| 🕰️ Hello, time traveller! |

| Found this page through a search engine? Look for the latest edition of this guide here |

As we kick off 2022, it’s never a bad idea to refresh your credit card game plan for the year ahead. Which cards should be your go-to options for miles? Which ones should be deprioritised, which ones cancelled? Just how many credit cards do you need, anyway?

Here’s my credit card strategy for the year ahead.

2022 Credit Card Strategy: Overview

Broadly speaking, there are two types of credit cards out there:

- General spending cards

- Specialised spending cards

General spending cards earn a flat rate (usually 1.2-1.4 mpd) on all transactions, while specialised spending cards earn up to 4 mpd on certain categories of transactions.

If there’s one resolution you make this year, it should be to use your general spending card as little as possible.

With specialised spending cards covering such a wide range of transactions, it seems almost sinful to settle for the lower earn rates of a general spending card. Put it another way- someone who regularly utilises 4 mpd cards will earn his/her free holiday 3X faster than someone who puts everything on a 1.2 mpd card.

The goal, therefore, is:

| 💡 Maximize 4 mpd Opportunities 💡 |

Every time you use a general spending card for a specialised spending category, you’re leaving money on the table.

Yes, it may mean applying for more than one credit card. Yes, it may be slightly less convenient. Yes, your spouse may get annoyed when you nag them about using the right card. But I promise you this: no one ever moaned about having to carry multiple credit cards when kicking back in a Business Class seat with some pre-flight champagne.

| 💳 2022 Credit Card Guide |

Contactless Payments: HSBC Revolution, UOB Preferred Platinum Visa, or UOB Visa Signature

| Card | Earn Rate | Remarks |

HSBC Revolution HSBC RevolutionApply |

4.0 mpd | Max S$1K per c. month on dining, groceries, shopping, travel Review |

UOB Pref. Plat Visa UOB Pref. Plat VisaApply |

4.0 mpd | Max S$1,110 per c. month, must use mobile payments Review |

UOB Visa Signature UOB Visa Signature Apply |

4.0 mpd | S$1K-2K per s. month on contactless/ petrol Review |

| C. Month= Calendar Month, S. Month= Statement Month | ||

Contactless payments aren’t a category of spending as such, more like a method. But since contactless terminals are so ubiquitous nowadays, earning 4 mpd on the vast majority of your transactions should be child’s play.

The UOB Preferred Platinum Visa (PPV) continues to be the go-to card here, earning 4 mpd on all mobile payment transactions except UOB$ merchants (previously known as SMART$), and UOB’s standard exclusion list (e.g. hospitals, schools, government bodies). This is capped at S$1,110 per calendar month.

| ⚠️ UOB PPV: Use Mobile Wallet! |

| To earn 4 mpd on the UOB Preferred Platinum Visa, you must add the card to your mobile wallet and tap your phone; you won’t earn the bonus if you tap the physical card. |

Those who regularly spend beyond the UOB PPV’s monthly cap can consider the UOB Visa Signature, which earns 4 mpd on contactless transactions with a minimum spend of S$1,000 per statement month on contactless and/or petrol transactions. This is capped at S$2,000 per statement month.

