Welcome to The MileLion’s Weekly Deal Summary, a round up of all the latest deals and promotions for credit cards, airlines and hotels. Get these posts pushed to your phone by subscribing toour Telegram Channel.

Credit Card/Banking Deals

💳 [Updated] Get Dyson Airwrap Origin, Apple iPad (A16) 11″ Wi-Fi 128GB, or S$390 cash with a new HSBC Advance, HSBC Live+, or HSBC Revolution and min. spend of S$500 by end of month after approval [Expires 30 Jun 25]

💳 AMEX Platinum Credit Card offering S$250 statement credits (new-to-AMEX) or S$200 statement credits (existing) with a min. spend of S$1,000 within 60 days. Enjoy additional perks like a S$200 annual Lifestyle Credit and a Comoclub C4 membership [Expires 30 Jun 25]

💳 AMEX KrisFlyer Ascend offering new-to-AMEX cardholders 37,600 bonus miles + S$50 with min. S$2,000 spend within 90 days [Expires 30 Jun 25]

💳 StanChart Beyond and Visa Infinite Cards offering S$300 cashback on admin fees for income tax payments, limited to the first 50 customers per month [Expires 30 Jun 25]

💳 SC EasyBill offering S$200 cashback on admin fees for income tax payments, limited to the first 50 customers per month [Expires 30 Jun 25]

💳 DBS Altitude Card offering 5 mpd on in-person overseas spend in Australia, Japan, Malaysia and Thailand. Min. spend of S$2,000 in SGD/FCY required, capped at S$1,200 of FCY spend [Expires 30 Jun 25]

💳 Get up to 33,600 bonus miles with a new HSBC TravelOne Card and a minimum spend of S$1,000 [Expires 30 Jun 25]

💳 Get 50,000 miles with a new StanChart Visa Infinite Card and a minimum spend of S$2,000 within 60 days of approval, for both new-to-bank and existing customers [Expires 30 Jun 25]

💳 Get up to 30,000 miles & Samsonite Straren Spinner 67/24, 12,000 Max Miles, S$250 Shopee vouchers or S$180 cash when you sign-up for a StanChart Journey Card and spend S$800 within 60 days of approval. For new-to-bank customers only [Expires 30 Jun 25]

💳 Get up to S$80 Grab vouchers, Accor Plus Explorer membership, Samsonite luggage, and bonus miles or points with the purchase of AMEX MyTravel Insurance [Expires 30 Jun 25]

💳 UOB Visa Infinite Metal Card offering up to 80,000 miles for new sign-ups with S$4,000 spent within 30 days of approval and payment of S$654 annual fee [Expires 30 Jun 25]

💳 HSBC Premier Mastercard offering uncapped 1.8 mpd on selected SGD spend, and uncapped 2.8 mpd on all FCY spend [Expires 30 Jun 25]

💳 OCBC Rewards Card offering 6 mpd on department stores and Watsons, capped at S$1,000 per month [Expires 30 Jun 25]

💳 StanChart Beyond Card offering 100,000 miles welcome bonus with payment of annual fee and S$20,000 spend in the first 90 days of approval [Expires 30 Jun 25]

💳 DBS yuu Cards offering S$300 cashback to new-to-bank customers who spend S$800 within first 60 days of approval [Expires 31 Jul 25]

💳 Get 16,000 miles with a new Citi Rewards Card and S$800 min. spend in the first 2 months. Must be new-to-bank [Expires 31 Jul 25]

💳 [New] HSBC Premier Mastercard offering 65,000 miles welcome bonus with min. spend of S$4,000, for both new and existing HSBC customers [Expires 15 Aug 25]

💳 Buy unlimited miles from 1.7-2.2 cents each with the UOB Payment Facility [Expires 31 Aug 25]

💳 DBS Vantage Card offering 60,000 bonus miles with min. spend of S$4,000 in 30 days, for new-to-bank customers [Expires 31 Aug 25]

💳 DBS Altitude Cards offering 28,000 bonus miles with min. spend of S$800 in 30 days, for new-to-bank customers [Expires 31 Aug 25]

💳 Pay your income taxes with CardUp and Visa cards with a 1.75% fee using the code MLTAX25R [Expires 31 Aug 25]

💳 Pay your income taxes with CardUp and Mastercard with a 1.55% (new) or 1.67% (existing) fee using the code MCTAX25N or MCTAX25. Limited redemptions [Expires 31 Aug 25]

💳 CardUp offering 1.79% admin fee with promo code SAVERENT179 for all rental payments. Not valid for AMEX cards [Expires 31 Jan 26]

💳 CardUp offering 2.25% admin fee with the promo code OFF225 for all payments. Not valid for AMEX cards [Expires 31 Jan 26]

💳 CardUp offering 1.55-2% admin fees for OCBC credit cards, buy miles from 0.95 cents each [Expires 31 Mar 26]

💳 UOB One Account offering 6% rebate on tax payments made through GIRO [Expires 31 Mar 26]

Airline Deals

✈️ [New] Pelago offering 35% off KrisFlyer miles redemptions, or 1.03 cents each [Expires 30 Jun 25]

✈️ KrisFlyer Spontaneous Escapes: Save 30% off selected Economy, Premium Economy and Business Class awards for travel between 1-31 July 2025 [Expires 30 Jun 25]

🏨 Mastercard World and World Elite cardholders enjoy instant I Prefer Titanium status, with an extra 25,000 points on your first stay for World Elite [Expires 30 Jun 25]

🏨 World of Hyatt offering instant Explorer status for 90 days, with further upgrade to Globalist with 20 qualifying nights during this period. For employees of selected companies only [Expires 31 Dec 25]

🏨 Enjoy a 12-month upgrade to elite status with ONYX Rewards via Mastercard [Expires 31 Dec 25]

🏨Hilton status match: Get instant Hilton Gold for 90 days, with fast-track to Diamond. Status valid till 31 March 2026, existing status with competing chain required [No expiry]

Singapore Airlines recently announced that from 1 July 2025, the value of a KrisFlyer mile would be standardised at 1 cent across all its platforms. Whether you’re paying for Singapore Airlines or Scoot tickets, KrisShop purchases, Pelago experiences or Kris+ transactions, the same rate of 100 miles = S$1 will apply.

This seemed like especially great news for Kris+. Not only would the value of existing KrisPay miles appreciate by 50% overnight (up from the current 150 miles = S$1), it would also mean a commensurate increase in rebates. The top earning band of 9 mpd, for instance, would soon be a 9% rebate— before even factoring in the value of credit card miles!

Unfortunately, it’s not quite going to play out that way, because Kris+ has just announced a major nerf in earn rates across the board. While it’s hard to calculate exact numbers, by my estimates more than 250 merchants will be reducing their earn rates come July and, I suspect, more to come in subsequent months.

Get S$5 (in the form of 750 KrisPay miles) when you sign-up with code W644363 and make your first transaction

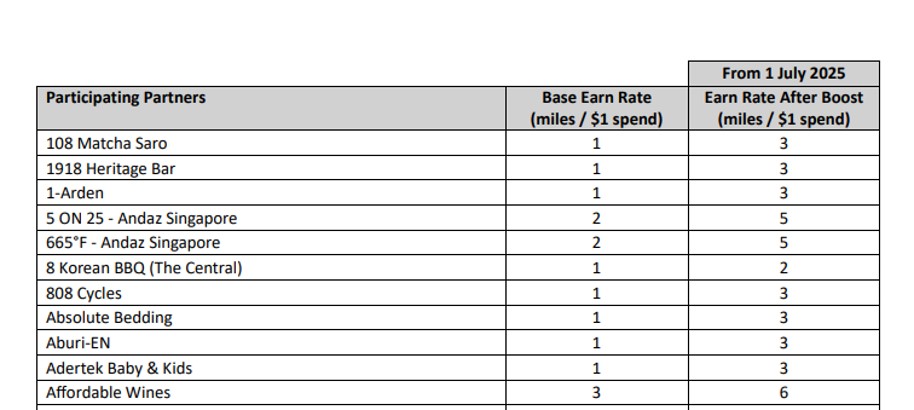

Kris+ cutting earn rates at more than 250 merchants

Club5 at PARKROYAL Beach Road- one of 250+ merchants cutting earn rates from 1 July 2025

Kris+ has published an updated list of merchants and earn rates that takes effect from 1 July 2025, which I’ve parsed into the table below and compared with the previous version (dated 1 November 2024).

📱 Summary: Kris+ Earn Rates

Earn Rate

At 1 Nov 24

At 1 Jul 25

9 mpd

95

4

6 mpd

114

48

5 mpd

4

74

4 mpd

27

47

3 mpd

153

158

2 mpd

8

135

1.5 mpd

0

1

1 mpd

19

29

0.5 mpd

1

2

0.33 mpd

0

3

⚠️ Be careful when reading the document!

The PDF that Kris+ publishes is very misleading. On first glance, you might think “Yay! Everything’s going up!”

On closer inspection, however, you’ll realise the left column shows the base rate, and not the “before” rate you’re earning now. The base rate is practically irrelevant to the consumer; all you care about is what you’re earning now, and what you’ll earn going forward.

For example, the way Affordable Wines is shown in the table suggests it’s increasing from 3 mpd to 6 mpd, when in reality it’s decreasing from 9 mpd to 6 mpd!

Now, before we compare the numbers, I want to highlight a problem. We only have snapshot views of the Kris+ merchant ecosystem, based on how often Singapore Airlines decides to publish an updated list.

In the period between 1 November 2024 and 1 July 2025, there would be new joiners and leavers, and existing merchants might also have had “off-cycle” earn rate adjustments. This introduces noise into the data, but short of maintaining an auto-updating list (and if anyone knows how to do that, I’m all ears), I don’t know how to solve it.

That said, we can still get a rough sense of the overall generosity of the Kris+ programme, as measured by average earn rates.

