Here’s the MileLion’s review of the BOC Elite Miles Card, which is a good barometer for how long you’ve been collecting miles.

If you see this as nothing more than a punchline, then you clearly weren’t playing the game back in 2018 when — believe it or not — this was undoubtedly the best miles card in Singapore.

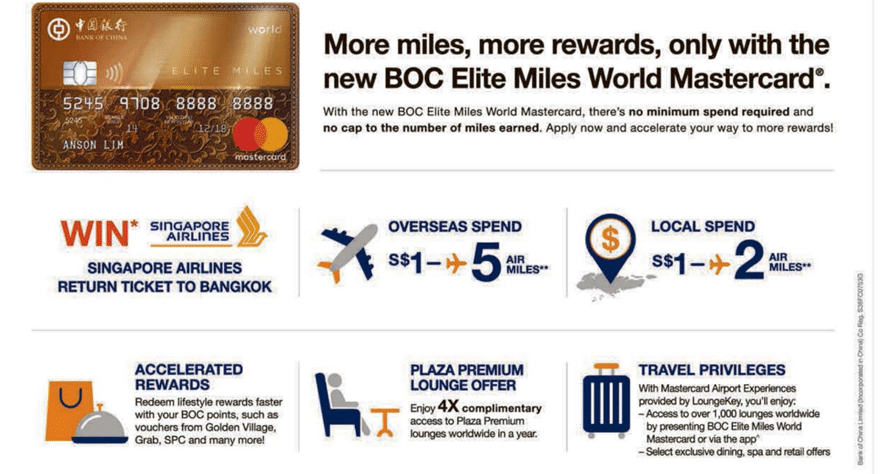

2 mpd on all local spend. 5 mpd on all foreign currency (FCY) spend. No minimum spend, no caps. Virtually no exclusions, not even for GrabPay and YouTrip top-ups. 4x Plaza Premium visits. What a time to be alive!

Those earn rates were part of a limited-time launch promotion, but even at the regular 1.5/3 mpd (local/FCY), the BOC Elite Miles Card was a force to be reckoned with. It wasn’t perfect by any means — cardholders quickly learned that dealing with BOC meant having to navigate a litany of annoyances — but the returns were so good that many were willing to turn the other cheek.

Until one day they weren’t. In June 2020, BOC cut the earn rates to just 1/2 mpd (local/FCY), added numerous exclusion categories, and even devalued previously-earned BOC Points by increasing the cost of a block of miles!

The cardholder exodus was fast and furious, and the BOC Elite Miles Card quickly faded into irrelevance, where it remained until July 2025, when BOC revitalised it by boosting the earn rates to 1.4/2.8 mpd (local/FCY).

I know, I know. That’s a lot of figures to keep track of, but long story short, the BOC Elite Miles Card is competitive once again. It might even be the card for you — provided you’re willing to stomach BOC’s many annoyances.

|

|

| BOC Elite Miles Card | |

| 🦁 MileLion Verdict | |

| ☐ Take It ☑ Take It Or Leave It ☐ Leave It |

|

| What do these ratings mean? | |

| The BOC Elite Miles Card’s improved earn rates make it a competitive general spending option — provided you’re willing to stomach BOC’s many annoyances. | |

| 👍 The Good | 👎 The Bad |

|

|

| 💳 Full List of Credit Card Reviews | |

Overview: BOC Elite Miles World Mastercard

Let’s start this review by looking at the key features of the BOC Elite Miles Card.

|

|||

| Apply | |||

| Income Req. | S$30,000 p.a. | Points Validity | 12-24 months |

| Annual Fee | S$207.10 (FYF) |

Min. Transfer |

50,000 pts (10,000 miles) |

| Miles with Annual Fee |

N/A | Transfer Partners |

1 |

| FCY Fee | 3% | Transfer Fee | S$30.56 |

| Local Earn | 1.4 mpd | Points Pool? | No |

| FCY Earn | 2.8 mpd | Lounge Access? | No |

| Special Earn | N/A | Airport Limo? | No |

| Cardholder Terms and Conditions | |||

Do note that even though the card name features the word “Elite”, the BOC Elite Miles Card is a World Mastercard, and not a World Elite Mastercard. Therefore, you won’t enjoy privileges such as GHA DISCOVERY Titanium status, Avis President’s Club status, or complimentary FlexiRoam data packages.