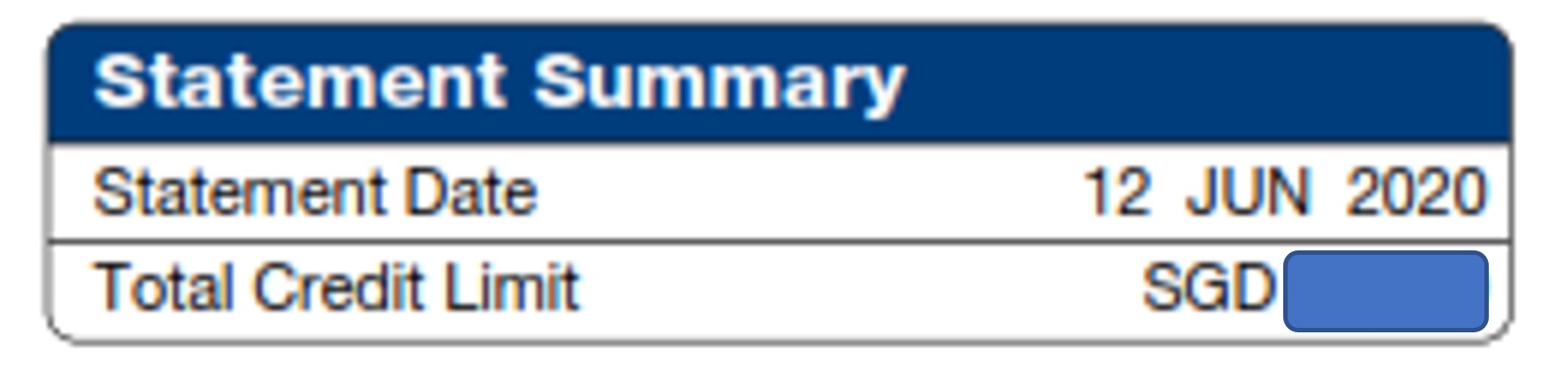

| ⚠️ Statement Month vs Calendar Month |

|

Your card’s 4 mpd cap may follow the calendar month or statement month. Calendar month is straightforward (i.e. 1-31 January), but statement month needs a little explaining. Generate your UOB e-statement and look for the statement date at the top right hand corner. This tells you what your statement month is; in the example below, it’s 12th to the 11th of the following month.

The UOB Visa Signature’s 4 mpd cap resets at the start of the statement month. This adds an unnecessary level of confusion, but you can always call up customer service and ask them to change your statement date to follow the calendar month instead. |

Alternatively, you can use the HSBC Revolution for 4 mpd on selected contactless payments, namely:

- Airlines and hotels

- Department and retail stores

- Supermarkets, restaurants and food delivery

- Transportation (excluding public transport)

This is capped at S$1,000 per calendar month.

It’s not quite the “4 mpd everywhere” that the UOB cards offer, but still a very wide range of day-to-day merchants. Even better, it covers both restaurants and hotels, which means no more confusion about what card to use when you’re dining at a hotel.

Dining: HSBC Revolution or UOB Lady’s Card/ UOB Lady’s Solitaire

| Card | Earn Rate | Remarks |

| HSBC Revolution Apply |

4.0 mpd | Max S$1K per c. month. Must use contactless Review |

UOB Lady’s Card UOB Lady’s CardApply |

4.0 mpd | Max S$1K per c. month. Must choose dining as 10X category. Review |

UOB Lady’s Solitaire UOB Lady’s SolitaireApply |

4.0 mpd | Max S$3K per c. month. Must choose dining as 10X category. Review |

| C. Month= Calendar Month | ||

Those who like eating out should arm themselves with either a HSBC Revolution or UOB Lady’s Card. I much prefer these over the Maybank Horizon Visa Signature, because not only are the earn rates better (4 mpd vs 3.2 mpd), the definition of dining is broader.

| Comparison of Dining Card MCC Coverage | |||

|

|

|

|

| HSBC Revo (4 mpd) |

UOB Lady’s Card (4 mpd) |

MB Horizon (3.2 mpd) |

|

| 5811 | ✅ | ✅ | |

| 5812 | ✅ | ✅ | ✅ |

| 5813 | ✅ | ||

| 5814 | ✅ | ✅ | |

| 5441 | ✅ | ||

| 5462 | ✅ | ||

| 5499 | ✅ | ✅ | |

| Examples | |||

|

|||

The UOB Lady’s Card is only available to women, but a simple workaround is to get your wife/girlfriend/wife and girlfriend to apply for the card, then add it to your mobile wallet. If possible, go for the UOB Lady’s Solitaire Card (min. income: S$120K), because it offers two bonus categories and a 4 mpd cap of S$3K per calendar month.

Sadly, 2021 saw the demise of the UOB Preferred Platinum AMEX, which had been a dependable dining card for many years. Goodnight sweet prince.

Foreign Currency (FCY): Amaze or UOB Visa Signature

| Card | Earn Rate | Remarks |

Amaze + Citi Rewards Amaze + Citi RewardsApply |

4.0 mpd | Max $1K per s. month |

| UOB Visa Signature Apply |

4.0 mpd | Min S$1K Max S$2K per s. month on FCY spending Review |

| C. Month= Calendar Month, S. Month= Statement Month | ||

In 2021, Instarem shook up the market for overseas card spending with the introduction of the Amaze. This card allows you to earn up to 4 mpd + 1% cashback on all foreign currency (FCY) spending, with zero FCY fees- what’s there not to like?

Unlike Revolut or YouTrip, Instarem does not use a prepaid wallet to fund Amaze. Instead, users link up to five Singapore-issued Mastercard credit or debit cards to Amaze, and select a default one to be charged at the time of transaction.

In that sense, transactions are a two-step process, with Amaze working as a passthrough. First your Amaze card is charged, then the underlying credit/debit card is charged.

By pairing the Amaze with a Citi Rewards, you can earn 4 mpd on all foreign currency transactions, subject to the usual MCC exclusions. Unfortunately, DBS nerfed Amaze transactions from 1 June 2022 onwards, which eliminates the DBS WWMC as a potential pairing option.

