Welcome to the 2023 edition of the $120K Credit Card Showdown, my annual look at the finest pieces of plastic (or metal) that money can buy. $120K cards come with hefty annual fees that are generally non-waivable, so before you hop onboard, it makes sense to formulate a game plan to extract maximum value.

In the sixth iteration of this guide, we’ll walk through all the pertinent aspects to see which $120K card is right for you!

What is the $120K segment?

The credit card market in Singapore is broadly segmented into three tiers, which I’ve illustrated below with helpful band descriptors.

At the bottom are entry-level cards like the Citi PremierMiles, DBS Altitude and HSBC Revolution. The income requirement here is the MAS-mandated minimum of S$30,000, and benefits are limited to a few free lounge visits or generic bank discounts.

At the top are invitation-only cards like the AMEX Centurion, Citi ULTIMA, DBS Insignia, and UOB Reserve. Income requirements here are well in excess of S$500,000; benefits include who-do-you-want-killed concierge services, and invitations to events on Epsteinesque private islands.

In between those two you’ll find the mass-affluent tier, otherwise known as the $120K segment (note that despite the name, income requirements actually range from S$120,000 to S$150,000).

Some argue this to be the sweet spot. While nowhere as glamorous as the segment above, annual fees are ~80% lower and perks still include unlimited lounge access, complimentary airport transfers and exclusive hotel offers. Some sport metal cardstock too, for that extra premium feel.

The $120K candidates

| 💳 $120K Candidates | |

|

|

| AMEX Platinum Reserve Plastic |

Citi Prestige Metal |

|

|

| DBS Vantage Metal |

HSBC Visa Infinite Plastic |

|

|

| Maybank Visa Infinite Plastic |

OCBC VOYAGE Metal |

|

|

| SCB Visa Infinite Plastic |

UOB VI Metal Card Metal |

2023’s lineup of $120K cards features the same eight faces that contested the 2022 edition. There have been no new entrants to the market since DBS launched the Vantage Card in June 2022, although some cards have received a makeover.

This year, we can lay to rest the question of whether the StanChart X Card should be included. StanChart has finally put the beleaguered product out of its misery by replacing it with the mass market Journey Card.

Another common question is whether or not the AMEX Platinum Charge should feature. My answer is no, because even though it’s targeting the same market (while American Express no longer states an official income requirement, the last published figure was S$150,000/year), it’s a very different product due to its S$1,728 annual fee. This makes it almost impossible to do a fair comparison, because an annual fee that’s 3X the competition provides the scope to offer more benefits.

I’ve also excluded $120K cards like the Bank of China Visa Infinite and CIMB Visa Infinite, because they earn cashback instead of points. Likewise, there’s no room for the UOB Lady’s Solitaire Card because it’s less of a general spending card and more of a specialised spending option (and a superb one at that).

What’s changed since last year?

Here’s a quick snapshot of what’s changed since the previous $120K showdown in June 2022.

| AMEX Plat. Reserve |

|

| + Improvements | – Devaluations |

|

|

| Citi Prestige |

|

| + Improvements | – Devaluations |

|

|

DBS Vantage DBS Vantage |

|

| + Improvements | – Devaluations |

|

|

| HSBC Visa Infinite |

|

| + Improvements | – Devaluations |

|

|

| Maybank Visa Infinite |

|

| + Improvements | – Devaluations |

|

|

| OCBC VOYAGE |

|

| + Improvements | – Devaluations |

|

|

| SCB Visa Infinite |

|

| + Improvements | – Devaluations |

|

|

| UOB Visa Infinite Metal Card |

|

| + Improvements | – Devaluations |

|

|

Annual Fees and Welcome Gifts

| Card | Annual Fee | Welcome Gift |

| AMEX Plat. Reserve |

S$540 | 2N stay at Fraser properties + dining & lifestyle vouchers 🔁 Recurring |

| Citi Prestige 🥇 Winner 🥇 |

S$540 | 25,000 miles 🔁 Recurring |

| DBS Vantage |

S$594 | 25,000 miles 🔁 Recurring |

| HSBC Visa Infinite |

S$656.08 (S$492.56 for HSBC Premier) |

35,000 miles |

| Maybank Visa Infinite |

S$600 (1st yr. free) |

None |

| OCBC VOYAGE |

S$492.50* |

15,000 miles 🔁 Recurring |

| SCB Visa Infinite |

S$594 | 35,000 miles |

| UOB VI Metal Card |

S$648 | 25,000 miles 🔁 Recurring |

| *Alternative option: Pay S$3,240 for 150,000 miles | ||

If you want to join the $120K club, you’d better get used to the idea of paying annual fees- and not insignificant ones. The annual fee for a $120K card ranges from $493 to S$656, and it’ll only get more expensive in 2024 when GST goes up to 9%.

| 💸 Annual Fee Waiver? |

|

While $120K cards generally don’t provide annual fee waivers, there are a few exceptions:

|

On the bright side, most $120K cards cushion the blow by offering miles in exchange for the annual fee.