How much must I earn to qualify for a BOC Elite Miles Card?

The BOC Elite Miles Card is an entry-level offering with a S$30,000 income requirement, the MAS-mandated minimum to hold a credit card.

How much is the BOC Elite Miles Card’s annual fee?

| Principal Card | Supp. Card | |

| First Year | Free | Free |

| Subsequent | S$207.10 | S$103.55 |

The BOC Elite Miles Card has an annual fee of S$207.10 for the principal cardholder, and S$103.55 per supplementary card. This is waived for the first year — unless you decide to pay it as part of a welcome offer (see below).

There is no automatic fee waiver in the second year, but as with all cards, you’re welcome to appeal for one.

Here’s where you need to be careful, because back in 2019, some cardholders were told that their fee waiver had been approved, only for BOC to quietly deduct 95,000 points (worth 31,667 miles at the time). I shouldn’t have to say this, but when customers ask for a fee waiver, they typically don’t mean “can you deduct my points instead”. It’s just sneaky, especially since the value of the points deducted was worth much more than the annual fee!

BOC later reduced the requirement for an annual fee waiver to 30,000 points (6,000 miles), and the latest set of T&Cs does not mention fee waivers at all, so I’m unclear what the current practice is.

What sign-up bonus or gifts are available?

The BOC Elite Miles Card may no longer be a laughingstock, but its welcome bonus is certainly amusing.

New-to-bank customers who get approved for a BOC Elite Miles Card from 1 April to 31 December 2026 will receive 10,000 bonus miles when they:

- Enter the promo code WELCOME26 during application

- Pay the first year’s S$207.10 annual fee

- Make a minimum spend of S$50 within 60 days of approval

| ❓ New-to-bank definition |

|

New-to-bank customers are defined as those who:

|

I hope you see the issue here. While the minimum spend is very low, this offer requires customers to pay the S$207.10 annual fee. You’re therefore buying miles at 2.07 cents each, which is ridiculously expensive given the alternatives.

I would much rather you apply through SingSaver instead, which is offering new-to-bank customers a first year annual fee waiver, plus a choice of one of the following gifts:

- S$10 cash

- S$15 Grab voucher

- 1,000 Max Miles

Yes, it’s not very generous compared to the S$400+ cash you can often get for signing up for a Citi credit card. But it’s certainly better than paying S$207.10 for 10,000 miles!

How many miles do I earn?

| 🇸🇬 SGD Spend | 🌎 FCY Spend | ⭐ Bonus Spend |

| 1.4 mpd | 2.8 mpd | None |

SGD/FCY Spending

The BOC Elite Miles Card’s earn rates have fluctuated over the years, but the current earn rates are:

- 7 BOC Points per S$1 spent in Singapore Dollars (1.4 mpd)

- 14 BOC Points per S$1 spent in FCY (2.8 mpd)

These are very competitive earn rates for a general spending card, as the table below illustrates.

| 💳 Earn Rates for General Spending Cards (Income Req: S$30K) |

||

| Cards | Local Spend | FCY Spend |

UOB PRVI Miles Card UOB PRVI Miles CardAMEX Mastercard Visa |

1.4 mpd | 3 mpd IDR, MYR, THB, VND 2.4 mpd All Others |

BOC Elite Miles Card BOC Elite Miles CardApply |

1.4 mpd | 2.8 mpd |

HSBC TravelOne Card HSBC TravelOne CardApply |

1.2 mpd | 2.4 mpd |

DBS Altitude Card DBS Altitude CardAMEX Visa |

1.3 mpd | 2.2 mpd |

OCBC 90°N Card OCBC 90°N CardMastercard Visa |

1.3 mpd | 2.1 mpd |

Citi PremierMiles Card Citi PremierMiles CardApply |

1.2 mpd | 2.2 mpd |

StanChart Journey Card StanChart Journey CardApply |

1.2 mpd | 2 mpd |

AMEX KrisFlyer Ascend AMEX KrisFlyer AscendApply |

1.2 mpd | 1.2 mpd |

KrisFlyer UOB Credit Card KrisFlyer UOB Credit CardApply |

1.2 mpd | 1.2 mpd |

AMEX KrisFlyer Credit Card AMEX KrisFlyer Credit CardApply |

1.1 mpd | 1.1 mpd |

What is the FCY fee?

