPS Club* | S$561.35 First Year Free |

AMEX PPS Credit Card AMEX PPS Credit Card |

PPS Club | S$561.35 First Year Free |

AMEX KrisFlyer Ascend AMEX KrisFlyer Ascend |

General public | S$397.85 |

AMEX KrisFlyer Credit Card AMEX KrisFlyer Credit Card |

S$179.55 First Year Free |

|

| *Only for principal Solitaire PPS Club members; supplementary members do not qualify |

||

It’s worth noting that a Solitaire PPS member is not obliged to take up the AMEX Solitaire PPS Credit Card. They can also choose the AMEX KrisFlyer Ascend or AMEX KrisFlyer Credit Card if they so wish. The only restriction here is that a Solitaire PPS member cannot take up the AMEX PPS Credit Card (and obviously, vice versa).

How much must I earn to qualify for an AMEX Solitaire PPS Credit Card?

American Express no longer publishes minimum income requirements for any of its cards, saying instead that “card application is subjected to customers meeting the regulatory minimum income requirement and internal assessment”.

Prior to this, however, the AMEX Solitaire PPS Credit Card had an income requirement of S$30,000 per year, the MAS-mandated minimum.

The biggest hurdle to membership isn’t so much the income requirement, but the fact that you must be a principal Solitaire PPS Club member to apply for this card. Supplementary Solitaire PPS Club members are not eligible.

If you subsequently lose your Solitaire PPS Club status, your AMEX Solitaire PPS Credit Card (and its associated benefits) will still be valid till the end of its expiry date, after which it will not be renewed.

And before someone asks, no. You cannot use the AMEX Solitaire PPS Credit Card in lieu of the Solitaire PPS Club membership card. Please don’t try to flash it for entry into the SilverKris Lounge; you’ll just embarrass yourself and everyone around you.

How much is the AMEX Solitaire PPS Credit Card’s annual fee?

| Principal Card | Supp. Card | |

| First Year | Free | Free |

| Subsequent | S$561.35 | S$81.75 |

The AMEX Solitaire PPS Credit Card has an annual fee of S$561.35 for the principal cardholder, and S$81.75 for supplementary cardholders.

The first year’s annual fee is waived for the principal card, as well as the first two supplementary cards. However, this only applies if you do not currently hold any other cobrand American Express Singapore Airlines cards. For example, someone upgrading from the AMEX KrisFlyer Ascend to the AMEX Solitaire PPS Credit Card would still have to pay the annual fee.

Principal cardholders can request an annual fee waiver for the second and subsequent years, but unless you’ve been using it regularly over the past year (American Express does not define a minimum spend threshold for a fee waiver), or hold a premium card like the AMEX Platinum Charge or AMEX Centurion, you may not be successful.

What welcome offers are available?

| AMEX Solitaire PPS Credit Card |

|

| Apply | |

| First Spend | 5,000 miles |

| Spend S$10,000 (First 90 days) |

29,500 miles |

| Base Miles from S$10,000 spend (@ 1.3 mpd) |

13,000 miles |

| Total Spend | S$10,000 |

| Total Miles | 47,500 miles |

New-to-AMEX cardholders who apply for an AMEX Solitaire PPS Credit Card by 31 January 2027 will receive 29,500 bonus miles when they pay the annual fee and spend S$10,000 within 90 days of approval.

Cardholders will also earn a further 13,000 base miles from the S$10,000 minimum spend (S$10,000 @ 1.3 mpd).

In addition to this, all first-time American Express KrisFlyer cobrand cardholders will enjoy 5,000 bonus miles on their first spend of any amount. This is a once per lifetime bonus, so if you’ve held an American Express Singapore Airlines cobrand card before, you won’t receive it a second time.

| ❓ New-to-AMEX definition |

|

New-to-AMEX customers are defined as those who:

Do note that American Express has tightened its definition of new-to-AMEX customers, and holding even a supplementary card will disqualify you! |

Truth be told, this is a very poor welcome bonus. Earning 34,500 bonus miles with a minimum spend of S$10,000 works out to just 3.45 mpd — well below what other cards are offering.

