| 🕰️ Hello, time traveller! |

| Found this page through a search engine? Look for the latest edition of this guide here |

Welcome to The MileLion’s 2023 Credit Card Strategy, where I lay my cards on the table, quite literally.

|

📢 Update: I’ve given this article a mid-year refresh to reflect the changes that have taken place over the past six months, as well as add some useful resources.

|

This article features the cards I use on a day-to-day basis; they’re not the only ones I have, but they certainly get the most action.

Three things to note before we get started.

First, this article is not intended to be a comprehensive listing of the best cards for each category. For example, in the petrol section I’ve not included the Maybank World Mastercard even though it earns the same 4 mpd as other featured cards like the UOB Preferred Platinum Visa and UOB Visa Signature.

That’s because I don’t find the rest of Maybank’s miles cards to be particularly compelling, and by introducing a single Maybank card just for petrol, I’d likely end up with orphan miles. Remember, the goal here is to share a strategy, not an encyclopaedia. If you’re interested in a comprehensive listing of the absolute best cards for a given category, refer instead to the What Card Do I Use For page.

Second, categories can overlap or be subsets of each other, so don’t think about them too rigidly. For example, a card which earns a bonus on contactless payments can be used at a restaurant, department store, supermarket, or anywhere that contactless payments are accepted. Likewise, if a card earns a bonus on foreign currency spend, it doesn’t matter whether that spend is dining, shopping or travel-related.

Third, different cards may define the same category differently. For example, what counts as “dining” to HSBC may be different from UOB. Always refer to the T&Cs for the exact list of MCCs.

|

| 💳 2023 Credit Card Strategy |

| ❓ What’s the MCC? |

|

Most of the above categories are defined by Merchant Category Code, or MCC. You can find the MCC of a given merchant before spending using either of the methods listed below |

| Abbreviations: c. month= calendar month, s. month= statement month, m. year= membership year |

Overall Strategy

Broadly speaking, there are two types of miles cards out there:

- General spending cards: Earn a flat rate of 1.0-1.6 mpd on all transactions

- Specialised spending cards: Earn 4-6 mpd on certain categories

If there’s one resolution you make this year, it should be to use general spending cards as sparingly as possible.

Since specialised spending cards cover such a wide range of transactions, it seems almost sinful to settle for the lower earn rates of a general spending card. Put it another way: someone who regularly utilises 4-6 mpd cards will earn a free flight much faster than someone who puts everything on a 1.2 mpd card.

Your goal, in so many words, is to:

Use specialised spending cards as much as possible

Yes, it may mean applying for more than one credit card. Yes, it may be slightly less convenient. Yes, your spouse may get annoyed when you nag them about using the right card. But I promise you this: no one ever moaned about having to carry multiple credit cards when kicking back in a Business Class seat with some pre-flight champagne.

Contactless Payments: HSBC Revolution, UOB Preferred Platinum Visa, UOB Visa Signature

| Card | Earn Rate | Remarks |

HSBC Revolution HSBC RevolutionApply |

4 mpd | Max S$1K per c. month on dining, groceries, shopping, travel Review |

UOB PPV UOB PPVApply |

4 mpd | Max S$1.1K per c. month, must use mobile payments Review |

UOB Visa Signature UOB Visa Signature Apply |

4 mpd | S$1K-2K per s. month on contactless & petrol Review |

Contactless payments aren’t a category of spending as such, more like a method. But who cares? Contactless terminals are so ubiquitous these days that earning 4 mpd on the vast majority of your spending should be straightforward.

There are no changes here from last year. The UOB Preferred Platinum Visa (PPV) continues to be the go-to option, earning 4 mpd on all mobile payment transactions except UOB$ merchants and UOB’s standard exclusion list (e.g. hospitals, schools, government entities). This is capped at S$1,110 per calendar month.

| ⚠️ UOB PPV: Use Mobile Wallet! |

| To earn 4 mpd on the UOB PPV, you must add the card to your mobile wallet and tap your phone; you won’t earn the bonus if you tap the physical card. |

Those who regularly spend beyond the UOB PPV’s monthly cap can consider the UOB Visa Signature, which earns 4 mpd on contactless transactions with a minimum spend of S$1,000 per statement month on contactless and/or petrol transactions. This is capped at S$2,000 per statement month.