The BOC Elite Miles Card is especially compelling for FCY spend because BOC charges a 3% FCY transaction fee, slightly lower than the rest of the market.

| 💳 FCY Fees by Issuer and Card Network |

||

| Issuer | ↓ MC & Visa | AMEX |

| Standard Chartered | 3.5% | N/A |

| American Express | N/A | 3.25% |

| Citibank | 3.25% | N/A |

| DBS | 3.25% | 3.25% |

| HSBC | 3.25% | N/A |

| Maybank | 3.25% | N/A |

| OCBC | 3.25% | N/A |

| UOB | 3.25% | 3.25% |

| BOC | 3% | N/A |

| CIMB | 3% | N/A |

This means that using your BOC Elite Miles Card overseas represents buying miles at an attractive rate of 1.07 cents each. In fact, this is the best uncapped FCY earn rate available on a S$30,000 card, once you adjust for the FCY fee.

| 💳 FCY Earn Rates by Card (For cards with uncapped earn rates only, and S$30K min. income) |

||

| Card | Earn Rate | CPM |

| BOC Elite Miles Card Apply |

2.8 mpd 3% fee |

1.07¢ |

| UOB PRVI Miles Card AMEX Mastercard Visa |

3 mpd IDR, MYR, THB, VND 2.4 mpd Other FCY 3.25% fee |

1.08¢ IDR, MYR, THB, VND 1.35¢ Other FCY |

Maybank Horizon Visa Signature Maybank Horizon Visa SignatureApply |

2.8 mpd* 3.25% fee |

1.16¢ |

| HSBC TravelOne Card Apply |

2.4 mpd 3.25% fee |

1.35¢ |

| *Min. S$800 spend per c. month, otherwise 1.2 mpd |

||

The main annoyance is that like UOB, BOC defines overseas spending as “transactions made at merchants with payment gateway outside of Singapore”. In other words, it’s not sufficient for the transaction to be in a currency other than SGD; the payment processing must be done outside of Singapore too.

This won’t be an issue for payments made when you’re physically outside of Singapore, but can be a problem for online spending. Fortunately, there’s a way of checking this before you make a transaction, which I’ve written about in the article below (the context of the article is UOB, but it’s equally applicable to BOC).

When are BOC Points credited?

BOC Points are credited when your transaction posts, which generally takes 1-3 working days.

How are BOC Points calculated?

The BOC Elite Miles Card used to have an extremely favourable rounding policy, where points were awarded down to the very last cent. This meant you would never lose points to rounding, regardless of transaction size.

However, BOC revised its calculations at some point. I have not been able to figure out the exact formula, unfortunately, but from what I can tell, rounding down your transaction to the nearest S$1 and multiplying by 7 (local) or 14 (FCY) gives you roughly the right amount.

For the full list of formulas that banks use to calculate credit card points, do refer to these articles:

What transactions aren’t eligible for BOC Points?

When the BOC Elite Miles Card first launched, rewards exclusions were non-existent. You could earn points on government transactions, utilities bills, charitable donations, even YouTrip or GrabPay top-ups!