- The Citi Prestige, DBS Vantage, OCBC VOYAGE, and UOB VI Metal Card offer bonus miles each year the annual fee is paid

- The HSBC Visa Infinite and StanChart Visa Infinite offer bonus miles only in the first year, as a one-time welcome gift. No miles are officially given upon renewal, but unofficially, customers who call up and complain are sometimes placated with 20,000-25,000 miles (YMMV)

- The AMEX Platinum Reserve does not offer miles with the annual fee, but renewing members receive another 2N Fraser Hospitality voucher upon renewal, plus other dining and spa vouchers

- The Maybank Visa Infinite does not offer miles with the annual fee, but waives the first year’s fee while still including an unlimited-visit Priority Pass

If we’re just looking at the first year, the winner would be the HSBC Visa Infinite. Cardholders receive 35,000 miles in exchange for a S$492.56 annual fee, which works out to 1.41 cents per mile. However, this only applies if you’re a HSBC Premier customer (min. AUM: S$200,000). For regular customers, the annual fee is a much higher S$656.08, or 1.87 cents per mile. In that case, the Standard Chartered Visa Infinite would offer cheaper miles at 1.70 cents per mile.

But my opinion is that we should look at this on an recurring basis, and in that case the Citi Prestige offers the best deal: S$540 for 25,000 miles, or 2.16 cents each. 2.16 cents per mile may sound expensive, but remember: you’re not just buying miles with the annual fee, you’re buying other benefits like lounge access that need to be factored into the equation as well.

Earn Rates

| Card | Local | FCY | Min. Spend for Points |

| AMEX Plat. Reserve |

0.69 mpd | 0.69 mpd | S$1.60 |

| Citi Prestige |

1.3 mpd^ | 2.0 mpd^ | S$1 |

| DBS Vantage |

1.5 mpd | 2.2 mpd | S$1.34 (SGD) S$0.91 (FCY) |

| HSBC Visa Infinite |

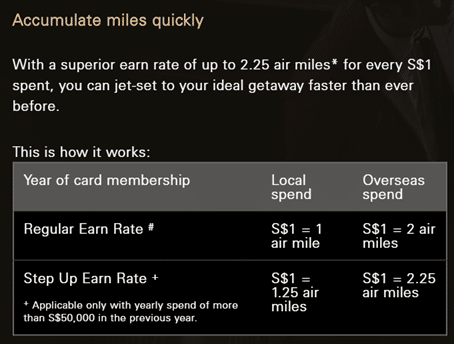

1.25 mpd* | 2.25 mpd* | S$0.50 |

| Maybank Visa Infinite |

1.2 mpd | 2.0 mpd | S$5 |

| OCBC VOYAGE |

1.3 mpd |

2.2 mpd | S$5 |

| SCB Visa Infinite 🥇 Winner 🥇 |

1.4 mpd# | 3.0 mpd# | S$0.20 |

| UOB VI Metal Card |

1.4 mpd | 2.4 mpd | S$5 |

| ^Additional 0.02 to 0.12 mpd awarded based on tenure with bank *With minimum S$50K spend in previous membership year. Otherwise (or if first year), 1 mpd for local, 2 mpd for overseas #With minimum S$2K spend per statement month. Otherwise 1 mpd for both |

|||

For the record: you shouldn’t be spending a lot on your $120K card, because of the opportunity cost involved. Think about it: every dollar you put on your $120K card is a dollar that doesn’t go towards a specialised spending card. And with specialised spending cards earning 4-6 mpd, that is a lot of foregone miles.

But fine. For argument’s sake, in this section we’ll take the perspective of someone who does spend regularly on their $120K card (maybe you’re such a big spender you’ve busted your bonus caps already).

If that describes you, then the StanChart Visa Infinite would be the best bet with its 1.4/3 mpd earn rates for local/overseas spend. However, we need to put a big asterisk on that because those rates only apply if you spend at least S$2,000 per statement month. Fail to do so, and it’s a pitiful 1 mpd across the board.

If you don’t want to bother with minimum spends, the next best would be the UOB VI Metal Card, which since June 2023 has earned 1.4/2.4 mpd for local/overseas spend.

| 💳 OCBC Premier VOYAGE |

| It’s worth mentioning that if you qualify for an OCBC Premier VOYAGE (min AUM: S$200,000), you’ll enjoy earn rates of 1.6/2.3 mpd for local/overseas spend. |

But the UOB VI Metal Card has UOB’s annoying S$5 earning blocks. That means miles lost due to rounding, especially if the typical transaction size on your $120K card is <S$50. Should that be a problem, consider the DBS Vantage Card as an alternative. While it no longer offers 4 mpd for petrol or dining, you still earn 1.5/2.2 mpd on local/overseas spend, with smaller earning blocks than UOB.

I’m not so hot about the HSBC Visa Infinite, which requires cardholders to spend at least S$50,000 in the previous membership year to unlock its 1.25/2.25 mpd rates. Fail to hit that (or if it’s the first year), and the earn rate is a ho-hum 1/2 mpd. And even if you unlock the higher earn rate, think of all the opportunity cost involved with putting S$50,000 on a general spending card!

However, the HSBC Visa Infinite does have a trick up its sleeve: the Everyday Global Account (EGA). This offers an additional 1% cashback on card spend, subject to the following conditions:

- Depositing the following fresh funds into an EGA each calendar month:

- HSBC Personal Banking: S$2,000

- HSBC Premier: S$5,000

- Performing at least five eligible transactions of any amount each calendar month on their card

Eligible transactions simply refer to anything not on the exclusions list (Point 3 of T&Cs), such as GrabPay top-ups, government transactions, insurance premiums, utilities bills. All other retail spend (e.g. dining, groceries, clothing and apparel) is fair game.