That said, there are still other solid alternatives, as summarised in the article below.

There’s absolutely no reason not to use Amaze, but for those who insist on an alternative, try the UOB Visa Signature. This earns 4 mpd on FCY spending, provided:

- you spend at least S$1,000 in FCY in a given statement month, and

- the payment processing is done outside of Singapore

The 4 mpd is capped at S$2,000 of FCY per statement month, and is shared with the 4 mpd cap for contactless payments/petrol. For a more detailed explanation of the caps, refer to my review of the UOB Visa Signature.

Offline Shopping: HSBC Revolution, Citi Rewards or OCBC Titanium Rewards

| Card | Earn Rate | Remarks |

| HSBC Revolution Apply |

4.0 mpd | Max S$1K per c. month. Must use contactless Review |

Apply |

4.0 mpd | Max S$1K per s. month Review |

OCBC Titanium Rewards OCBC Titanium RewardsApply |

4.0 mpd | Max S$13.3K per m. year. Pink and Blue cards have their own cap Review |

| M. Year= Membership Year, S. Month= Statement Month | ||

Why yes, my Gen Z friend. People still shop at brick-and-mortar stores. And when they do, they use the HSBC Revolution, Citi Rewards or OCBC Titanium Rewards for 4 mpd.

I would, however, lean towards the OCBC Titanium for the following reasons:

- The OCBC Titanium Rewards has a relatively narrower range of 4 mpd categories compared to the Citi Rewards and HSBC Revolution, and as a general rule you should utilise the less flexible caps first

- The OCBC Titanium Rewards’ 4 mpd cap is based on membership year, so if you have a big-ticket item to purchase, you can burn your entire year’s cap (S$13.3K) at one go

If possible, OCBC Titanium Rewards cardholders should try and get their hands on an OCBC Premier Visa Infinite. This no-fee card offers free conversions to KrisFlyer, and since OCBC$ are pooled, serves as a no-cost way of cashing out the OCBC$ from the Titanium Rewards.

Online Transactions: Citi Rewards or DBS Woman’s World Card

| Card | Earn Rate | Remarks |

Apply |

4.0 mpd | Max S$1K per s. month, excludes travel Review |

DBS WWMC DBS WWMCApply |

4.0 mpd | Max S$2K per c. month Review |

| C. Month= Calendar Month, S. Month= Statement Month | ||

Why yes, my boomer friend. People can shop on the interweb now. And when they do, they use the Citi Rewards or DBS WWMC for 4 mpd.

Like contactless payments, online transactions are another big catch-all category. Just think of how many online transactions you typically make in a given month: movie tickets, Grab rides, Deliveroo, Lazada shopping, Netflix subscriptions etc.

So long as it isn’t in the bank’s general list of exclusions (e.g. insurance, government), all online transactions will earn 4 mpd with the Citi Rewards (except travel) or DBS WWMC.

| ❓ Blacklist vs Whitelist |

|

You could certainly use the HSBC Revolution or UOB Preferred Platinum Visa, but it’s important to remember these cards follow a “whitelist” approach- a given online transaction doesn’t earn 4 mpd unless its MCC falls within the inclusion list. Contrast this with the Citi Rewards and DBS WWMC, which follow a “blacklist” approach- a given online transaction will earn 4 mpd unless its MCC falls within the exclusion list. |

If you’re using the Citi Rewards Card, remember not to use it for in-app mobile wallet payments, because you won’t earn any bonus. For example, using your Citi Rewards Card with Deliveroo directly would earn 4 mpd, but using your Citi Rewards Card with Deliveroo via Google Pay would earn only 0.4 mpd.

Petrol: Maybank World Mastercard, UOB Visa Signature or UOB Lady’s Card

| Card | Earn Rate | Remarks |

Maybank World Mastercard Maybank World MastercardApply here |

4.0 mpd | |

| UOB Visa Signature Apply |

4.0 mpd | Min S$1K Max S$2K on petrol + contactless per s. month Review |

| UOB Lady’s Card Apply |

4.0 mpd | Max S$1K per c. month. Must choose transport as 10X category Review |

| UOB Lady’s Solitaire Apply |

4.0 mpd | Max S$3K per c. month. Must choose transport as 10X category Review |

| C. Month= Calendar Month, S. Month= Statement Month | ||

Although I feel the best card for petrol is the one that gives the biggest discount, if you’re just looking at miles then it’s a toss up among the Maybank World Mastercard, the UOB Visa Signature, or the UOB Lady’s Card.

The Maybank World Mastercard is probably the best choice, because you don’t have to deal with minimum spending or merchant restrictions. Plus, you can apply for the Corporate Fuel Card and enjoy 15% off petrol at Shell.

