Ever since the debut of SimplyGo in 2017 (then known as Account-Based Ticketing, or ABT) passengers have been able to pay for bus or MRT rides with credit cards, making it possible to earn rewards on their daily commute.

Public transport is unlikely to be a significant chunk of your monthly expenditure, but every little bit helps. A regular recurring expense, charged to the right credit card, can add up over time. In this post, we’ll look at which credit cards offer the best rewards for SimplyGo.

How are you paying for public transport?

There are three ways to go about using your credit card for public transport, but be warned: only one of them will earn rewards!

❌ Top-up at General Ticketing Machines/ Add Value Machines

EZ-Link cards can be topped up with credit cards at General Ticketing Machines (GTMs) or Add Value Machines (AVMs) located inside MRT stations, ever since 2016. However, you will not earn any credit card points for transactions at these machines, so avoid them as much as possible.

❌ Top-up via EZ-Link app

EZ-Link cards can also be topped up via the EZ-Link app, either on an ad-hoc basis or via Auto Top-Up.

Again, this isn’t the right path to take. While it was possible in the past to earn 2 mpd on Auto Top-Up (then called EZ-Reload) with the HSBC Revolution or up to 1.4 mpd with the Standard Chartered Visa Infinite, both have been nerfed.

✔ Pay via SimplyGo

The only way to earn miles on your public transport rides is also the simplest. All you need to do is tap your credit card (or credit card linked to a mobile wallet) at the gantry.

All contactless-enabled credit cards can be used at bus and MRT gantries, with no need to register the card beforehand (although registration does allow you to track your fares and usage online or via the SimplyGo app).

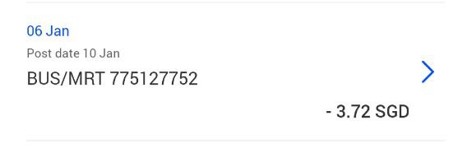

What MCC do SimplyGo transactions code as?

SimplyGo transactions code as MCC 4111 (Transportation, Suburban and Local Commuter Passenger, including Ferries) and will appear on your card statement as BUS/MRT.

There’s really no reason to doubt the MCC, but in any case, here are three ways of looking it up before making a purchase:

| Method | Ease of Use | Reliability |

| ❓HeyMax | ●●● | ● |

| 📱 Instarem app | ●● | ●● |

| 🤖 DBS digibot | ● |

●●● |

| Note: “Ease of use” and “reliability” are all relative. HeyMax already provides a solid baseline for reliability, and the DBS digibot is still simple enough to use, despite requiring more steps than the other two methods. | ||

What credit cards earn rewards for SimplyGo?

Here’s a summary of which banks offer rewards on SimplyGo transactions.

| 🚆 SimplyGo Transactions | |

| Bank | Awards Points? |

| ✕^ | |

| ✓ | |

| ✕ | |

| ✓ | |

| ✓ |

|

| ✓ |

|

| ✕* |

|

| ✓ | |

|

✓ |

| ^Exclusion does not apply to DBS- and UOB-issued AMEX cards *Exclusion applies to OCBC 90°N and OCBC VOYAGE Cards. The OCBC Rewards Card will earn 0.4 mpd on SimplyGo (but there’s really no reason to use it) |

|

| ❓Why do I see SimplyGo on the exclusion list? |

|

If you read through the T&Cs for Maybank and Standard Chartered, you’ll spot SimplyGo listed as an exclusion. Don’t panic. This refers to topping up the EZ-Link Mastercard available in the SimplyGo app, and not riding the bus or MRT. Remember, bus and MRT rides paid via SimplyGo code as BUS/MRT, not as SimplyGo (confusing as that is!). |

With that in mind, you can use the following cards to earn the most miles on SimplyGo. For the avoidance of doubt, you will earn the same miles regardless of whether you tap the physical card to pay at the gantry, or use the digitised version on your mobile wallet.

| 🚆 Best Cards For SimplyGo (Specialised Spending Cards) |

||

| Card | Earn Rate | Remarks |

DBS yuu Card DBS yuu CardApply |

10 mpd | Min. S$800 per c. month with 4x participating merchants; max S$823 per c. month |

StanChart Smart Card StanChart Smart CardApply |

Up to 9.28 mpd | Min. S$1.5K per s. month; 7.42 mpd with min. S$800 per s. month, 0.46 mpd otherwise |