Date

Average Earn Rate

October 2023

6.2 mpd

April 2024

5.8 mpd

August 2024

5.4 mpd

July 2025

3.3 mpd

As you can see, the July 2025 changes will entail a severe cut of about 40%, though perhaps it shouldn’t be a surprise given the rebasing of KrisFlyer mile value (more on that later).

Here’s a full rundown of all the merchants whose earn rates have changed between 1 November 2024 and 1 July 2025.

Merchant

Old Rate

New Rate

5 ON 25 – Andaz Singapore

9 mpd

5 mpd

665°F – Andaz Singapore

9 mpd

5 mpd

Affordable Wines

9 mpd

6 mpd

Alley on 25 – Andaz Singapore

9 mpd

5 mpd

Alma by Juan Amador

9 mpd

6 mpd

Amici Events and Catering

9 mpd

2 mpd

Amò

9 mpd

5 mpd

ANTI:DOTE (Fairmont Singapore)

9 mpd

5 mpd

Asian Market Café (Fairmont Singapore)

9 mpd

5 mpd

Atelier Lounge

9 mpd

4 mpd

Atrium Bar 317

9 mpd

6 mpd

Atrium Restaurant – Holiday Inn Singapore Atrium

9 mpd

6 mpd

BAKALAKI Greek Taverna

9 mpd

5 mpd

Bar Square – Andaz Singapore

9 mpd

5 mpd

BBQ Express

9 mpd

5 mpd

Bratpack

9 mpd

6 mpd

Chokmah

9 mpd

5 mpd

CLOVE

9 mpd

5 mpd

Club 5 (PARKROYAL on Beach Road)

9 mpd

6 mpd

Duomo Ristorante

9 mpd

4 mpd

Eden Restaurant

9 mpd

4 mpd

Farm Frozen

9 mpd

5 mpd

Ginger (PARKROYAL on Beach Road)

9 mpd

6 mpd

GROHE

9 mpd

6 mpd

Herschel Supply Co

9 mpd

6 mpd

Honeymill

9 mpd

6 mpd

JAAN By Kirk Westaway

9 mpd

5 mpd

Janice Wong Singapore

9 mpd

4 mpd

Jiang-Nan Chun – Four Seasons Hotel Singapore

9 mpd

6 mpd

KEVIN SEAH

9 mpd

6 mpd

Kim Choo Kueh Chang

9 mpd

6 mpd

L’Angelus

9 mpd

4 mpd

Les Bouchons

9 mpd

4 mpd

LeVeL33

9 mpd

6 mpd

Li Bai Cantonese Restaurant (Sheraton Towers)

9 mpd

5 mpd

Lime (PARKROYAL COLLECTION Pickering)

9 mpd

6 mpd

Maharaja’s Tailors

9 mpd

6 mpd

Mitsu Sushi Bar

9 mpd

6 mpd

Mr Stork – Andaz Singapore

9 mpd

5 mpd

NOBU Singapore

9 mpd

6 mpd

One-Ninety Bar – Four Seasons Hotel Singapore

9 mpd

6 mpd

One-Ninety Restaurant – Four Seasons Hotel Singapore

9 mpd

6 mpd

Origin Grill (Shangri-La Singapore)

9 mpd

6 mpd

OverEasy

9 mpd

4 mpd

P.S.O. Beach Club

9 mpd

4 mpd

Pastaria Abate

9 mpd

5 mpd

Penhaligon’s

9 mpd

5 mpd

Perk By Kate

9 mpd

5 mpd

Po Restaurant

9 mpd

4 mpd

Prego (Fairmont Singapore)

9 mpd

5 mpd

Restaurant JAG

9 mpd

5 mpd

RISIS

9 mpd

5 mpd

Si Chuan Dou Hua (PARKROYAL on Beach Road)

9 mpd

6 mpd

Si Chuan Dou Hua (TOP of UOB)

9 mpd

6 mpd

Singapore Sidecars

9 mpd

6 mpd

SKAI Bar (Swissôtel The Stamford)

9 mpd

5 mpd

SKAI Restaurant (Swissôtel The Stamford)

9 mpd

5 mpd

SO France Bistro

9 mpd

6 mpd

SO France Market

9 mpd

6 mpd

Solo Ristorante

9 mpd

4 mpd

Southbridge

9 mpd

5 mpd

State Property

9 mpd

5 mpd

Tandoor (Holiday Inn® Singapore Orchard City Centre)

9 mpd

4 mpd

Tapas,24

9 mpd

4 mpd

The 1872 Clipper Tea Co.

9 mpd

6 mpd

The Coconut Club

9 mpd

4 mpd

The Dining Room (Sheraton Towers)

9 mpd

5 mpd

THE EIGHT

9 mpd

5 mpd

The Line (Shangri-La Singapore)

9 mpd

6 mpd

The Par Club Singapore

9 mpd

6 mpd

The Ring Boxing Community

9 mpd

5 mpd

The Spot

9 mpd

5 mpd

The Stamford Brasserie

9 mpd

5 mpd

The White Tiffin

9 mpd

2 mpd

Tian Fu Tea Room

9 mpd

6 mpd

Timbuk2

9 mpd

6 mpd

TONITO Latin American Kitchen

9 mpd

5 mpd

Virtual Room

9 mpd

6 mpd

WAKANUI Grill Dining Singapore

9 mpd

5 mpd

Window on the Park (Holiday Inn® Singapore Orchard City Centre)

9 mpd

4 mpd

Wooloomooloo Steakhouse

9 mpd

5 mpd

Xin Cuisine Chinese Restaurant – Holiday Inn Singapore Atrium

9 mpd

6 mpd

108 Matcha Saro

6 mpd

3 mpd

808 Cycles

6 mpd

3 mpd

Adertek Baby & Kids

6 mpd

3 mpd

AIBI

6 mpd

3 mpd

Alegria Singapore

6 mpd

3 mpd

Andersen’s of Denmark

6 mpd

3 mpd

Anglo Indian Café & Bar

6 mpd

4 mpd

Babynatureco.

6 mpd

2 mpd

Bacha Coffee

6 mpd

3 mpd

Bee Cheng Hiang

6 mpd

3 mpd

Bee Cheng Hiang Grillery

6 mpd

3 mpd

Beppu Menkan

6 mpd

2 mpd

Bynd Artisan

6 mpd

2 mpd

Carv Artisanal Butchery

6 mpd

2 mpd

Cedele

6 mpd

5 mpd

Cheeselads

6 mpd

2 mpd

Chingu Dining

6 mpd

4 mpd

COCA

6 mpd

3 mpd

Coconut Queen

6 mpd

5 mpd

Cycle Project Store

6 mpd

3 mpd

Dancing Crab

6 mpd

5 mpd

Doco Donburi

6 mpd

3 mpd

Douraku Sushi

6 mpd

5 mpd

Dragon Brand Bird’s Nest

6 mpd

2 mpd

EA Detailer

6 mpd

5 mpd

Edith Patisserie

6 mpd

5 mpd

EGA Juice Clinic

6 mpd

3 mpd

Enjoy Eating House and Bar

6 mpd

5 mpd

Evan’s Kitchen

6 mpd

3 mpd

Flipper’s

6 mpd

5 mpd

For the Love of Laundry

6 mpd

2 mpd

Four Seasons Durians

6 mpd

3 mpd

Fried Chicken Master

6 mpd

3 mpd

Gaia

6 mpd

2 mpd

Garrett Popcorn Shops®

6 mpd

3 mpd

Geometry

6 mpd

3 mpd

Georges

6 mpd

2 mpd

Gong Cha

6 mpd

5 mpd

GUESS

6 mpd

3 mpd

Gyutan-Tan

6 mpd

4 mpd

Her Velvet Vase

6 mpd

2 mpd

HipVan

6 mpd

2 mpd

Huggs Coffee

6 mpd

5 mpd

Ikigai Izakaya the Riverwalk

6 mpd

3 mpd

In Good Company

6 mpd

3 mpd

Joy Luck Teahouse

6 mpd

3 mpd

Kam’s Roast

6 mpd

3 mpd

Kazo Singapore

6 mpd

3 mpd

Klarra

6 mpd

2 mpd

Krispy Kreme

6 mpd

3 mpd

Lao Beijing

6 mpd

5 mpd

LeCaine Gems

6 mpd

5 mpd

LingZhi Vegetarian

6 mpd

5 mpd

llaollao

6 mpd

3 mpd

Madame Tussauds SG

6 mpd

3 mpd

Mayer

6 mpd

5 mpd

Menya Kokoro

6 mpd

3 mpd

Mrs Pho

6 mpd

5 mpd

National Gallery Singapore

6 mpd

3 mpd

Neal’s Yard Remedies

6 mpd

2 mpd

Niku Kappo

6 mpd

3 mpd

Ola Beach Club

6 mpd

3 mpd

Old Seng Choong

6 mpd

3 mpd

Paris Baguette

6 mpd

5 mpd

PATISSERIE G

6 mpd

3 mpd

Polar Puffs & Cakes

6 mpd

5 mpd

Prestige Affairs

6 mpd

2 mpd

Sakunthala’s Food Palace

6 mpd

2 mpd

SIMONE PÉRÈLE

6 mpd

5 mpd

Simple Wellness

6 mpd

2 mpd

Slappy Cakes

6 mpd

5 mpd

Smeg

6 mpd

2 mpd

St. Gregory (PARKROYAL COLLECTION Pickering)

6 mpd

3 mpd

St. Gregory (PARKROYAL on Beach Road)

6 mpd

3 mpd

Straits Chinese Restaurant

6 mpd

2 mpd

Sushi Airways

6 mpd

2 mpd

TANOKE

6 mpd

2 mpd

The Experts Sound

6 mpd

2 mpd

The Little Gym Singapore

6 mpd

5 mpd

The Meatery

6 mpd

3 mpd

The Queen’s Pub

6 mpd

3 mpd

Tóng Lè Private Dining

6 mpd

5 mpd

Toss & Turn

6 mpd

5 mpd

TP Tea

6 mpd

3 mpd

Tsuta Japanese Dining

6 mpd

5 mpd

TUNG LOK HEEN

6 mpd

5 mpd

TUNG LOK PEKING DUCK

6 mpd

5 mpd

TUNG LOK SEAFOOD

6 mpd

5 mpd

TUNG LOK SIGNATURES

6 mpd

5 mpd

TUNG LOK TEAHOUSE

6 mpd

5 mpd

TWG Tea

6 mpd

3 mpd

USHIO Sumiyaki & Sake Bar

6 mpd

5 mpd

Vitakids

6 mpd

2 mpd

Waku-Shin Yakiniku Restaurant

6 mpd

2 mpd

WhyQ

6 mpd

3 mpd

Willow Stream Spa

6 mpd

3 mpd

Yakiniquest

6 mpd

4 mpd

Zaffron Kitchen

6 mpd

3 mpd

Kind Kones

5 mpd

4 mpd

Delsey Paris

4 mpd

3 mpd

L’Entrecôte The Steak & Fries Bistro

4 mpd

3 mpd

Riviera

4 mpd

3 mpd

Sabio

4 mpd

3 mpd

TAJINE Moroccan Tapas & Cocktail Bar

4 mpd

3 mpd

Travel Zone

4 mpd

3 mpd

Victorinox

4 mpd

3 mpd

8 Korean BBQ (The Central)

3 mpd

2 mpd

ASAP & Co.