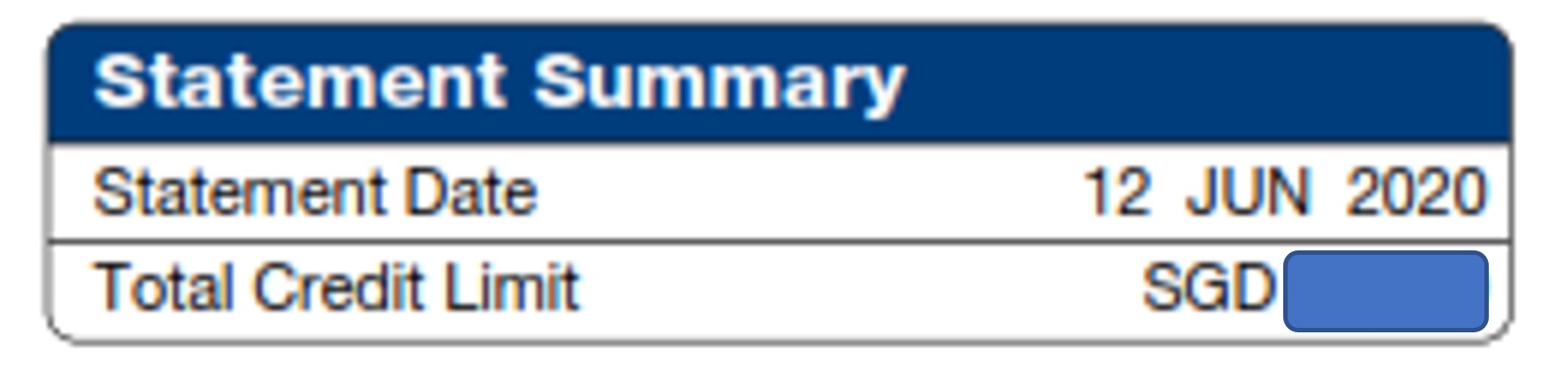

| ⚠️ Statement Month vs Calendar Month |

|

Your card’s 4 mpd cap may follow the calendar month or statement month. Calendar month is straightforward (i.e. 1-31 January), but statement month needs a little explaining. Generate your UOB e-statement and look for the statement date at the top right hand corner. This tells you what your statement cycle is; in the example below, it’s 12th to the 11th of the following month.

The UOB Visa Signature’s 4 mpd cap resets on the statement date. This adds an additional level of complexity, but you can always call up customer service and ask them to change your statement cycle to follow the calendar month instead. |

Alternatively, you can use the HSBC Revolution for 4 mpd on selected contactless payments, namely:

- Airlines, hotels, car rental, cruise liners, travel agencies

- Department and retail stores

- Supermarkets, restaurants and food delivery

- Transportation (excluding public transport) and membership clubs

This is capped at S$1,000 per calendar month. It’s not quite the “4 mpd everywhere” that the UOB cards offer, but still a very wide range of day-to-day merchants.

Dining: HSBC Revolution, UOB Lady’s Cards

| Card | Earn Rate | Remarks |

UOB Lady’s Card UOB Lady’s CardApply |

6 mpd | Max S$1K per c. month. Must choose dining as bonus category Review |

UOB Lady’s Solitaire UOB Lady’s SolitaireApply |

6 mpd | Max S$3K per c. month. Must choose dining as bonus category Review |

| HSBC Revolution Apply |

4 mpd | Max S$1K per c. month. Must use online or contactless Review |

In February 2023, the UOB Lady’s Cards were given one heck of a buff: 6 mpd on a choice of up to two bonus categories, valid till 29 February 2024. This is capped at S$1,000 per calendar month for the UOB Lady’s Card, and S$3,000 per calendar month for the UOB Lady’s Solitaire. Dining is one of the bonus categories you can choose.

Otherwise, try the HSBC Revolution. This offers 4 mpd on dining, capped at S$1,000 per calendar month. While the earn rate is lower, it does compensate by having a wider definition of dining.

| 🍽️ Comparison of Dining Card MCC Coverage | ||

|

|

|

| MCC | HSBC Revo (4 mpd) |

UOB Lady’s Card (6 mpd) |

| 5811 | ✅ | ✅ |

| 5812 | ✅ | ✅ |

| 5813 | ✅ | |

| 5814 | ✅ | ✅ |

| 5441 | ✅ | |

| 5462 | ✅ | |

| 5499 | ✅ | ✅ |

| ❓ MCC Descriptions | ||

|

||

For example, the HSBC Revolution covers bakeries, confectionary stores and bars, all of which don’t fall under the UOB Lady’s Card’s definition of dining. More importantly, the HSBC Revolution also earns 4 mpd on hotel spending, which could make all the difference for a hotel restaurant (sometimes they code as restaurants, sometimes they code as hotels).

