There’s nothing like a pandemic-driven recession to make people reconsider how much they’re willing to pay for a premium credit card.

After all, these expensive pieces of plastic (or metal) typically cost upwards of S$500 per year, and with most of their benefits effectively negated by Covid-19, what’s the point in shelling out?

And yet, it seems like business-as-usual for most premium card issuers. There’s been a deafening silence regarding Covid-19 initiatives, beyond the token “we’re all in this together guys” eDM.

What have banks done so far?

AMEX Platinum Charge

Annual Fee: S$1,712 Annual Fee: S$1,712Points from renewal: 20-50K (12.5-31K miles, on request) |

| COVID-19 initiatives |

|

The AMEX Platinum Charge has arguably had the biggest response to Covid-19, but with an annual fee that’s 3X the rest of the cards here, you’d expect them to.

From 21 April to 20 July 2020, all spending on the AMEX Platinum Charge will earn double the usual Membership Rewards points, and cardholders will receive double the value when redeeming points for statement credit.

| Normal | Promo Period (21 Apr-20 July) |

|

| General Spend | 0.78 mpd | 1.56 mpd |

| SIA/SilkAir/Scoot tickets | 1.95 mpd | 3.9 mpd |

| Platinum EXTRA Merchants | 7.8 mpd | 15.6 mpd |

| Statement Credit for 1,000 MR Points | S$4.80 | S$9.60 |

Cardholders who wish to redeem Membership Rewards points to offset their S$1,712 annual fee can also do so at an enhanced rate of 1,000 points= S$11.

Alternatively, if they choose to pay cash, they can receive a retention bonus of anywhere from 20-50,000 bonus Membership Rewards points. This does require a call to membership services, and depends on your negotiating ability, how long you’ve been with AMEX, and how much you’ve spent on your card.

AMEX is also offering extensions for the S$800 annual travel credit, as well as any spa or dining vouchers that are nearing expiry.

Finally, cardholders may also receive an extension of the qualifying window for sign-up bonuses. Normally, AMEX Platinum Charge members need to spend S$20,000 in the first 3 months after approval to receive 75,000 bonus Membership Rewards points. Some cardholders have been informed that they now have 6 months to do so. If you’re in this situation and haven’t received a call, it’s well worth requesting.

OCBC VOYAGE

Annual Fee: S$488 Annual Fee: S$488Miles from renewal: 15K |

| COVID-19 initiatives |

|

Limo rides earned through the VOYAGE normally need to be used within three months. However, in view of the current circumstances, OCBC has announced that any limo rides earned in 2020 will be valid until 31 December 2020 (or keep their original expiry date, whichever is later). It’s a customer-friendly move, and I applauded them for it.

And then…this happened. OCBC announced some major changes to the VOYAGE card, cutting earn rates, adding new exclusion categories and increasing the minimum spend for a limo ride.

| Until 1 June 2020 | From 1 June 2020 | |

| Local Earn Rate | 1.2 mpd | 1.3 mpd |

| FCY Earn Rate | 2.3 mpd | 2.2 mpd |

| Dining Earn Rate | 1.6 mpd | 1.3 mpd |

| Earning Blocks | S$1 | S$5 |

| Min. Spend for Limo | S$3,000 | S$5,000 |

There’s never a good time to cut back on benefits, but the decision to do so when customers are extra price sensitive is a puzzlement to me.

Citi Prestige

Annual Fee: S$535 Annual Fee: S$535Miles from renewal: 25K |

| COVID-19 initiatives |

|

I am very, very generously including Citi Prestige in the column of “cards which have done something.”

The fact of the matter is: Citi Prestige cardholders have got bupkis. Despite the fact that the lounge access, limo rides and the 4th Night Free benefit are effectively worthless at the moment, there have been no reports of annual fee discounts, much less waivers.

The T&Cs of the benefits remain the same. For example, airport limo rides must be earned and used within the same calendar quarter. Can’t use it? Too bad- there’s no carry forward. You could even argue that some benefits have gotten worse, such as the 4th Night Free perk. This has had extra restrictions imposed since 1 March 2020.

