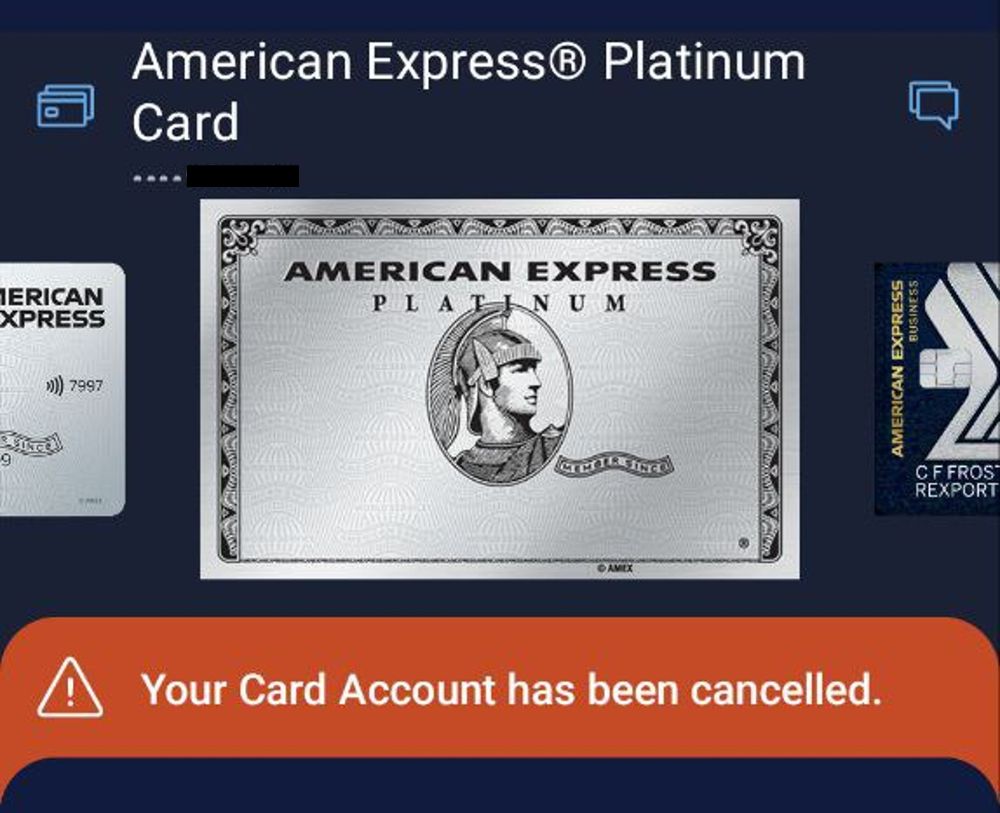

I got my AMEX Platinum Charge back in 2018, which means that to date, I’ve paid roughly S$12,000 in annual fees (technically, I used Membership Rewards points to pay the 2020 annual fee, but anyway…).

That’s a hefty sum for a credit card, but it’s given me some great experiences over the years, and I’ve been able to share its perks with family members through supplementary cards.

However, 2025 is when that all comes to an end, because I’ve decided against renewing for a further year.

The AMEX Platinum Charge was good while it lasted, but with its benefits dwindling and competitors stepping up their game, I’m just not convinced it’s pulling its weight for me anymore.

Why I’m not renewing my AMEX Platinum Charge

Why am I cancelling my AMEX Platinum Charge?

I blame it on what I call Platinum Anxiety — the feeling that you might not be getting a good enough return on the S$1,744 annual fee.

Of course, Platinum Anxiety exists with any expensive card. I’m sure there’s Beyond Anxiety, Reserve Anxiety, Insignia Anxiety, heck, probably even Centurion Anxiety. But Platinum Anxiety is particularly vexing, because the value you get from the AMEX Platinum Charge is, to a large degree, within your control.

This is a double-edged sword. On the one hand, there are some min-maxers out there who really squeeze every cent of value from their AMEX Platinum Charge, and then some (you should see the claw machine reports come Christmas).

On the other, the typical cardholder may not have the time nor inclination to do so. And as they read the stories of the min-maxers, or stare at the growing mountain of unused vouchers and soon-to-expire credits, they start to wonder: am I getting the short end of the stick? Should I be calling up customer service and negotiating for a better renewal offer, or doing wine runs to collect all my complimentary bottles, or monitoring the AMEX Experiences app for free events, or scheduling spa treatments to use the vouchers, or polishing my claw machine skills, etc. etc.

