The UOB Visa Infinite Metal Card is the spiritual successor to the original UOB Visa Infinite Card, which became Singapore’s first-ever Visa Infinite card when it launched in September 2003.

For many years, this was an underwhelming product. But in June 2023, UOB revamped the card by improving the earn rates and adding unlimited lounge visits for the cardholder and a guest, making it a viable alternative to other S$120K cards like the Citi Prestige.

Unfortunately, it looks like the pendulum has swung back in the other direction. Recent months have seen scaled-down welcome offers and the removal of key benefits— most notably unlimited lounge access. Unless you have very specific use cases — like needing to earn miles on education spending — I believe there are better alternatives out there.

UOB Visa Infinite Metal Card UOB Visa Infinite Metal Card |

|

| 🦁 MileLion Verdict | |

| ☐ Take It ☐ Take It Or Leave It ☑ Leave It |

|

| What do these ratings mean? |

|

| With cuts to lounge access and other benefits, the UOB Visa Infinite Metal Card feels far less compelling these days — unless perhaps you need to pay school fees. | |

| 👍 The good | 👎 The bad |

|

|

| 💳 Full List of Credit Card Reviews | |

Overview: UOB Visa Infinite Metal Card

Let’s start this review by looking at the key features of the UOB Visa Infinite Metal Card

|

|||

| Apply | |||

| Income Req. |

S$120,000 p.a. |

Points Validity |

2 years |

| Annual Fee |

S$654 |

Min. Transfer |

5,000 UNI$ (10,000 miles) |

| Miles with AF | 25,000 | Transfer Partners | 3 |

| FCY Fee | 3.25% | Transfer Fee | Waived |

| Local Earn | 1.4 mpd | Points Pool? | Yes |

| FCY Earn | 2.4 mpd | Lounge Access? | Yes |

| Special Earn | N/A | Airport Limo? | No |

| Cardholder Terms and Conditions | |||

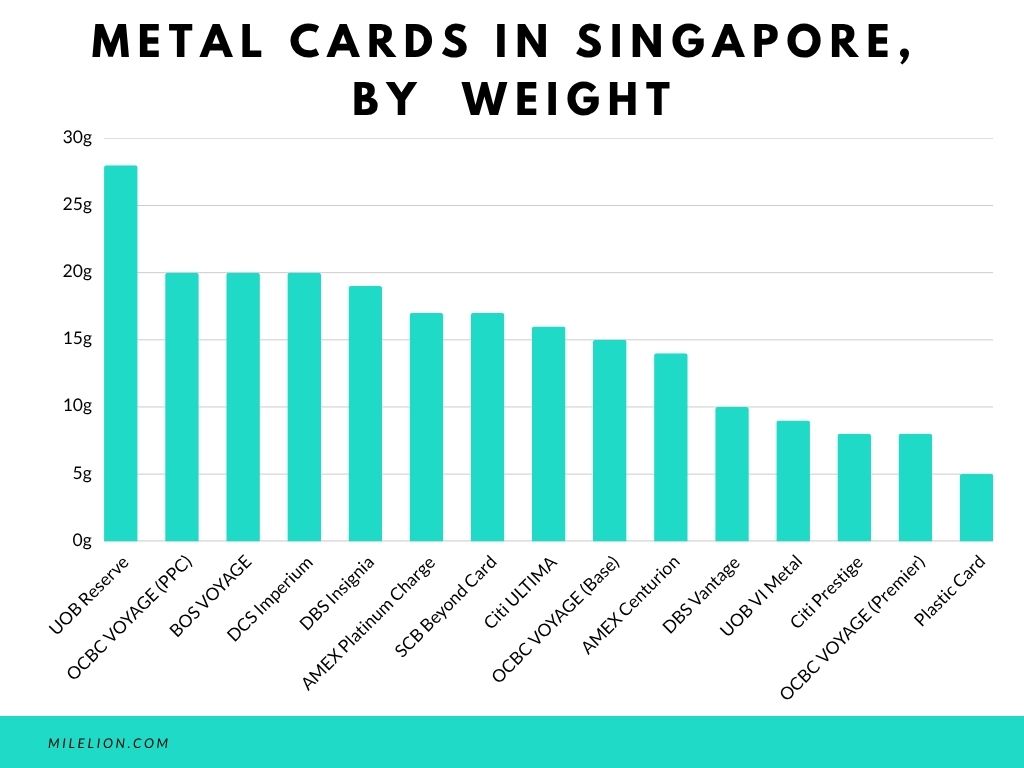

The UOB Visa Infinite Metal Card, as the name proudly reminds you, is made out of metal. However, it’s one of the lighter metal cards on the market, and only marginally heavier than a standard plastic card.