How many miles do I earn?

| 🇸🇬 SGD Spend | 🌎 FCY Spend | ⭐ Bonus Spend |

| ≤S$3.8K: 1.3 mpd >S$3.8K: 1.5 mpd |

≤S$3.8K: 1.3 mpd >S$3.8K: 2.4 mpd |

2 mpd (SIA, Scoot, KrisShop, Pelago) |

SGD/FCY Spend

The AMEX Solitaire PPS Credit Card has a rather complicated earning structure.

| First S$3,800 | S$3,801 and more | |

| SGD | 1.3 mpd | 1.5 mpd |

| FCY | 1.3 mpd | 2.4 mpd |

- For spending up to S$3,800 per calendar month, both SGD and FCY spend earns 1.3 mpd

- For spending above S$3,800 per calendar month, SGD and FCY spend earns 1.5 mpd and 2.4 mpd respectively

On the surface, these sound like competitive rates compared to other general spending cards — but they’re not.

First, the higher earn rates only apply to every S$1 spent above S$3,800. In other words, if you spend S$4,000 on the AMEX Solitaire PPS Credit Card, you’ll earn S$3,800 x 1.3 miles + S$200 x 1.5 miles. This means that your blended earn rate will always be pulled down by the “drag” imposed by the first S$3,800.

| 💳 Example: Weighted Average Earn Rates |

||

| SGD | FCY | |

| S$5,000 | 1.35 mpd | 1.56 mpd |

| S$10,000 | 1.42 mpd | 1.98 mpd |

| S$15,000 | 1.45 mpd | 2.12 mpd |

Second, local and foreign currency spending are not cumulative for the purposes of determining whether the S$3,800 minimum spend has been hit. In other words, you’ll need to spend more than S$3,800 in SGD alone, or S$3,800 in FCY alone, to unlock the higher earn rates. It cannot be a mix of the two— how silly!

Third, Singapore Airlines, Scoot, KrisShop and Pelago purchases do not count towards the S$3,800 minimum spend. Again: why?

Long story short, the earn rates are woefully uncompetitive compared to other general spending cards.

| 💳 Earn Rates for General Spending Cards (Income Req: S$30K) |

||

| Cards | Local Spend | FCY Spend |

UOB PRVI Miles Card UOB PRVI Miles CardAMEX Mastercard Visa |

1.4 mpd | 3 mpd IDR, MR, THB, VND 2.4 mpd All Others |

BOC Elite Miles Card BOC Elite Miles CardApply |

1.4 mpd | 2.8 mpd |

HSBC TravelOne Card HSBC TravelOne CardApply |

1.2 mpd | 2.4 mpd |

DBS Altitude Card DBS Altitude CardAMEX Visa |

1.3 mpd | 2.2 mpd |

OCBC 90°N Card OCBC 90°N CardMastercard Visa |

1.3 mpd | 2.1 mpd |

Citi PremierMiles Card Citi PremierMiles CardApply |

1.2 mpd | 2.2 mpd |

StanChart Journey Card StanChart Journey CardApply |

1.2 mpd | 2 mpd |

| AMEX Solitaire PPS Card Apply |

1.3 mpd Up to S$3,800 1.5 mpd S$3,801 onwards |

1.3 mpd Up to S$3,800 2.4 mpd S$3,801 onwards |

| AMEX PPS Card Apply |

1.3 mpd Up to S$3,800 1.4 mpd S$3,801 onwards |

1.3 mpd Up to S$3,800 2 mpd S$3,801 onwards |

| AMEX KrisFlyer Ascend Apply |

1.2 mpd | 1.2 mpd |

KrisFlyer UOB Credit Card KrisFlyer UOB Credit CardApply |

1.2 mpd | 1.2 mpd |

| AMEX KrisFlyer Credit Card Apply |

1.1 mpd | 1.1 mpd |

2 mpd for Singapore Airlines, Scoot, KrisShop and Pelago

The AMEX Solitaire PPS Credit Card earns an uncapped 2 mpd on:

- Singapore Airlines bookings (commercial and award tickets) made through singaporeair.com, mobile app or over the phone

- Scoot bookings (commercial and award tickets) made through flyscoot.com or the mobile app

- KrisShop purchases made onboard Singapore Airlines flights or at krisshop.com

- Pelago bookings made through pelago.com or the Pelago mobile app

Tickets must originate from Singapore and be purchased in Singapore dollars. Do note that the bonuses for KrisShop and Pelago transactions do not apply if you shop via the Kris+ app.

Considering how you could easily earn up to 4 mpd on these purchases with other credit cards, there’s nothing to get excited about here. And even if you run out of caps on those cards, the KrisFlyer UOB Credit Card offers an uncapped 3 mpd on Singapore Airlines, Scoot, KrisShop and Pelago.

What is the FCY fee?

All FCY transactions on the AMEX Solitaire PPS Credit Card are subject to a 3.25% FCY fee, which is on par with the market.

| 💳 FCY Fees by Issuer and Card Network |

||

| Issuer | ↓ MC & Visa | AMEX |

| Standard Chartered | 3.5% | N/A |

| American Express | N/A | 3.25% |

| Citibank | 3.25% | N/A |

| DBS | 3.25% | 3.25% |

| HSBC | 3.25% | N/A |

| Maybank | 3.25% | N/A |

| OCBC | 3.25% | N/A |

| UOB | 3.25% | 3.25% |

| BOC | 3% | N/A |

| CIMB | 3% | N/A |

Therefore, using your AMEX Solitaire PPS Credit Card overseas represents buying miles at 2.5 cents each (3.25%/1.3 mpd), which is far more than you should be willing to pay.

Transaction date or posting date?

The AMEX Solitaire PPS Credit Card tracks spending based on the posting date, not transaction date.

If you’re accumulating spend towards your welcome bonus, be careful about making transactions towards the end of the qualifying period– anything that posts beyond the deadline will not be included!

Which cards track spending by transaction date vs posting date?

How are KrisFlyer miles calculated?

Here’s how KrisFlyer miles earned on the AMEX Solitaire PPS Credit Card are calculated:

| SGD/FCY Spend (up to S$3,800) |

Multiply transaction by 1.3, then round to the nearest whole number |

| SGD Spend (S$3,801 and above) |

Multiply transaction by 1.5, then round to the nearest whole number |

| FCY Spend (S$3,801 and above) |

Multiply transaction by 2.4, then round to the nearest whole number |

Notice how the transaction is not rounded down to the nearest S$1; instead, it’s multiplied by 1.3, 1.5 or 2.4 straight away. This means the minimum spend to earn points is S$0.77.

This beneficial rounding policy allows the AMEX Solitaire PPS Card to compete favourably with ostensibly higher-earning cards like the UOB PRVI Miles (1.4 mpd), at least where smaller transactions are concerned:

| AMEX Solitaire PPS Card 1.3 mpd |

UOB PRVI Miles UOB PRVI Miles1.4 mpd |

|

| S$5 | 7 miles | 6 miles |

| S$9.99 | 13 miles | 6 miles |

| S$15 | 20 miles | 20 miles |

| S$19.99 | 26 miles | 20 miles |

| S$25 | 33 miles | 34 miles |

| S$29.99 | 39 miles | 34 miles |

If you’re an Excel geek, here are the formulas you need to calculate miles:

| SGD/FCY Spend (up to S$3,800) |

=ROUND (X*1.3,0) |

| SGD Spend (S$3,801 and above) |

=ROUND (X*1.5,0) |

| FCY Spend (S$3,801 and above) |

=ROUND (X*2.4,0) |

| Where X= Amount Spent | |

For the full list of formulas that banks use to calculate credit card points, do refer to these articles:

What transactions aren’t eligible for KrisFlyer miles?

