With travel bans, circuit breakers, and a potential recession lurking around the corner, is it still worth holding a premium credit card?

I think that’s a very important question to ask yourself. After all, these cards often cost upwards of S$500 a year, and the fact that most are focused on travel benefits makes them expensive paperweights at the moment.

So what card benefits are still usable in these Covid-19 times, and can they justify the fees? Are fee waivers even possible, and if not, should you pull the plug?

Let’s take a closer look.

Citi Prestige

|

|

| Annual Fee | S$535 |

| Waiver Possible? | ☓* |

| Key Benefits | • 25,000 miles • Unlimited Priority Pass (+1 guest) • Airport limo • Boingo Wi-Fi • 4th night free on hotels • 1-for-1 4 Hands Kitchen experiences • Buy miles at 1.54 cents via PayAll |

| *Citigold Private Clients can get the first year’s fee waived |

|

The effective ban on non-essential travel means the Citi Prestige’s lounge, airport limo, and Boingo Wi-Fi benefits are close to useless right now. And unless you’re planning to do a four-night staycation, the Fourth Night Free benefit goes out the window too.

Cardholders get the occasional invite to special Citi Prestige events, and 1-for-1 offers on concert tickets/ 4 Hands Kitchen experiences, but these are understandably on hold until the worst of the outbreak passes.

This leaves buying miles as the main value proposition of the card. With income tax season at hand, Citi Prestige cardholders can buy miles for just 1.54 cents each via PayAll (2% fee @ 1.3 mpd).

Citi has also been running “spend and buy” promotions- the most recent one offers cardholders the chance to buy miles at just 1.15 cents each when they spend at least S$12,000 by June 30.

Finally, paying the S$535 annual fee gives you a further 25,000 miles, although it’s not the best of deals at 2.14 cents per mile.

So unless you really wanted to stock up on miles, I’d have difficulty justifying the annual fee of this card at the moment.

OCBC VOYAGE

|

|

| Annual Fee | S$488 |

| Waiver Possible? | ✔ (S$30/60K spend for Premier/regular customers) |

| Key Benefits | • 15,000 VOYAGE miles • Unlimited Plaza Premium Lounge (principal + supp) • Airport limo • Tower Club access (for PPC + BOS only) • Buy unlimited miles at 1.9-1.95 cents each |

Just like the Citi Prestige, the OCBC VOYAGE’s lounge access and airport limo benefits are pretty much negated in the current situation.

However, there’s one important distinction: OCBC has announced that VOYAGE cardholders can accumulate limo rides throughout 2020, which means your spending might yet reap dividends if travel becomes possible towards the second half of the year.

In contrast, the Citi Prestige (and all other cards with limo benefits for that matter) is adopting a “use it or lose it” policy. Any limo rides earned through spending simply expire if not used by the end of the quarter. This gives the VOYAGE a slight leg up in that regard.

You could use the OCBC VOYAGE to buy all the miles you want for 1.9-1.95 cents each, but you could just as well get the much cheaper UOB PRVI Miles card (which annual fee can be waived) and wait for a 1.8 cents PRVI Pay offer to come round again.

The silver lining is that annual fees on the OCBC VOYAGE can be waived if you spend at least S$60,000 (regular) or S$30,000 (Premier) in a membership year. Even if you don’t hit this, there are scattered stories of customers getting partial waivers (S$288) or full waivers by calling up. It’s worth a shot- the worst thing they can say is “no”.