Over the years, however, BOC progressively added exclusions which brought this card in line with the rest of the market. The full list can be found at Point 2.2 of the T&Cs, but the key ones to highlight are:

- Charitable donations

- Education

- Government services

- Hospitals

- Insurance premiums

- Real estate agents

- Utilities

Both CardUp and ipaymy are also explicitly excluded from earning points. BOC has provided some specific examples of excluded merchants below.

| Category | Examples |

|---|---|

| Cleaning, Maintenance, and Janitorial Services | Helpling, Sendhelper |

| Educational Institutions | Institute of Technical Education (ITE), NTU, NUS, SIM, SIT, SMU, SUSS, SUTD |

| Financial Institutions for Financial Services | AxiTrader, BANC DE BINARY, BANCDEBINARY.COM, CardUp, City Index, FOREX.COM, MONEYBOOKERS.COM, IC Markets, IG Asia, IGMarkets.com.sg, ipaymy, OANDA, Peppersone, Plus500, Revolut, Saxo Capital Markets/Saxo Cap Mkts Pte Ltd, SKRSKRILL.COM, SKRxglobalmarkets.com, SKYFX.COM |

| Government Services | ACRA, CPF, HDB Season Parking, ICA, IRAS, LTA, MOM, Town Council, URA |

| Hospitals | Farrer Park Hospital, Gleneagles Hospital, KK Women’s and Children’s Hospital, Mount Alvernia Hospital, Mount Elizabeth Hospital, National University Hospital, Parkway Shenton Hospital, Singapore General Hospital, Tan Tock Seng Hospital |

| Insurance Payments | AIA Insurance, AIG, AVIVA, AXA, Great Eastern, Manulife, MSIG Insurance, NTUC Income, Prudential, QBE Insurance, Sompo Insurance, TM Life Insurance |

| Money Transfer and Remittance Services | MoneyGram, Swiss Money Transfer, Western Union, Wise, WorldRemit |

| Prepaid Accounts and Payment Service Providers | AXS, EZ Link/EZ-Link/EZLINK, eNETS, HelloPay, MatchMove Pay, NETS FlashPay, SAM, SingTel Dash, Transit/TransitLink, YouTrip, Grab wallet top-ups, ShopeePay wallet top-ups |

| Real Estate Agents and Managers | ERA Singapore, MCST, RentHero |

| Utility Bill Payments / Other Payments | AXS, SAM payments, SP Services |

What do I need to know about BOC Points?

| ❌ Expiry | ↔️ Pooling | ✈️ Transfer Fee |

| 12-24 months | No | S$30.56 |

| ⬆️ Min. Transfer | ✈️ No. of Partners | ⏱️ Transfer Time |

| 50,000 BOC Points (10,000 miles) |

1 | 2-3 weeks |

Expiry

BOC Points are valid for 12-24 months, depending on when they were earned.

| Earned | Expiry |

| 1 Jul 2024 to 30 Jun 2025 | 30 Jun 2026 |

| 1 Jul 2025 to 30 Jun 2026 | 30 Jun 2027 |

| 1 Jul 2026 to 30 Jun 2027 | 30 Jun 2028 |

Points expiry takes place on 30 June each year, which means that in a worst case scenario, points could be valid for as little as 12 months (if they were earned on 30 June). However, points could be valid for as long as 24 months (if they were earned on 1 July).

Pooling

BOC Points do not pool across cards. You will need to pay a separate conversion fee for every points-earning card you hold.

Transfer Partners & Fees

BOC Points can be converted into KrisFlyer miles at a 5:1 ratio, with a minimum conversion block of 10,000 miles. Transfers to Asia Miles were previously offered, before being discontinued on 1 July 2025.

| Frequent Flyer Programme | Conversion Ratio (BOC Points: Miles) |

| 50,000 : 10,000 |

It’s worth noting that the conversion ratio was originally 30,000 BOC Points = 10,000 miles, but was devalued to 45,000 BOC Points = 10,000 miles on 15 June 2020, and then again to the current 50,000 BOC Points = 10,000 miles on 1 July 2025. It’s very rare to see a bank in Singapore devaluing transfer ratios, let alone twice, but BOC is not like most banks!

Each transfer costs S$30.56, and you can transfer a maximum of 10 blocks in a single transaction, i.e. 100,000 miles.