Despite this, you should be aware that UOB is the only bank (other than OCBC) to charge for replacement metal cards. Should you lose your UOB Visa Infinite Metal Card, you’ll pay a S$150 replacement fee.

UOB issues a total of five Visa Infinite cards, which are easy to confuse with each other. The table below summarises the relative positioning.

| Card | Description |

UOB Reserve Diamond Card UOB Reserve Diamond CardT&Cs |

|

UOB Reserve Card UOB Reserve CardT&Cs |

|

UOB Privilege Banking Card UOB Privilege Banking CardT&Cs |

|

UOB Visa Infinite Card UOB Visa Infinite CardT&Cs |

|

UOB Visa Infinite Metal Card UOB Visa Infinite Metal CardT&Cs |

|

How much must I earn to qualify for a UOB Visa Infinite Metal Card?

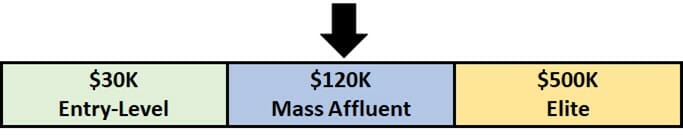

The original UOB Visa Infinite was labelled “an exceedingly-exclusive card for the mega-rich”, and required a minimum income of S$350,000 (equivalent to S$546,000 today after adjusting for inflation).

Thankfully, the UOB Visa Infinite Metal Card has a much broader appeal, available to anyone who earns at least S$120,000 per year. This was previously set at S$150,000, but was lowered in 2023.

As far as I know, it’s not possible to apply for a secured version of this card. If you’re asset rich but income poor, you might be directed to the UOB Privilege Banking Visa Infinite instead (minimum AUM S$350,000).

How much is the UOB Visa Infinite Metal Card’s annual fee?

| Principal Card | Supp. Card | |

| First Year | S$654 | 1st card free, 2nd onwards S$293.38 |

| Subsequent |

The UOB Visa Infinite Metal Card has an annual fee of S$654, which is strictly non-waivable. The first supplementary card is free for life; the second card onwards costs S$293.38 per year.

Cardholders receive 25,000 miles each year the annual fee is paid. That’s a fairly unattractive 2.61 cents per mile, but depending on your annual spending, you may be eligible for an extra 15,000 miles or 25,000 miles when you renew (more on that later).

Moreover, it’s insufficient to look at cost per mile alone, as we need to factor in the value of the other card benefits as well.

What sign-up bonus or gifts are available?

Customers who apply and receive approval for a UOB Visa Infinite Metal Card between 1 January and 30 June 2026 will be eligible to receive up to 60,000 bonus miles, as shown in the table below.

| New customers | Existing customers | |

| Pay S$654 annual fee | 25,000 miles | 25,000 miles |

| Spend S$4,000 within 30 days of approval | 35,000 miles | 15,000 miles |

| Total | 60,000 miles | 40,000 miles |

Cardholders must pay the S$654 annual fee and spend at least S$4,000 within 30 days of approval. Unlike most UOB sign-up offers, there is no cap on the number of eligible applicants.

Given the S$654 annual fee, you’re basically paying 1.09 cents (new) or 1.64 cents (existing) per mile. It’s a decent price for new customers, though it’s worth remembering that once upon a time, the offer used to be 80,000 miles + S$200 Grab vouchers!

Bonus miles are awarded on top of the regular base miles, so if you spent the entire S$4,000 on local spend at 1.4 mpd, you’ll receive a total of 65,600 miles (new) or 45,600 miles (existing).

How many miles do I earn?

| 🇸🇬 SGD Spend | 🌎 FCY Spend | ⭐ Bonus Spend |

| 1.4 mpd | 2.4 mpd | None |

SGD/FCY Spending

The UOB Visa Infinite Metal Card earns:

- UNI$3.5 for every S$5 spent in SGD (1.4 mpd)

- UNI$6 for every S$5 spent in FCY (2.4 mpd)

Compared to the rest of the S$120K pack, these are very solid earn rates. However, UOB has S$5 earning blocks, which means your actual earn rate could be lower, especially on small transactions (more on that later).

| 💳 Earn Rates for S$120K Cards (Sorted by Sum of Local and FCY Earn Rates) |

||

| Card | Local | FCY |

StanChart Visa Infinite StanChart Visa InfiniteApply |

1.4 mpd# | 3 mpd# |

Maybank Visa Infinite Maybank Visa InfiniteApply |

1.2 mpd | 3.2 mpd@ |

| UOB Visa Infinite Metal Card Apply |

1.4 mpd | 2.4 mpd |

DBS Vantage Card DBS Vantage CardApply |

1.5 mpd | 2.2 mpd |

OCBC VOYAGE OCBC VOYAGEApply |

1.3 mpd | 2.2 mpd |

Citi Prestige Card Citi Prestige CardApply |

1.3 mpd^ | 2 mpd^ |

HSBC Visa Infinite HSBC Visa Infinite |

1 mpd | 2 mpd |

AMEX Platinum Reserve AMEX Platinum ReserveApply |

0.57 mpd | 0.57 mpd |

| #With minimum S$2K spend per statement month. Otherwise 1 mpd for both @With minimum S$4K spend per calendar month. Otherwise 2 mpd ^Additional 0.02 to 0.12 mpd awarded based on tenure with bank |

||

What is the FCY transaction fee?