Cardholders who meet the eligibility criteria will earn 1% cashback, capped at S$300 per month for HSBC Personal Banking and S$500 per month for HSBC Premier. That sweetens the deal somewhat, though not enough to turn it into the winner.

At the bottom of the heap is the AMEX Platinum Reserve with an anaemic 0.69 mpd earn rate on local and overseas spending. Spending at 10Xcelerator partners does qualify for 3.47 mpd, however, and American Express has the fewest rewards restrictions of any bank in Singapore. You could earn miles on government transactions, education and charitable donations, assuming AMEX cards are accepted.

Points Flexibility and Expiry

| Card | Expiry | Xfer Partners (Fee) |

Min Xfer* |

Pool |

| AMEX Plat. Reserve 🥇 Winner 🥇 |

N/A | 11 (Free) |

250 miles | Yes |

| Citi Prestige |

N/A | 11 (S$27) |

10K miles | No |

| DBS Vantage |

3 yrs. | 4 (S$27) |

10K miles | Yes |

| HSBC Visa Infinite |

37 mo. | 2 (S$43)^ |

10K miles | No |

| Maybank Visa Infinite |

N/A | 4 (Free) |

10K miles | Yes |

| OCBC VOYAGE |

N/A | 1 (S$25) |

1 mile | No |

| SCB Visa Infinite |

N/A | 10 (S$27) |

10K miles | No |

| UOB VI Metal Card |

2 yrs. | 3 (Free) |

10K miles | Yes |

| ^An annual fee that covers unlimited transfers during a 12-mth period *Refers to KrisFlyer, min. blocks may be different for other frequent flyer programmes |

||||

Quantity of points is one thing; quality is another. All things equal, credit card points are more valuable if they:

- don’t expire

- can be transferred to multiple airline partners

- don’t incur conversion fees

- have smaller minimum transfer blocks

- pool with other cards

Based on this criteria alone, the AMEX Platinum Reserve would be the winner. It has non-expiring points, a wide variety of transfer partners, no transfer fees, and a minimum transfer of just 250 miles. And if you have other cards that earn Membership Rewards, your points will be pooled together for redemptions.

But the problem with Membership Rewards points is that they’re high quality and low quantity. I’d love to have a ton of them, but with AMEX’s measly earn rates, that’s a tall order!

In that sense, the Citi Prestige may be a more realistic option. Even though it carries a S$27 transfer fee, ThankYou points never expire and can be transferred to 11 different partners. You can also accumulate low-cost points via the PayAll feature (see next section).

But the Citi Prestige has one major weakness: ThankYou points don’t pool. This means that those of you using the Citi Rewards Mastercard and Citi Rewards Visa will be paying up to three different conversion fees, not to mention three different minimum blocks.

If all you care about is Asia Miles and KrisFlyer, then the UOB VI Metal Card would be a better pick. Since UNI$ pool, you can use the UOB VI Metal Card to anchor a UOB-centric strategy, cashing out UNI$ earned on other cards like the UOB Preferred Platinum Visa, UOB Lady’s Card and UOB Visa Signature for free. The main catch is the 2-year expiry of UNI$.

The StanChart Visa Infinite isn’t bad either, but remember, it applies different transfer ratios among its partners (e.g. 2.5 points= 1 mile for KrisFlyer, but 3.5 points= 1 mile for Emirates Skywards), which could be a stumbling block for anyone looking to earn more “exotic” miles.

Free conversions are also offered by the Maybank Visa Infinite, but not the OCBC VOYAGE- these were nerfed earlier this year, replaced with a standard S$25 fee. OCBC has long been talking about adding eight new airline and hotel transfer partners, but the timeline for this has been perpetually slipping, with a Q2 launch now looking unlikely.

Miles Purchase Facilities

| Card | Buy Miles From | Limit |

| AMEX Plat. Reserve |

N/A | N/A |

| Citi Prestige 🥇 Winner 🥇 |

1 cpm (PayAll) |

Actual bill amount |

| DBS Vantage |

1.67 cpm (Tax payment) |

Actual tax amount |

| HSBC Visa Infinite |

N/A | N/A |

| Maybank Visa Infinite |

N/A | N/A |

| OCBC VOYAGE |

1.9-1.95 cpm (VOYAGE Pay) |

None |

| SCB Visa Infinite |

1.14 cpm (Tax Payment) |

Actual tax amount |

| UOB VI Metal Card |

2.2 cpm (UOB Payment Facility) |

None |

Most $120K cards offer a payment facility, which is basically a way of buying miles at a discount.

To recap, there are two types of payment facilities:

- Those which let you buy as many miles as you want, no questions asked

- Those which let you buy miles provided you have a rental, tax, insurance or some other bill to pay

(1) is available to OCBC VOYAGE and UOB VI Metal Cardholders, with prices hovering around 2 cents per mile. This is certainly cheaper than paying US$40 per 1,000 miles (what SIA charges if you top up when redeeming), but hardly cheap.