3 mpd

2 mpd

Bangkok Jam

3 mpd

2 mpd

Barossa Steak & Grill

3 mpd

2 mpd

Beauty in The Pot

3 mpd

2 mpd

Benjamin Barker

3 mpd

2 mpd

Bottles & Bottles

3 mpd

2 mpd

Canadian Pizza

3 mpd

2 mpd

Canton Paradise

3 mpd

2 mpd

Capitol Optical

3 mpd

2 mpd

Carrie K.

3 mpd

2 mpd

Cherry & Oak

3 mpd

2 mpd

Chez Vous

3 mpd

2 mpd

Columbia

3 mpd

2 mpd

D’Cuisines Restaurant

3 mpd

2 mpd

De Arte Hair Studio

3 mpd

2 mpd

DrHair

3 mpd

2 mpd

DrSpa

3 mpd

2 mpd

Erabelle

3 mpd

2 mpd

Esso

3 mpd

0.5 mpd

Famous Amos

3 mpd

2 mpd

Fish Mart Sakuraya

3 mpd

2 mpd

Fresver Beauty

3 mpd

2 mpd

G2000

3 mpd

2 mpd

GINLEE

3 mpd

2 mpd

GRT Jewellers

3 mpd

2 mpd

Hansgrohe Singapore

3 mpd

2 mpd

Hook Coffee

3 mpd

2 mpd

iFly Singapore

3 mpd

2 mpd

Ikeda Spa

3 mpd

2 mpd

Joo Bar

3 mpd

2 mpd

Joyre TCMedi SPA

3 mpd

2 mpd

Kenko Wellness Spa & Reflexology

3 mpd

2 mpd

Kinohimitsu

3 mpd

2 mpd

Le Petit Society

3 mpd

2 mpd

Little Island Brewing Co (Gillman Barracks)

3 mpd

2 mpd

Little Island Brewing Co. (Changi)

3 mpd

2 mpd

Little Island Brewing Co. (South Beach)

3 mpd

2 mpd

Love & Co.

3 mpd

0.33 mpd

MANAM

3 mpd

2 mpd

Multiflora TCM Spa

3 mpd

2 mpd

Nailz Treats

3 mpd

2 mpd

Nalan Restaurant

3 mpd

2 mpd

Octapas Spanish Tapas Bar

3 mpd

2 mpd

Orchid Live Seafood

3 mpd

2 mpd

Outdoor Life

3 mpd

2 mpd

Overscoop

3 mpd

2 mpd

Paradise Classic

3 mpd

2 mpd

Paradise Hotpot

3 mpd

2 mpd

Paradise Teochew

3 mpd

2 mpd

Pianoland

3 mpd

2 mpd

QUEIC BY OLIVIA

3 mpd

2 mpd

Royal Sporting House

3 mpd

2 mpd

Ryan’s Kitchen

3 mpd

0.33 mpd

Sake+

3 mpd

2 mpd

SARAI

3 mpd

2 mpd

Scent by SIX

3 mpd

2 mpd

Seafood Paradise

3 mpd

2 mpd

Shunji Matsuo

3 mpd

2 mpd

SK Jewellery

3 mpd

0.33 mpd

Social Place

3 mpd

2 mpd

Spa Rael

3 mpd

2 mpd

Splice Barbershop

3 mpd

2 mpd

Suki-Ya KIN

3 mpd

2 mpd

Sun & Sand Sports (SSS)

3 mpd

2 mpd

Sunday Staples

3 mpd

2 mpd

Swatow Restaurant

3 mpd

2 mpd

SYOUJIN

3 mpd

2 mpd

Tai Cheong Bakery

3 mpd

2 mpd

Tajimaya Yakiniku

3 mpd

2 mpd

Tanglin Cookhouse

3 mpd

2 mpd

Taste Paradise

3 mpd

2 mpd

The Art Nooq

3 mpd

2 mpd

The Assembly Ground

3 mpd

2 mpd

The Café & Bar

3 mpd

2 mpd

The Kind Bowl

3 mpd

2 mpd

Vineyard

3 mpd

2 mpd

This was always inevitable

While no one likes to see a nerf, this really shouldn’t come as a surprise. It was bound to happen once the rebasing of KrisFlyer miles was announced.

Think about it: suppose you’re a merchant who’s currently offering 9 mpd with Kris+ and paying X% commission. If Kris+ increase the value of KrisPay miles by 50%, it can’t be the case that you keep the same earn rates and commissions. Either you pay more to Kris+, or you cut your earn rate proportionately.

In other words, the merchants are rebasing too. For example, we’re seeing a lot of merchants moving from the 9 mpd to 6 mpd category. That’s exactly what you’d expect to see, if the value of a KrisPay mile was increased by 50%.

If your end goal was always to take the miles earned from Kris+ and spend them at other Kris+ merchants, then you probably won’t mind this change too much— though not every rebasing reflects a 50% increase in value (i.e 33% reduction in earning); some merchants have taken the opportunity to cut their earn rates proportionately more.

But let’s be honest: how many people fall into that category? Practically everyone converts the miles earned from Kris+ into KrisFlyer, and in that case, these changes are going to sting something fierce. We’re seeing the number of 9 mpd merchants get cut from 95 to just four, and 6 mpd merchants from 114 to 48.

Mind you, I don’t think this is the end of it. There are approximately 190 merchants whose earn rates have not changed, but I find it hard to believe they’ll be able to maintain those rates for long with the rebasing. My guess is that either this group has contracts with Kris+ that guarantee their current earn rates and commissions for a certain period, or they plan to do “off-cycle” earn rate adjustments.

Earning miles via Kris+

Kris+ miles can be earned at more than 1,500 partner outlets across Singapore

Earning miles at Kris+ merchants is simple. All you need to do is:

Scan the merchant’s Kris+ QR code

Enter the amount to be paid, and press “Pay” to pay via Apple/Google Pay

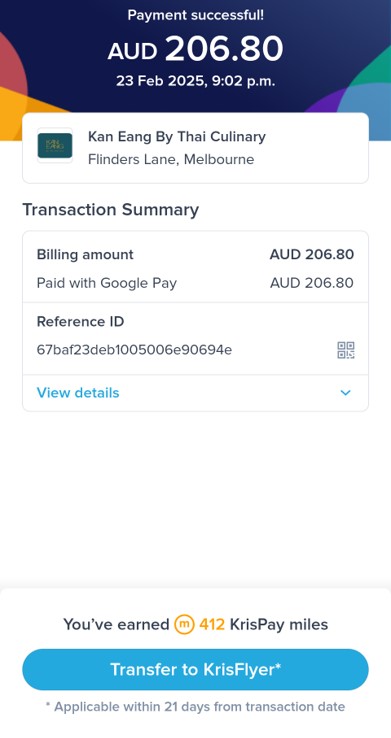

Miles will be credited immediately upon completing the transaction, which makes Kris+ an excellent way of topping up a KrisFlyer balance.

Don’t forget to transfer any KrisPay miles earned to KrisFlyer within 21 days of the transaction, in their entirety. If you wait longer than 21 days, or spend any of the accrued miles, the balance will be stuck in Kris+. Miles in Kris+ expire after six months, and can only be spent at a rate of 150 miles = S$1 (or 100 miles = S$1 from 1 July 2025).

A big “Transfer to KrisFlyer” button appears after every transaction. Alternatively, you can turn on the new auto-transfer feature, which will automatically deposit any miles earned from Kris+ into your KrisFlyer account.

What card should I use with Kris+?

In general, Kris+ retains the MCC of the underlying merchant (though there are some exceptions, most notably for travel agencies), so you can use whatever card you’d normally use for that particular merchant.

When in doubt, the following cards are the safest to use with Kris+, as they earn 3-4 mpd regardless of Kris+ merchant.

However, there are also other cards you can use for dining or retail that will earn up to 4 mpd, such as the HSBC Revolution or UOB Lady’s Cards. Refer to the post below for more details.

From 1 July 2025, Kris+ will cut earn rates at more than 250 partners, all but eliminating the 9 mpd category and reducing average earn rate to an all-time low of 3.3 mpd.

While this is no doubt unpleasant, it’s perhaps not unexpected. It was always going to be necessary to “rebase” the Kris+ earn rates in light of the decision to boost the value of KrisPay miles to 1 cent each, and the adjustments — for the most part— reflect this.

But so long as it costs nothing extra to use Kris+ (and be mindful of opportunity costs, because you can’t stack other promotions like Love Dining), then some miles are better than no miles at all.

You still have a few days more to take advantage of the current earn rates, so try and do some shopping or dining out this weekend if you can. You might also consider buying vouchers from the Kris+ app, to lock in today’s earn rates for future consumption.