All overseas transactions are subject to a 3.25% fee, so using your UOB Visa Infinite Metal Card overseas is equivalent to buying miles at 1.35 cents each.

| 💳 FCY Fees by Issuer and Card Network |

||

| Issuer | ↓ MC & Visa | AMEX |

| Standard Chartered | 3.5% | N/A |

| American Express | N/A | 3.25% |

| Citibank | 3.25% | N/A |

| DBS | 3.25% | 3.25% |

| HSBC | 3.25% | N/A |

| Maybank | 3.25% | N/A |

| OCBC | 3.25% | N/A |

| UOB | 3.25% | 3.25% |

| BOC | 3% | N/A |

| CIMB | 3% | N/A |

Unfortunately, there’s a quirk here. While other banks define overseas transactions simply as those charged in currencies other than Singapore Dollars, UOB further requires that the payment gateway be overseas. As per the T&Cs:

For the avoidance of doubt, card transactions made overseas but effected/charged in Singapore dollars and online transactions effected in Singapore dollars or in foreign currencies at merchants with payment gateway in Singapore will not be treated as overseas transactions and will earn UNI$3.5 per S$5 spend

In other words, if you’re shopping on an online website which bills you US$100 (~S$140), but processes the payment within Singapore, you’ll earn miles at the local spending rate of 1.4 mpd.

For what it’s worth, this will only be an issue with online transactions; if you’re spending at brick-and-mortar stores overseas, you can rest assured you’ll receive the FCY earn rate so long as you’re not charged in SGD (watch out for DCC!).

To find out where a merchant’s payment gateway is located, follow the steps in the guide below.

Transaction date or posting date?

The UOB Visa Infinite Metal Card tracks spending based on the posting date, not transaction date.

If you’re accumulating spend towards your welcome bonus, be careful about making transactions towards the end of the qualifying period — anything that posts beyond the deadline will not be included, even if the transaction was made during the qualifying period!

Which cards track spending by transaction date vs posting date?

When are UNI$ credited?

UNI$ are credited when your transaction posts, which generally takes 1-3 working days.

How are UNI$ calculated?

Here’s how you can work out the UNI$ earned on your UOB Visa Infinite Metal Card

| Local Spend | Round down transaction to nearest S$5, then divide by 5 and multiply by 3.5. Round down to the nearest whole number |

| FCY Spend |

Round down transaction to nearest S$5, then divide by 5 and multiply by 6. Round down to the nearest whole number |

Unfortunately, UOB has one of the most punitive rounding policies in the game, which can adversely affect your earn rates especially on smaller transactions.

UOB first rounds your transaction down to the nearest S$5, divides it by 5, then multiplies the amount by 3.5 UNI$ (assuming it’s a Singapore Dollar transaction). This UNI$ figure is then rounded down again to the nearest whole number.

So imagine you spent S$9.99 on your UOB Visa Infinite Metal Card. You might figure that’s 14 miles (S$9.99 @ 1.4 mpd), but…

- The S$9.99 is rounded down to S$5

- S$5 is awarded 3.5 UNI$

- 3.5 UNI$ is rounded down to 3 UNI$

You actually earn 3 UNI$ (6 miles), an effective rate of just 0.6 mpd!

This is an extreme example, of course, and the effect of rounding gets smaller as your transaction size increases. But it’s exactly why you should think twice about using your UOB Visa Infinite Metal Card for small transactions that aren’t in S$5 blocks. In fact, the minimum spend required to earn miles is S$5.

| 🚆 What about SimplyGo? |

|

If the minimum transaction to earn miles is S$5, does this mean there’s no point using the UOB Visa Infinite Metal Card with SimplyGo? Don’t worry. For UOB Visa cards, fare charges are accumulated daily, but UNI$ are calculated based on the accumulated spend on SimplyGo Transactions per calendar month, and awarded to Cardmembers by the 7th calendar day of the following month. So with the exception of extreme circumstances (e.g. where you take just 1-2 rides a month), you’ll definitely earn some miles. |