The AMEX Solitaire PPS Credit Card’s full exclusion list can be found below:

Exclusions

a) Charges processed and billed prior to the Enrolment Date or charges prepaid on any Card Account prior to the first billing statement for that Card Account following the Enrolment Date;

b) Cash Advance and other cash services;

c) Express Cash;

d) American Express Travellers Cheque purchases;

e) Charges for dishonoured cheques;

f) Finance charges – including Line of Credit charges and Credit Card interest charges;

g) Late Payment and collection charges;

h) Tax refunds from overseas purchases;

i) Balance Transfers;

j) Instalment plans;

k) Annual Card fees;

l) Amount billed for purchase of KrisFlyer miles to top-up your miles balance;

m) Bill payments and all transactions via SingPost (e.g. SAM kiosks, mobile app, online portal);

n) Payments to insurance companies (except payments made for insurance products purchased through American Express authorized channel);

o) Payments to Singapore Petroleum Company Limited (SPC) service stations;

p) Payments for public transit in Singapore, including transactions on public trains and buses, and all transactions bearing the merchant description “BUS/MRT”;

q) Payments for the purpose of stored value card purchase / load / top-ups and/or the topping-up or loading of currency (or equivalent) for digital wallets, including but not limited to GrabPay and ShopeePay (with effect from 30 September 2025);

r) Payments to utilities merchants;

s) Payments to public/restructured hospitals, polyclinics and other public/restructured healthcare institutions and facilities;

t) Transactions relating to education and other non-profit purposes (including charitable donations);

u) Charges at merchants or establishments that are excluded by American Express at its sole discretion and notified by American Express to you from time to time.

Historically speaking, the AMEX Solitaire PPS Credit Card was very liberal with awarding miles, and merchant acceptance was a bigger issue than exclusions. However, in recent times the exclusion list has been growing (though to be fair, it’s no different from what other banks do).

Key exclusions are charitable donations (although in practice, miles still seem to be awarded!), education, GrabPay top-ups, insurance premiums, SimplyGo rides, SPC transactions, utilities and public hospitals. For the avoidance of doubt, private hospitals, CardUp and government organisations still earn miles, to the extent that AMEX is accepted.

However, American Express imposes certain restrictions on the types of payments that can be made via CardUp, which are explained below.

What do I need to know about KrisFlyer miles?

| ❌ Expiry | ↔️ Pooling | ✈️ Transfer Fee |

| 3 years | N/A | None |

| ⬆️ Min. Transfer | ✈️ No. of Partners | ⏱️ Transfer Time |

| N/A | 1 | Miles batched and credited once a month |

Expiry

KrisFlyer miles earned on the AMEX Solitaire PPS Credit Card will expire at the end of the month, three years after they were earned. For example, KrisFlyer miles credited to an account from 1-31 July 2024 will expire at the end of the day on 31 July 2027.

Cancelling an AMEX Solitaire PPS Credit Card has no impact on the miles already in your KrisFlyer account.

Pooling

All miles earned on the AMEX Solitaire PPS Credit Card will be credited directly to your KrisFlyer account, where they will pool with miles earned from all other sources (be it other credit cards, flights etc.).

Transfer partners & fees

At the risk of stating the obvious, the AMEX Solitaire PPS Credit Card is a co-brand card which does not give you a choice of where to credit your points. If you want to earn points that can be converted into a range of frequent flyer partners, pick a non-cobrand card instead.

All conversions to KrisFlyer are free of charge.

Transfer times

Miles earned on the AMEX Solitaire PPS Credit Card are batched and credited to your KrisFlyer account once a month.

You can typically expect to see them credited around the end of your statement period.