UOB Preferred Platinum Visa UOB Preferred Platinum VisaApply |

4 mpd | Max. S$600 per c. month. Must use mobile contactless |

UOB Visa Signature UOB Visa SignatureApply |

4 mpd |

Min. S$1K max. S$1.2K contactless spend per s. month |

UOB Lady’s Solitaire UOB Lady’s SolitaireApply |

4 mpd | Max. S$750 per c. month, choose Transport as bonus category |

UOB Lady’s Card UOB Lady’s CardApply |

4 mpd | Max. S$1K per c. month, choose Transport as bonus category |

KrisFlyer UOB Credit Card KrisFlyer UOB Credit CardApply |

2.4 mpd | With min. S$1K SIA Group spend in a m. year |

The DBS yuu Cards offer an unbeatable 10 mpd earn rate, so long as you meet a minimum spend of S$800 per calendar month, and spend with at least four participating merchants (of which SimplyGo can be one).

The StanChart Smart Card offers an impressive-sounding uncapped 9.28 mpd, but the catch here is the minimum spend. Unless you can somehow spend at least S$1,500 in a month on fast food, streaming, public transport and EV charging, you’ll have to make up the difference with non-bonus spend that is rewarded at a much lower rate of just 0.46 mpd.

A lower tier of 7.42 mpd is available with a minimum spend of S$800, but even that is a significant amount of spending to hit on bonus categories alone.

Otherwise, the UOB Lady’s Cards offer 4 mpd, provided you’ve chosen Transport as your quarterly bonus category. But I’m of the opinion that Transport is a poor choice of categories, unless you also spend enough each month on taxis, ride-hailing and petrol to max out the bonus cap — all of which will divert spend from public transport anyway.

The KrisFlyer UOB Credit Card is another good option with an uncapped 2.4 mpd on public transport, provided you spend at least S$1,000 in a membership year with Singapore Airlines, Scoot and KrisShop.

If none of these work for you, then the remaining options are general spending cards with lower earn rates.

| 🚆 Best Cards For SimplyGo (General Spending Cards) |

||

| Card | Earn Rate | Remarks |

StanChart Beyond Card StanChart Beyond CardApply |

PB/PP: 2 mpd Regular: 1.5 mpd |

|

HSBC Premier Mastercard HSBC Premier MastercardApply |

1.68 mpd | |

DBS Insignia DBS InsigniaApply |

1.6 mpd | |

UOB Reserve UOB ReserveApply |

1.6 mpd | |

DBS Vantage Card DBS Vantage CardApply |

1.5 mpd | |

UOB PRVI Miles Card UOB PRVI Miles CardApply |

1.4 mpd | AMEX, Mastercard and Visa |

UOB Visa Infinite Metal Card UOB Visa Infinite Metal CardApply |

1.4 mpd | |

StanChart Visa Infinite StanChart Visa InfiniteApply |

1.4 mpd | Min. S$2K spend per s. month, otherwise 1 mpd |

DBS Altitude Card DBS Altitude CardApply |

1.3 mpd | AMEX and Visa |

HSBC TravelOne Card HSBC TravelOne CardApply |

1.2 mpd | |

Maybank Visa Infinite Maybank Visa InfiniteApply |

1.2 mpd | |

StanChart Journey Card StanChart Journey CardApply |

1.2 mpd | |

| Options earning less than 1.2 mpd are not shown |

||

A few important things to note:

- The HSBC Revolution will only earn 0.4 mpd on SimplyGo, because MCC 4111 is not included under its Transport bonus category

- The StanChart Journey Card awards 3 mpd for MCC 4111, but only if the transaction is made online — which SimplyGo is not

What about UOB’s S$5 minimum spend?

Because of UOB’s points rounding policy, you need to spend a minimum of S$5 to earn any miles on UOB cards— spend S$4.99 and you walk away empty-handed. Since most people won’t be spending that much on public transport rides per transaction (or even per day), the question then becomes how you could possibly earn anything out of this.

The answer lies in the fine print.

- For AMEX and Visa cards, fare charges are accumulated daily, but UNI$ are calculated based on the accumulated spend on SimplyGo Transactions per calendar month, and awarded to Cardmembers by the 7th calendar day of the following month. You’ll see a lump sum of UNI$ credited.

- For Mastercard, your accumulated fares are posted to your credit card account every 5 days or S$15, whichever comes first.

So except in extreme circumstances, you’ll definitely earn some miles on your rides.

Conclusion

While you won’t be redeeming a First or Business Class ticket on MRT and bus rides alone, every mile counts. By choosing the right credit card and payment method, you can turn an otherwise unrewarding expense into a steady trickle of miles or points over time.