(2) is available to Citi Prestige, DBS Vantage and StanChart Visa Infinite Cardholders, with much lower prices.

Do you really need a miles purchase facility, when alternatives like CardUp exist? Perhaps not, unless the price on offer is fantastic- like what Citi Prestige cardholders enjoy.

Citi has been pouring big money into its Citi PayAll bill payment service, and the current promotion (which runs till 20 August 2023) offers 2.2 mpd with a 2.2% admin fee; basically 1 cent per mile.

| 💰 Citi PayAll: Supported Payments | |

|

|

Compared to that, every other option pales in comparison. The StanChart Visa Infinite has a great tax payment facility with miles at 1.14 cents each, yes, but you’re limited by the amount on your NOA. The HSBC Visa Infinite scrapped its tax payment facility earlier this year, and the DBS Vantage offers a so-so rate of 1.67 cents (you’d actually be better off paying via CardUp).

By the way, if you’re looking for the cheapest options for paying income tax with your credit card, have a read of the post below.

Lounge Access

| Card | Lounge Network | Free Visits (Per Year) |

|

| Main | Supp. | ||

| AMEX Plat. Reserve |

N/A | N/A | N/A |

| Citi Prestige 🥇 Winner 🥇 |

Priority Pass | ∞ + 1 guest | N/A |

DBS Vantage DBS Vantage |

Priority Pass | 10 | N/A |

| HSBC Visa Infinite 🥇 Winner 🥇 |

LoungeKey | ∞ | ∞ |

| Maybank Visa Infinite |

Priority Pass | ∞ | N/A |

| OCBC VOYAGE |

Plaza Premium | ∞ | ∞ |

| SCB Visa Infinite |

Priority Pass | 6 | N/A |

| UOB VI Metal Card 🥇 Winner 🥇 |

Dragon Pass | ∞ + 1 guest | N/A |

It’s really hard to pick a winner here.

The way I see it, this is a toss up between the Citi Prestige, HSBC Visa Infinite, and UOB VI Metal Card. All three offer unlimited visits, but…

…in terms of guests:

- Citi Prestige and UOB VI Metal Card both offer one free guest

- HSBC Visa Infinite does not have a guest benefit, but up to five supplementary cardholders enjoy an unlimited-visit LoungeKey

If you travel with different people all the time, the Citi Prestige and UOB VI Metal Card would be better, since your guest could be anyone.

If you travel with the same people (e.g. family), then the HSBC Visa Infinite would let you give each of them a supplementary card with the same lounge benefit you enjoy. This frees them from dependence on you, since they can access the lounge whether or not you’re travelling.

…in terms of network:

Back in July 2021, Plaza Premium announced its shock divorce from the Priority Pass and LoungeKey networks. There were numerous airports where Plaza Premium Lounges were the only contract lounge option, and because of that, every $120K card which relied on Priority Pass or LoungeKey for access automatically became weaker.

Then in June 2023 came a resolution: 63 Plaza Premium Lounges rejoined Priority Pass and LoungeKey, basically erasing the deficit and returning us to pre-July 2021 conditions.

Because of this, there isn’t much to separate the networks:

- Priority Pass and LoungeKey have the same owner, and their benefits are practically identical. Some unique things include non-lounge experiences like dining credits

- Dragon Pass gets access to railways lounges in China, and even though they don’t offer dining credits, you can still redeem set menus at certain airport restaurants

It’s hard to say definitively which network is better, since there will be a lot of overlap. So I’m going to be magnanimous and give the prize to all three.

The other $120K cards all have their drawbacks: Maybank Visa Infinite has no guest allowance or supp. cardholder benefit, OCBC VOYAGE will only get you into Plaza Premium Lounges, which are far from omnipresent, the DBS Vantage and StanChart Visa Infinite are limited to 10 and 6 visits a year.

Airport Limo Transfers

| Card | Qualifying Spend | Cap |

| AMEX Plat. Reserve |

N/A | N/A |

| Citi Prestige |

S$12K per quarter for 2 rides | 2 per quarter |

| DBS Vantage |

N/A | N/A |

| HSBC Visa Infinite 🥇 Winner 🥇 |

S$2K per month for 1 ride* |

24 per year |

| Maybank Visa Infinite |

S$3K per month for 1 ride | 8 per year |

| OCBC VOYAGE |

S$12K per quarter for 2 rides | 8 per year |

| SCB Visa Infinite |

N/A | N/A |

| UOB VI Metal Card |

N/A | N/A |

| *First 2 (Regular customer) or 4 (HSBC Premier) per membership year are free | ||

While lounge access may be murky, we have a clear winner for limo benefits: HSBC Visa Infinite.

By paying the annual fee, cardholders enjoy two complimentary airport transfers per calendar year (four if you’re a HSBC Premier customer), and up to 24 rides per year (including the free ones) can be unlocked with just S$2,000 spend each.

The Maybank Visa Infinite ran a close second last year, but now lags behind because it nerfs its limo benefit from July 2023: S$3,000 now unlocks one ride, instead of two previously.

Everything after that is far from ideal. The Citi Prestige and OCBC VOYAGE both require S$12,000 per quarter for two rides, and the rest of the cards have no benefit at all!