While direct crediting avoids conversion fees, it does mean the three year expiry countdown for KrisFlyer miles starts immediately.

Contrast this with non-cobrand cards where you pay conversion fees, but enjoy “two validities”, one on the bank side, and one on the airline side. For example, if I had a UOB PRVI Miles Card:

- My UNI$ are valid for two years

- Once I convert UNI$ to KrisFlyer miles, they’re valid for a further three years

- In total I get five years of validity

This means there’s slightly more time pressure to use your miles, though three years should be plenty for most people.

Other card perks

Business to Suites or First Class upgrade voucher

AMEX Solitaire PPS Credit Cardholders who spend at least S$50,000 on Singapore Airlines tickets via singaporeair.com or the Singapore Air mobile app between 1 July and 30 June each year of membership will receive an upgrade voucher from Business to Suites or First Class.

All tickets must originate in Singapore, and be purchased in Singapore dollars to count towards the minimum spend.

This voucher can only be used to upgrade commercial bookings (not redemption tickets) on Singapore Airlines in the Z, C or J booking classes. These correspond to Business Flexi, the most expensive fare class of all. It’s worth noting that until late 2024, it was possible to use this voucher with the U booking class (Business Standard).

| Fare Class | Fare Codes |

| Business Flexi | Z, C, J |

| Business Standard | U |

| Business Lite | D |

The voucher can be used for a cardholder or a redemption nominee, at least 48 hours before travel commences. It is valid for a one-sector upgrade only (e.g. if you have a round-trip SIN-LHR-SIN itinerary, only the outbound or inbound leg can be upgraded).

I love an upgrade as much as the next guy, but having to spend S$50,000 on Singapore Airlines tickets to unlock it? If you put that on the KrisFlyer UOB Credit Card instead, you’d earn 150,000 miles, compared to 100,000 miles with the AMEX Solitaire PPS Card. That’s enough for a First Class ticket to Hong Kong!