| S$5 for new Kris+ Users | |||

| ⚠️ Don’t forget Kris+ | |||

|

Whenever you dine out, be sure to check whether the restaurant is featured on Kris+. This can be an opportunity to earn bonus miles, on top of whatever you’d get from your credit card. For the best cards to use with Kris+, refer to this post. Get S$5 when you sign-up with code W644363 and make your first Kris+ transaction. |

Foreign Currency (FCY): Amaze or UOB Visa Signature

| Card | Earn Rate | Remarks |

Amaze + Citi Rewards Amaze + Citi RewardsApply |

4 mpd | Max $1K per s. month Review |

| UOB Visa Signature Apply |

4 mpd | S$1-2K per s. month on FCY spending Review |

Amaze continues to be my first choice for all overseas spend, since it allows you to earn credit card rewards and InstaPoints (worth up to a 1% cash rebate), while enjoying lower FCY transaction fees than you would by using the credit card directly.

The question then becomes which credit card you pair it with, and my default option is the Citi Rewards Card. There’s a few other cards you can consider too, depending on category; refer to the article below for more information.

If you don’t want to use the Amaze, consider the UOB Visa Signature. This earns 4 mpd on overseas spending, subject to a minimum FCY spend of S$1,000 per statement month, and capped at S$2,000 FCY spend per statement month. Do note that this cap is shared with the 4 mpd cap for contactless payments/petrol. For a more detailed explanation of how the caps work, refer to this article.

While this post is meant to focus on evergreen earn rates rather than limited time offers, you might want to refer to the article below for some overseas spending promotions run by various banks.

Offline Shopping: Citi Rewards, HSBC Revolution, OCBC Titanium Rewards

| Card | Earn Rate | Remarks |

Apply |

4 mpd | Max S$1K per s. month Review |

| HSBC Revolution Apply |

4 mpd | Max S$1K per c. month. Must use contactless Review |

OCBC Titanium Rewards OCBC Titanium RewardsApply |

4 mpd | Max S$13.3K per m. year. Pink and Blue cards have their own cap Review |

If you shop at brick-and-mortar stores for bags, shoes and clothes, use the Citi Rewards, HSBC Revolution, or OCBC Titanium Rewards for 4 mpd.

I would, however, lean towards the OCBC Titanium as my first choice for the following reasons:

- The OCBC Titanium Rewards has a relatively narrower range of 4 mpd categories compared to the Citi Rewards and HSBC Revolution, and as a general rule you should utilise the less flexible caps first (e.g. it makes more sense to use the OCBC Titanium Rewards for shopping and the HSBC Revolution for groceries)

- The OCBC Titanium Rewards’ 4 mpd cap is based on membership year, so if you have a big-ticket item to purchase, you can utilise your entire year’s cap (S$13.3K) at one go

The OCBC Titanium Rewards Pink and Blue cards each have their own S$13,335 annual cap, so big spenders can get both (OCBC$ will pool together).

Do note that each bank has a slightly different definition of shopping, so I’d advise you check the T&Cs for clarity.

Online Transactions: Citi Rewards or DBS Woman’s World Card

| Card | Earn Rate | Remarks |

Apply |

4 mpd | Max S$1K per s. month, excludes travel Review |

DBS WWMC DBS WWMCApply |

4 mpd | Max S$2K per c. month Review |

Like contactless payments, online transactions are another big catch-all category. Just think of how many online transactions you typically make in a given month: movie tickets, Grab rides, Deliveroo, Shopee, Netflix subscriptions etc.

Both the Citi Rewards or DBS WWMC will earn 4 mpd, so long as it doesn’t fall into the bank’s general list of exclusions (e.g. insurance, donations), or in the specific case of the Citi Rewards, travel (e.g. airfares, hotels, rental cars, travel agencies).

| ❓ Blacklist vs Whitelist |

|

You could certainly use the HSBC Revolution or UOB PPV for some online transactions, but it’s important to remember these cards follow a “whitelist” approach: a given online transaction doesn’t earn 4 mpd unless its MCC falls within the inclusion list. Contrast this with the Citi Rewards and DBS WWMC, which follow a “blacklist” approach: a given online transaction will earn 4 mpd unless its MCC falls within the exclusion list. It just means you need to be more careful with the HSBC Revolution and UOB PPV. |

If you’re using the Citi Rewards Card, remember to avoid in-app mobile wallet payments, because you won’t earn any bonus. For example, using your Citi Rewards Card with Deliveroo directly would earn 4 mpd, but using your Citi Rewards Card with Deliveroo via Google Pay would earn only 0.4 mpd.