In my case, I feel I’ve transitioned from the first group to the second. There was a time when I had the energy to run around Singapore on some sort of AMEX Amazing Race, but these days things are different. And because so many of the benefits require active monitoring and participation, I don’t think this is a good card for me anymore.

Anyway, there are three main reasons why I’ve decided against renewing my card.

Benefits have been nerfed

Over the years, the AMEX Platinum Charge has lost some of the key benefits that made it worth paying for.

I’m going to list, in no particular order of merit, the nerfs that come to mind:

- American Express removed non-lounge airport experiences like restaurants and spas from its Priority Pass memberships (to be fair, this was a worldwide change, but it still affects how you value the card)

- The guest allowance for Plaza Premium Lounges was cut from two to one guest

- The first supplementary cardholder lost unlimited Priority Pass visits

- No more Avis President’s Club or Shangri-La Golden Circle Jade

- The AMEX Platinum Reserve lost its S$100 Tower Club voucher, and its Fraser Hospitality free stay was cut from two nights to one night

- The annual voucher pack has steadily declined in value

- There are fewer luxury options for the complimentary 1-night Plat Stay voucher (almost half of the current list are Fraser properties), the room entitlement has been downgraded in some cases, and breakfast is no longer offered at Singapore hotels

- Cardholders used to get 4x S$50 St. Regis dining vouchers, which had no minimum spend and could be stacked with Love Dining. Now, dining vouchers have many more strings attached, like minimum diners or maximum vouchers per visit.

- The Tower Club voucher was cut from S$100 to S$50

- Complimentary spa treatments have been replaced with cash vouchers requiring minimum spends

- Wine vouchers for Fairmont now require dining in with a main course

- The relatively easy-to-use hotel and airline credit was replaced with a complicated system of bi-annual statement credits (more on that in the next section)

I’m not denying there were bright spots along the way. I’ll always remember that, unlike many other so-called “premium” cards, American Express made a genuine effort during COVID to take care of its members. To compensate for the fact that many of its travel and dining couldn’t be used, AMEX stepped up with:

- S$500 and S$300 credits for groceries and food delivery in 2020 and 2021 respectively

- S$350 credits for dining in 2021

- a very generous double points and double statement credits campaign in 2020

- upsized value for paying the annual fee with MR points in 2020

Even outside of COVID, there were times where the card offered excellent value. For example, the transition from the old airline and hotel credits to the new Platinum Statement Credits created a one-time opportunity for cardholders to double dip on both in the same year. Then there was the addition of a Comoclub C5 membership which, for a period, was basically S$780 in extra value. And who could forget the days when the welcome bonus was as high as 180,000 MR points, or when you could get 50% off the annual fee (with a Samsonite luggage) on top of the two sets of Platinum Statement Credits in the first membership year?

But the worst thing you can do is get sentimental over your cards, and the AMEX Platinum Charge, like every other card, needs to prove its worth year after year.

My stance is that the card’s current crop of benefits don’t justify its price, unless perhaps you’re eligible for a welcome bonus (and remember, American Express has tightened the criteria for that too, by excluding anyone who holds a supplementary credit card).

It’s too much cognitive load

I’ve alluded to this earlier when I talked about Platinum Anxiety, but to put it mildly, the AMEX Platinum Charge is not a card that rewards passivity.

A prime example of this are the Platinum Statement Credits. Originally introduced in 2023, they were further “enhanced” in 2025 by splitting them into half-year allotments: one for January to June, and another from July to December.

| 💳 Platinum Statement Credits | ||

| 2024 | 2025 | |

| Local Dining | S$200 per yr. | S$100 per 6 mo. |

| Overseas Dining | S$200 per yr. | S$100 per 6 mo. |

| Lifestyle | S$400 per yr. (Min. S$600 spend) |

S$200 per 6 mo. (Min. S$300 spend) |

| Airline | S$200 per yr. (Min. S$600 spend) |

S$100 per 6 mo. (Min. S$300 spend) |

| Entertainment | S$17 per mo. | |

| Fashion | S$75 per 6 mo. | |

| Total | S$1,354 | |

It should be very clear why they’ve done this: to drive spending, and encourage breakage.

Twice-yearly credits create more opportunities for “overspending”, because cardholders are unlikely to hit the minimum spend exactly on the dot.