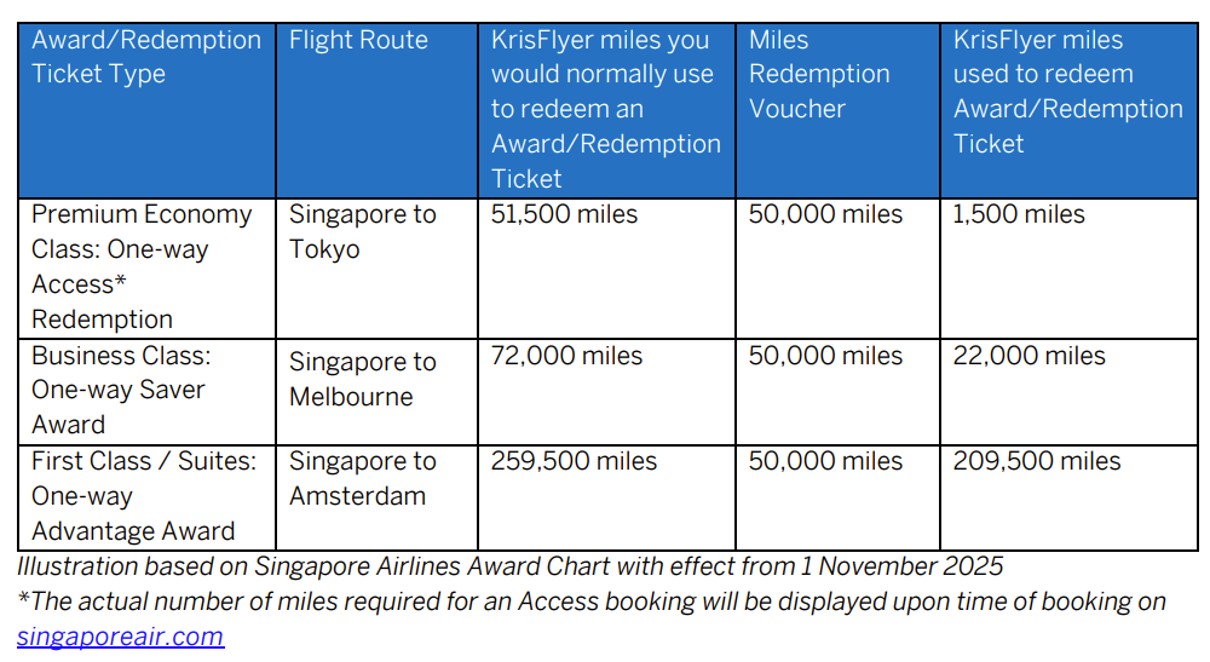

50,000 KrisFlyer miles redemption voucher

AMEX Solitaire PPS Credit Cardholders who spend at least S$75,000 on all retail transactions from 1 July to 30 June each year of membership will receive a 50,000 KrisFlyer miles redemption voucher.

This offers 50,000 miles off any Singapore Airlines redemption booking or upgrade, for the cardmember or any of their redemption nominees.

To use the voucher, your KrisFlyer account must satisfy both conditions at the time of redemption:

- Have at least 50% of the miles required to cover the full cost of the redemption booking/upgrade before applying the voucher, and

- Have sufficient miles to cover the full cost of the redemption booking/upgrade after applying the voucher

The following illustrations have been provided (though I don’t really understand how the last scenario makes sense!)

| Cost of redemption booking or upgrade | Miles required before voucher | Miles required after voucher |

| 50,000 miles | 25,000 miles | 0 miles |

| 80,000 miles | 40,000 miles | 30,000 miles |

| 100,000 miles | 50,000 miles | 50,000 miles |

| 140,000 miles | 70,000 miles | 90,000 miles |

Here’s an illustration of how the voucher works:

The voucher can be used for a cardholder or a redemption nominee, but do note that it’s only valid for a single passenger. For example, if you book two Business Class Saver awards between Singapore and Shanghai (45,000 miles each), you will pay 45,000 miles in total — the voucher covers the first passenger’s ticket, and the balance 5,000 miles is forfeited.

You also cannot combine the voucher with any other discount or promotion, so you can’t use it on a Spontaneous Escapes award. All bookings and travel must be within the voucher’s 12-month validity period.

Ultimately, S$75,000 is a lot to spend on a card like this. A 50,000 miles discount based on S$75,000 of spending is an incremental 0.66 mpd at best. You could earn far more miles by spending on other cards in the first place.

Complimentary travel insurance

| Coverage | Amount |

| Accidental Death | S$1,000,000 |

| Medical Benefits | N/A |

| Travel Inconvenience |

|

| Policy Wording | |

AMEX Solitaire PPS Credit Cardholders who charge their airfares to the card will receive automatic travel insurance coverage, underwritten by Chubb. For the avoidance of doubt, this applies both to cash tickets, as well as award tickets where the taxes and fees are paid for with the AMEX Solitaire PPS Credit Card.

Cardholders receive S$1,000,000 coverage for accidental death or permanent disability while traveling on a public conveyance. There’s also coverage for travel inconveniences like missed connections and bag delays.

However, there is no coverage for medical expenses, nor medical evacuation. This is something you can’t afford to miss, so a separate travel insurance policy is almost mandatory.

AMEX Offers

AMEX Offers are targeted deals pushed to AMEX cardholders, which can range from small savings like getting a few dollars back on contactless transactions, to much more substantial offers like S$790 worth of hotel credits at Four Seasons, Hilton, IHG, Marriott and other major chains. They can also take the form of bonus miles promotions, like a bonus 2 mpd on Deliveroo and foodpanda.

Some of the better offers we’ve seen recently include:

- S$60 back on S$300 spend with World of Hyatt

- S$3 back on every S$6 SimplyGo spend

- S$100 off S$500 spend with Cathay Pacific

- S$60 back on S$300 spend with Hilton

- S$80 back on S$400 spend with Shangri-La

AMEX Offers can result in excellent savings, but they’re not a unique feature of the AMEX Solitaire PPS Card.