HSBC Visa Infinite

|

|

| Annual Fee | S$650 (S$488 for HSBC Premier) |

| Waiver Possible? | ☓ |

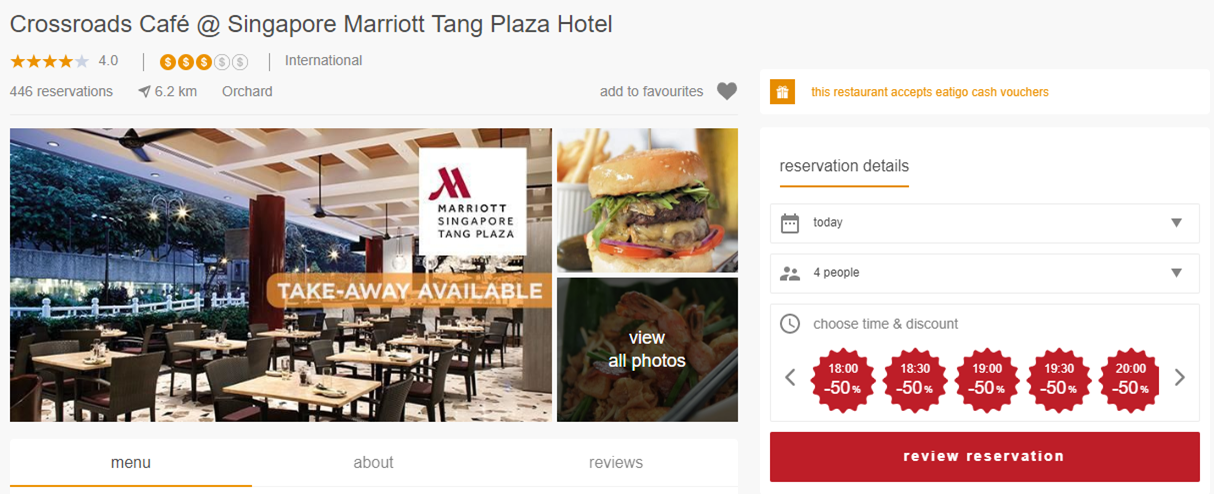

| Key Benefits | • 35,000 miles (first year only) • Unlimited LoungeKey (principal + supp) • Airport limo • Expedited immigration • ESPA access • Up to 50% off dining at Marriott Tang Plaza • Buy miles at 1.2/1.5 cents each via tax payment |

If this is the first year you’re holding the HSBC Visa Infinite, then there isn’t much to worry about. The 35,000 miles you receive upon approval more than offset the S$650 annual fee (even better if you’re an HSBC Premier customer).

However, the equation changes from the second year, because the annual fee doesn’t get you any renewal miles (if you make a fuss, you might get 20,000 miles, but that depends on a lot of factors and is hardly a given). That means you’re banking on the LoungeKey, airport limo, and expedited immigration to get your money’s worth- all unusable right now.

The complimentary ESPA access and 50% off dining at Marriott Tang Plaza shouldn’t move the needle either. The former is certainly not enough to justify the annual fee alone, and the latter isn’t unique to the HSBC Visa Infinite. You could enjoy the same benefit through the AMEX Love dining program, or even for free through Eatigo (where the 50% can be enjoyed by more than 2 people)

HSBC cardholders do have the opportunity to buy miles at 1.2/1.5 cents each when paying their income taxes (the cost depends on whether you’ve unlocked the “step-up” rate of 1.25 mpd), which is a decent price. But it’s otherwise difficult to make a case for the annual fee, and I’d have serious second thoughts about staying in the absence of a fee waiver.

Maybank Visa Infinite

|

|

| Annual Fee | S$600 (first year free) |

| Waiver Possible? | ✔ (S$60K spend) |

| Key Benefits | •Unlimited Priority Pass • Airport limo • Complimentary JetQuay access • Complimentary golf |

The Maybank Visa Infinite’s lounge access, airport limo and JetQuay access don’t count for much right now.

The only benefit to speak of is the complimentary golf for cardholders who spend at least S$1,000 in a calendar month. There are five clubs in Singapore (and 95 overseas, but that’s not so relevant now) to choose from, and a paying guest isn’t required in Singapore.

The annual fee on the Maybank Visa Infinite can be waived if you spend at least S$60,000 in a membership year. If so, carry on. If not, well I hope you really like golf.

UOB Visa Infinite Metal Card

|

|

| Annual Fee | S$642 |

| Waiver Possible? | ☓ |

| Key Benefits | • 25,000 miles • Four lounge visits • Complimentary Singtel ReadyRoam plans • Up to 50% off dining at Grand Hyatt • Gourmet Collection membership • Buy unlimited miles at 2 cents each |

What’s the best thing about the UOB Visa Infinite Metal Card during this time? You won’t miss the travel benefits.

I kid, I kid. But seriously, with only four free lounge visits, no airport limo, and data roaming plans only Singtel subscribers can enjoy, this isn’t exactly a card you get for travel. And that, kind of perversely, could potentially work in its favor.

Or does it? At the end of the day you’re still paying S$642 for 25,000 miles and some dining benefits. 50% off dining at the Grand Hyatt and 25% off at IHG hotels is nice enough, but with so many distressed F&B outlets practically spamming discounts, is that really much of a perk?