If you prefer to stick with UOB, then the UOB Visa Signature will earn 4 mpd on petrol, provided you spend at least S$1,000 on contactless payments and/or petrol in a given statement month. UOB Lady’s Card members can earn 4 mpd on petrol as well, provided they choose transport as their quarterly 10X bonus category.

UOB cardholders will need to avoid Shell and SPC though, because these merchants will not earn UNI$.

Public Transport: SCB Smart Card or UOB Lady’s Card

| Card | Earn Rate | Remarks |

SCB Smart Card SCB Smart CardApply |

Up to 7.7 mpd | Max S$818 per s. month |

| UOB Lady’s Card Apply |

4.0 mpd | Max S$1K per c. month. Must choose transport as 10X category Review |

| UOB Lady’s Solitaire Apply |

4.0 mpd | Max S$3K per c. month. Must choose transport as 10X category Review |

| C. Month= Calendar Month, S. Month= Statement Month | ||

Public transport won’t be a huge component of your monthly expenditure, but it’s still a category worth optimizing.

Last year saw the launch of the Standard Chartered Smart Card, which despite its rather unimaginative name, packs a mighty wallop of up to 7.7 mpd on bus/MRT rides charged via SimplyGo.

| ❓ “Up to” 7.7 mpd |

| The earn rate of 7.7 mpd only applies if you have a Standard Chartered X Card or Visa Infinite. Otherwise, you’ll earn 5.6 mpd. For a detailed explanation why, refer to this link. |

Otherwise, a fallback option would be the UOB Lady’s Card/Lady’s Solitaire Card for 4 mpd, with transport selected as the quarterly 10X category.

Weddings

Getting hitched in 2022? Well done, you.

Assuming you’ve already maxed out your sign-up bonuses, you can use the following cards to pay off S$11,220 of your banquet amount each month, earning 44,880 miles in the process.

| Monthly Banquet Payments | ||

| 🤵 Him | 👰 Her | |

| UOB Pref. Plat. Visa Apply |

S$1,110 | S$1,110 |

| UOB Visa Signature Apply |

S$2,000 | S$2,000 |

| UOB Lady’s Solitaire Apply |

N/A | S$3,000 |

| HSBC Revolution Apply |

S$1,000 | S$1,000 |

| Total Spend | S$4,110 | S$7,110 |

| Total Miles | 16,440 | 28,440 |

For more details, refer to the dedicated post I wrote on the topic.

General Spending: AMEX HighFlyer Card or UOB PRVI Miles

| Card | Earn Rate | Remarks |

|

|

1.8 mpd | Only available to SME owners |

|

|

1.4 mpd (local) 2.4 mpd (overseas) |

Awarded per S$5 of spending Review |

UOB PRVI Miles

UOB PRVI MilesIn July last year, Singapore Airlines doubled the value of HighFlyer points, which turned the AMEX HighFlyer Card from unexciting also-ran into one of the best general spending cards on the market (1.8 mpd on all local and overseas spend).

My preferred approach is to use this card to top-up a GrabPay account, then spend via the GrabPay Mastercard. This way, I can earn 1.8 mpd + GrabRewards points, at no incremental cost. It’s also an easy way of getting around American Express’ sometimes limited merchant acceptance.

Don’t forget, you can also use a GrabPay card to pay bills with AXS, which means 1.8 mpd on normally-excluded categories like insurance, town council bills, MCST fees, income tax etc.

The main catch is that the AMEX HighFlyer Card is not a consumer card; it’s intended for owners of SMEs. Applications require an ACRA business registration number, so it won’t be an option for everyone.

In that case, I’d default to the UOB PRVI Miles (or the DBS Vantage for 1.5/2.2 mpd, if you meet the income requirement), although do remember that your general spending card is a card of last resort. Save it for occasions where 4 mpd opportunities don’t exist.

While the DBS Altitude/ Citi PremierMiles/ OCBC 90°N Card will earn slightly fewer miles at 1.2 mpd, I don’t see much harm in using them either. Ideally, you’d be putting minimal spending on your general spending cards anyway, and a 0.2 mpd difference should not be too material.

| ⚠️Don’t forget rounding! |

| In fact, despite its lower earn rate of 1.2 mpd, the Citi PremierMiles Card might be a better option for smaller transactions than the UOB PRVI Miles thanks to its more generous rounding policy. |

Of course, if you earn enough to qualify for one of the 1.6 mpd general spending cards such as the Citi ULTIMA, UOB Reserve, DBS Insignia or Premier/Private Banking versions of the OCBC VOYAGE, by all means go ahead and use it.