Moreover, the added complexity ensures that more cardholders don’t fully utilise their credits, either through forgetfulness, or because they don’t have the opportunity (e.g. the Overseas Dining credit requires that you travel overseas at least twice a year, to cities with participating restaurants).

So even though the total amount remained the same (S$1,354), the “realisable value” will have decreased. You’ll need a strategy each year to get your money’s worth, and I’ve often found myself having to make plans around the credits. For example, which destinations can I visit that will let me spend the Overseas Dining credit? What’s the cheapest item I can buy on Mr Porter to use the Fashion credit? How do I use the Lifestyle credit at Grand Cru while avoiding those Platinum-specific markups?

I was perfectly OK to do this in the past, but all the planning gets a bit tiring after a while. And now that I have added family responsibilities, I place a greater premium on my time. I don’t want to have to feel like I’m doing homework.

And to be fair, it isn’t just a Singapore-specific problem. Even elsewhere in the world, American Express has pivoted to a “coupon book” model, where cardholders are presented with a collection of use-it-or-lose-it credits. Just look at the US version, where cardholders have to juggle 13 different credits— some of which are half-yearly!

It’s not as fun anymore

This might be related to the previous point, but I just don’t find the AMEX Platinum Charge to be “fun” anymore.

Before COVID, you had big annual blowout events like Platinum af’FAIR, basically a carnival for grown-ups with great food, free flowing wines, fun activities and giveaways practically begging you to win champagne and Mont Blanc pens. Even during COVID, there was still an attempt to do a virtual edition, and while it was nowhere near as good as an in-person event, I appreciated the effort that went into organising it.

I often joked that Platinum af’FAIR was AMEX’s attempt to show cardholders that the af (annual fee) was fair, and as I wrote back in 2022:

You might say I’m making too much of it, but I don’t think you can underestimate the halo effect that Platinum af’FAIR has. Speaking from personal experience, it’s not uncommon that one person is a firm proponent of the AMEX Platinum Charge, and his/her partner is more of a skeptic who thinks shelling out S$1,712 (and S$1,728 from 2023) for a credit card is the height of frivolity.

Events like Platinum af’FAIR go a long way towards tipping the balance towards renewing, and why wouldn’t it? A blowout evening with good food, fine wines, great entertainment and plenty of activities is going to put a smile on anyone’s face. While you obviously won’t eat and drink four-digits’ worth, it’s one of those intangible things that’s hard to place an exact value on, yet creates a sense of goodwill towards the brand.

Moreover, it’s a great marketing tool. In previous years, Platinum Charge members could bring one guest to Platinum af’FAIR for free, and another two for a nominal fee. Guests (who would presumably be of the same socio-economic status as the cardholder) get a firsthand taste of the good life, and some of them might sign up as cardholders themselves.

Then there were members-only pop-ups like Platinum VIBES and NOOK by Platinum, where cardholders enjoyed a complimentary glass of wine and a pleasant place to catch up on some work between meetings, or host friends.

But as American Express started to swell the Platinum Charge ranks, it became impossible to offer such things. The few events that exist now are more modest affairs, and unless you’re religiously monitoring the AMEX Experiences app, they’re likely to be fully subscribed by the time you even get a notification.

It’s a shame, if you ask me. Events and pop-ups were hard to place a value on, yet made card membership feel extra special— certainly more so than your run-of-the-mill S$120K cards anyway.

What I’m switching to instead

AMEX Platinum Credit Card

Cancelling the AMEX Platinum Charge also means cancelling the AMEX Platinum Reserve, because I’ll no longer enjoy the annual fee waiver granted to those grandfathered in on the “one annual fee” scheme.

But I still want to enjoy Love Dining and Chillax benefits, and I need a “bucket” to store my remaining MR points. Therefore, I’ve got myself an AMEX Platinum Credit Card, which costs just S$327 (mandatory in the first year, waivable in subsequent years).

This is offset by a S$200 annual Lifestyle Credit, which can be used at participating restaurants and fashion boutiques across Singapore (with many more options than the AMEX Platinum Charge).