This means that despite having a higher headline rate, you may earn fewer miles on the UOB Visa Infinite Metal Card than the Citi Prestige Card depending on transaction size. Consider the following:

| UOB VI Metal 1.4 mpd |

Citi Prestige 1.3 mpd |

|

| S$5 | 6 miles | 6.4 miles |

| S$9.99 | 6 miles | 11.6 miles |

| S$15 | 20 miles | 19.6 miles |

| S$19.99 | 20 miles | 24.8 miles |

| S$25 | 34 miles | 32.4 miles |

| S$29.99 | 34 miles | 37.6 miles |

If you’re an excel geek, here’s the formulas you need to calculate points:

| Local Spend | =ROUNDDOWN (ROUNDDOWN (X/5,0) * 3.5,0) |

| FCY Spend |

=ROUNDDOWN (ROUNDDOWN (X/5,0) * 6,0) |

| Where X= Amount Spent |

|

Don’t forget that UOB makes it easy to check your points breakdown thanks to the TMRW app, which will show transaction-level points for the UOB Visa Infinite Metal Card.

UOB TMRW: Get transaction-level credit card rewards points breakdowns

For the full list of formulas that banks use to calculate credit card points, do refer to these articles:

What transactions aren’t eligible for UNI$?

A full list of transactions that do not earn UNI$ can be found at point 1.5 of the T&Cs.

I’ve highlighted a few noteworthy categories below:

- Amaze (not that it matters in this case, as it was never possible to pair Visa cards with Amaze in the first place)

- Charitable Donations

- Government Services

- Hospitals

- ipaymy

- Prepaid account top-ups (e.g. GrabPay, YouTrip)

- Real Estate Agents & Managers

- Utilities

However, the UOB Visa Infinite Metal Card is somewhat unique among UOB cards in that it does not exclude education-related expenses from earning points. This alone could be a big selling point, since it’s almost impossible to find a decent miles-earning card for schools and tuition fees.

For the avoidance of doubt, CardUp transactions will earn miles with the UOB Visa Infinite Metal Card, at the usual rate of 1.4 mpd.

What do I need to know about UNI$?

| ❌ Expiry | ↔️ Pooling | ✈️ Transfer Fee |

| 2 years | Yes | Waived |

| ⬆️ Min. Transfer | ✈️ No. of Partners | ⏱️ Transfer Time |

| 5,000 UNI$ (10,000 miles) |

3 | 48 hours (KF) |

Expiry

UNI$ expire 2 years from the last day of each periodic quarter in which the UNI$ was earned.

For example, if any UNI$ earned in January 2024 will expire on 31 March 2026. This means that the validity could technically be up to 2 years 3 months in some cases.

Pooling

UNI$ pool across cards. If you have 10,000 UNI$ on the UOB Lady’s Card, and 5,000 UNI$ on the UOB Visa Infinite Metal Card, you can redeem 15,000 UNI$ in a single transaction.

It also means that you don’t need to transfer your UNI$ out before cancelling the UOB Visa Infinite Metal Card, assuming it’s not your last UNI$-earning card.

Transfer Partners & Fees

UNI$ transfer to frequent flyer programmes at a 1:2 ratio, with a minimum transfer block of 5,000 UNI$.

There are effectively only two partners available however (converting points to Air Asia is like throwing them away), which is somewhat limited compared to competitors like Citi, HSBC and OCBC.

| Frequent Flyer Programme | Conversion Ratio (UNI$: Partner) |

| 5,000 : 10,000 | |

| 5,000 : 10,000 | |

| 2,500 : 4,500 |

UOB Visa Infinite Metal Cardholders enjoy a waiver of the usual S$27 conversion fee. Moreover, since UNI$ pool, you can use the Visa Infinite Metal Card as a conduit to convert UNI$ earned on other UOB cards for free too.

Transfer Times

UOB transfers to KrisFlyer are typically completed within 48 hours. Do note that transfers to Asia Miles can take significantly longer; it’s good to budget up to three weeks.

If you need your points credited instantly, you can move them via Kris+ at a rate of 1,000 UNI$ = 1,700 KrisPay miles. KrisPay miles can then be instantly converted to KrisFlyer miles at a 1:1 ratio.

| S$5 for new Kris+ Users |

| Get S$5 (in the form of 500 KrisPay miles) when you sign-up with code W644363 and make your first transaction |

However, those 1,000 UNI$ would normally have earned you 2,000 KrisFlyer miles, so you effectively take a 15% haircut. Therefore I wouldn’t recommend taking this option, unless you need a small top-up to redeem a flight, or have an orphan UNI$ balance (<5,000 points).