Heck, even the birthday benefits have gone down the toilet. It used to be (at least, back when I was a cardholder) that you’d get a free haircut, a complimentary workshop at Leica, and a wine tasting. What are customers getting now?

A vague reassurance that “your well-being is of utmost importance”, plus the token “best of health and happiness.”

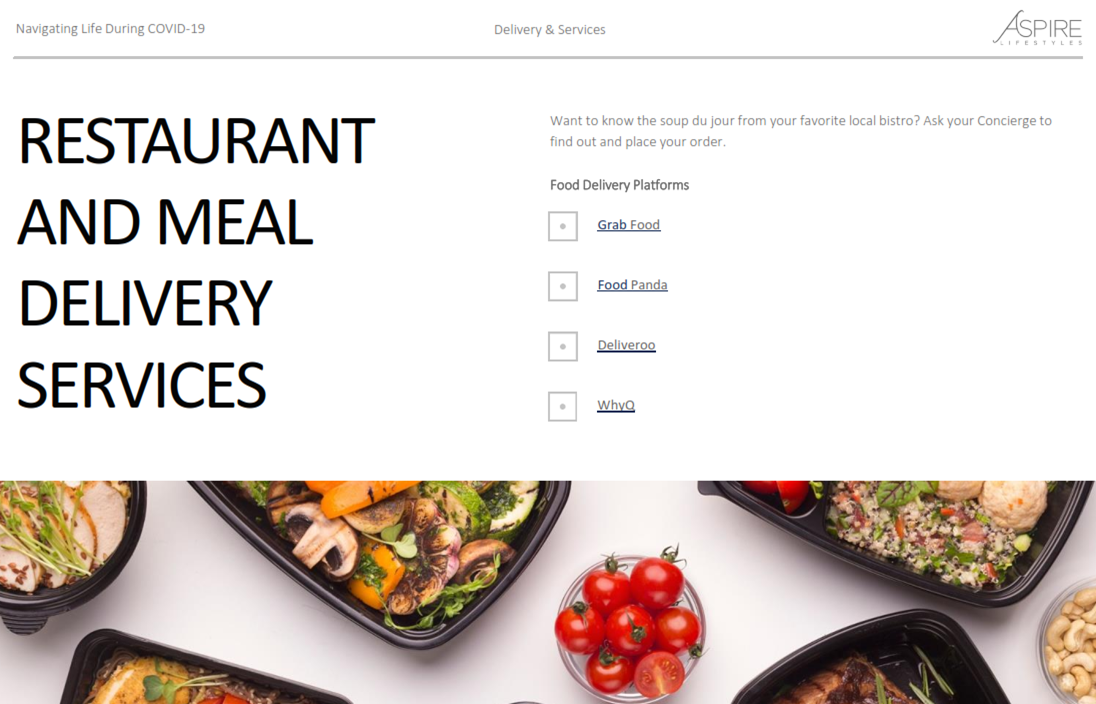

So why am I mentioning them here? Well, check out this amusing “resource pack” from the Citi Prestige concierge, which provides a series of pro-tips for navigating life during COVID-19.

Inside you’ll find such gems as a list of food delivery apps…

…ideas for working out at home…

…and links to livestreams from various zoos and aquariums.

Thanks guys.

And the rest?

I’m not aware of any initiatives by the rest of the premium cards on the market. As far as I know, they continue to charge annual fee as per normal, some awarding miles in return, but never enough to justify the fee in and of itself.