The UOB Visa Infinite Metal Card also has a “pay anything” feature that effectively lets you buy miles for 2 cents each. This sometimes drops to 1.9 cents, but like I said earlier, you’d be better off getting a UOB PRVI Miles card if you want to buy miles.

SCB Visa Infinite

|

|

| Annual Fee | S$588.50 |

| Waiver Possible? | ☓ |

| Key Benefits | • 25,000 miles (first year only) • Six lounge visits • Up to 50% off dining at The Fullerton Hotel & Fullerton Bay Hotel • Buy miles at 1.14/1.6 cents each via tax payment |

I guess you could crack the same joke for the now-discontinued SCB Visa Infinite. What travel benefits?

The SCB Visa Infinite comes with only six lounge visits, and gives you 25,000 miles in the first year. There’s an offer for up to 50% off dining at The Fullerton Hotel & Fullerton Bay Hotel, but that’s it for benefits.

It’s true that cardholders have access to the lowest cost miles facility in all of Singapore- by paying your income tax, you can buy miles for as low as 1.14 cents each. Is that worth an almost S$600 annual fee though? I doubt it.

SCB X Card

|

|

| Annual Fee | S$695.50 |

| Waiver Possible? | ? |

| Key Benefits | • 30,000 miles • Two lounge visits • Up to 50% off dining at The Fullerton Hotel & Fullerton Bay Hotel • Buy miles at 1.67 cents each via EasyBill |

The SCB Visa Infinite’s replacement is the even more expensive SCB X Card. It’s a relatively new product, however, so we don’t yet have data points about whether annual fee waivers will be offered (I doubt it), or whether the 30,000 miles will be given each year (quite possible).

Let’s be clear: no one’s going to pay almost S$700 for two lounge visits and 30,000 miles. I strongly suspect we’ll see a few new benefits added before July (where the first batch of annual fees come due), and to be fair, we have seen some nice offers of late, like a bonus on Emirates Skywards and Accor Live Limitless points transfers.

But neither of those will convince cardholders to stick around- if anything, they’ve given them excuses to cash out their points. So keep an eye out as July approaches, and hopefully we’ll be surprised.

AMEX Platinum Charge

|

|

| Annual Fee | S$1,712 |

| Waiver Possible? | ☓ |

| Key Benefits | • S$800 of travel credit • Unlimited Priority Pass (principal + supp) • Hotel elite status • Rental car elite status • S$200 of St Regis dining vouchers • 1 night at St Regis/W Singapore • 2 nights at selected Banyan Tree/ Mandarin Oriental hotels (1st year only) • 3x complimentary spa treatments • Tower Club access • Love Dining |

The AMEX Platinum Charge is a good deal more expensive than any other card listed here, which means you all the more need to weigh the benefits.

There’s no using the lounge or hotel benefits right now, and you’re obviously going to have issues spending the S$800 travel credit, what with all the uncertainty around future travel plans. The good news is that American Express has been quite understanding about this, and cardholders who call in have managed to get extensions on their credit.

In fact, as per data points in the AMEX Platinum Charge group, cardholders have managed to get extensions on the other perks too, be it spa treatments, dining vouchers or hotel nights. If you’ve got an expiring voucher on your hands, you definitely want to call up customer service and see what can be done.

Otherwise, Love Dining remains a big perk as ever (it doesn’t apply to takeaways, so it won’t be an option during the circuit breaker), although you don’t need the AMEX Platinum Charge to enjoy that. NOOK is also a useful place to go for a free drink and to get some work done. AMEX is known for its excellent Platinum events that typically happen once every two months or so, and I’m sure we’ll see these return once circumstances allow. I for one am really looking forward to the annual Platinum af’FAIR, where everyone tries to eat and drink their annual fee’s worth.

I last renewed my AMEX Platinum Charge in September 2019, so there’s still half a year to go before I need to make my renewal decision. For those of you facing the question now, I’d advise you to call up customer service and try to work something out- anecdotally, they do offer retention bonuses in the form of Membership Rewards points.

All things considered though, S$1,712 is no small amount of money, and you shouldn’t feel bad if you decide to walk away now and come back when the situation picks up.

How should you decide?

In my opinion, this all boils down to:

- How far away you are from renewal, and

- How you think the Covid-19 situation is going to pan out.

If renewal is due imminently, you need to accept the very real possibility of not being able to use any of the travel benefits for the better part of half a year (or more, who knows). Unless the card lets you carry forward benefits and entitlements (like the OCBC VOYAGE’s limo, or the vouchers with the AMEX Platinum Charge), you may want to cancel now and come back another time.