If you choose to do so nonetheless, do remember that it’s a two-step process:

- Transfer UNI$ to KrisPay miles

- Transfer KrisPay miles to KrisFlyer miles

Do not forget the second step! If you wait more than 21 days, or spend any of the converted KrisPay miles via Kris+, the entire balance will be stuck in the Kris+ app. KrisPay miles expire after six months, and can only be spent at a poor ratio of 100 miles = S$1.

Other card perks

12 complimentary lounge visits

When the UOB Visa Infinite Metal Card first launched, it offered just four free lounge visits per membership year. That was woefully inadequate for its segment, so thankfully that was rectified in 2023, with cardholders upgraded to unlimited visits together with one guest.

Unfortunately, that benefit has now been cut to 12 visits per calendar year, effective 1 June 2026. These can be shared with one or more guests (e.g. you could bring 11 guests and use up your entire allowance in a single visit), and visits can be used for both lounge and non-lounge experiences (such as spa treatments and restaurants).

| 💳 Airport Lounge Benefits (Income Req.: S$120K) |

||

| Card | Free Visits (Per Year) |

|

| Main | Supp. | |

HSBC Visa Infinite HSBC Visa Infinite |

∞ | ∞ (up to 5x cards) |

| OCBC VOYAGE Apply |

∞ | 2 CY No Share |

| Citi Prestige Card Apply |

12 CY Share |

N/A |

| DBS Vantage Card Apply |

10 MY Share |

N/A |

| UOB Visa Infinite Metal Card Apply |

12 MY Share |

N/A |

| StanChart Visa Infinite Apply |

6 MY Share |

N/A |

| Maybank Visa Infinite Apply |

4 MY No Share |

N/A |

| AMEX Platinum Reserve Apply |

N/A | N/A |

| Legend | ||

| Whether visits are tracked by calendar year CY or membership year MY Whether lounge visits can or can’t be shared with guests Share No Share |

||

That said, it’s still a respectable allowance for its segment, given that the Citi Prestige has also removed unlimited lounge visits, and the HSBC Visa Infinite has been closed to new applications since September 2024.

Dining discounts

UOB Visa Infinite Metal Cardholders enjoy up to 30% off a la carte food orders at the following restaurants.

| Hotel | Venues |

|---|---|

| The Fullerton Hotel Singapore |

|

| The Fullerton Bay Hotel Singapore |

|

| The Ritz-Carlton, Millenia Singapore |

|

| Grand Hyatt Singapore |

|

| Pan Pacific Singapore |

|

| Pan Pacific Orchard |

|

| PARKROYAL COLLECTION Marina Bay |

|

| PARKROYAL on Beach Road |

|

| PARKROYAL COLLECTION Pickering |

|

| Sheraton Towers Singapore Hotel |

|

UOB Visa Infinite Metal Cardholders also enjoy the Infinite Dining programme, which offers specially-curated menus from celebrity chefs.

15,000 miles loyalty bonus

UOB Visa Infinite Metal Cardholders who spend at least S$100,000 in a membership year will receive 15,000 bonus miles when they renew their card for the following membership year. This is on top of the usual 25,000 miles awarded each year the annual fee is paid.

The bonus miles will be awarded two months after the annual fee is posted.

While extra miles are always good, 15,000 bonus miles for S$100,000 spend is not much of an incremental return. There’s really no reason why you should be putting so much spend on a general spending card in the first place (unless perhaps you’re charging school fees).

10,000 miles retention bonus (?)

This isn’t an official benefit, but cardholders have reported receiving 10,000 bonus miles as an additional incentive for renewal — on top of the regular 25,000 miles and published 15,000 miles loyalty bonus — though they will have to call up to request for it.

You can browse community-provided data points in the UOB Visa Infinite Metal Card Telegram Chat by searching for “10k”.