Just remember: topping up your EZ-Link card won’t earn rewards, but tapping your credit card or mobile wallet via SimplyGo will (provided you don’t use AMEX, Citi or OCBC cards).

Now that the UOB PRVI offer has lapsed, I’m using the Zipster card for public transport. The transactions on this card code as online transactions, so I get 4 mpd on the WWMC or CRV

That’s interesting, but I can’t find any way to apply for the zipster card.

Interesting! What’s the MCC for Zipster postpaid payments?

If I opt for postpayment, they will collect the entire months worth and charge on one transaction, which may be more efficient than my current UOB Krisflyer $5 block miles earnings.

It’s the same as 4111. But these are online transaction hence can earn 4mpd. MCC doesn’t really matter

Email them to buy the card..

May I know what card is good for ERP and carpark? Any ideas on how to earn miles? Appreciate if this topic can be covered too.

Thank you for this post! Wondering why you did not include the UOB PP Visa though?

Because the UOB PPV only earns 0.4mpd for SimplyGo

Is UNI$ award for public transport based on monthly spend? Else if it is per trip basis, I am wondering if it is possible for 4 mpd using lady card, as UNI$ is awarded based on $5 block and each trip on public transport is unlikely to be more than $5.

I am very sorry, you have actually answered and I have completely missed it. Please ignore my comments.

Hi Aaron, OCBC clarified that OCBC N90 does award base points.

https://forums.hardwarezone.com.sg/credit-cards-line-credit-facilities-243/ocbc-ocbc-90%B0n-card-8-miles-%24-6101219-26.html

MCC 4111 is not in their blacklist

interesting- i was told otherwise at first. i’ll double check and update.

update: the post you linked to is dated 13 march 2020. the new t and c started from 1 june 2020, and 4111 is indeed blacklisted.

I see, thanks for the clarification! I do see MCC 4111 blacklisted in the Jun T&C:

https://www.ocbc.com/iwov-resources/sg/ocbc/personal/pdf/cards/tnc-ocbc-90n-card-programme.pdf

Ah! I had always thought Citi premier visa did

citi is sneaky about this. it’s not mentioned explicitly in their T&C, and is quite hard to find. however, navigate to this page (https://www.citibank.com.sg/citi-mastercard/index.html) and scroll to the bottom, where under the T&C (click to expand) you’ll read

Please note that SimplyGo transactions on Citi Cards will not earn Citi ThankYouSM Points / Citi Miles / Cash Back / SMRT$ / Citi M1 Rebate / Cash Rebate. Click here for the Citi ThankYou Points / Citi Miles / Cash Back / SMRT$ / Citi M1 Rebate / Cash Rebate Issuance Exclusion Terms and Conditions.

I have recently called Citi, and the service agent told me that we can earn rewards for MRT and busses as they fall MCC for Transportation. The agent clearly confirmed that for Premier mileage 1.2mpd, and for Rewards 0.4mpd. Did I get a wrong information?

How about the new HSBC Revo?

https://milelion.com/2020/07/01/awesome-hsbc-revolution-receiving-major-upgrade-from-1-august/

Do you see 4111 in the whitelist ? Read article please

thank you, i appreciate your input, but you really can use a better manner to tell me, why must be so challenging?

Why you expect to be spoonfed and still expect to be spoonfed politely. you emperor is it? all hail emperor karen!

Replying a comment from 11 months ago. Maybe you are the one that needs to read carefully.

Actually I am a blind man, so I really don’t “see”, but do you have to be so mean?

I’m teaching you how to find answer instead of not reading article & waiting for spoon-feed answer.

Halo, you yourself never read article. People provided info and you blamed other people ?

alternatively, i will use dash for public transport thru apple pay, since it can be topped up via Singtel with up to $200/mo and the telco bill can be paid by WWMC/CRV/CRMC for 4mpd.

hi, does this still work?

what about HSBC revolution card? does it earn 4mpd for SimplyGo too?

Nope

While grab MC do not give points for top-up, you can use grab mc for simply-go as well. They will give points now (afaik, they stopped giving points for a while but now it is back again). However, the points will only be given about a week after the transaction so it is not easy to track.

That being said, 1.7% Cashback for top-up then grab point for transport

PS. I tried it after reading somewhere on forum that the point is back and tested. It was working as of jun 7.

yup, i remember that public transport used to be on the grabpay exclusion list, but when i checked it yesterday it had been removed.