That said, even if you conclude your premium credit card isn’t pulling its weight at the moment, you shouldn’t cancel it prematurely. After all, it’s not like you get a pro-rated refund of the annual fee. You might as well sit tight until renewal comes round, then pick up the phone and talk to an RM.

Depending on your spending history and importance to the bank, you might get a retention offer (or waiver) that could change your mind. But if not, be prepared to walk away.

Conclusion

If there’s one thing the Covid-19 outbreak reveals, it’s how reliant premium cards are on travel benefits. Hopefully, this event gets product managers to rethink their approach, and introduce new benefits that can be used locally.

As a final point, do note that not all your card’s purported benefits are provided by the bank itself. Some may be offered by the card network (e.g Visa), and you can still enjoy them on other (cheaper) cards. For example, if you really value the Visa Infinite golf benefits, or the ability to book hotels through the Visa Infinite 4th night free program, then just get yourself a no-fee CIMB Visa Infinite and be done with it.

Are you holding on to a premium credit card? Do you plan to renew it?

Why no love for existing holders of the SCB VI?

Would you believe it didn’t even cross my mind? Will update later…

I think Amex Platinum isn’t charging the annual fee for those with card anniversary in March (at least in my case) – I have not seen them bill this amount in my statement although I have been monitoring it. I’m guessing they are going to wait awhile till things clear up a bit.

Interesting- did you get the vouchers?

Sorry for the late reply. Nope I did not. I’ve been monitoring my account every few days to see if they will charge me. Nada.

Not sure if that is a good or bad thing haha.. Maybe it’s fine while we are in Covid-19 mode.

I’ve been billed on 8 Apr.

I got 20k MR points for renewal after calling Amex. I’m taking a long term view that this is a card I’d like to keep. And who knows, maybe one day we can aspire to Centurian. I rather be a “model card member” than opportunistic. I don’t think the $800 or most other benefits are going anywhere. If COVID carries on till end of 2020 (ugh!), pretty sure extensions will happen on all perks in 2021. I don’t see this as a loss. Bottom line though, is that by God’s grace we can afford it. So I’m playing the long… Read more »

But if we don’t pay the (upcoming) annual fee, we have to transfer the points out. In this climate, we are probably not gonna redeem anything for a while. So wouldn’t it be better to pay a little premium to keep the points in the bank especially for those cards whose points that have no expiry?

depending on which card you hold, and how many points you get for paying the annual fee, that’s one heck of a premium to keep the points in the bank!

transfer fees, in the grand scheme of things, aren’t really that much no? you’re talking $25, and most FFP partners for SG cards either have activity-based expiry policies or 3 year validity. surely this will all be resolved in 3 years…

Of course, if we pay the annual fee, it has to be that they also give miles in return. If around the 2cpm range, I think it’s worth the slight premium (in normal times we would have paid anyway, no?). Moreover, I have a bunch of miles stuck because of Jun and potentially Dec cancellations. These were booked way before but from the look of things, are likely to be no go.

So the Amex platinum is worth having because you ‘are waiting to use the card’ while citi prestige is useless because you cannot use the benefits now?

I got a waiver for my amex platinum. Protip: look for Jamie Lee..

Haha, thanks for the tip. Does the waiver mean you don’t get the vouchers too?

Same question, waiver means no vouchers and no freebies?

Got the vouchers with waiver

This is for Platinum or Platinum Charge?

“Platinum” = Platinum Charge

“Platinum credit card” = well… Platinum credit card

“There are five clubs in Singapore (and 95 overseas, but that’s not so relevant now)”

Well, the local ones are not so relevant either now 🙂

faster path to relevance than the overseas ones at least!

Citi Prestige is worth considering for the heterogeneity of transfer partners; otherwise the new T&C for the 4th night has more or less gutted the card. To be fair though, the savings I got out of it when terms were better will cover another 3-4 years of annual fee so it balances out I guess.

Tried asking for a waiver for my Citi Prestige last week, today they confirmed that it’s impossible. No love.

They don’t do waivers for Prestige because of the 25K renewal miles. Anyway 1-for-1 at Iggy’s and Alma (ongoing) will add up to the annual fee. Not ‘offer’ menus but the regular full degustation menus. It covers the gap in Amex Love Dining for top-end establishments.