In fact, here’s where a lowly 4 p.m Pioneer Mall UOB PRVI Miles AMEX card excels: all you need to spend is S$1,000 FCY in a calendar quarter to get two free rides.

Travel Insurance

| Card | Accident | Medical | Travel Inc. |

| AMEX Plat. Reserve [Policy Wording] |

S$1M | N/A | Yes |

| Citi Prestige [Policy Wording] |

S$1M | S$50K (+ COVID cover) |

Yes |

| DBS Vantage |

N/A | N/A | N/A |

| HSBC Visa Infinite [Policy Wording] 🥇 Winner 🥇 |

US$2M | S$100K (+ COVID cover) |

Yes |

| Maybank Visa Infinite [Policy Wording] |

S$1M | N/A | Yes |

| OCBC VOYAGE |

N/A | N/A | N/A |

| SCB Visa Infinite [Policy Wording] |

S$1M | S$50K (+ COVID cover) |

Yes |

| UOB VI Metal Card [Policy Wording] |

US$1M | N/A | Yes |

While most $120K cards offer complimentary travel insurance, not all coverage is made equal.

In general, you’ll want to make sure the policy covers three things:

- Death and permanent disability: In case you perish or suffer permanent bodily damage while on your trip

- Medical expenses: In case you need to visit a doctor or a hospital overseas

- Travel inconvenience: Flight delays, lost and damaged luggage

If not, I’d highly advise you to buy a stand-alone insurance policy, because 1 or 2 out of 3 isn’t sufficient. And even if the policy covers all three, it’s your responsibility to make sure the coverage limits are within your risk tolerance.

We don’t have the space here to do a detailed analysis, but based on my cursory reading, the policy offered by the HSBC Visa Infinite has the highest coverage of all. Cardholders are covered for up to US$2 million for accidental death, with S$100,000 of overseas medical expenses (including COVID), S$10,000 of post medical expenses in Singapore, and S$250,000 for emergency medical evacuation.

In terms of travel inconvenience, there’s S$10,000 coverage for trip cancellation, S$5,000 coverage for lost luggage, as well as coverage for loss of travel documents, rental car excess, and personal liability. Coverage even extends to family members travelling on the same trip. If you ask me, this is as good as any stand-alone policy.

Private Club Access

| Card | Private Club Access |

| AMEX Plat. Reserve 🥇 Winner 🥇 |

Tower Club |

| Citi Prestige |

N/A |

| DBS Vantage |

N/A |

| HSBC Visa Infinite |

N/A |

| Maybank Visa Infinite |

N/A |

| OCBC VOYAGE |

N/A* |

| SCB Visa Infinite |

N/A |

| UOB VI Metal Card |

N/A |

| *Premier Private Client and Bank of Singapore versions have Tower Club access |

|

Not much of a contest here, really.

The AMEX Platinum Reserve continues to be the only $120K card with private club access via Tower Club. Bookings can be made through the AMEX concierge, and access is limited to five cardholders per day. All expenses will incur a 10% surcharge, as is Tower Club’s policy for affiliate members.

Although the Straits Bar is a nice place to have a drink, I find the overall Tower Club experience a bit stuffy and overrated. It’s certainly not a decisive factor for choosing a $120K card.

Dining Perks

| Card | Dining Perks |

| AMEX Plat. Reserve 🥇 Winner 🥇 |

|

| Citi Prestige |

|

| DBS Vantage |

|

| HSBC Visa Infinite |

|

| Maybank Visa Infinite |

|

| OCBC VOYAGE |

|

| SCB Visa Infinite |

|

| UOB VI Metal Card |

|

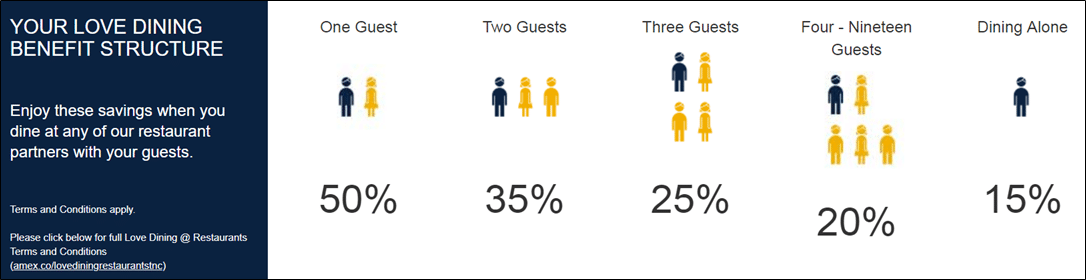

The AMEX Platinum Reserve may not have a lot going for it, but it does offer a solid dining proposition. Cardholders enjoy Love Dining benefits, which offers up to 50% off at a range of hotels and high-end restaurants around Singapore. Love Dining has lost some of its A-list participants over the years, but still offers more than 40 restaurants to choose from.

In addition to this, there’s also Chillax, which gives 1-for-1 drinks at selected bars islandwide. The full list of Love Dining and Chillax partners can be found below:

|

|

AMEX Platinum Reserve cardholders also receive a S$100 Tower Club dining credit plus assorted dining and free wine vouchers.

| 💡 Love Dining Alternative |

| You don’t actually need the AMEX Platinum Reserve to enjoy Love Dining and Chillax benefits; they’re also available on the entry-level AMEX Platinum Credit Card (AF: S$321). |

I don’t think any other card matches up to this, though the HSBC Visa Infinite does a valiant job with its complimentary copy of The Entertainer, which includes 1-for-1 offers at more than 200 dining merchants across Singapore, plus additional deals for use overseas.