“Troublesome transactions”

There are a few categories of what I call “troublesome transactions”, generally excluded from rewards by most if not all banks.

Examples include:

- 💗 Charitable Donations

- 🏫 Education

- 🏣 Government Payments

- 🏥 Hospital Bills

- ☂️ Insurance

- 🚰 Utilities Bills

These aren’t lost causes, however. There are two ways to get something out of such payments.

UOB Absolute Cashback Card + GrabPay Mastercard

The first way is to use the UOB Absolute Cashback Card to top-up a GrabPay wallet, then pay for the transaction with a GrabPay Mastercard (or via AXS). You’ll effectively earn 1.7% cashback (plus Grab points, provided the MCC isn’t on Grab’s exclusion list), which may not be that exciting, but certainly better than walking away empty handed.

Since I have access to the AMEX HighFlyer Card, I use that for my GrabPay top-ups instead and earn 1.8 mpd.

Use a bill payment service

The second way is to use a bill payment service, which allows you to earn credit card miles on “troublesome transactions”, in exchange for a small fee.

| Provider | Fee | Cost Per Mile* |

| 2.5% | 1.52-2.50 | |

|

2.25% (code: GET225) S$30 off first payment with code: MILELION |

1.38-1.83 |

| 2% | 1.25-1.67 (only for Citi cards) |

|

|

1.9% | 1.36-1.9 (only for SC cards) |

| *Based on general spending cards with earn rates of 1.2 to 1.6 mpd | ||

You can use these services to pay things like tax, insurance, rent, tuition bills, MCST fees, season parking, donations, utilities bills and more.

Do look out for periodic promotions that can bring down the cost of miles even further.

Pulling double duty

While the sheer number of cards mentioned above may seem intimidating, the good news is that many can pull double duty. For example, a HSBC Revolution would take care of your dining, grocery and travel expenses, while a UOB PPV would be a simple solution for anywhere that accepts mobile payments.

If you told me I could have four cards and no more, my picks would be:

- UOB PPV (for all mobile payments at physical merchants)

- Citi Rewards (for all online transactions)

- DBS WWMC (for all online transactions)

- HSBC Revolution (for dining, grocery, travel and shopping transactions)

Is it possible to over-optimize?

As much as we want to maximize 4 mpd everywhere, is it possible to overdo it?

Yes, definitely. The way I see it, there are two additional considerations:

(1) Conversion Fees

By spreading your cards across multiple banks, you’re collecting different points currencies and will have to pay more than one conversion fee.

However, I’m not too worried about this. Conversion fees are annoying and we try to minimize them where we can, but paying them isn’t the end of the world. In the grand scheme of things, an extra S$25 fee here and there isn’t going to destroy the overall value proposition of the miles game.

Moreover, it doesn’t necessarily mean more cards = more fees. If you own multiple cards from the same bank, you may still pay only a single conversion fee, provided the points are pooled.

For example, there’s a UOB customer could hold a UOB PRVI Miles, UOB Preferred Platinum Visa, UOB Visa Signature and UOB Lady’s Card while paying only a single conversion fee.

(2) Orphan Points

Orphans points are a bigger concern than conversion fees in my book. If you spread yourself too thin, you may end up in a situation where you’re optimizing on individual transactions, but not in an overall sense.

To illustrate, suppose I drive very infrequently but get a Maybank World Mastercard just so I can earn 4 mpd on petrol. I may be optimizing on that particular transaction, but it counts for very little if I end up with a small chunk of TREATS points that I can’t cash out.

Optimization is good, but you need to look at both the micro and macro picture. If you don’t spend a significant amount on a particular category, then consider using your general spending card instead.

Conclusion

Spending categories may not always fall into neat little buckets, and may often overlap. For example, if you’re dining at an overseas restaurant, you could use the HSBC Revolution (dining) or the UOB Visa Signature (FCY) to earn 4 mpd. In a way that’s a good thing, because it helps reduce the number of cards you need to carry.

I’d also advise you to utilise the more restrictive caps first. Since the UOB PPV can earn 4 mpd at any merchant with a contactless terminal, I’d rather use my HSBC Revolution to pay for lunch and conserve the PPV’s cap for non-dining venues.

I’ve updated the “What Card Do I Use For…” guide, which provides more granular advice for certain categories. Do bookmark that page for further reference.

Any other cards you think should feature in the game plan? Sound out below.

Happy New Year Aaron!

One card to conquer them all (OK, two cards): Amaze + WWMC.

Agree!

2K is too low when you really want to do some online purchase after pairing it with Amaze.