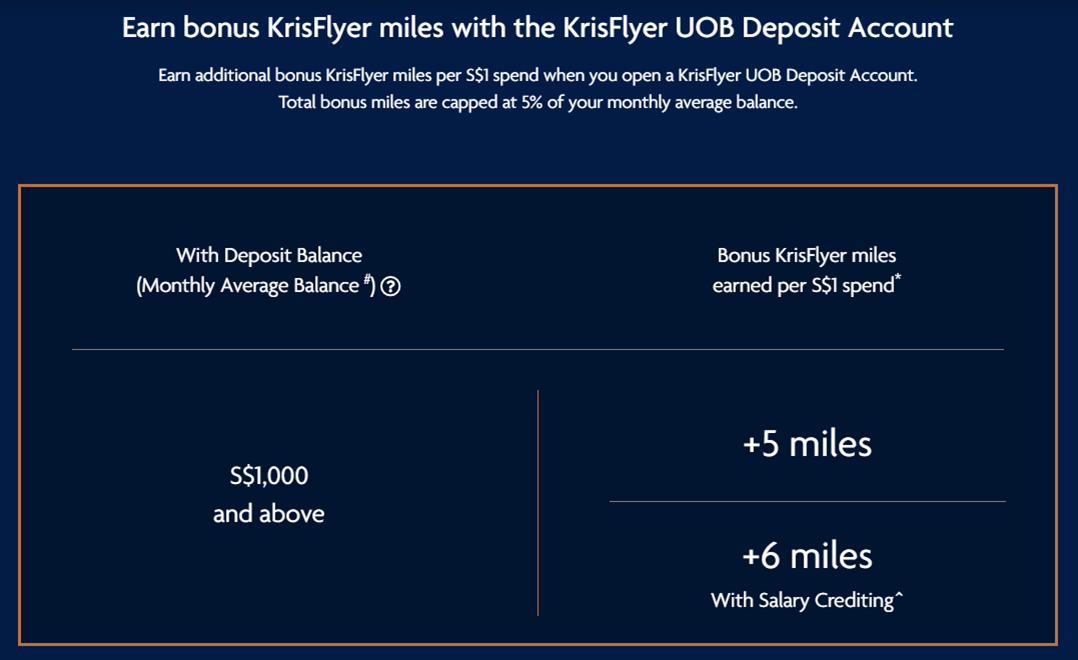

Bonus miles with KrisFlyer UOB Account

UOB Visa Infinite Metal Cardholders can earn bonus miles on their spending with a KrisFlyer UOB Account.

For example, if I spend on my UOB Visa Infinite Metal Card in SGD, I will earn:

- A base reward of 1.4 mpd from my UOB Visa Infinite Metal Card

- A bonus reward of 5-6 mpd from my KrisFlyer UOB Account

| Without Salary Crediting | With Salary Crediting | |

| UOB VI Metal Card | 1.4 mpd | 1.4 mpd |

| KrisFlyer UOB Account | 5 mpd | 6 mpd |

| Total | 6.4 mpd | 7.4 mpd |

| To unlock the salary crediting bonus, you must credit a minimum salary of S$1,600 to the KrisFlyer UOB Account |

||

However, I’d strongly advise against this, because the opportunity cost of the funds you need to deposit in the account would almost certainly outweigh the value of any miles earned. That’s mainly because the maximum miles you can earn each month are capped at 5% of your Monthly Average Balance (MAB).

For example, if your MAB is S$1,000 (the minimum required to earn miles), you can earn at most 50 miles (5% of S$1,000) from the KrisFlyer UOB Account each month. Assuming you don’t credit a salary (5 mpd), the account would stop rewarding you after spending just S$10 (50/5 mpd) on your cards!

| MAB | Monthly Cap (5% of MAB) |

Card Spending Cap | |

| No Salary Credit (5 mpd) |

With Salary Credit (6 mpd) |

||

| S$1,000 | 50 miles | S$10 | S$8.33 |

| S$10,000 | 500 miles | S$100 | S$83.33 |

| S$20,000 | 1,000 miles | S$200 | S$166.67 |

| S$50,000 | 2,500 miles | S$500 | S$416.67 |

| S$100,000 | 5,000 miles | S$1,000 | S$833.33 |

This means that unless you have a ridiculously high valuation for a mile, the opportunity cost is simply too high.

To learn more about the KrisFlyer UOB Account, and why it’s such a raw deal, refer to the post below.

Complimentary travel insurance

| Accidental Death | US$1,000,000 |

| Medical Expenses | N/A |

| Travel Inconvenience | Flight Delay: S$400 Baggage Delay: S$500 Lost Baggage: S$1,000 |

| Policy Wording | |

The UOB Visa Infinite Metal Card offers complimentary travel insurance to cardholders who charge their travel fares to the card (it’s unclear from the policy wording whether coverage applies in the case where an airline ticket is redeemed with miles and the UOB Visa Infinite Metal Card is used to pay for taxes and surcharges).

This provides up to US$1,000,000 of coverage for accidental death or dismemberment while traveling on a scheduled public conveyance, with further coverage also for travel inconvenience like lost luggage or flight delays.

However, there is no coverage for overseas medical expenses or evacuation, so you’ll definitely want to get separate protection there.

Buy miles with UOB Payment Facility

|

| UOB Payment Facility |

The UOB Visa Infinite Metal Card has a “no questions asked” Payment Facility that allows cardholders to buy as many miles as they wish.

The regular fee is 2.2 cents per mile, though there are frequent promotions which reduce this further. The current offer, which is set to lapse on 31 August 2026 (but likely to be further extended) lowers the cost to 1.8 cents per mile.