Annual Fee: S$488/650 Annual Fee: S$488/650Miles from renewal: 20K (on request) |

Annual Fee: S$695.50 Annual Fee: S$695.50Miles from renewal: 30K |

Annual Fee: S$642 Annual Fee: S$642Miles from renewal: 25K |

Annual Fee: S$600 Annual Fee: S$600Miles from renewal: None |

| 👍 To the SCB X Card’s credit, it has rolled out a few points transfer promotions to Emirates and Accor Live Limitless, as well as an FCY spending bonus. It’s questionable how useful these are in the current climate, but hey, at least it’s something. | |

At the rate things are going, they’re just setting themselves up for a wave of cancellations come annual fee payment time. And who can blame the customers, really? When you’re stuck at home all day and most of your spending is online, you’d do much better with basic cards that offer annual fee waivers.

Conclusion

With the possible exception of American Express, there’s hardly been what you might call a robust response to the current Covid-19 situation. In fact, all the stay-home spending promotions have come from the so-called entry level cards, with their expensive cousins nowhere to be found.

It’s time for cardholders to vote with their wallets. There’s no point paying good money if the sum total of the bank’s efforts is an eDM wishing you all the best.

Premium cardholders with upcoming renewals- are the banks offering you any enticements to pay the fee?

How about an article for those who are stuck on annual travel insurance plans too? 🙂

not too familiar with how that works actually. i know some policies are offering refunds, but i haven’t looked into it.

Mine is up for renewal in May and axa has been very persistent in my renewal over the last 2 months with no new benefits or guarantees Luckily I decided not to renew and start a new policy when things get better. There does not seem to have any benefits to renew besides a 20% off but there are so many new sign up policies that are better

Already cut up SCB VI and SCB X.

Errrr SCB X is made of metal right ? What u used to cut? Chainsaw ? Sorry just kidding

i don’t think there’s any point cancelling the x card ahead of time. might as well wait till july and see what else the team has planned.

The big 3 banks are sitting on a pile of non – performing loans, most notably from the collapse of Hin Leong. The last thing they want is to tweak rewards to suit CB spending patterns.

Unfair comparison. The miles given for renewal of Citi prestige more or less offsets the annual fee. Anything above that is a bonus.

Looks like someone’s getting some good ad spend from Amex. Anything to justify their huge fee.

1. Amex has 0 ad spending on this site, and any Amex ads you may see are served by Google adsense. quite the contrary actually, it’s citi who has done direct ad spending in the past!

2. I wouldn’t pay 2.14 cents per mile in this current environment, but to be fair, the value of a mile is inherently subjective. If you feel that’s worth it, more power to you 🙂

Dont think there are any ad spend, but he will get bonus miles from the member get member (MGM) programme if you sign up The Platinum Card using his link. It is quite a significant amount per referral. To be fair, his reviews are insightful and informative.

Agree with you on the huge annual fee, the Singapore version of “The Platinum Card” is one of the most costly Platinum Card in the world if you compare it with “The Platinum Card” issued by Amex Canada, UK or US. Of course, the perks and benefits are slightly different for different countries. I would rather the product manager here to remove the useless $800 of travel credit and reduce the annual fee to SGD 1k.

but i found you are giving more unfair comments than without scroll thru other hard work unbiased articles. Do some homework before giving unfair comments.

I think Amex still does give retention bonuses for payment with MR points.

After using Citi Prestige for almost a year, I’ve already found their benefits as “premium” credit card are pathetic. Now that it lost even those pathetic benefits under the circumstances, I’m highly skeptical if I will ever renew the membership.

In the meantime, I’m also unsure if the mileage accumulation will continue to be meaningful in the first place, as the world order is drastically changing, majority of airlines are facing bankrupt, and mileage demotion fest is almost sure to come.

Just tried requesting for an annual fee waiver for prestige today. Still not possible. Transferring my miles now, will call back to cancel it

That’s the right choice for you. I think Prestige card is for those can utilize at least one of the other benefits. Either very frequent Priority Pass User with guest or 4th night free. Local spend at 1.42 mpd is nice but not a clincher. The 25K miles are only worth $250 (1 cent per mile, since I expect major devaluation to happen soon, either through higher price of mile redemptions or lower cash price of tickets) so the other $285 has to come from another benefit utilization. If your usage doesn’t include such utilization, then I applaud your choice… Read more »