Hi Arron, what is the best card strategy to buy a 50k watch?

at that level, you should be looking at sign up bonuses (https://milelion.com/credit-cards/current-credit-card-sign-up-bonuses/).

assuming you’ve maxed those out, then i suppose i’d ask to split the payment over multiple cards and earn the respective bonuses for uob vs, uob ppv, maybe citi rewards/hsbc revo/uob lady’s card (really depends on what the mcc is) before putting the rest on a general spending card.

Thanks for the suggestion

Happy new year! Agree with your choice of top 4 cards, here’s hoping they don’t get nerfed anytime soon..

It will be most useful to state that wwmc and uob ppv 4 mpd only come with block of min. 5 spending

Why dont low spenders use Amaze + WWMC for nearly everything in Singapore?

You certainly could, since amaze converts all offline transactions into online ones

The problem with WWMC and UOB PPV is that both round down to the nearest $5. If you’re making a lot of small purchases, you’ll end losing a lot of miles.

My first choice would be the HSBC Revolution which awards miles per dollar AND rounds UP every 50¢ or more.

I save the WWMC for situations when there’s no difference in miles earned (e.g. $25.30).

I’ve stopped using PPV as they’re always wiping out my UNI$ for the card’s annual fee.

The WWMC calculation isn’t that straightforward. You will still earn 9X points on transactions <$5 because of how the formula works. See https://milelion.com/2020/06/06/review-dbs-womans-world-card/ for more details

@ortloc @aaron, if UOB uses your UNI$ for your annual fee, is it possible to reverse this by calling in? if not, how to prevent this in the first place? convert your UNI$ into miles before the annual fee is charged?

you can call and ask for a waiver. if they dont want to waive, say you are cancelling the card- then they will have to refund and give you time to cash out before closing the account

Are banks obliged to give you time to cash out? The cheery CSO said “ok” after I told her I wanted to cancel my card. I had already cashed out whatever I could of my remaining UNI$ for a pathetic $10 voucher before calling in to cancel after the evildoers refused to waive my fee. UOB only called me later in the day to finally relent and waive off the charges, but the damage had already been done. I believe it’s going to be the same every card anniversary – UOB will charge the annual fee (in miles if there’s… Read more »

One can actually request the fee waiver via the TMRW app (it is a little deep but it is there). I tried it a few weeks ago for the PPV and it worked – instant waiver. For info, PPV is my only UOB card now.

Cardup is not eligible for 4 mpd with Citi rewards. However you could stack it with something like the uob prvi miles MasterCard for 1.4 mpd + 1% cashback

Can you pls advise where we get the 1% cashback with uob prvi miles mastercard? thanks

I suppose since there isn’t a specific category for flight tickets you would just park it under online transactions?

correct. can use WWMC (But not Citi rewards, because it’s travel).

Great, thanks for advising. Silly question but recurring payments like gym memberships and broadband charges would fall under online transactions too as well right?

How about pairing with Amaze? So that if I book my flights with citi rewards paired with Amaze, Amaze will convert the travel to online transactions, and then citi rewards will award me 4mpd right?

What cards will be good for large online transactions? Seems all of them have a fairly low cap. Say if I want to buy something for 5000

Titanium Rewards if it falls under the relevant MCC.

Hi Aaron, I’m curious on your thoughts on why the Singapore market has no hotel co-branded cards?

Is it the market size; might we see too much demand in some cases?

I’ve used Amaze on my recent overseas transactions now incur between 0.7-1% FX fee. Looks like Amaze is starting to incorporate a small margin for the transactions in foreign currencies. Anyone else have similar experience?

What rate are you comparing against? Amaze is usually pretty close to Mastercard rates – which are worse than mid market rates – like Revolut etc use. Amaze is better than the NIUM remittance rates.

Hey Aaron, would love to get your advice on maximizing my upcoming hotel wedding banquet spend (balance of around $13k payable mid Jan and mid Feb each). Unfortunately AMEX plat charge is not an option for now 🙁

Current cards: Citi PremierMiles, WWMC, Citi Rewards, HSBC Revolution, DBS Altitude

The option I’m currently thinking is to get the sign up bonus for Ascend, max out WWMC and HSBC revo, and put the rest to Citi PremierMiles.

Is there anything else that I’m missing here?

for wedding banquets where you pay in installments, what could be fun is that you and your spouse each get a uob ppv, uob vs and uob lady’s card (For her at least). declare travel as your 10x category for the uob lady’s card, then each month tap

1. $1k each on uob ppv

2. $2k each on uob vs

3. $1K on uob lady’s card

This way you earn 4 mpd on $7k of payments (and if your spouse qualifies for the uob lady’s solitaire, you can boost that up to $9K).

thanks! seems doable, now i just need get over the mental barrier of asking our coordinator to split this across 8 cards each month 😮

No shame just do it

You can add HSBC Revolution ($1K on contactless) on top of that too.

oh yes, forgot about that one. that’s another $2k for the two of you

Hi Aaron, for the HSBC Revo, contactless payment at:

1)Department and retail stores

2) Airlines and Hotels

Would Decathlon be counted as a retail store in HSBC’s definition and contactless payment for Airlines would mean making payment at SQ ION?