Why? Because BOC said so. There is absolutely no technical reason for this; it’s a pure money-grab on the part of the bank. 100,000 miles may sound like a lot, but if you’re redeeming long-haul premium cabin awards for more than one person, it really isn’t. For the record, BOC is the only bank in Singapore with such a policy.

That’s not the only frustration. To convert BOC Points to miles, you must fill up a PDF form and email it to cardservice.sg@bankofchina.com, because the bank lacks an online rewards portal.

What is this, the early 2000s?

Transfer Time

While most banks advise customers to wait up to 14 working days for conversions to be completed, that’s really more of a CYA kind of thing, and transfers are usually completed within 3-5 days at most.

In BOC’s case, they really mean it. Don’t expect speedy conversions with BOC. Points conversions take 14-21 working days to be completed, little surprise since the process is manual.

Other card perks

Annual “Spend and Earn” promotion

Since 2024, the BOC Elite Miles Card has run an annual “Spend and Earn” promotion, which offers cardholders the opportunity to earn bonus miles.

The first two editions were simply insane:

- 2024: Uncapped 7-8 mpd on overseas and online spend, dining, Singapore Airlines, Scoot, KrisShop and Pelago

- 2025: 7.4-8.8 mpd on overseas and online spend, dining, Singapore Airlines, Scoot, KrisShop and Pelago, capped at S$5,000 per month

These rates were really too good to be true, so it wasn’t a surprise when both promotions were pulled early. Still, if you had your card prepped and ready to go, you could have made some serious hay in that short period of time.

There is an indication that BOC might be scaling these offers back, however, as 2026’s Spend & Earn promotion was very disappointing. Cardholders who spent S$5,000 per month for three consecutive months received 50,000 bonus miles — but only the first 50!

It remains to be seen if BOC decides to run an additional Spend & Earn promotion this year, but I’m not hopeful.

BOC SmartSaver bonus interest

Spending on the BOC Elite Miles Card is eligible to earn bonus interest on the BOC SmartSaver account.

Cardholders will earn bonus interest of up to 0.9% p.a. if they spend S$2,500 or more on their card each month.

| Monthly Spend | Bonus Interest |

| S$2,500 and above | 0.90% p.a. |

| S$750 to S$2,499.99 | 0.60% p.a. |

The bonus interest is capped on a balance of S$100,000, so this has the potential to yield an extra S$75 of interest each month. Not exactly life-changing, but if you’ve decided to bank with BOC anyway…

BOC customer experience

It’s rare that I need to add a section like this to a credit card review, but BOC has a well-deserved reputation of being difficult to deal with.

I mean, their internet banking interface looks like something from the early 2000s, complete with SimSun-esque fonts and menus that were obviously machine-translated. I don’t know if this is still the case, but during my first stint with the bank in 2018, you had to visit a BOC bank branch to register for internet banking access. Then, when your credit card came, you had to go down again to link it!

That said, I’m going to give credit where it’s due. BOC has improved certain aspects of its customer experience — though others are still lacking.

Processing times

When the BOC Elite Miles Card first launched, applications were only accepted through paper forms, and the processing time often stretched over several months. When my wife misplaced her card in July 2019, it took 36 working days to get a replacement!

Fortunately, it looks like things have improved. BOC now has a dedicated online platform for card applications, complete with SingPass integration. When I applied for this card in October 2025, I received an approval notification within three days, and the physical card within a week.

eGIRO payments are supported

It’s hard to believe that even though eGIRO launched in November 2021, none of the major banks have adopted it for credit card payments yet.

But BOC has, and I was able to set up GIRO payment for my BOC Elite Miles Card through my DBS bank account in a matter of minutes.

There’s a functional (ish) mobile banking app

BOC previously offered desktop-only internet banking, but it now has an app that lets you do pretty much everything the desktop platform does.

That said, it’s hypersensitive about what other apps you have installed (which banking app isn’t these days?) and getting a lot of 1-star reviews from people saying it refuses to work if it detects legitimate apps like antivirus, Tasker and Nova Launcher. I had to guess and check which app to delete until I figured it didn’t like my Parallel Space app cloner.