This covers a wider range of restaurants than Love Dining, though the savings for Love Dining will always be superior since it’s 50% off all food, while The Entertainer generally offers a 1-for-1 main course.

HSBC Visa Infinite Cardholders also enjoy up to 50% off dining at Fairmont Singapore, Swissotel The Stamford, Marriott Tang Plaza and Goodwood Park Hotel.

DBS Vantage includes an Accor Plus membership that offers up to 50% off food at participating Accor hotel restaurants across Asia Pacific, as well as 15% off drinks. It also has a tie-up with Dining City to offer 15-50% off dining at various restaurants (though the typical discount is much closer to 15-20%).

The UOB VI Metal Card offers 50% off weekday lunch for two diners at Pan Pacific Singapore, PARKROYAL Pickering, Beach Road and Kitchener Road, as well as Si Chuan Dou Hua at UOB Plaza (a 30% discount applies otherwise).

Citi Prestige and OCBC VOYAGE offer periodic celebrity chef dining experiences, which are sometimes offered on a 1-for-1 basis (though the nett price still won’t be cheap).

Weight

What’s the point of having a $120K card if you can’t let the whole world know by dropping it casually on the counter with a fragile-masculinity-assuaging “plonk”?

That is, if your card is actually made of metal like the DBS Vantage, Citi Prestige, OCBC VOYAGE and UOB VI Metal Card. The main change this year is that new VOYAGE cards are issued on heavier cardstock, boosted from 10g to 15g.

| Card | Weight |

| AMEX Plat. Reserve |

~5g |

| Citi Prestige |

8g |

| DBS Vantage |

10g |

| HSBC Visa Infinite |

~5g |

| Maybank Visa Infinite |

~5g |

| OCBC VOYAGE 🥇 Winner 🥇 |

15g |

| SCB Visa Infinite |

~5g |

| UOB VI Metal Card |

9g |

That’s enough to make it the leader of the $120K pack, though still lighter than $500K cards like the UOB Reserve (28g)- there’s always a bigger fish!

Supp. Cardholder Benefits

| Card | Supp. Cards | Perks |

| AMEX Plat. Reserve |

2 free (S$162 after) |

|

| Citi Prestige |

Free |

|

| DBS Vantage |

Free |

|

| HSBC Visa Infinite 🥇 Winner 🥇 |

5 free |

|

| Maybank Visa Infinite |

Free | |

| OCBC VOYAGE |

S$189* |

|

| SCB Visa Infinite |

5 free | |

| UOB VI Metal Card |

1 free (S$290.69 after) |

|

| *First year fee waived for the first two supp. cards | ||

First things first: if anyone you know and love says “sub” card, your duty is to stare at them witheringly until they realise the error of their ways (or perhaps invite them to go for a swap test).

Now that we’ve settled that, it seems to me that the HBSC Visa Infinite takes the title of best supp. card benefits. Up to five supp. cardholders receive an unlimited-visit LoungeKey, free of charge, and they’ll also enjoy the standard dining discounts that principal cardholders get.

OCBC VOYAGE cardholders also get unlimited lounge visits, but this is hamstrung by the fact that (1) only two supp. cards are free, and even then, only for the first year, and (2) the lounge network is the much smaller Plaza Premium Group.

I suppose there’s no harm getting a supplementary Citi Prestige or AMEX Platinum Reserve card too, insofar as it’s a way of sharing GHA Titanium membership or Love Dining perks. But in general, you shouldn’t expect a lot of love for supp. cardholders in this segment.

Unique Perks

In addition to the benefits above, some $120K cards have unique perks which are well worth discussing.

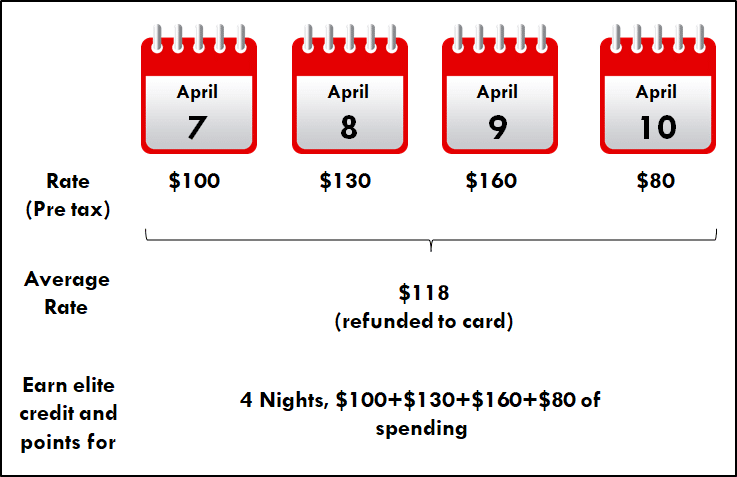

Citi Prestige: Fourth Night Free

The Citi Prestige Card’s ace in the hole is supposed to be its 4th Night Free (4NF) benefit, which, used judiciously, can help cardholders recover large chunks of their annual fee.