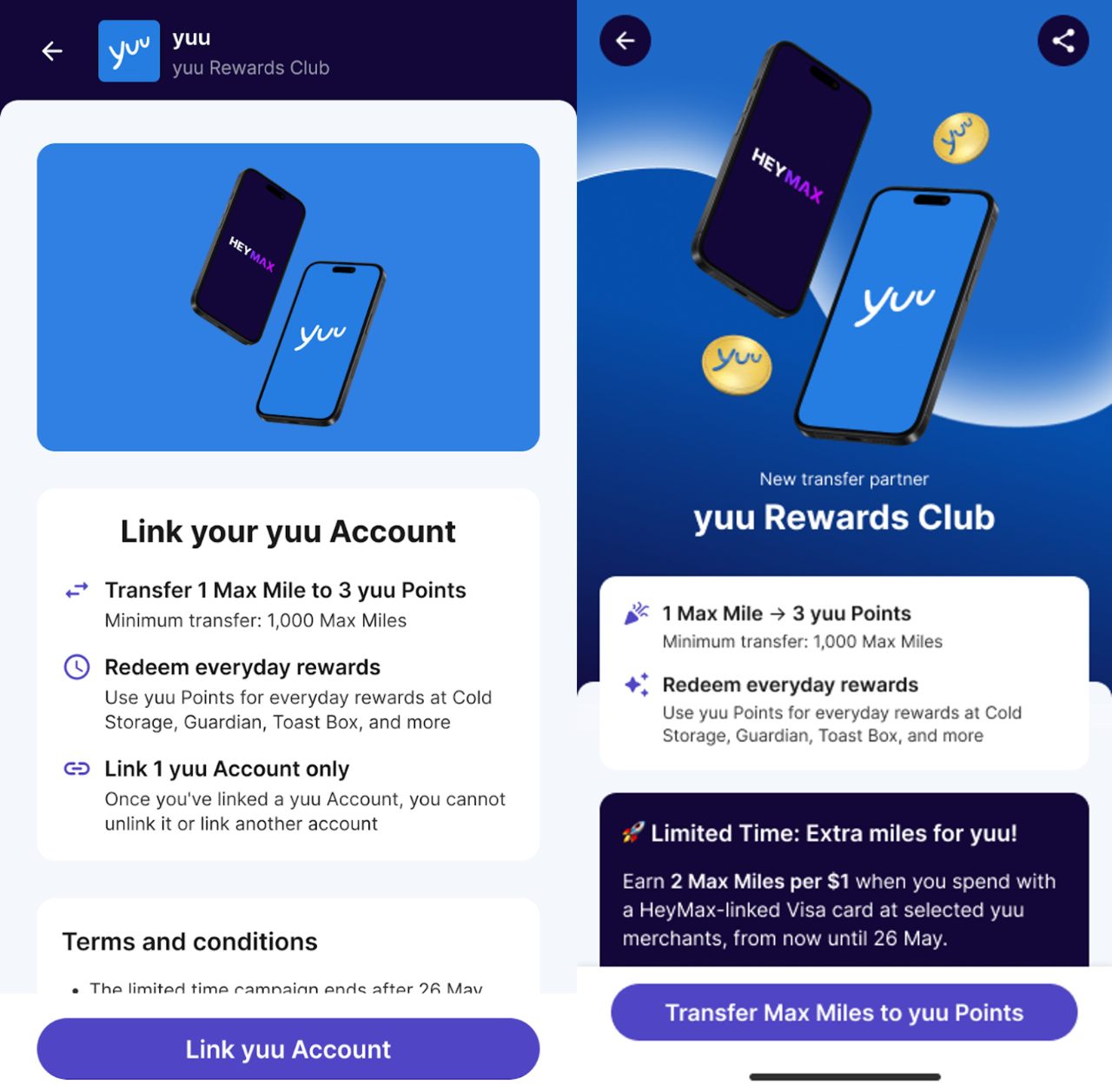

HeyMax has launched the latest edition of Max Miles Day, a monthly promotion which offers 20% milesback on selected redemptions.

This month, like last, users can enjoy 20% milesback on Max Miles to yuu Points conversions and all voucher redemptions. This effectively allows for 1:1 conversions between Max Miles and KrisFlyer miles, though I’d personally prefer to keep my Max Miles for more “exotic” points currencies.

👍 250 Max Miles joining bonus

Sign up for a HeyMax account and get up to 250 Max Miles as a welcome bonus

On Wednesday, 25 June 2025, HeyMax users will enjoy 20% milesback when they convert Max Miles into yuu Points.

As a reminder, Max Miles can be converted into yuu Points at a 1:3 ratio.

A minimum conversion of 1,000 Max Miles is required

All conversions are free of charge

Transfers will be processed within 3-14 working days (instant conversions will be possible in the future)

With 20% milesback, the conversion ratio is boosted to 0.8:3. For example, if you convert 1,000 Max Miles, you’d receive 3,000 yuu Points and a rebate of 200 Max Miles, for a nett outlay of 800 Max Miles.

Milesback is tracked instantly, and will be awarded within seven days. There is no cap on the maximum milesback you can receive.

HeyMax and yuu accounts can be linked via the HeyMax app. Look for the yuu logo on the home screen and follow the instructions. The linking process is instant.

Each HeyMax account can only be linked to one yuu account (which must be your own), and once a yuu account is linked, it cannot be unlinked.

Convert Max Miles to KrisFlyer miles at 1:1 ratio

The HeyMax x yuu partnership creates the possibility of converting Max Miles into KrisFlyer miles, via a two-step process:

Convert Max Miles to yuu Points

Convert yuu Points to KrisFlyer miles

Under normal circumstances, the prevailing conversion ratios would mean 1 Max Mile = 0.83 KrisFlyer miles. But with 20% milesback in play, the ratio becomes 1:1 (technically 1: 1.04 miles).

Max Miles

yuu Points

KrisFlyer Miles

1 mile

3 points

0.83 miles 1 mile

Should you be doing this?

While I’m sure there’ll be many who have eagerly awaited the opportunity to convert Max Miles into KrisFlyer miles, I’m not one of them.

Max Miles can be converted to 28 airline and hotel loyalty programmes at a 1:1 ratio, without any fees.

✈️ HeyMax Airline Partners

Air Canada Aeroplan

Air France-KLM Flying Blue

Air India Maharaja Club

Alaska Mileage Plan

American Airlines AAdvantage

Avianca LifeMiles

British Airways Executive Club

Emirates Skywards

Etihad Guest

EVA Air Infinity MileageLands

Frontier Miles

GarudaMiles

Hainan Fortune Wings Club

Qantas Frequent Flyer

Qatar Privilege Club

THAI Royal Orchid Plus

Turkish Miles&Smiles

United MileagePlus

Vietnam Airlines Lotusmiles

Velocity Frequent Flyer

🏨 HeyMax Hotel Partners

Accor Live Limitless

Hilton Honors

IHG One Rewards

Marriott Bonvoy

Radisson Rewards

Shangri-La Circle

World of Hyatt

Wyndham Rewards

Given this incredible versatility, I feel it’s a waste to convert them into garden variety KrisFlyer miles. You could enjoy Business Class sweet spots to Europe and North America with EVA Air Infinity MileageLands. You could fly First Class to Japan with American AAdvantage. You could accumulate incredibly rare (in Singapore, at least) World of Hyatt points. I could go on— and in fact I have, in this post.

Even if you don’t have a critical mass of Max Miles for a redemption with one of these programmes, Max Miles can also be cashed out for 2 cents each via FlyAnywhere, with a minimum redemption of 1,000 Max Miles. All you need to do is submit a recent commercial air ticket on any airline, to anywhere in the world.

This effectively sets a baseline value for Max Miles, and you shouldn’t be converting them to KrisFlyer unless you value a KrisFlyer mile at more than 2 cents.

But in spite of my protestations, I’m sure there’ll still be those who want to go down the KrisFlyer route. If that’s you, just make sure you get it done today.

20% milesback on voucher redemptions

In addition to yuu Points conversions, HeyMax users will also receive 20% milesback on all voucher redemptions.

The regular value offered for voucher redemptions is 1 cent per Max Mile, so 20% milesback improves that to 1.25 cents.