How it works is that cardholders fill out an online form and specify how much they’d like to charge to the facility, e.g. S$5,000. UOB will then:

- Deposit S$5,000 into their designated bank account

- Charge S$5,090 to their card (S$5,000 + 1.8% fee)

- Award UNI$ at a rate of UNI$2.5 per S$5, or 2,500 UNI$ in total (5,000 miles; the payment facility fee doesn’t earn miles)

Cardholders are then out of pocket S$90, for which they purchased 5,000 miles. This works out to 1.8 cents per mile.

1.8 cents per mile is slightly above what I would be willing to pay, given that cheaper alternatives exist with services like CardUp (maybe not for long) and Citi PayAll. However, those require a legitimate bill to pay, while the UOB Payment Facility does not.

The UOB Payment Facility would also come in useful if you need to top off your UNI$ balance to the next 5,000 UNI$ block required for a transfer.

Generic Visa Infinite benefits

UOB Visa Infinite Metal Cardholders enjoy the following additional perks, which are available to all Visa Infinite cards.

| 🏨 Hotel Elite Status | |

| 🚗 Rental Car Elite Status | |

| 👍Other Perks |

For more information on how these perks work, refer to the post below.

Summary Review: UOB Visa Infinite Metal Card

|

| Apply |

| 🦁 MileLion Verdict |

| ☐ Take It ☐ Take It Or Leave It ☑ Leave It |

The UOB Visa Infinite Metal Card remains one of the few options for earning miles on education-related expenses, and if you’re a heavy user of other UOB cards such as the UOB Lady’s Card, UOB Preferred Platinum Visa and UOB Visa Signature, then the UOB Visa Infinite Metal Card can anchor this strategy by providing a general spending option and free UNI$ conversions.

But even though the earn rates are competitive for a S$120K card, an entry-level UOB PRVI Miles Card could match or even outperform the UOB Visa Infinite Metal Card (it earns 3 mpd on IDR, MYR, THB and VND transactions)!

Moreover, it’s extremely painful to see the lounge benefit go from unlimited visits with one guest to just 12 per year, though to be fair, it does mirror the cuts to lounge privileges we’ve seen from the AMEX Platinum Charge and Citi Prestige.

Besides that, the slate of benefits feels very lightweight relative to its annual fee, with no airport limo rides or anything noteworthy beyond generic Visa Infinite perks. For my money, you might be better off getting a Citi Prestige instead.

So that’s my review of the UOB Visa Infinite Metal Card. What do you think?

Hi,

can you confirm if owning this card waives the transfer fee to Krisflyer?

i did transfer the miles to krisflyer yet I m still charged $25

i was under the impression that uob waives all transfer fees for visa infinite cards, based on this: https://www.uob.com.sg/assets/pdfs/personal/cards/rewardsplus_tnc.pdf Each transfer by the Eligible Person to his/her designated airline’s frequent flyer programme is subject to a S$25 conversion fee (or a conversion fee of such other amount as UOB may determine in its discretion), with the exception of UOB Reserve, UOB Visa Infinite and UOB Privilege Banking Cardmembers; and must be to a frequent flyer account bearing his/her own name. Each transfer must be in block of 10,000 miles It’d be strange if they waived it for the classic Visa… Read more »

Ok let me call the bank and update you,

also to let you know that owning this card entitles you to have access to privilege banking lounge i,e, privilege banking in Raffles Place etc.

i tried and was granted access

i am also thinking whether to keep this card coming renewal in sept. Just used this card to pay my income tax via card up haha, will have a few more months to think about it.

Just don’t care about the 25 dollar, just transfer and dump the card lah, after reading so much from this article, still want to hold it?

Haha yeah signed up impulsively last year. Coz there was some bonus miles for few k spending. But the promotion is over already. They gave free privilege banking lounge to try out as well.

when its up for renewal, may not keep it anymore ..

I used to hold this useless card. It is a really pretty card but that’s really all about it. I never used the useless Gourmet Collection once because I have The Entertainer and Amex Love Dining programme also offers far better discounts. The free transfer as per the terms that Aaron had quoted, do not apply for this card unfortunately.

thanks Raymond. have updated the post.

Hi Aaron, love the addition of the tl;dr and star rating sections to your credit card reviews! It would be awesome if you could add a page or table somewhere with the grouping of cards by star rating!

thanks christian! i need to figure out how to do that, will keep it in mind (as usual i’m hopeless with the tech side of things)

https://milelion.com/tag/card-review/

here’s where you can see all card ratings at a glance

Isn’t the SCB VI the highest earning $120K card? No longer issued, but still

all style, no substance

Thanks for another great analysis. Was contemplating to renew or cancel. Now it’s clear.

This is a very good article. Excellently written. Well done.