With 4NF, principal cardholders can book four nights at a hotel, and get one night refunded to their card (based on the average nightly pre-tax room rate). The refund is done on Citi’s side, so you’ll still earn hotel points and elite credit (where applicable) for four night’s worth of spending.

However, all bookings must be made through the Citi Prestige concierge, and Citi has been tightening the screws on this benefit:

- Only rates that appear on the hotel’s official website or Expedia can be booked

- All rates must be fully prepaid

- You can’t book suites or villas (even if that’s the lead-in category at a hotel)

- You can’t book half or full-board stays

- The rate must be “publicly available”. Even though it costs nothing to sign up for a Hilton/Marriott/Hyatt etc. membership, you won’t be able to enjoy the extra 10% or so they offer to their own members because it’s not a “publicly-available” rate

It’s an unpleasant number of hoops to jump through, but if you’re willing to play ball you can certainly save some money- and because Citi has not capped the 4NF benefit in Singapore (it has in a few other countries), frequent travellers should be able to make the math work.

Citi Prestige: GHA DISCOVERY Titanium

![]()

Citi Prestige Cardholders (both principal and supplementary) enjoy a complimentary upgrade to GHA DISCOVERY Titanium status. This can be done through the Mastercard World Elite concierge.

GHA Titanium status normally requires 30 nights, or US$15K spend, or 3 brands to qualify for. As a reminder, here’s the benefits that DISCOVERY elites can look forward to.

| Gold | Platinum | Titanium | |

| Earn D$ | 5% | 6% | 7% |

| D$ Validity | 18 mo. | 24 mo. | 24 mo. |

| Room Upgrade | – | Single | Double |

| Early Check-in | – | – | From 11 a.m |

| Late Check-out | – | Till 3 p.m | Till 4 p.m |

| Welcome Amenity | – | Yes | Yes |

| Share Status | – | – | Yes |

| Silver is the entry-level GHA tier, with 4% D$ and 6 mo. D$ validity |

|||

DBS Vantage: Accor Plus membership

DBS Vantage Cardholders receive a complimentary Accor Plus Explorer membership, which normally retails for S$418.

This includes perks such as:

- One complimentary hotel night per year

- Up to 50% off dining at participating Accor hotels across Asia Pacific

- 15% off drinks bill in Asia

- 10% off the best available public rate

- Access to Red Hot Room sales with up to 50% off

- Accor Live Limitless Silver status

The free hotel night is obviously a big draw, which can be used at participating hotels in Singapore and across Asia Pacific.

But equally useful are the dining discounts, tiered as follows:

- 25% off dining: 1 member only

- 50% off dining: 1 member and 1 guest

- 33% off dining: 1 member and 2 guests

- 25% off dining: 1 member and 3 guests

- 15% off drinks in Asia

Some examples of participating Accor Plus restaurants in Singapore include Prego, Mikuni and Asian Market Café at the Fairmont, SKAI, The Stamford Brasserie, and CLOVE at Swissotel and The Cliff and Kwee Zeen at the Sofitel Sentosa Resort.

HSBC Visa Infinite: Priority Immigration

HSBC Visa Infinite cardholders who spend at least S$2,000 in a calendar month receive complimentary fast-track immigration service at selected airports for themselves and a guest (in addition to the previously-mentioned free limo ride).

Just like the limo benefit, two complimentary uses are provided each year with no minimum spend (four for HSBC Premier customers).

Depending on the airport, fast-track immigration may also include meet and assist services, which escort you to/from the airplane.

Maybank Visa Infinite: JetQuay access

JetQuay is a private terminal at Changi for CIPs (commercially important people). You get dropped off at a private driveway, your check-in is handled by the terminal staff while you relax in the lounge, and the only time you mingle with the unwashed masses is en route to your flight in an electric buggy.

All that sounds great, but having tried it first hand, I can say it’s rather underwhelming. The JetQuay facility is dated, the food selection is poor, and although the service is excellent, there’s no reason why you should choose it over an airport lounge. Thank goodness there’s plans to transform JetQuay into a “premium travel hub” by 2025 with new interiors and private suites- it can’t happen soon enough!

The full-fledged JetQuay Quayside experience normally costs ~S$432, but Maybank Visa Infinite cardholders can get it for free. Spending S$3,000 a month unlocks a choice of either one limo ride or a single JetQuay use.

Take the limo ride.

OCBC VOYAGE: Redeem miles for any flight

A unique feature of OCBC VOYAGE is that VOYAGE Miles can be used to pay for any flight in any cabin on any airline. It’s conceptually the same as buying a commercial ticket, freeing you from the vagaries of award inventory and waitlisting, plus presenting the opportunity to earn miles and elite status credits on your flight.

The value of a VOYAGE Mile when redeemed for commercial airfares is opaque. However, community-sourced data points suggest it’s around 2.25 cents/mile for Business Class redemptions (it will vary by cabin class as well as destination).

While I can see the value of this feature, what makes me slightly uncomfortable with VOYAGE Miles is that they’re susceptible to unannounced devaluations. Since there’s no official value per mile, the value is whatever OCBC says it is!