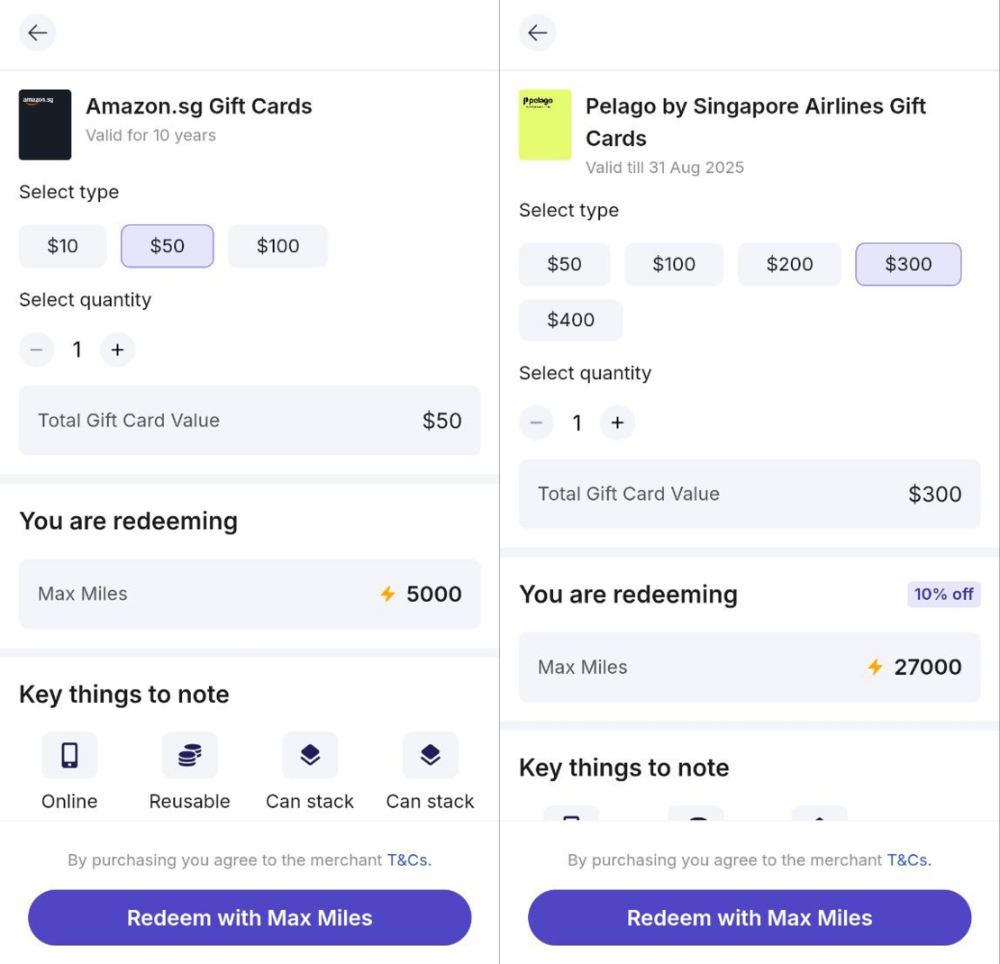

However, HeyMax also offers flash deals on selected vouchers, so you could achieve an even higher value by stacking the two. For example, a S$300 Pelago gift card is currently being offered for 27,000 Max Miles, so with 20% milesback the nett cost is reduced to 21,600 Max Miles, or 1.39 cents each.

Still, I don’t feel this is particularly lucrative, since the presence of FlyAnywhere means that you shouldn’t be accepting anything less than 2 cents per Max Mile.

Conclusion

On 25 June 2025 only, HeyMax users can enjoy 20% milesback on conversions of Max Miles to yuu Points. This also allows for 1:1 transfers between Max Miles and KrisFlyer miles, and if that’s what you want to do, today’s the day to do it.

I would personally rather keep my Max Miles for “exotic” points currencies that are hard (or impossible) to earn with credit cards in Singapore. And even if not, I’d sooner choose to cash them out via FlyAnywhere, since my KrisFlyer mile valuation is lower than the 2 cents I’d otherwise receive.

Users can also enjoy 20% milesback on voucher redemptions, but again there’s little reason to do this with FlyAnywhere offering better value.

Here’s The MileLion’s review of the DBS Altitude Card, which once upon a time was a very solid general spending card.

True, its local/overseas earn rates of 1.2/2 mpd weren’t very exciting, but cardholders could earn 3 mpd on air tickets and hotel bookings, for up to S$5,000 per month. And unlike its competitors, you weren’t forced to book on special OTA portals with inflated pricing and limited selections. Cardholders could book any airline or hotel, any way they wished.

The DBS Altitude comes in two varieties: AmericanExpress, and Visa. The fees, earn rates and benefits of the two are almost identical, though historically speaking, the American Express had a more generous welcome offer than the Visa (at the time of writing, there’s no such differentiation).

The main advantage the Visa has is two airport lounge visits per year, which the American Express version lacks.

How much must I earn to qualify for a DBS Altitude Card?

The DBS Altitude has a minimum income requirement of S$30,000 per year, the MAS-mandated minimum.

If you don’t meet the minimum income requirement, you can place a S$10,000 fixed deposit with DBS and get a secured version of the card. Visit any DBS branch for further information.

🤓 History Lesson

The DBS Altitude Card can probably take credit for democratising the miles game, because once upon a time, the minimum income requirement for any miles card was S$80,000, well beyond the reach of most fresh graduates.

Then in 2016, DBS became the first bank in Singapore to offer a miles card at the MAS-mandated minimum of S$30,000. This put pressure on the rest of the market, and eventually the Citi PremierMiles and UOB PRVI Miles Cards reduced their income requirements to S$30,000 as well.

How much is the DBS Altitude Card’s annual fee?

Principal Card

Supp. Card

First Year

Free

Free

Subsequent

S$196.20

S$98.10

The DBS Altitude Card has an annual fee of S$196.20 for the principal cardholder, and a S$98.10 fee per supplementary card.

The first year’s fee is waived. Subsequent years’ fees are automatically waived if you spend at least S$25,000 in a membership year, though based on personal experience, it is possible to get a fee waiver even if you don’t meet the minimum spend.

Cardholders will receive 10,000 miles (in the form of 5,000 DBS Points) every year they pay the principal card’s annual fee, which is equivalent to buying miles at 1.96 cents each.

If the annual fee is subsequently waived, these DBS Points will be clawed back. Should you have an insufficient balance (because you already redeemed those points), then you’ll be charged S$0.0388 per DBS Point.

Base Miles From S$800 Spend (1.3 mpd local, 2.2 mpd FCY)

1,040 – 1,760 miles

Miles From S$196.20 Annual Fee

10,000 miles

Fee waived

Total Miles

39,040- 39,760 miles

29,040- 29,760 miles

DBS is currently offering a 28,000 miles welcome bonus for new-to-DBS cardholders, defined as those who:

do not currently hold any principal DBS/POSB credit cards, and

have not cancelled any principal DBS/POSB credit cards in the past 12 months

Customers must apply for a DBS Altitude Card between 1 March and 31 August 2025, and receive approval by 14 September 2025. They must also spend at least S$800 within 60 days of approval, which will earn:

28,000 bonus miles

1,040 to 1,760 base miles, depending on how the S$800 spend is split between SGD/FCY

On top of this, there is the option of paying the first year’s S$196.20 annual fee for an extra 10,000 miles. This needs to be indicated at the time of application via a promo code:

ALT38: If you wish to pay the first year’s annual fee

ALTW28: If you wish to have a first year fee waiver

Make sure to enter one code or the other. No code, no bonus!

There’s nothing stopping you from signing up for both the DBS Altitude AMEX and DBS Altitude Visa cards. However, you will only enjoy the new-to-bank bonus on the first card that’s approved.

How many miles do I earn?

🇸🇬 SGD Spend

🌎 FCY Spend

⭐ Bonus Spend

1.3 mpd

2.2 mpd

N/A

SGD/FCY Spend

DBS Altitude Card members earn:

3.25 DBS Points for every S$5 spent in Singapore Dollars (SGD)

5.5 DBS Points for every S$5 spent in foreign currency (FCY)

1 DBS Point is worth 2 airline miles, so that’s an equivalent earn rate of 1.3 mpd for SGD spending, and 2.2 mpd for FCY spending. These are acceptable rates for a general spending card, though certainly not market-leading.

💳 Earn Rates for General Spending Cards (income req.: S$30K)

Cards

Local Spend

FCY Spend

UOB PRVI Miles Card

1.4 mpd

3 mpd IDR, MR, THB, VND 2.4 mpd All Others

HSBC TravelOne Card

1.2 mpd

2.4 mpd

DBS Altitude Card

1.3 mpd

2.2 mpd

OCBC 90°N Card

1.3 mpd

2.1 mpd

Citi PremierMiles Card

1.2 mpd

2 mpd

StanChart Journey Card

1.2 mpd

2 mpd

AMEX KrisFlyer Ascend

1.2 mpd

1.2 mpd

AMEX KrisFlyer Credit Card

1.1 mpd

1.1 mpd

BOC Elite Miles Card

1 mpd

2 mpd

KrisFlyer UOB Credit Card

1.2 mpd

1.2 mpd

All foreign currency transactions on the DBS Altitude AMEX and Visa Cards are subject to a 3% and 3.25% FCY fee respectively. Therefore, using your DBS Altitude Card overseas represents buying miles at 1.36 cents (AMEX) and 1.48 cents (Visa).

💳 FCY Fees by Issuer and Card Network

Issuer

↓ MC & Visa

AMEX

Standard Chartered

3.5%

N/A

American Express

N/A

3.25%

Citibank

3.25%

N/A

DBS

3.25%

3%

HSBC

3.25%

N/A

Maybank

3.25%

N/A

OCBC

3.25%

N/A

UOB

3.25%

3.25%

BOC

3%

N/A

CIMB

3%

N/A

When are DBS Points credited?

DBS Points for local and overseas spending will be credited when your transaction posts, which generally takes 1-3 working days.

But DBS’s calculations aren’t nearly as penalising. Here’s how the DBS Points on your DBS Altitude Card are calculated:

Local Spend

Divide transaction by 5 and multiply by 3.25. Round down to the nearest whole number

FCY Spend

Divide transaction by 5 and multiply by 5.5. Round down to the nearest whole number

Notice how the transaction is not rounded down to the nearest S$5; instead, it’s divided by 5 straight away. This means the minimum spend to earn points is not S$5, but rather:

SGD spend: S$1.54

FCY spend: S$0.91

To illustrate the point, here’s how the DBS Altitude compares to the UOB PRVI Miles. Note how it outperforms the ostensibly higher-earning PRVI Miles (1.4 mpd) on certain transaction sizes.

DBS Altitude Earn rate: 1.3 mpd

UOB PRVI Miles Earn rate: 1.4 mpd

S$5

6 miles

6 miles

S$9.99

12 miles

6 miles

S$15

18 miles

20 miles

S$19.99

24 miles

20 miles

S$25

32 miles

34 miles

S$29.99

38 miles

34 miles

If you’re an Excel geek, here’s the formulas you need to calculate points:

Local Spend

=ROUNDDOWN ((X/5)*3.25,0)

FCY Spend

=ROUNDDOWN ((X/5)*5.5,0)

Where X= Amount Spent

For the full list of formulas that banks use to calculate credit card points, refer to these articles:

The DBS Altitude Card will not earn points on the following transactions:

Amaze transactions (not that it matters here, because only Mastercards can be paired with Amaze)

Charitable donations

Education

Government institutions and services

Hospitals

Insurance

Top-ups of prepaid accounts e.g. GrabPay

Utilities bills

A full list of transactions that do not earn DBS Points can be found at point 2.6 of the DBS Rewards Programme’s T&Cs.