Thanks.

Decathlon falls under a non-qualifying MCC for HSBC Revo from my personal experience.

I currently have hsbc revolution, amex plat, dbs woman and dbs altitude. Starting to find that altitude actually isn’t that useful for me. If I want to apply for one more to maximize miles, and most of my spends are on dining and online, what do you advise? I’m also worried about a hit to my credit score if I apply for too many cards.

Anyone has issue using Amaze and Grab MC on AXS? Seems not be accepted anymore 🙁

For the visa signature, do we have to clock at least $1000 in FCY before the 4mp kicks in? thanks

yup.

thanks Aaron

AXS Online support MCST fees, have to check if your MCST, if not ask your condo manager to sign up (I got mine to sign up). Used to be able to use Amaze and Grab MC on AXS online but now both cards seem to be unaccepted 🙁 If not, all Mastercard cards are accepted

Happy New Year guys! How about telco bills?

This is a great post. As most of these cards have an annual fee, do you have any recommendations on how much one should be paying in annual fees per year? Paying $500 or $800 or more seems like a lot. Do you have advice on how to think about this?

What’s the upside of paying annual fees? Most of the cards have first year waiver. If the bank doesn’t waive after that then just cancel. 12 months after cancelling you can get the sign up bonuses again. It takes a bit of effort to manage points and payments but paying fees for credit cards is a waste of money. Just churn them.

Got it. Thank you!

Please can you update WHAT CARD DO I USE FOR… Page as well Aaron? Thank you

Since the WWMC is such a great card, would it make sense to apply for you and your spouse to apply for a main + supplementary card each since that would give you a a total of $8k/month cap?

your spouse should apply, but the cap is shared between principal and supp.

Hi Aaron, do recurring payments for utilities, home broadband, membership fees, etc. fall under online transactions?

Would the Citi Rewards card via Instarem still exclude travel related online transactions even if its charged in foreign currency?? Also does paying via Instarem bypass this exclusion? I’m confused!

Not sure if it’s just me, but as a current UOB cardholder without the PPV, I no longer see the UOB PPV on my list of cards that I can apply for.

https://bit.ly/34GYazj

Still can apply directly on the UOB site.

Hi all,

Do Citi Rewards and OCBC Titanium cards earn 4 mpd for offline shopping at furniture shops such as Picket & Rail, Kuka Sofas and Novena Furniture?

If not, which card would be optimal for offline furniture purchases from non department stores?

Thanks in advance

Does it make sense to get the UOB PPV instead of HSBC Revo since the caps between the two is just $100 difference, and the latter lets you use contactless payment, plus no $5 blocks and fewer limits on merchants that qualify? Would be good to get everyone’s thoughts, thanks

You need to look at your strategy as a whole.

Points on UOB cards pool, so if your strategy is heavy on UOB cards, PPV means you have little risk of orphan points. Whereas HSBC would mean you may have a few thousand points sitting in HSBC and the rest in UOB.

why not both though? it’s not either/or.

That’s true, although I’m not sure I’d spend $2.1K in most months 😀

Hi Aaron, Thanks for the very informative article! I have a target to score a business class upgrade for a roundtrip Singapore-Paris flight with Qatar Airways. As per checking, an upgrade to business class would require 85,000 Qmiles. To earn miles faster, I am thinking of getting an Amaze card + DBS Woman’s Card that would let me earn 4 MPD. However, I wanted to know if I can convert my Amaze miles and DBS miles to Qmiles? If I can, how and what is the ratio? Is there also a redemption fee? I currently have a Citipremiermiles Visa card… Read more »

Just curious, will there be any reason for someone to use WWMC without Amaze if he has the Amaze card?

Does anyone know if all offline spend will be converted to online spend for Citi Rewards to earn 4mpd? I’m travelling for an extended period soon and it would be useful to rely largely on Amaze + Citi Rewards instead of cash.

TIA!

appreciate for your effort to share, calculate and advisory!

“Citi Rewards (for all online transactions)

DBS WWMC (for all online transactions)”

Both are for online? No offline?

Hi Aaron,

First of all would like to thank you for providing a sea of information on this forum which isnt readily available and most of the people arent even aware.