Petrol: UOB Lady’s Cards, UOB Preferred Platinum Visa, UOB Visa Signature

| Card | Earn Rate | Remarks |

| UOB Lady’s Card Apply |

6 mpd* | Max S$1K per c. month. Must choose transport as bonus category Review |

| UOB Lady’s Solitaire Apply |

6 mpd* | Max S$3K per c. month. Must choose transport as bonus category Review |

| UOB PPV Apply |

4 mpd* | Max S$1.1K per c. month, must use mobile payments Review |

| UOB Visa Signature Apply |

4 mpd* | S$1K-2K on petrol + contactless per s. month Review |

| *SPC transactions will earn bonus UNI$ but not base UNI$, i.e. deduct 0.4 mpd from the amounts above. UOB PPV will not earn any points with SPC | ||

Although I feel the best card for petrol is the one that gives the biggest discount, if you’re just looking at miles then it’s a toss up among the UOB Lady’s Cards, UOB PPV or UOB Visa Signature.

UOB Lady’s Cardholders will earn 6 mpd on petrol, provided they select transport as their quarterly bonus category. UOV PPV Cardholders will earn 4 mpd, provided they pay by mobile contactless, and UOB Visa Signature Cardholders will earn 4 mpd, provided they spend at least S$1,000 on local contactless payments and/or petrol in a given statement month.

It was previously thought that UOB cards would not earn miles at Shell and SPC stations, but on-ground testing has shown otherwise. Shell transactions earn full UNI$, while SPC transactions earn bonus UNI$ with all cards except the UOB PPV.

For a better understanding on the trade-off between miles and discounts, refer to the post below.

Public Transport: UOB Lady’s Cards, KrisFlyer UOB Card

| Card | Earn Rate | Remarks |

| UOB Lady’s Card Apply |

6 mpd | Max S$1K per c. month. Must choose transport as bonus category Review |

| UOB Lady’s Solitaire Apply |

6 mpd | Max S$3K per c. month. Must choose transport as bonus category Review |

KrisFlyer UOB Credit Card KrisFlyer UOB Credit CardApply |

3 mpd | Min. S$800 on SIA Group transactions in a m. year |

| C. Month= Calendar Month, S. Month= Statement Month | ||

Public transport won’t be a huge component of your monthly expenditure, but it’s still a category worth optimising.

The UOB Lady’s Card and UOB Lady’s Solitaire Card will earn 6 mpd, provided transport is chosen as the quarterly bonus category. Alternatively, use the KrisFlyer UOB Credit Card for 3 mpd, subject to a minimum S$800 spend on SIA Group transactions in a membership year.

Weddings

If you’re planning a wedding, your first step should be to see what sign-up bonuses you can take advantage of.

Assuming you’ve already maxed those out, you can use the following cards to pay off S$11,220 of your banquet amount each month, earning 50,880 miles in the process. I’m assuming the lady qualifies for a UOB Lady’s Solitaire Card (min. income S$120,000- not strictly enforced), but you can swap it out for the regular UOB Lady’s Card if not, for the loss of 12,000 miles each month.

| 💒 Monthly Banquet Payments | ||

| 🤵 Him | 👰 Her | |

| UOB PPV Apply |

S$1,110 | S$1,110 |

| UOB Visa Signature Apply |

S$2,000 | S$2,000 |

| UOB Lady’s Solitaire Apply |

N/A | S$3,000* |

| HSBC Revolution Apply |

S$1,000 | S$1,000 |

| Total Spend | S$4,110 | S$7,110 |

| Total Miles | 16,440 | 34,440 |

| *If banquet held in a hotel, select travel as your bonus category. If banquet held in a restaurant, select dining as your bonus category | ||

For more details, refer to the dedicated post I wrote on the subject.

General Spending: AMEX HighFlyer Card, UOB PRVI Miles Card

| Card | Earn Rate | Remarks |

|

|

1.8 mpd | Only available to SME owners Review |

|

|

1.4 mpd (local) 2.4 mpd (overseas) |

S$5 blocks mean your effective mpd may be less on smaller transactions Review |

| If you haven’t fully utilised the 4 mpd cap on the Citi Rewards, then pairing it with Amaze would also work for general spending (since Amaze converts all offline transactions into online ones)- just avoid travel related transactions. | ||

UOB PRVI Miles Card

UOB PRVI Miles CardAs I said at the start, you should be using your general spending card as sparingly as possible. This should be reserved for situations where you’ve exhausted your bonus caps on specialised spending cards, or when the category is not “bonus-able”.

If you happen to own an SME, then the AMEX HighFlyer Card is a great general spending solution with 1.8 mpd on all local and overseas spend.

The main drawback of this card is that it limits you to converting a maximum of 150,000 KrisFlyer miles per calendar year (30,000 miles to five accounts), but you probably won’t be putting that much on a general spending card in the first place. Also, it no longer earns miles on GrabPay top-ups, effective 4 April 2023.