Terms and conditions

Summary review: AMEX Solitaire PPS Credit Card

|

|

| Apply | |

| 🦁 MileLion Verdict | |

| ☐ Take It ☐ Take It Or Leave It ☑ Leave It |

As the flagship card of the Singapore Airlines co-brand portfolio, you might expect the AMEX Solitaire PPS Credit Card to offer eye-watering perks.

Well, the perks are eye-watering alright, but for the wrong reasons.

The fundamental problem is that the AMEX Solitaire PPS Credit Card has very crappy earn rates. It feels almost derisory to offer just 1.3 mpd on SGD and FCY spending, when other entry-level cards earn significantly more. And don’t let the 1.5/2.4 mpd rates deceive you — those only kick in for spending above S$3,800, and you will never actually be able to attain 1.5/2.4 mpd on a weighted average basis, due to the drag imposed by the first S$3,800 of spending.

Because of the poor earn rates, the opportunity cost of earning that First Class upgrade or 50,000 KrisFlyer miles redemption discount is simply too high. All you’re really doing is clawing back some of the miles that you lost by not spending on a higher-earning card!

Speaking of higher-earning card, I’m a firm believer that the KrisFlyer UOB Credit Card is the real MVP of the co-brand portfolio, with its uncapped 3 mpd on Singapore Airlines, Scoot, KrisShop, Kris+ and Pelago transactions. And you don’t need to be a Solitaire PPS member to qualify for it either!

So that’s my review of the AMEX Solitaire PPS Credit Card. What do you think?

S$50K spend getting you an upgrade voucher + S$75K spend giving you an additional 50,000 miles voucher isn’t bad at all. But the clause “Eligible flight bookings are for travel originating from Singapore only is a real killer — we usually buy tickets originated from Australia/Japan/SEA, rarely book flights originating from Singapore….

I dunno- that $75k could have earned way more miles on another card, and the 50k miles voucher is a lot more restrictive than 50k miles free and clear. 75k over 12 months is ~6k per month, most of which could probably found their way onto 4 mpd cards

75K for luxury spending busts 4mpd limits. It’s only another 22.5K miles on a 1.6mpd card. Maybe better taking the AmexPPS 50K voucher. For TPPS achieved on personal travel it wouldn’t be unusual spending. Look at the premium tiers for ION rewards, Paragon, Takashimaya Prestige. 250-500K vs TPPS 50K only.

you are absolutely right… this is the worst card on earth! A total failure card ! I was at a great shock to know how worthless it was when I enquired with amx on this card when i was awarded the pps some yeard ago. You are absolutely correct. 👍

It’s a pretty nice card. Imagine getting a first class suites upgrade or even a first class upgrade on a long haul 777-300 is not bad. I use it mostly for SQ tickets so the miles per dollar is 2.0 plus I get the first class upgrade and the 50K miles every year. All the 4 dollar per mile cards have stupid limits and you lose out once you cross those limits.

Will you be forced to upgrade/renew your regular Amex PPS CC to this Amex Solitaire PPS CC when your PPS membership upgrades to Solitaire PPS? Frankly the spend rewards of the regular Amex PPS CC are easier to reach…

nope- all that matters is your status at the time of application

Had it and gave it up after 1 year. Quite useless. Upgrade are subject to availability and not guaranteed. In the past when A380 suites had 10 it was much easier and 777 had 8 instead of 4.

I did use this card as proof of status at several pps events and they accepted it as my KF number was on it and they could verify.

really disappointed Amex n SQ came out with such a poor offering. But I guess that’s the a reflection of the sincerity of an organization

I believe the 140k to 70k vs 90k was from a time the voucher was 50% off miles instead of 50k miles flat rate.