Hey Aaron, have you noticed that UOB has taken away the gourmet collection benefit from this card? I was checking this card just now but can’t find anything about this benefit any more, have you heard about anything about the changes of this card?

Thanks!

Hi Aaron, they’re now offering 3 nights stay with Accor as an alternative sign up benefit to the 25k miles. Do you think it’s worth the annual fee?

https://milelion.com/2022/01/12/uob-visa-infinite-metal-card-offering-accor-plus-membership-with-3-free-nights/

Seems there’s some updates to the benefits? There’s some golfing benefits now.

Seems like refuelling at shell also award uni$. I thought fuel station dont reward uni$ as it is stated clearly on shell website. Also if I remember correctly other cards dont award uni$ on phone bills but this card does, maybe I remember wrongly, Anyway, these could be additional perks for this UOB visa infinite card.

yes, shell transactions earn UNI$ despite what the T&Cs say (confirmed on other UOB cards too like the PPV, lady’s)

I currently have the UOB Metal Infinite Visa as my main credit card. I was thinking of canceling the metal card and switching to the UOB KrisFlyer Mastercard. However, I am aware that I won’t benefit from any new to bank sign up bonus. I will be using my card for every possible daily expense, shopping, dining, travel, etc. I travel every month via SQ. Would it make sense to keep both cards? Or just stick to one. If so, which card?

Hi,

do we know if the Dragon Pass benefit extends to sub card holders?

I also would like to know

No, only applies to main cardholders

UOB$ is UOB’s card-wide cashback programme and includes Cold Storage, Crystal Jade, Giant, Guardian, Starbucks and Toast Box, among others. For the full list, refer to this link.

the above link appears to be broken

will get that fixed, thank you!

UOB VI Metal excludes hospital bills wef 01 Oct 2024

See page 2 of

https://www.uob.com.sg/personal/cards/credit/visa-infinite/pdf/VI-Metal-Pdt-TnC.pdf

8062 Hospitals (wef 1 Oct 2024)

Thanks HST.

Oh man, one more reason to drop this card..

I just tried to cancel this card after holding it for about 6 months, but I was told by the CSO that there’s a minimum holding period of 12 months!

Anyone with the same experience? I looked through the T&C and can’t find any such clause.

CardUp can be used for qualifying spend?

Would like to know this as well. Also, can we pair with Kris+ app?

+1 same Q

iPaymy does have UOB Infinite crad as an option

If you do clock $100,000 on this card, you get additional 15,000 miles. This means overall a 1.55 (1.4 + 0.15) mpd, not too bad. If i have $100,000 of cardup expenses, other than this uob vim that gives 1.55 mpd, which card is a better option?

Confused over what is meant by lounge visit misuse.

Coming from someone who makes maybe only 2 flights out of Sg in a year.

It’s getting worst off, their insurance also useless, they make it almost impossible to claim, drop this card, it’s a no go for me if they decide to reduce to 12 complimentary passes, sounds terrific way to end this card

I hold secured uob credit cards, and was told to top up my fixed deposit to $30k to be able to get this card.

there’s another data point out there saying $50k min.

Hi Aaron, Just like to clarify on the write up of “Thankfully, that’s now been rectified, and cardholders now receive unlimited visits (+1 guest) to DragonPass lounges worldwide.” In fact, the benefit is provided by Airport Companion Program by Dragon Pass. The list of airport lounge in the Airport Companion App is different from that offered in Dragon Pass list of lounges. The list of lounges in Airport Companion App is limited and of poor experience. One example is Sapporo airport. It is not listed in the Airport Companion App while the Dragon Pass site shows there are two lounges… Read more »

Can this card be used for insurance premiums like how citi can utilise citipayall?

This card is like the older sibling of the UOB PRVI Miles, but without the latter’s handy 3mpd for regional spend and 5mpd Jun/Dec overseas spend promotions. Since the Visa variant of the PRVI is also a Visa Infinite, I’m not sure if it’s worth it to pay 2.5x more in annual fees for the Visa Infinite Metal just to get 8x more lounge access and waived transfer fees for KrisFlyer.

I just renewed it last month, paying the $654 renewal fee. I value the 250,000 miles at about $400, with the balance justified by the 0.2 cent savings on the UOB Payment Facility, unlimited free miles transfers, and 12 Priority Pass lounge visits. I’d love to hear from others who have also renewed the card, what made you decide to do so?

i believe you mean 25,000 miles, not 250,000 miles? the uob payment facility rate is currently the same for the uob prvi miles and uob vi metal card though.

Yes 25,000 miles 🫢

It’s unusual to see the same fees for the VI Metal and Prvimiles. If this becomes the norm I will reconsider cancelling it next year.