All CardUp transactions are eligible to earn DBS Points. However, when it comes to qualifying spend for the purposes of welcome offers, only CardUp rental transactions which code under MCC 6513 (Real Estate Agents and Managers) will count.

If you plan to use CardUp to meet the qualifying spend for a welcome offer, do read the article below for greater clarity.

ipaymy transactions are explicitly excluded from counting towards qualifying spend.

What do I need to know about DBS Points?

❌ Expiry

↔️ Pooling

💰 Transfer Fee

No expiry

Yes

S$27.25 (per conversion) or

S$43.60 (per year)

⬆️ Min. Transfer

✈️ No. of Partners

⏱️ Transfer Time

5,000 DBS Points (10,000 miles)

4

1-3 working days (for KF)

Expiry

DBS Points normally expire after one year, but points earned on the DBS Altitude Card never expire.

Pooling

DBS Points pool across cards for the purposes of redemption.If you have 10,000 DBS Points on the DBS Altitude Card and 5,000 DBS Points on the DBS Woman’s World Card, you can redeem 15,000 DBS Points at one shot and pay a single conversion fee.

However, DBS Points are not pooled when it comes to card cancellations. If I have a DBS Altitude Card and DBS Woman’s World Card and decide to cancel the former, I’ll need to transfer my points out before cancelling, or else forfeit them.

Partners and Transfer Fee

DBS partners with four frequent flyer programmes, though it’s arguably three because Air Asia Rewards offers such poor value it might as well not exist.

Frequent Flyer Programme

Conversion Ratio (DBS Points: Miles)

5,000: 10,000

5,000: 10,000

5,000: 10,000

500: 1,500

For KrisFlyer specifically, DBS offers an alternative “Auto Conversion programme”. This charges a flat fee of S$43.60 per membership year, and automatically converts DBS Points to KrisFlyer miles each calendar quarter in blocks of 500 DBS Points.

This reduces the minimum transfer block from 10,000 miles to 1,000 miles, but has the downside of starting the three-year expiry on your KrisFlyer miles early.

Whether the Auto Conversion programme makes sense depends on your miles transfer patterns. If you make only one transfer to KrisFlyer per year, the “per transfer” model of S$27.25 would make more sense. However, if you find yourself making two or more transfers, the Auto Conversion programme would be better.

Cardholders enrolled in the Auto Conversion scheme can make ad-hoc conversions from DBS Points to KrisFlyer miles without paying the usual S$27.25 fee, but the usual minimum block of 5,000 DBS Points applies.

💡Protip: Alternative to miles?

While I normally would advise against redeeming DBS Points for anything other than miles, the bank runs a monthly promotion that offers extra value for selected voucher redemptions. You can usually get around 1.8 cents per mile, which might interest you if you have orphan points.

Transfer Times

DBS quotes a points conversion time of 1-2 weeks, but in reality it usually takes about 1-3 working days at the very most for KrisFlyer (transfer times to other programmes may be longer).

If you need your points credited instantly, you can do so via Kris+. 100 DBS Points can be instantly transferred to 170 KrisPay miles, which can then be converted to KrisFlyer miles at a 1:1 ratio with no fees.

Get S$5 (in the form of 750 KrisPay miles) when you sign-up with code W644363 and make your first transaction

However, those 100 DBS Points would normally have earned you 200 KrisFlyer miles, so you effectively take a 15% haircut. Therefore, I wouldn’t recommend taking this option, unless you need a small top-up to redeem a flight, or have an orphan DBS Points balance (<5,000 points).

If you choose to do so nonetheless, do remember that it’s a two-step process:

Transfer DBS Points to KrisPay miles

Transfer KrisPay miles to KrisFlyer miles

Do not forget the second step! If you wait more than 21 days, or spend any of the converted KrisPay miles via Kris+, the entire balance will be stuck in the Kris+ app. KrisPay miles expire after six months, and can only be spent at a poor ratio of 150 miles = S$1.

Principal DBS Altitude Visa Cardholders enjoy two free Priority Pass lounge visits per membership year.

The two visit allowance is tracked by membership year, based on when they applied for their Priority Pass. Lounge entitlements can be shared with a guest, but once you exhaust your free visits you’ll be charged US$32 per additional visit.

Here’s how this compares to other cards in its segment.

Card

Network

Free Lounge Visits (per year)

HSBC TravelOne Card

DragonPass

4X* Share

UOB PRVI Miles Card

Priority Pass

4X*

Citi PremierMiles Card

Priority Pass

2X* Share

DBS Altitude Visa

Priority Pass

2X Share

StanChart Journey Card

Priority Pass

2X Share

AMEX KrisFlyer Ascend

N/A

N/A

AMEX KrisFlyer Credit Card

N/A

N/A

BOC Elite Miles Card

N/A

N/A

KrisFlyer UOB Credit Card

N/A

N/A

OCBC 90°N Card

N/A

N/A

*Allowance tracked based on calendar year

Overseas spending promotions

The DBS Altitude Card usually offers two overseas spending promotions each year, to cover the June and December peak travel periods. You can usually expect to see a boosted overseas spend rate of 5 mpd, subject to meeting a certain minimum spend and with an overall earning cap.

Unfortunately, the most recent promotion (which ends on 30 June 2025) was rather weak, offering 5 mpd on in-store FCY spend made in the following countries:

🇦🇺 Australia

🇯🇵 Japan

🇲🇾 Malaysia

🇹🇭 Thailand

Cardholders had to spend at least S$2,000 per calendar month to be eligible, and the bonus was capped at S$1,200 of in-store FCY spend.

Past promotions were significantly more generous, with 5 mpd offered without any geographical restrictions, a lower minimum spend of S$1,000 per calendar month, and a higher bonus cap of S$2,000 per calendar month.

Income tax payment facility

DBS Altitude Cardholders can pay their income tax via DBS Payment Plans, earning 1.5 mpd (instead of the usual 1.3 mpd) with a 2.5% fee. The cost per mile works out to 1.67 cents each. This is decent, but you could buy miles for less through a service like CardUp.

The article below summarises the lowest-cost way of paying taxes with your DBS Altitude Card and other credit cards.

With the loss of its bonus categories, the DBS Altitude Card is a pure vanilla general spending card, and while there are situations which call for that, most of the time you’ll want to keep your spending on 4 mpd alternatives.

The two lounge visits offered by the Visa version are useful, especially if you’re trying to rack up free visits without paying annual fees, but otherwise I don’t see much here to get excited about.

Since I’m never going to be new-to-bank for DBS anyway (I value my DBS Woman’s World Card too much to go one year without it), I do keep the Altitude handy, if only to wait for its bi-annual 5 mpd overseas spending promotions.

So that’s my review of the DBS Altitude Card. What do you think?

It is a truth universally acknowledged, that the boy who cries devaluation will eventually be proven right.

That said, I’ve been hearing rumours for some time now that Singapore Airlines plans to adjust its award redemption charts soon, and in my mind, its latest email to members all but confirms it.

To be clear, nothing has been officially announced yet. But I trust my sources on this, and as much as I’d love to be proven wrong, I would be amazed if we made it to the end of 2025 unscathed.

Singapore Airlines hints at upcoming changes to KrisFlyer

Yesterday, Singapore Airlines announced that from July 2025, the value of a KrisFlyer mile will be standardised at 1 cent each for spending on Singapore Airlines and Scoot commercial flights, Kris+ transactions, KrisShop purchases and Pelago bookings.

Until 30 Jun 2025

From 1 Jul 2025

Miles & Cash (SIA and Scoot)

105 miles = S$1 0.95¢/mile

100 miles = S$1 1¢/mile

Kris+

150 miles = S$1 0.67¢/mile

KrisShop

125 miles = S$1 0.80¢/mile

Pelago*

150 miles = S$1 0.67¢/mile

*Only full payment with miles allowed

On the one hand, this is a positive change because in every single case, the value of a mile will be higher than before. For Kris+ in particular, I imagine that those who transferred miles with the recent 35% transfer bonus will be chuffed to end up with a beefy 1.35 cents per mile, instead of the 0.90 cents they originally envisioned!

In the coming months, we will be introducing new benefits for KrisFlyer members as well as changes to the KrisFlyer programme.

-Singapore Airlines

Now, you can tell me I’m reading way too much into that, but “changes to the KrisFlyer programme” is a euphemism the airline has historicallytrotted out whenever devaluations take place.

Besides, this is in line with what I’ve been hearing from sources inside Singapore Airlines, who tell me:

A KrisFlyer devaluation is likely to take place this summer

The return of fuel surcharges on SIA award tickets has been discussed, but no final decision has been made

I don’t have any information as to how severe the devaluation will be, but I have written a detailed article that tracks how KrisFlyer award prices have evolved since the programme started in 1999.

Given the generally inflationary nature of mileage programmes, it might surprise you to know that some awards are even cheaper today than 25 years ago!

Why do I think a devaluation is likely?

It’s been three years since the last devaluation

From its inception in 1999 till today, KrisFlyer has updated its award charts a total of six times.

✈️ A History of KrisFlyer Devaluations

Devaluation (One-way Business Saver award from SIN)

Changes

October 2003 (NRT 27.6K | SYD 36.1K | LHR 51K) Fuel Surcharges

12 award zones expanded into 23

One-way awards now available for redemption, at 70% cost of round-trip

Option to purchase KrisFlyer miles introduced

February 2007 (NRT 29.8K | SYD 38.2K | LHR 51K) Fuel Surcharges

23 award zones consolidated into 14

Price of Unrestricted awards increased to 2X Saver (previously: 1.25-2X)

Companion awards removed

Saver awards blocked for latest First & Business Class cabin products

March 2012 (NRT 34K | SYD 46.8K | LHR 68K) Fuel Surcharges

Saver awards now available for all First & Business Class cabin products

March 2017 (NRT 43K | SYD 58K | LHR 85K) No Fuel Surcharges

Fuel surcharges removed

15% online redemption discount removed

January 2019 (NRT 47K, | SYD 62K | LHR 92K) No Fuel Surcharges

Waitlist “filled or killed” 14 days before departure

2 cabin upgrades from Y to J now permitted

July 2022 (NRT 52K, | SYD 68.5K | LHR 103.5K) No Fuel Surcharges

“Stopover trick” killed; no more option to add paid stopovers

Complimentary stopovers capped at 30 days max

✈️ May 2016’s “Devaluation”

Technically speaking, there was another devaluation in May 2016, though relatively minor. Europe 1 and Europe 2 were combined into a single award zone, which used the higher Europe 2 pricing. This led to a price increase for the four cities in Europe 1, namely Amsterdam, Athens, Copenhagen and Rome.