Speaking of MR points, I know I’m taking a hit in the conversions department, since the AMEX Platinum Charge enjoys a preferential 400 MR points = 250 miles, versus 450 MR points = 250 miles for other AMEX cards.

| Frequent Flyer Programme | Conversion Ratio (AMEX: Partner) |

|

| Plat Charge & Centurion | Others | |

| 400 : 250 | 450 : 250 | |

| 450 : 250 | 450 : 250 | |

| 400 : 250 | 450 : 250 | |

| 400 : 250 | 450 : 250 | |

| 400 : 250 | 450 : 250 | |

|

400 : 250 | 450 : 250 |

| 400 : 250 | 450 : 250 | |

| 400 : 250 | 450 : 250 | |

|

400 : 250 | 450 : 250 |

| 1,000 : 1,000 | 1,000 : 1,000 | |

| 1,000 : 1,250 | 1,000 : 1,250 | |

My solution was to dump out what I needed into miles (taking advantage of Cathay’s 10% transfer bonus), and keep the rest for hotel points where the ratio is identical between the AMEX Platinum Charge and other AMEX cards.

My earn rate at 10Xcelerator merchants will also be lower at 3.47 mpd (vs 3.9 mpd on the AMEX Platinum Charge), but it’s not like I spend a lot on these anyway.

HSBC Premier Mastercard

With the loss of my AMEX Platinum Charge, I now have a bit of a gap in lounge coverage.

My solution? The HSBC Premier Mastercard, which offers unlimited Priority Pass visits for myself and three supplementary cardholders— including non-lounge experiences like restaurants and spa treatments, which AMEX-issued Priority Pass cards don’t enjoy.

What’s more, I’m also eligible for a 106,200 miles welcome bonus with a minimum spend of S$5,000, and there’s no annual fee so long as I maintain S$200,000 with HSBC Premier (you’ll obviously want to deploy those funds as efficiently as you can, otherwise you end up paying “fees” in terms of forgone interest).

Together with secondary perks like limo rides, very decent complimentary travel insurance, and World Elite benefits, there’s more than enough here to replace the AMEX Platinum Charge as my “benefits card” (a card you keep for perks rather than spending; even though the earn rates aren’t terrible either!).

| ❓ What about the StanChart Beyond Card? |

|

While I’m not planning to sign up for the StanChart Beyond Card at the moment, it can also be an attractive alternative to the AMEX Platinum Charge— especially if you qualify for the Priority Banking or Priority Private variants that enjoy higher earn rates and additional perks. |

Conclusion

After eight years as a member, I’ve decided it’s time to say farewell to my AMEX Platinum Charge.

I have no regrets about getting the card, but with the recent wave of devaluations and the increasing complexity of benefits, I don’t feel it’s a good match for my lifestyle anymore. Besides, competing cards — in particular the HSBC Premier Mastercard — now offer a more compelling value proposition, and don’t impose anywhere near the same level of cognitive load.

And now, for a life free of Platinum Anxiety!

How’s your Platinum Anxiety doing these days?

agreed.. just cancel mine. not worth the trouble tracking usage of the vouchers. also the perks have all kinds of conditions to meet. platinum credit is good enough. Only regret is losing the bonvoy gold which is nice to have.

Think you mean hilton gold. Bonvoy gold is useless

HSBC Premier Mastercard is nice. but it doesnt solve the guest Priority Pass issue if you are bringing your kid with you as the priority pass supplements needs to be over 18…. If any suggestion will be welcomed

Get citi prestige or DBS vantage.

you’re right, the kid thing will be an issue. but right now she’s small enough to not be charged herself; I’ll worry about that when the time comes.

I also want to cancel this card. But my question is: what’s the latest time I should request the cancellation? since once you see the annual fee appear on your statement, it actually means you’ve already passed your previous year’s membership period

annual fee is charged in advance of the upcoming year. you can cancel once you see it

I left 2 1/2 yrs back. It was such a hassle tracking so many voucher categories. Very stressful & I could never fully utilise all the categories (which is probably what Amex hoped for)

Surprised anyone is still holding on to this card. Cancelled mine last year

I share your feelings Aaron although I am evaluating this from a first time subscriber POV. this pay huge annual fee + get a coupon scrapbook concept just dont sit well with me, especially with the extra hoops like registration and biyearly split

the amount of money you pay + the mental gymnastic you have to do is just too great

I feel you, I dropped mine last November. Right now I am using my HSBC premier card .

I thought the HSBC Premier Mastercard do not issue Priority Passes anymore. Was told by the helpdesk to show the Mastercard to enter the PP Lounges. o how to have non-Lounge experience?

just…present your hsbc premier mastercard.

Yes I was told the same thing, there is no need to access the app so I didnt know I have the non lounge priviledges too. so how to know I have that and which restaurants / bars can I go ? especially in other cities ?

I cancel mine last year and now use the Australia Amex Platinum.