For everyone else, there’s the UOB PRVI Miles Card which earns 1.4 mpd on local spend and 2.4 mpd overseas. There’s no real harm in using the DBS Altitude/ Citi PremierMiles/ OCBC 90°N Card either, even though they earn slightly less. Ideally, you’d be putting as little spending as possible on your general spending card anyway, so the difference shouldn’t be too material.

| ⚠️ Don’t forget the effects of rounding! |

|

A card with a lower earn rate could still end up earning more miles than a card with a higher earn rate if its rounding policy is more favourable. For example, the UOB PRVI Miles Card rounds all transactions down to the nearest S$5 before awarding points, while the Citi PremierMiles Card rounds transactions down to the nearest S$1. To learn more about rounding policies for each card, refer to this post. |

Of course, if you earn enough to qualify for one of the 1.6 mpd general spending cards such as the Citi ULTIMA, UOB Reserve, DBS Insignia or the OCBC VOYAGE (Premier/PPC/BOS), by all means go ahead and use it.

“Troublesome transactions”

There are a few categories that I refer to as “troublesome transactions”, since they’re generally excluded from rewards by most if not all banks.

Examples include:

- 💗 Charitable Donations

- 🏫 Education

- 🏣 Government Payments

- 🏥 Hospital Bills

- ☂️ Insurance

- 🚰 Utilities Bills

AMEX HighFlyer Cardholders used to be able to earn miles on such transactions by way of topping up a GrabPay account, then paying the bill via AXS, but that’s no longer possible- GrabPay-AXS was nerfed on 16 January, and GrabPay top-ups on 4 April)

These aren’t lost causes, however. In the articles linked above I’ve mentioned some cards that still earn rewards, and if all else fails, there’s always the option of using a bill payment service. These allow you to pay bills with your credit card in exchange for a small admin fee.

| Provider | Fee | Cost Per Mile* |

| 2.5% | 1.52-2.03 | |

|

2.25% (code: GET225) S$30 off first payment with code: MILELION |

1.38-1.83 |

| 2.2% | 1 cent^ (till 20 Aug 23) |

|

|

1.9% | 1.36-1.9 |

| ^Min. spend of S$8,000 required on all Citi PayAll transactions during promo period *Based on general spending cards with earn rates of 1.2 to 1.6 mpd. For more information about what cards to use with CardUp, refer to this post |

||

Whether or not the admin fee makes sense depends on how much you value a mile. I personally would consider options that let me buy miles at less than 1.5 cents apiece, but your situation may differ. Do look out for periodic promotions that can bring down the cost of miles even further.

Pulling double duty

While the sheer number of cards mentioned above may seem intimidating, the good news is that many can pull double duty. For example, a HSBC Revolution would take care of your dining, grocery and travel expenses, while a UOB PPV would be a simple solution for anywhere that accepts mobile payments.

Likewise, if you’re dining at an overseas restaurant, you could use the HSBC Revolution (dining) or the UOB Visa Signature (FCY) to earn 4 mpd.

If you told me I could have four cards and no more, my top picks would be:

- UOB PPV (for all mobile payments at physical merchants)

- Citi Rewards (for all online transactions)

- DBS WWMC (for all online transactions)

- HSBC Revolution (for dining, grocery, travel and shopping transactions)

And of course, I’d take the UOB Lady’s Solitaire Card as well if I were otherwise qualified.

Is it possible to over-optimise?

As much as we want to maximize 4 mpd everywhere, is it possible to overdo it?

Yes, definitely. The way I see it, there are two additional considerations:

(1) Conversion Fees

By spreading your cards across multiple banks, you’re collecting different points currencies and will have to pay more than one conversion fee.

However, I’m not too worried about this. Conversion fees are annoying and we try to minimise them where we can, but paying them isn’t the end of the world. In the grand scheme of things, an extra S$25 here and there isn’t going to destroy the overall value proposition of the miles game.

| Issuer | Per Conversion | Annual Option |

|

S$201 | N/A |

|

S$30 | N/A |

| S$272 | N/A | |

| S$27 | S$43.203 | |

| N/A | S$43.204 | |

|

S$275 | N/A |

| S$25 | N/A | |

| S$27 | N/A | |

| S$256 | S$507 | |

| 1. Waived for all AMEX Platinum and AMEX Centurion cardholders 2. Waived for Citi ULTIMA cardholders 3. Automatic conversions in blocks of 500 DBS points (1,000 miles) each quarter. Additional ad-hoc redemptions can be done for free 4. Covers all HSBC cards you may have, even though HSBC points don’t pool 5. Waived for Maybank Visa Infinite and Maybank World Mastercard cardholders 6. Waived for UOB Reserve, UOB Visa Infinite Metal, UOB Visa Infinite and UOB Privilege Banking cardholders 7. Automatic conversions in blocks of UNI$2,500 (5,000 miles) each month for balances above UNI$15,000. Additional ad-hoc redemptions cost S$25 |

||

Moreover, it doesn’t necessarily mean more cards = more fees. If you own multiple cards from the same bank, you may still pay only a single conversion fee, provided the points are pooled.