Devaluations used to take place at a cadence of 4-5 years, but more recently it’s been happening every 2-3 years. And perhaps that’s not surprising. With KrisFlyer recently reaching 10 million members globally, and more miles than ever in circulation, something has to give.

Since the last devaluation took place in July 2022, there’s good reason to believe that 2025 will see another award chart adjustment.

Capacity constraints increase the opportunity cost of award seats

“To be very candid with you, our planning horizon is being controlled by Boeing and Airbus. Unfortunately, there have been a fair number of delays by the aircraft manufacturers, in part because of the pandemic, in part because some of them have production issues and constraints (strikes, etc.).

Our deliveries, like with many other airlines, have been delayed. At this point in time, we do not have very strong visibility on how the deliveries will come about, consequently impacting our expansion plans.”

-Singapore Airlines RVP for Europe

I suppose he was being diplomatic by not singling out a specific company (“Boeing and Airbus”), but everyone knows that the entire SIA backlog is with Boeing.

SIA currently has 48 Boeing aircraft on order: 5 B787-10s, 12 B737-8 MAXs, and, of course, 31 of the infamously-delayed B777-9s. However:

The airline only expects to receive seven aircraft by the end of the current financial year (31 March 2026), of which five will be narrow-body B737-8 MAXs— the most recent, 9V-MBQ, came after a 30-month gap in deliveries

The first of the 31 Boeing 777-9s won’t arrive until late 2026 at the earliest, and possibly (likely?) even in 2027

All that to say, when load factors are high and aircraft are in short supply, the opportunity cost of releasing seats for awards instead of selling them for cash is high. That then puts pressure on the award charts to be adjusted accordingly.

Singapore Airlines A380 Suites

It doesn’t help that SIA only has 160 Suites and First Class suites in its fleet today, compared to more than double that pre-COVID. This is largely due to A380-800 retirements and refits, where the Suites cabin was cut from 12 seats to six.

While it will improve in time with the arrival of the B777-9s (where the First Class cabin is rumoured to be 50% larger than the B777-300ERs) and the addition of a 4-seat First Class cabin on the A350-900 ULRs, we now have a lot of miles chasing very few seats, and I don’t have to tell you what that results in.

New cabin products are coming

Singapore Airlines new Business Class | Credit: Singapore Airlines

Singapore Airlines will unveil its next generation First and Business Class seats in early 2026, with the first refit aircraft expected to enter service in Q2 2026. We don’t know much about how the new seats will look, but what we do know is that historically, there has been a close correlation between new seats and award chart devaluations.

Singapore Airlines 2006 Business Class

For example, in October 2006, SIA debuted new First and Business Class seats on the B777-300ER. The following month, it announced that award charts would be devalued from February 2007, and Saver redemptions would not be allowed for aircraft with the new cabin products.

Another KrisFlyer devaluation took place about a year before the launch of the current generation First and Business Class seats in 2013, and further KrisFlyer devaluation took place in March 2017, ahead of the unveiling of the new A380 cabin products later that year.

Rebasing KrisFlyer mile value to 1 cent each

Singapore Airlines’ decision to standardise the value of a KrisFlyer mile to 1 cent each across all platforms doesn’t feel like something you do in isolation. It has broader implications for how the company measures the value of its outstanding liabilities, and it stands to reason that award chart prices will also need to be adjusted to reflect this new valuation.

Other mileage programmes have adopted a standardised value per mile as a precursor to fully dynamic award pricing, where the number of miles required is tied to the cash price of a ticket. Even though I highly doubt that KrisFlyer will go that far with its next devaluation, we might see a “dynamic-lite” model introduced with peak and off-peak award pricing.

What should you do when a devaluation happens?

Completely normal phenomenon

It really boils down to how bad the devaluation is.

If the price increases are mild, you might want to book a couple of speculative trips at the current prices, but otherwise keep the rest of your powder dry. If the award chart is gutted, then you’ll probably want to drain your entire balance.

For perspective, here’s how Saver award prices changed during the past six devaluations (with the caveat that past performance etc. etc.).

✈️ KrisFlyer Devaluations Min Increase | Max Increase

Economy

Business

First

Oct 2003

-32% | 2%

-31% | 0%

-19% | 13%

Feb 2007

-8% |13%

-10% |13%

-7% |11%

Mar 2012

0% | 9%

0% | 45%

0% | 30%

Mar 2017

18%| 32%

18%| 42%

18%| 59%

Jan 2019

0% | 0%

7% | 12%

6%| 10%

Jul 2022

8%| 16%

10%| 15%

10%| 15%

Based on Saver prices for SIA redemptions

Either way, you will have approximately one month to book awards at the existing prices, based on past experience. Remember, you don’t need to travel before the devaluation, but you must book before it comes into effect.

Award tickets can be booked up to 355 days in advance, and new inventory is loaded daily at (all times SGT):

8 a.m (All destinations except USA)

1 p.m (EWR/JFK)

4 p.m (LAX/SEA/SFO)

Do note that any waitlists which clear after the effective date of the devaluation will be charged at the new prices, even if you joined the waitlist prior to this date. Likewise, any changes made to award tickets after the devaluation that involve reissuance (e.g. changing route, cabin or award type) will require a top up of the miles difference.

Date changes and flight number changes on the same route (e.g. you want to take an earlier flight to Bangkok) do not require reissuance.

Conclusion

Will we see a KrisFlyer devaluation in 2025?

Singapore Airlines has hinted that the coming months will see “new benefits” for members as well as “changes” to the KrisFlyer programme. We’ll need to wait for the full details, though I can’t see that as pointing to anything other than an award chart devaluation.

This, of course, is simply part and parcel of the miles game. Nothing stays the same forever, and if the idea of a devaluation keeps you up at night, you’re probably keeping too large a miles balance on hand.

What does your Spider Sense say about a KrisFlyer devaluation?

In addition to redeeming award flights, KrisFlyer members can also spend their miles like cash to pay for Singapore Airlines and Scoot tickets, KrisShop purchases, Pelago experiences and Kris+ transactions. However, the value per mile can vary widely across these options, often causing confusion.

But this will soon be a thing of the past, as Singapore Airlines will introduce a standardised redemption rate of 100 KrisFlyer miles = S$1 across all platforms on 1 July 2025— boosting the value per mile by 5-50%, depending on the use case.

“These enhancements to the KrisFlyer redemption rates deliver more value to members, while making miles redemption more intuitive and consistent. Members will get more from every mile when booking flights, dining out, shopping, or enjoying travel experiences. This is all part of our commitment to rewarding loyalty with meaningful benefits that truly enhance the KrisFlyer experience”

-Bryan Koh, DVP Loyalty Marketing, SIA

KrisFlyer to standardise redemption rates

Until 30 Jun 2025

From 1 July 2025

Miles & Cash (SIA and Scoot)

105 miles = S$1 0.95¢/mile

100 miles = S$1 1¢/mile

Kris+

150 miles = S$1 0.67¢/mile

KrisShop

125 miles = S$1 0.80¢/mile

Pelago*

150 miles = S$1 0.67¢/mile

*Only full payment with miles allowed

Singapore Airlines KrisFlyer members can use their miles to pay for:

Commercial tickets with Singapore Airlines and Scoot

Purchases at Kris+ merchants

Purchases on KrisShop

Experience bookings with Pelago

Members can mix miles and cash in whatever proportion they wish, with the exception of Pelago, where only full payments with miles are permitted.

The current redemption rate ranges between 105-150 KrisFlyer miles = S$1, or 0.67 to 0.95 cents per mile. Honestly speaking, there’s very little logic behind this— unless perhaps the goal is to incentivise some types of redemptions over others (or maybe you believe that KrisShop prices are naturally inflated, so a higher valuation is in order!).

From 1 July 2025, the redemption rate across the entire KrisFlyer ecosystem will be harmonised to 100 KrisFlyer miles = S$1, or 1 cent per mile, with the following minimum redemption amounts:

Miles & Cash with Singapore Airlines and Scoot: 1,000 miles (S$10)

Kris+: 10 miles (S$0.10)

KrisShop: 1,000 miles (S$10)

Pelago: 1,000 miles (S$10)

This is actually great news if you have miles that are stuck in Kris+, either because you forgot to transfer them to KrisFlyer or because they can’t be transferred (such as miles earned from referrals). By simply waiting a week, their value will appreciate by 50%!

And if you happened to take advantage of the recent 35% transfer bonus between KrisFlyer and Kris+ (or any transfer bonus in the past six months), your faith is going to be rewarded. For example, if you transferred 10,000 KrisFlyer miles into 13,500 KrisPay miles (35% bonus), that stash will soon be worth S$13.50, a very decent 1.35 cents per mile.

However, you might remember that prior to August 2021, the rate offered for Miles & Cash for Singapore Airlines flights was 980 miles = S$10, so even with the change we’re still slightly worse off than “the good old days”, though frankly the difference is marginal.

