If you want to give a spouse or family member a credit card for spending, there are two ways of going about it. The first is to pass them your physical card, or add it to their mobile wallet. The second is to apply for a supplementary card in their name.

Option 2 is by far the safer (and “proper”) way of doing things. Not only can you set a separate credit limit for the supplementary card, its transactions will be neatly compiled into a separate billing statement, making reconciliation a lot easier. A supplementary card may also allow you to share certain benefits, such as GHA Titanium status or complimentary FlexiRoam data packages with World Elite Mastercards.

But it’s a different story with Standard Chartered (SC), because believe it or not, an SC supplementary card has exactly the same card number, expiry date and CVV as the principal card!

This isn’t a particularly recent development, mind you. It’s been the case for some time now that an SC supplementary card is basically the principal card, with a different name printed on it. And it’s not just an amusing little quirk, because it creates a host of real-world problems…

The problem with Standard Chartered supplementary cards

The fact that SC supplementary cards share the same details as principal cards gives rise to issues with security, benefits, and day-to-day usability.

You can’t set a separate credit limit

It is not possible to set a separate credit limit for an SC supplementary card. Whatever the credit limit is for the principal card, so too will it be for the supplementary.

Replace one, replace all

If the supplementary card is lost, damaged, or gets hit with fraudulent transactions, then all supplementary and principal cards need to be replaced.

Block one, block all

If you place a temporary block on a supplementary card, then all supplementary and principal cards will be blocked too.

No SC EasyBill

As you may already know, SC EasyBill is now capped at one payment per category per month. Unfortunately, getting a supplementary card doesn’t bypass this restriction, as supplementary cardholders aren’t eligible to use SC EasyBill.

Oddly enough, this does not affect the SC Income Tax Payment Facility, which can be used by both principal and supplementary cardholders.

Supplementary cardholders can’t enjoy certain privileges

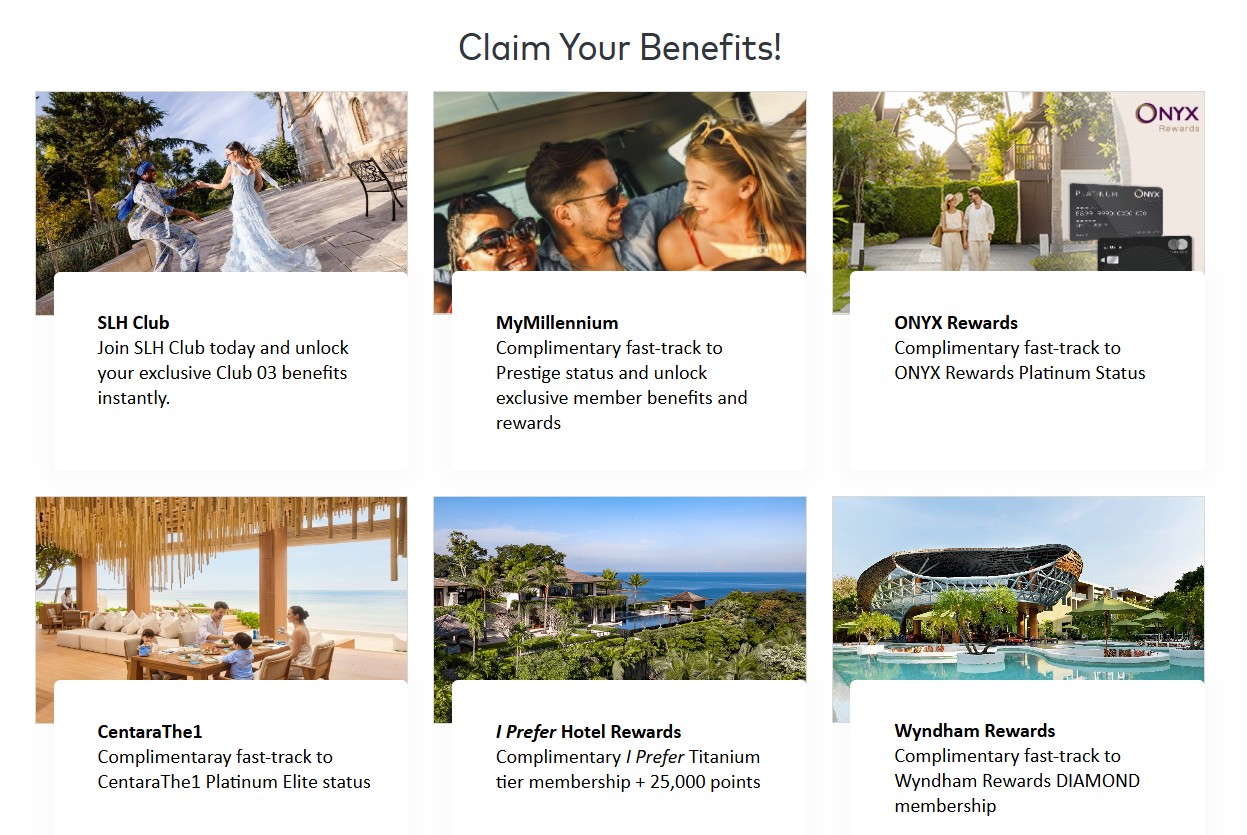

If you’re an SC Beyond Cardholder, you might want to share World Elite Mastercard benefits with family members through supplementary cards.

| 🏨 Hotel Elite Status |

|

| 🚗 Rental Car Elite Status | |

| 👍Other Perks |

However, there’s a problem. To claim the hotel elite status benefits, you need to create an account on the Mastercard Redemption Portal and generate a redemption code, or click on a special tokenised link.