I have a question – for people like me who pay rent as the biggest expense, is there any card that can get me best miles for rent? Or i have to list under 1.4 mpd only by paying via card-up? I tried searching but couldnt find an effective answer.

Kind Regards

Ron

you’d have to look at a service like cardup for rent, good news is they have some promotions: https://milelion.com/2021/12/28/cardup-extends-1-79-rent-payment-promo-till-june-2022/

Hi Aaron,

If i remember correctly i read some article where there is a credit card trick with “Amaze + Grabpay+ OCBC Cashflo credit card” to retain ~ 10K in bank account consistently.

Add Grabpay MC & OCBC Cashflo card in Amaze. Top up Grabpay wallet by 1K from ocbc CC, take out to bank account via amaze card. OCBC CC will split into 6 months instalment without any fees.

I vividly remember the details. can you please help to point out the article? thanks.

Hi Aaron

I will be living in the USA for one year. Does it make sense for me to:

I do wonder if the FCY and forex exchange rate might make earning miles this way not worth it!

thanks Aaron, great website!

Dude if you’re staying in the USA I’d totally see if I could get my hands on some us credit cards! Otherwise I suppose you could continue with amaze and wwmc, and the strarwfy you’ve described sounds fine too. But take note amaze only accepts mc

Thanks Aaron for the quick reply! Are USA 🇺🇸 issued credit cards 💳 better in terms of mile accruals than Singapore ones?? If so I really gotta go check those out!

Hi Aaron. Thanks for the informative post. What do you suggest for online foreign currency denominated bookings for overseas hotel (usually through aggregators eg booking.com)? Should I be looking at Amaze+Citi Rewards or just DBS WWMC (as Citi Reward excludes travel)?

Amaze + WWMC

Hi, thanks for the wonderful summary! I noticed that the UOB Prvi Miles also offers 6 miles per dollar for airlines and hotel spend. Therefore technically for those paying for hotel wedding banquets, that could perhaps be the best card to use (as compared with the other 4 miles per dollar cards e.g. UOB LADY – Travel Category)

Thanks Aaron, This is a great article! I have 2 questions A. What should be the strategy for a Dior / Hermes handbag that I purchase overseas in FCY (but around ~10K SGD equivalent) for at least 4mpd? Below is my strategy to use all physical cards for payment because I dont want to fumble and have to change to contactless/mobile payment for some cards for this big purchase. When I split across the physical cards for payment, I am thinking in priority: 1. OCBC Titantium rewards (I am applying for new card) for 12K spend 2. UOB lady’s solitaire… Read more »

Hi Aaron,

Between the 4 cards, which 2 cards would you pick for daily spending? 1k-2k per month.

Would it be UOB PPV and HSBC revolution?

For low spenders, won’t the Instarem + Citi Rewards card cover almost everything except travel??

yup, that would certainly work if you spend <$1K per statemet month.

Hi Aaron,

Do you know if monthly telco payments are considered online transactions? (eg Singtel, M1, Starhub, myRepublic, etc)

yes if you pay online at their websites

Just wondering what are the type of contactless transactions that would be covered by UOB PPV but not HSBC Revo?

Total refusal from HSBC to waive my Visa infinite fee, or offer any miles upon payment so I think I will not renew.

Any recommendations for another card please? Especially looking for travel insurance and airport limos, I have the new Vantage card but that doesn’t include these.

https://milelion.com/2022/06/26/2022-edition-the-120k-credit-card-showdown/

this might be helpful.

Great overview, thank you!

Looks like I might be stuck paying HSBC for the combination I’m after 🙁

Hey Aaron (or anyone how knows the answer), Does the Citi Rewards card consider the FairPrice app payments as Online groceries ? If so, will I earn 4mpd while using Scan & Go in stores ?

Only if you pair it with Amaze, as using it at physical store is not eligible for the 4mpd

Hi can i ask if UOB Visa Signature and PPV can be counted as contactless if i use credit card authorisation form for a restaurant for my wedding?

nope.

Hi, I’m new to this points & miles game. My wife and I have an average spending of 2k a month. Initially, I was thinking to do Amaze+Citi Rewards combo for each of us. But I realised for the points to miles transfer, the names on the CC had to match the name of the individual Krisflyer accounts (or any other travel loyalty programme accounts). That means we can’t pool our Citi points to 1 krisflyer account. What’s usually the set up for a family trying to collect points/miles.

Hi Aaron, thanks for this – this was super useful!

I wanted to ask, what do recurring payment for gym memberships fall under? Would it be Online transactions?

Hi Aaron,

Happy Early New Year!

When would u be posing your 2023 credit card strategy? Thanks!

Aaron, I need to pay Advertising cost 50-100k (FB, Google,..) every month. Which is the best card strategy for this?