It also doesn’t let you take screenshots, which is annoying.

Digital card support

BOC currently does not support Apple Pay, Google Pay or Samsung Pay, and I see no signs that’s going to change anytime soon.

This means that engaging a “player 2” to help accumulate spending is trickier, since your card can’t be in two places at once. You’ll instead need to apply for a supplementary card, and I don’t know how long that will take to process.

Other shenanigans

For the sake of full disclosure, it’s worth reading through some of the issues that cardholders have previously encountered with BOC relating to annual fee waivers and interest charges.

These were from the pre-COVID days, so I hope they’ve been sorted out by now…though with BOC, you never know.

Summary Review: BOC Elite Miles Card

|

|||

| Apply | |||

| 🦁 MileLion Verdict | |||

| ☐ Take It ☑ Take It Or Leave It ☐ Leave It |

The BOC Elite Miles Card can be a competitive general spending card, especially if you use it exclusively for FCY spending, where it earns an uncapped 2.8 mpd with no minimum spend and a lower-than-average 3% FCY fee. These earn rates can be further buffed by the annual Spend and Earn promotion, though they usually turn out to be rather short-lived!

But you won’t earn miles on CardUp or ipaymy. There is only one frequent flyer partner. You will need to pay multiple conversion fees if you’re transferring more than 100,000 miles. The conversion times will be measured in weeks, not days. And of course, you’ll have to put up with BOC’s antiquated, Kafkaesque systems which sometimes seem designed by Marquis de Sade himself.

Is it worth it? Only you can decide. For what it’s worth, I personally reapplied for this card in October 2025, in order to take advantage of the ongoing Spend and Earn promotion. I haven’t touched the card outside of this, and since BOC’s welcome gifts are rather underwhelming, I don’t see the need to cancel it to reset my new-to-bank status either.

So that’s my review of the BOC Elite Miles World Mastercard. What do you think?

I am surprised you even marked 1.5 for this trash.

I cash out all my points and cancelling it now~

just by seeing it now makes me sick~

More like 0.5 stars. But I have to give credit to the CSO who noted that after transferring the maximum points to KF, I still had enough points for a FairPrice voucher. She converted the balance points for me and I duly received the voucher. But everything else about BOC sucks big time. Not worth the energy.

1 star is the lowest rating on the scale, actually…but maybe this card warrants a new scale 🙂

The BOC Elite Miles World Mastercard scale?

I like the Harvey Dent reference thrown in

Under the Shenanigans section, you forgot to add that their transaction SMS alerts are arbitrarily set at $100 to trigger, this threshold can’t be reduced, because BOC is too cheapskate to pay for more SMS alerts triggered by lower amounts.

I am dumping both the card and SmartSaver account. What is a good alternative to credit my salary?

DBS Multiplier

True. There is alternative and no need to keep BOC account or card anymore.

When this card was launched, BOC has the best cashback card (Family Card) and general spending card (Elite Miles). Then BOC changed T&C three times a year for Family card making me cancel it and now the same thing happens to Elite Miles…0 star for BOC

Neither an “elite” nor “miles” card. No longer the same card as when it first launched despite the name

hahahaha … this is the funniest card on the market.. i am suprised you even bother to write a review on this card.. the best part is …even if any BOC staff / management reads this .. they wont change or do anything about it… if you get a chance you should really ask them what is the exact purpose of this card? who are they trying to target.. this by far is the funniest card there is… i am so curious as to the actual purpose of existence of this card .. if only they had great online earn… Read more »

🎶 if you like the way you look that much oh baby you should go and love yourself🎵

I dealt with it years ago. If you think going to the branch physically is bad enough? I would tell you no, it can be much worse. I came down to their branch to change my address and it didn’t reflect in the system. It took me another month or so to call them multiple times to get it changed until I decided enough is enough! I closed the account for good! And guess what, I think I received some letter from it eventually to my correct address saying that my account is closed. What a trash bank.

Based on the above review , why would anyone even consider BOC banking in general ?

Definitely, LEAVE IT!!