Will cancel it before next membership year as the devaluation of the points. 2 points to 1 miles change to 3 points to 1miles.

I wonder if Citi Prestige or Stanchart Beyond is a worthwhile alternative now. Its quite sad because I have the HK Amex Plat that I just canceled this year after moving to SG. And I got the SG Plat last year. I think Ive exhausted most of the vouchers and the other benefits but I feel very tired to track and so many minimum spends. I used the Avid PC a lot but now having till next year only, it feels the card doesnt seem to have a lot of value now.

I got it in May and only manage to get $400 credit in Grand cru wines + 3 times love dining. these fashion credits are really useless, the website they sell extremely overvalue stuff, $75 could only buy a tote bag or some pair of lame socks. The local dining $100 is just too little for fine dining I don’t have guts to try. The $100 airline credit is kinda useless as I’m trying to redeem miles and the airport fee + tax is less than min $300 required.

Then you are not really their target market are you

Depends on what you consider to be their target market. I’m in their original target market (200K about 10 years ago) and I don’t think it is worth the effort now. Perhaps the card is now targeted at hobby coupon clippers with free time to match and only the MAS-required 30K income requirement to meet (which may mirror Amex expectations on the value of their personal time).

The other cards above the 120K tier have less stressful ownership experiences. At the 120K tier, the HSBC Premier and Citi Prestige have no annual fee (stress) for their designated target AUM/income group.

so agree about the airline bit. but what fashion credit ?

Fully agree.

Luckily i left right after it got nerved as my renewal month was in January each year.

Wonder if next time can join as new customer after 2 years to get the MR gift lol…

Anyway, its a good heavy card to flex during shopping. My ex-girlfriend was upset when I cancelled the supp card lol lol

Good times..

Great! now more people will follow you and drop from Amex Plat, and when you call concierge will actually help you and also maybe give you more MR points during renewal.

I think you have to value the insurance component – the coverage is decent.

yes, but what if you could get equivalent coverage elsewhere for free, e.g. hsbc premier MC (https://www.hsbc.com.sg/content/dam/hsbc/sg/documents/credit-cards/premier-mastercard/travel-insurance-policy-wordings.pdf)

how do you know HSBC premier priority pass has the non lounge passes ? the HSBC told me I just need present credit card with boarding pass at lounge and there is no need to access the app. how do i know I have these priviledges ?

answering how. present the card at lounge counter. check your phone alert for a charge. if there is a charge ask counter. or message your RM. let them deal with it. have another drink.

You’ll know the answer if you read the Milelion writeup on the card.

Cancelled the card long ago when I realized they actually dropped their requirements to so low that almost anyone can have the card. The “prestige” factor that is probably the main draw is long gone. Whoever is calling the shots at amex has no idea what he/she is doing.

left earlier this year when you posted about the changes myself. just didn’t want to spend the brain power trying to “fit” into the amex experiences. Was a bit of a pain transferring all the points accumulated, and changing travel chains/lifestyle, but once it’s done, it’s a bit freeing~

I did the same recently, as I have ~bloviated about constantly~ mentioned once or twice. When I first signed up for an Amex card in *1999* (back in Europe) I did so because I wanted my life to be *easier*. I didn’t want to have to think about travel insurance, wanted a concierge who could actually deliver, and to be able to drop into a lounge whenever and wherever I needed. When we moved to SG, the $1700+ annual fee was a blow, but it could still be made to make sense, possibly via some man-maths. Over the last five… Read more »

Just a small data point from recent travel, non lounge experience – xpress spa in Abu Dhabi airport (AUH) cannot not be redeem with HSBC premier MC directly. They need a priority pass card (which HSBC premier MC do not issue, unlike DBS Altitude). I suspect maybe restaurants may also have the same problem.

Another dp – I’ve used the HSBC PMC directly at a restaurant in Changi, so it sounds more like an issue with the specific merchant…

Hi Aaron, Looking to do the same as my AF just came up, am now trying to figure out which other cards provide cover for the benefits – I will have Hertz PC with IHG, Avis PC with Citi Prestige via Mastercard. Is there another card that covers Hilton Gold? I realize it isn’t much but on the odd occasions I do stay at a Hilton (biz and leisure) the breakfast and upgrades have come in handy.

nope, you won’t be able to get hilton gold via any other credit card in singapore.

that said, there is a time lag between cancelling your amex plat charge and your hilton gold getting revoked. how long exactly is uncertain, my supp cardholders still have their gold status…