For example, a UOB customer could hold a UOB PRVI Miles, UOB PPV, UOB Visa Signature and UOB Lady’s Card, all while paying only a single conversion fee.

(2) Orphan Points

Orphan points are a bigger concern than conversion fees in my book. If you spread yourself too thin, you may end up in a situation where you’re optimising on individual transactions, but not in an overall sense.

To illustrate, suppose I drive very infrequently but get a Maybank World Mastercard just so I can earn 4 mpd on petrol. I may be optimising on that particular transaction, but it counts for very little if I end up with a small chunk of TREATS points that I can’t cash out.

| ✈️ Min. Conversion Blocks for KrisFlyer Miles | ||

| Currency | Points | Miles |

| AMEX Membership Rewards | 450 | 250 |

| AMEX Membership Rewards (Plat. Charge, Centurion) |

400 | 250 |

| BOC Points | 45K | 10K |

| Citi Miles | 10K | 10K |

| Citi ThankYou Points | 25K | 10K |

| DBS Points | 5K | 10K |

| HSBC Points | 25K | 10K |

| Maybank TREATS | 25K | 10K |

| OCBC$ | 25K | 10K |

| OCBC Travel$ | 1K | 1K |

| OCBC VOYAGE Miles | 1 | 1 |

| SC Rewards Points (Visa Infinite) |

25K | 10K |

| SC Rewards Points (Non-Visa Infinite) |

34.5K | 10K |

| UOB UNI$ | 5K | 10K |

| * Fee waived for Citi ULTIMA cardholders ^Fee waived for Maybank Visa Infinite and World Mastercard cardholders #Fee waived for UOB Reserve, Visa Infinite, Visa Infinite Metal and Privilege Banking Visa Infinite cardholders |

||

Optimisation is good, but you need to look at both the micro and macro picture. If you don’t spend a significant amount on a particular category, then consider using your general spending card instead.

Conclusion

A good credit card strategy is more than just knowing what the best cards are for each category. It’s about smartly managing your caps (e.g. since the UOB PPV earns 4 mpd on all contactless transactions, I’d rather use my HSBC Revolution to pay for lunch and conserve the PPV’s cap for non-dining venues), minimising conversion fees and avoiding orphan miles.

Don’t forget to check out the “What Card Do I Use For…” guide, which provides more granular advice for certain categories.

Any other cards that are featuring in your 2023 game plan?

Thanks Aaron for the very useful update. In my humble opinion, I think Kris+ deserves a mention since it allows you to earn up to 13 miles per dollar.

Certainly does! The more you can stack the better

Apparently, UOB visa infinite covers education as well.

Is Amaze still good for making non online purchases, online? I didn’t see it under the online transactions section..

Wouldn’t it be easier to just use the Amaze + Citi Rewards for overseas dining?

it would be easier to just use amaze + citi rewards for everything (except travel). however, i’m assuming you want to conserve your precious caps by using dedicated dining cards for dining.

Does HSBC Revo earn 4mpd overseas for dining/groceries + contactless?

What card would be good for big luxury purchase like $50k+ watches?

Plat charge. 7.8mpd on selected merchants

This? https://www.americanexpress.com/sg/charge-cards/platinum-card/

Annual fees is 1.7k. Any other alternative?

Hi Aaron, maybe you should take into consideration the opportunity cost of using a bill payment service.

For example, using citipayall isn’t really acquiring a mile for 1.1 cpm if you consider the loss of potential rebate of 1.5% (using Amex cashback to top up grabpay and then using AXS/grabpay to pay for eg income tax).

Well yes…but in that case there never really is such a thing as free miles. Every transaction that you use a miles card for is one you can’t earn cashback. This would apply even if you’re paying no fees for regular retail transactions

Don’t agree. The point being made above, is one I have made earlier too. Let’s say I have a $1000 transaction and 2 choices. Choice 1 is earn 1100 miles via Citipayall (the 1.1 cpm mile mentioned in the above post). Choice 2 is earn $15 cash back. Which is better? In my view the cash back is CLEALY better, because you can use this $15 to “buy” more than 1100 miles. In fact, right now, you can use the $15 to get 1850 miles (I won’t go into the detail here of how, but it most certainly can be… Read more »

You don’t want go into details then only you can buy at that rate. How to make comparison for everyone else?