If you’ve already registered the principal card under one account, you will get an error message (“This card is registered, please login to your existing account”) when you try to register the supplementary card under a second account. I guess even Mastercard thought that no bank would be dumb enough to generate cloned cards!

Moreover, the complimentary annual 3GB FlexiRoam package is issued based on card number, so it will not be possible for the supplementary cardholder to redeem this benefit if the principal cardholder has already claimed theirs.

| ❓Workarounds? |

|

For the hotel fast-track benefits, MyMillennium, ONYX Rewards, CentaraThe1, I Prefer, Wyndham Rewards and Brilliant by Langham require you to generate a code from the Mastercard Redemption Portal. You can only generate one code per card account, which rules out the supplementary cardholder getting a code of their own (I assume the codes are one-time-use only, but you never know…). However, SLH, Swiss-Belexecutive and GHA DISCOVERY work differently. The Mastercard Redemption Portal generates a link that sends you to the sign-up page (with a unique token appended to the URL). I don’t see how the system would know that someone already successfully signed up, so I suppose you could try to share that URL with your supplementary cardholder. I am not aware of any workaround for the FlexiRoam data package. |

Potential issues with lounge access

I came across a complaint from a SC Beyond Cardholder, who claimed he was denied entry to an airport lounge when attempting to enter with his wife, a supplementary cardholder. The reason? The agent said the card numbers were duplicates.

While the lounge agent was clearly wrong here, I can understand how things must have looked from her point of view. Normally, you wouldn’t expect two cards to share the same card number, expiry date and CVV, so it could easily raise suspicions.

Of course, this is a bit of an unfortunate situation. Lounge agents are usually too busy to scrutinise card details, but as this case shows, if they do take a closer look, you might have some explaining to do.

Transactions are all aggregated in one statement

SC does not differentiate between transactions made by the principal and supplementary cardholder(s). Instead, all spending is posted to the principal cardholder’s account, with no indication of who was responsible for what.

If the supplementary cardholder were to log in to the SC mobile app, they would not be able to see their transactions either.

Why does Standard Chartered do things this way?

This is a highly unusual arrangement, to say the least. Every other bank in Singapore issues supplementary cards with unique card numbers and CVVs — as they should!

Why does SC do things this way? I can only guess that it reduces operational complexity, since everything rolls into a single billing statement. On the other hand, I’m sure it also creates security risks, because the CVV is supposed to be unique per card. Having what basically amounts to clones of the principal card increases the attack surface, by increasing the risk of exposure of that single credential.

| ❓ How do OTPs work? |

|

If both the principal and supplementary cards have the same card details, who gets the OTP when an online transaction is made? Apparently, what happens is that after you enter your card details, the first step of the SC’s OTP process asks you if you’re a principal or supplementary cardholder. If you select the latter, you’ll be further prompted to enter the name, so the OTP can be routed to the right person. |

So I’d love to hear from someone who knows more about how these things work: is there a justifiable case for what SC is doing?

| 💬 Statement from Standard Chartered |

|

A Standard Chartered spokesperson has provided the following statement. We acknowledge the feedback and are actively reviewing it as part of our ongoing commitment to service excellence. Card benefits are generally designed around the principal card relationship. For Beyond Credit Card, we offer unlimited lounge access to both principal and supplementary cardholders. (Other banks may charge a fee for supplementary cardholders or impose a cap on complimentary lounge access.) For the example cited in your recent article, both the principal and supplementary cardholder should have been able to access the lounge. We will take this feedback to the lounge provider. |

Conclusion

Standard Chartered’s supplementary cards share the exact same card number, expiry date and CVV as the principal card.

This odd arrangement gives rise to numerous complications in day-to-day usage, from an inability to set spending controls and track individual transactions, to security risks and even awkward situations when accessing benefits or services that expect each card to be uniquely identified.

While it might simplify things on the bank’s end, it ultimately feels like a design that prioritises operational convenience over cardholder experience. And if supplementary cards are basically clones of the principal, what’s the point of getting one?

This isn’t a SG only arrangement, StanChart has been doing this exact same nonsense for years globally now.

I did in fact ask once why it’s like this, and they said that they really have one system that they run in every market, and this is a restriction coming from there.

Now, you can’t add a supplementary card to Apple Pay without the primary cardholder calling the Support Center to get approval.

They told me that it’s a fraud prevention measure. More and more difficult to just get things done . Great.

a better fraud prevention measure would be to issue unique supp cards!

i got supp cards from my parents in states. the supp cards are exactly the same as the main card (except name) for both BofA and Chase…

it also means you can’t add the supplementary card to SimplyGo to pool the transactions under one account for the Smart credit card rebate. Have terminated the card after this nonsense and the discontinued no minimum spend.

Chase in the US does this too, so it’s not unique to SCB

interesting…

https://thepointsguy.com/news/unique-numbers-authorized-users/

If travelling together, for PP usage, the main card holder must be the first person to clock in before the sup card when redeeming restaurants visits. PP seems to block and inform that the same card was just used when the order of signing in is sup card followed by main card.