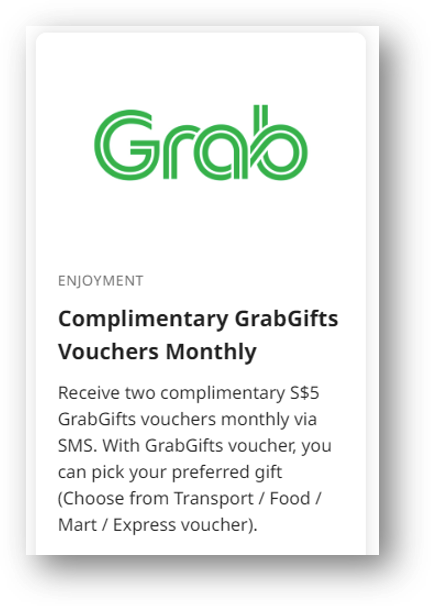

UOB Visa Infinite Metal Card: S$120 annual Grab vouchers

UOB VI Metal Cardholders receive 2x S$5 Grab vouchers every month via SMS, which can be redeemed for Transport, Food, Mart or Express services. Over the course of a year, this adds up to S$120, which helps offset the annual fee.

Of course, whether or not you take those vouchers at face value depends on whether you feel Grab prices are inflated in the first place…

Verdict: Which $120K card?

| 🥊 $120K Credit Card Showdown 🥊 | |

| Category | 🥇 Winner 🥇 |

| Annual Fee & Welcome Gift | Citi Prestige |

| Earn Rates | SCB Visa Infinite |

| Points Flexibility & Expiry | AMEX Plat. Reserve |

| Miles Purchase Facility | Citi Prestige |

| Lounge Access | Citi PrestigeHSBC Visa InfiniteUOB VI Metal Card |

| Airport Limo | HSBC Visa Infinite |

| Travel Insurance | HSBC Visa Infinite |

| Private Club Access | AMEX Plat. Reserve |

| Dining Perks | AMEX Plat. Reserve |

| Weight | OCBC VOYAGE |

| Supp. Cardholder Benefits | HSBC Visa Infinite |

Before we get to the winner, a couple of miscellaneous awards…

📈 Most improved: UOB VI Metal Card

I’ve never been a fan of the UOB VI Metal Card, but credit where it’s due, this card has been buffed in a big way.

Higher earn rates, a much-improved lounge membership, S$120 of annual Grab vouchers, and a rather generous sign-up bonus make it well worth considering, if even for just a year. Even better, you can use it as a conduit to funnel out the rest of your UNI$ without paying any conversion fees.

That’s enough to give it the title of “most improved”, though I guess it helps that they set the baseline so low initially!

📉 Most nerfed: OCBC VOYAGE

The past 12 months have not been kind to the OCBC VOYAGE Card. Cardholders saw their free limo ride entitlement cut from 24 to 8 per year, with the minimum spend hiked from S$5,000 per ride to S$12,000 for two. They lost their free KrisFlyer miles conversions. Those eight new airline and hotel partners have been perpetually delayed.

And while this obviously isn’t within OCBC’s control, the surge in revenge travel has led to a hike in airfares, especially in premium cabins. Given that the value of a VOYAGE Mile has remained the same, this counts as a de facto devaluation of the currency- a reversal of the bumper harvest of premium cabin fare deals we saw in late 2021 (Turkish Airlines round-trip Business Class to Europe for S$1.4K, anyone?).

It’s true that KrisFlyer had a devaluation in July 2022 which affects all the $120K cards, but this represented a price increase (in miles) of 8-16%. In contrast, the cost of premium cabin tickets (in cash) has gone up significantly more.

Hopefully the next 12 months will have more things to cheer.

🏆 Winner: Citi Prestige & HSBC Visa Infinite

Another year, another close fight between the Citi Prestige and HSBC Visa Infinite.

The Citi Prestige offers:

- unlimited lounge visits for the principal cardholder plus a guest

- 4NF benefit, which though troublesome to use, can help cover your annual fee and then some

- the cheapest miles purchase facility in the market, hands down

- 25,000 renewal miles each year

- a wide range of transfer partners

The HSBC Visa Infinite offers:

- lounge access for principal and supplementary cardholders

- 2-4 free airport limo rides and priority immigration clearances per year (plus the lowest qualifying spend requirement at just S$2,000 per ride)

- excellent complimentary travel insurance coverage

- a premium copy of The Entertainer

I’d say the Citi Prestige offers a clearer path to annual fee recovery through its 4NF benefit (provided you don’t mind jumping through hoops) and 25,000 miles each year. However, the HSBC Visa Infinite might be a better option for someone who wants to share benefits with family members, since lounge access applies to supplementary cardholders as well. Don’t underestimate the value of priority immigration clearance either, especially if you’re not flying in premium cabins or don’t have an APEC card.

Conclusion

At the risk of repeating myself: you don’t need a $120K card to play the miles game. If all you want is to accumulate miles as quickly as possible, you’d be better off with the cards I prescribe in my annual card strategy post, most of which are available with an annual income of just S$30,000.

But if you enjoy travelling, dining out, and sampling the finer things in life, a $120K card has the potential to be good value, provided you make regular use of it.

Which $120K card do you fancy the most?

Is there 2024 edition for 120K CC? want to such a premium card soon