OK. So here is how to use $35 to buy 5,833 miles – actually more than the above post. So after doing the $1000 transaction above I am $35 in cash better off with Choice 2 (cash back) as opposed to Choice 1 (City Payall). So now we need to use this $35 to buy miles. There is more than 1 way available at the moment. This is the UOB-way. UOB have a Pay Anything Payment facility. So, I do a payall facility over 12 months. The cost is 2.7%. But the money I receive from UOB can earn 3.8%… Read more »

Actually, I need to update the above, as Choice 2 is even better than what I stated above, as the above post does not take into account the COST of the miles via Citi Payall. So, I re-write below: Let’s say I have a $1000 transaction and 2 choices. Choice 1 is earn 1800 miles via Citipayall (the 1.1 cpm mile mentioned in the above post), but this comes at a cost of a $20 fee. Choice 2 is earn $15 cash back. Which is better? In my view the cash back is CLEALY better, because you can use this… Read more »

You keep saying can get at 0.8cpm but the only option is PayAll during tax season and not right now

Not correct at all. Read post above about UOB Pay Anything facility. In fact this is getting miles at even less than 0.8cpm. 0.6cpm to be exact. OK, that comes with a small amount of forward interest rate risk, but I reckon high chance end result will be in the range of 0.6cpm to 0.8cpm.

Your calculation is completely wrong. Because you incur a monthly expense. Which means that your capital earning interest will decrease every month. Your 2.7% is incurred immediately on the full sum but every month your interest bearing amount decreases by 1/12.

My calculation is not completely wrong. It is 100% accurate. The s/sheet has taken into account the pay-down of the $5833. That is why only $122.49 interest is earned – not a full 3.8% of the $5833, because this is being paid down. And my calculation also takes into account the 2.7% that is paid up-front. Well, it is not actually paid up-front, it is paid about 6 weeks later when your credit card payment is due. My figures are 100% accurate – maybe rather than writing nonsense you should apply some s/sheet skills to calculate it, as I have?… Read more »

This UOB facility only works for the listed 6 cards or can use on the cards that fulfil the One Account $500 spend requirement?

Per the UOB site, there are a number of cards you can use. Also, for some of those cards, the fee is lower than 2.7%. Best is 2.6%

https://www.uob.com.sg/personal/cards/payment-services/payment-facility.page#applynow

FDs you need to lock the entire sum up for 12 months to get anywhere close to 3+%. SCB esaver bonus only 3.85% until end Jan. UOB One needs extra CC spend, DBS multiplier needs 3 categories. What other methods can you use?

Ay yah! This is the last post I am going to reply to, for those who are very good at thinking of problems, but unable to think of solutions. Yes, the SCB e$saver rate is to end January. What will it be after that? We don’t know for sure, but I bet it will be near the 3.80% level. As I mentioned in a post above, yes, there is some forward interest rate risk. However, you can mitigate most of the forward interest rate risk. But no, you don’t need to lock the entire sum up for 12 months. There… Read more »

Have you actually done this or are you just talking about theoretically here? Have you actually verified that the monthly expense is exactly as your spreadsheet shows? Because when I did a quick spreadsheet the difference is much more than $35 for me even at 0.385%.

(removed)

Maybe an easier way to think about it without the bank account interest: The trade off is between the following two options (as one example): 1) Payment facility: Pay $1000 insurance premium via CardUp. Pay a fee of 2.25% ($22.5) and get 1500 miles (if using DBS Vantage). Cost per mile is 1.5 cent. 2) Cashback + UOB facility: Pay $1000 insurance with UOB Absolute Cashback (assuming Amex accepted) and get 1.7% ($17) cash back. If you now use that $17 plus the $22.5 from above, you can spend $39.5 on buying miles via UOB. Currently they charge around 1.9… Read more »

The above is correct Mike. However it makes sense now to include bank interest, as interest rates are no longer near-zero and the interest earning until you need to repay UOB makes a significant difference now. But I guess you still illustrate the point without the added complexity. Also, everyone has a different personal situation. If your main objective is to acquire as many miles as possible, then you would not consider either 1 or 2. You would do 1, and then separately you would max out your UOB credit limit to get the most miles that way too. Basically… Read more »

The above is correct Mike. However it makes sense now to include bank interest, as interest rates are no longer near-zero and the interest earning until you need to repay UOB makes a significant difference now. But I guess you still illustrate the point without the added complexity. Also, everyone has a different personal situation. If your main objective is to acquire as many miles as possible, then you would not consider either 1 or 2. You would do 1, and then separately you would max out your UOB credit limit to get the most miles that way too. Basically… Read more »

What about the DBS Vantage card? It has quite a high general spend earn rate.