Hi, just stumbled upon your article. Thanks for the summary. Just curious, does Citi SMRT Credit Card get points for SimplyGo?

5% rebate for total spend above 500

Tldr: revolut. Nothing beats revolut currently

Agreed. Getting 20% cashback takes some of the sting away from the bus fare hike.

What about the DBS credit card $5 rounding? Do they also accumulate on a monthly basis like UOB?

The policy applies across all banks. And btw Dbs minimum spend to earn miles isn’t $5, it’s something like $1.67 or so. I’ve covered why in a separate article: https://milelion.com/2019/08/16/how-do-banks-calculate-credit-card-points-general-spending/

Anyone might know what is the MCC for top-ups via EZ-Link App? I charged it DBS credit cards and it showed up as “Transportation” using the DBS digibank chatbot.

Car sharing services like GetGo and BlueSG has MCC of 7512. Does this earn reward points?

Did a search myself. For Citi Rewards, its not eligible

If I use my Citi Rewards or UOB Lady’s Card to top-up my Grab wallet, and use Grab card to tap through the gantries, will I still earn 4mpd PLUS Grab points? Thanks in advance!

Does DBS Altitude still award DBS points for public transportation? I don’t see the line under the promotion & benefits on their page anymore.

I just starting using UOB PRVI and each trip posts as an individual transaction of less than $5 with no uni$ earned. Has this changes since this article? I will try DBS Altitude next week and see if I get any miles that way.

Does vantage earn 1.5mpd for simplygo spending?

Hi… ur posts are helpful … Will there be a updated version ? Seems now Citi cards are earning rewards for simplygo… can help to share comparison?

can i check why doesnt citibank award miles for transport? since it is not part of the exclusion list they stated.

https://www.citibank.com.sg/credit-cards/pdf/rewards-exclusion-list.pdf

You may wanna take a look at page 3 of the exclusion list, which states several merchant descriptions/keywords that exclude them from awarding points. I think that pretty much covered all public transportations.

is DBS altitude 1.3mpd now? Thank you

updated, thanks!

UOB One Card – max 10% Cashback on SimplyGo transactions.

https://www.uob.com.sg/assets/pdfs/one_card_full_tnc.pdf

I thought SC Journey was 3mpd for SimplyGo instead of 1.2?

no. even though mcc 4111 is on the whitelist, you must transact online for it to be counted. bus and mrt rides are not considered online.

Hi Aaron, how about UOB visa signature? Does it earn 4mpd on simplygo since it’s counted as contactless

Hi Aaron, please add the UOB One credit card and review it if it’s a good credit card.

For DBS Altitude, there seems to be a min $5 spend to get any miles…

Thanks for pointing out. I did not realise i was missing out until i saw your reply. Some days my transport only costs $1.50 because I walk instead, so I thought I was saving money — but I didn’t realise I was actually losing out on earning miles.

https://milelion.com/2024/07/28/review-dbs-altitude-card/

“Notice how the transaction is not rounded down to the nearest S$5; instead, it’s divided by 5 straight away. This means the minimum spend to earn points is not S$5, but rather: SGD spend: S$1.54”

“KrisFlyer UOB Credit Card, which earns an uncapped 3 mpd on public transport rides.” We need to spend a minimum $5 to earn 3 mpd? A bus/mrt ride usually cost less than $5 per ride, do we still earn 3mpd for each ride?

I called UOB, they said that Simplygo transactions earn 1.2mpd not 3mpd. However, not sure if we need to spend minimum $5 spend to earn miles since we do not earn bonus miles on Simplygo transactions.

Can you do a guide on Best Cards for Overseas Public Transport? Given most of these will be <$5 per transaction and won’t accumulate like SimplyGo, is StanChart Smart Card the only option in this category for specialised spending cards?

Seeing this — Smart Card won’t count because Smart Card works by merchant description (i.e. BUS/MRT*) and not MCC 4111. You can use any of the other cards except DBS yuu because that works by merchant description too. Alternatively, you can use your FCY card since the fare will be charged in FCY.

I used Maybank XL in UK. Just need to hit $500 min spend

Hi, I realise the UOB PPV has been added in the 2026 edition. But I thought the 2025 edition said the PPV would only earn 0.4 mpd? What changed?

Terms and Conditions changed

OCBC Frank Credit Card awards 10% cashback (capped at S$25 a month) for mobile contactless transactions at selected green merchants (including SimplyGo and EV charging), if there is qualifying spend of minimum S$800 on the card in that month.