I always assumed that for overseas offline shopping spend, I could just use Amaze + OCBC Titanium for 4mpd, am I getting it all wrong :/ (of course ymmv)

I’d also give a shoutout to the HSBC Everyday Global account which gives you 1% cash back on GIROs. A nice way of not forgetting to pay your 5-10 credit cards and double/triple dipping value!

Is this only on eGIRO? Or all GIROs?

Not sure what the difference is, but I’ve got all my CCs on it for automatic deduction so whatever that kind is

Great! Thank you very much. Looks like Im going to create an account. Not sure if you have a referral code or something. Happy to punch in your code for the intro.

If it works on tax payment, I will switch this moment

Is DBS Altitude still among the “Specialized” list?

you can still earn 3 mpd on online airline and hotel spend, yes

Regarding hotel spend, must it be online hotel spend? Or is it still 3mpd if swiped at the hotel?

Hi!

If I’m planning to buy air tickets for a family holiday, with expected spend to be $4-5k, which card would be best to optimize?

Although 3MPD, am thinking DBS Altitude cos of $5k/mth cap and points pooled with DBS WWMC. But just wanted to see if anyone else had an alternative to optimize.

Also, does anyone know if DBS Altitude earns miles from spend on Airbnb?

Thanks in advance!

The best place for air tickets priced in SGD is DBS WWMC ($2k cap) or DBS Altitude ($5k cap). DBS Altitude and DBS WWMC earn miles on Airbnb. But because Airbnb process transactions outside of Singapore, even if the charge is in SGD, 1% DCC will be added. However, for a miles earn of 3 (Altitude) or 4 (WWMC) it is worth paying the 1%.

I have a stay at the Waldorf Astoria Maldives coming up later this month — what card would you recommend paying the final folio bill with? It will include all incidentals + yacht transfers (~$1K per person).

Would it make sense to split the payment between a few cards, prioritise those that do earn 4 miles / SGD for either contactless/Apple Pay and/or FCY (e.g. UOB PPV, HSBC Visa Revolution) first and then put the rest on a general spending card with a reasonably high FCY earn rate (e.g. UOB PRVI Miles)?

Hey mate very insightful post.. question though.. as a new expat if we want only 2 cards what would your recommendation be? Especially with Ikea spend in mind?

Same scenario as me. I’m looking at the OCBC Titanium Rewards for bulk IKEA spending and other one-time big ticket purchases. It has an annual cap for 4mpd vs other cards’ monthly cap.

uob PPV + dbs wwmc should cover most of your needs. although it needs to be said that if you only want to use 2 cards, you’re not doing the miles game right

UOB PPV (offline with mobile) + DBS WWWC (online), is it a good pair already?

Right now i got

WWWC for online

Altitude for general

OCBC platinum (for my wife general use)

Amex krisflyer (under utilised or for those didnt earn point thru master/visa).

Is it wise that i replace altitude with UOB PPV to maximise my miles game?

Anything else u can advise based on my owned card?

Thanks in advance.

Does the UOB PPV earn 4MPD for mobile contactless transactions at physical merchants overseas??

no problems for me.

Hi – will recurring payments setup for online video subscriptions like Netflix, Disney+, Prime Video, etc gain points for Citi Rewards and/or DBS WWMC? I know for telco recurring it does not. Thanks

Hi, I get 4mpd for Netflix using CRMC.

Hi Aaron, what’s best card to use for large Taobao purchases? does it qualify for FC spending on UOB visa signature card?

The best card for petrol is the Maybank Duo which gives a 5% rebate at any petrol stations in Singapore and Malaysia. Used at Sinopec which offers 23% discount, it’s 26.85% off net. No minimum spend and no merchant restrictions.

For the FCY, need to note that Citi will charge 1% if the transaction location is overseas. This would be added on top of any Amaze charges.

If you spend via amaze the transaction is in sgd, and processed in singapore

Unfortunately from 16 Jan 2023 we can’t use GrabPay account to pay bills via AXS

“Citi Rewards Card, remember to avoid in-app mobile wallet payments, because you won’t earn any bonus.”

Can I clarify what is considered an in-app mobile wallet payment?

Google pay, shopback pay, shopee pay etc ?

Anyone can help ?

Thanks in advance. 🙂

I believe Google pay, samsung pay and apple pay are excluded from this category for citi rewards