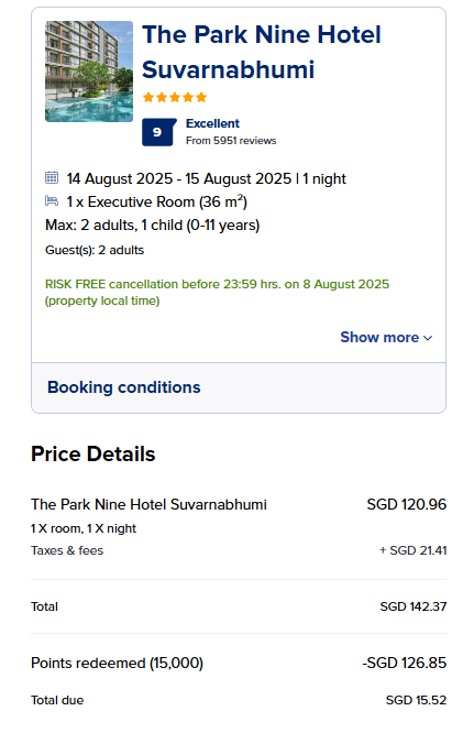

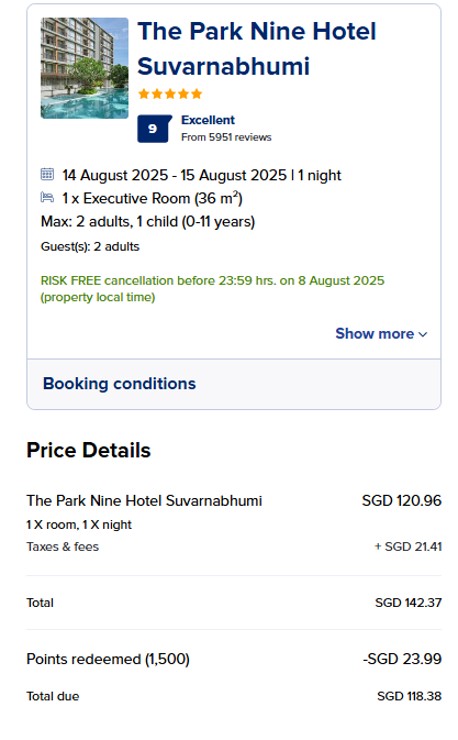

Interestingly enough, it seems like KrisFlyer vRooms (remember that?), Singapore Airlines’ portal for rental car and hotel bookings, has been forgotten completely.

It’s not addressed in the press release that Singapore Airlines sent out, so I can only surmise that the current value of 0.8 cents per mile will continue until further notice.

👍 You can get >0.8 cents per mile with KrisFlyer vRooms!

0.8 cents per KrisFlyer mile refers to the incremental value offered through KrisFlyer vRooms. But it’s actually possible to get a higher valuation, provided you redeem just the minimum number of miles (1,500 miles) required.

For example, in this booking I’ve redeemed 1,500 miles, which takes S$23.99 off the total bill, or 1.6 cents per mile. As I start to redeem more miles, however, the average value will decrease (because the incremental value is just 0.8 cents per mile).

Is it worth spending miles this way?

It should be noted that even with the enhanced value, 1 cent per KrisFlyer mile is not exactly a great way of spending them.

Award flights continue to be the best way of using miles, with valuations of 4-5 cents easily achievable (it’s debatable whether you can really value a mile that high if you weren’t willing to pay for First or Business Class with cash, but that’s another topic for another time).

💰 KrisFlyer Miles Redemption Value (from 1 July 2025)

Redemption Option

Value Per Mile

✈️

Award Flights with SIA or Partner Airlines

2+¢

🛍️

Cash + Miles, KrisShop, Pelago, Kris+

1¢

🚘

Book Hotels or Rental Cars on KrisFlyer vRooms

≥0.8¢

🏨

Shangri-La Circle Conversion

0.74¢

🏬

CapitaStar Conversion

0.70¢

🛒

yuu Rewards Club Conversion

0.66¢

🏨

Accor Live Limitless Conversion

0.64¢

🛒

LinkPoints Conversion

0.60¢

🏨

Marriott Bonvoy Conversion

0.50¢

⛽

Esso Smiles Conversion

0.47- 0.67¢

However, if you’re dealing with a small number of expiring KrisFlyer miles, and don’t have plans to travel, then getting some value would be better than no value at all

What this does at least is to draw a clear distinction between spending KrisFlyer miles within the core ecosystem, and outside of it.

In other words, from 1 July onwards there’s really no reason why you should even consider converting KrisFlyer miles into yuu Points, or Accor points, or CapitaStars, or any of the other options available, when you can easily get 1 cent per mile through Kris+ with a minimum spend of just 10 miles.

Conclusion

From 1 July 2025, Singapore Airlines will standardise the value of a KrisFlyer mile to 1 cent each, whether you’re paying for SIA and Scoot flights, or spending them via Pelago, Kris+ or KrisShop.

There’s very little to dislike about this, since it represents a 5-50% enhancement in value over the status quo. That said, I don’t want to sound like a Debbie Downer, but it’s always a little concerning when mileage programmes begin to standardise the value of a mile. We have seen other programmes do this as the precursor to revenue-based redemptions, where award charts are removed and the number of miles required for a redemption flight varies depending on the cash price. I’m not saying that will definitely happen here too, but perhaps a decade of miles collecting has made me paranoid!

While online shopping is obviously more convenient, there are still situations that call for in-person purchases.

A merchant may simply not have an online storefront, or even if they do, visiting a brick-and-mortar location to negotiate can get you discounts or extras that you wouldn’t get online. I recently bought a display set TV from Courts at nearly 50% off the list price, something I wouldn’t have been able to do online.

But just because you’re spending in-store doesn’t mean you have to give up online spending bonuses!

Which cards earn bonuses for online spending?

The two cards that should instantly come to mind for online spending are the DBS Woman’s World Card and Citi Rewards Card, both of which earn 4 mpd for online spending.

*Min. S$1,000 on SIA Group for membership years ending November 2025 onwards

The KrisFlyer UOB Credit Card earns an uncapped 2.4 mpd for online shopping transactions, defined as merchants with the following MCCs.

KrisFlyer UOB Credit Card bonus-eligible MCCs

MCC

Examples

4816 Computer Network/ Info Services

GoDaddy, Twitch, Peatix

5309

Duty Free Stores

DFS, KrisShop, The Shilla

5310

Discount Stores

Lotte Mart

5311 Department Stores

Taobao, Isetan, Marks & Spencer

5331 Variety Stores

Muji, Mustafa, Miniso

5399

Misc General Merchandise

Iuiga, Japan Home, Comgateway

5611

Men’s Clothing

Benjamin Barker, Dockers, Superdry

5621

Women’s Ready to Wear

bYSI, Coast, Forever21

5631

Women’s Accessories

Bimba Y Lola, Chomel, Coach

5641 Children’s and Infants’ Wear

Abercrombie Kids, Cotton On Kids, Kidstyle

5651

Family Clothing

ASOS, Bossini, Desigual

5661 Shoe Stores

ALDO, Bata, Birkenstock

5691

Men’s and Women’s Clothing

Prada, G2000, Ezbuy

5699 Accessory and Apparel

LeSportsac, Crumpler, Esprit

5732-5735

Electronics, Music Stores, Computer Software

Apple, Audio House, MealPal

5912 Drug Stores and Pharmacies

Guardian, NTUC Unity, Watsons

5942 Book Stores

Book Depository, Kinokuniya, Books Actually

5944-5949

Jewelry, Watches, Toys, Camera, Gift Cards, Leather Goods, Sewing

Cartier, Action City, Canon

5999

Misc. and Specialty Retail

Atome, Amazon, eBay

The StanChart Journey Card earns 3 mpd for online groceries, food delivery, transport, though this only applies to transactions charged in SGD.

StanChart Journey Card bonus-eligible MCCs

MCC

Examples (non-exhaustive)

Groceries MCC 5411

NTUC FairPrice Online, Lazada Redmart

Bakeries MCC 5462

Bengawan Solo, BreadTalk, Four Leaves

Misc. Food Stores MCC 5499

Bottles and Bottles, Famous Amos, Irvins Salted Egg

Liquor, Wine or Beer Stores MCC 5921

1855 The Bottle Shop, The Oaks Cellars, Grand Cru

Food Delivery* MCC 5811 MCC 5812 MCC 5814

GrabFood, Deliveroo, Foodpanda

Transport MCC 4111 MCC 4121 MCC 4789

Grab rides, Comfort taxi, gojek

Cruise Liners MCC 4411

Royal Caribbean, Princess Cruises, Norwegian Cruise

*Despite the name, the bonus would be equally applicable in situations where a restaurant has online ordering for dine-in (e.g. scan a QR code menu and pay online before receiving your food)

Finally, the HSBC Revolution Card awards bonuses for online spending on department and retail stores, dining, transport and membership clubs (bonuses for offline spending were removed in June 2024).

HSBC Revolution bonus-eligible MCCs

Category

MCCs

Department Stores & Retail Stores

4816, 5045, 5262, 5309, 5310, 5311, 5331, 5399, 5611, 5621, 5631, 5641, 5651, 5655, 5661, 5691, 5699, 5732 to 5735, 5912, 5942, 5944 to 5949, 5964 to 5970, 5992, 5999

Dining

5441, 5462, 5811, 5812, 5813

Transport & Membership Clubs

4121, 7997

So if you’re spending with these five cards, the question then becomes: is it possible to turn an offline transaction into an online one?

⚠️ When you don’twant a transaction to be online

There’s actually one card which penalises you for turning offline transactions into online: the Maybank World Mastercard. Cardholders earn 4 mpd on petrol transactions in Singapore, but only when paying offline. If you pay online (e.g. via Kris+), you will not earn the bonus.

Atome transactions code as online, whether they’re performed on a website, in-app, or physically in-store. This not only lets you turn offline spend into online, it also allows you to use credit cards at merchants which might not otherwise accept them.

Your payment will code as MCC 5999, and split into three interest-free instalments. The first payment is due at the time of the transaction, and it’s advisable to trigger the 2nd and subsequent payments manually via the Atome app as there have been reports that automatic payments do not trigger online spending bonuses.

For a recommended list of cards to use with Atome, refer to the post below.

Gift card purchases through websites like Giftano, HeyMax, ShopBack and Wogi all count as online transactions.

You can then use those gift cards for in-store transactions at places including Best Denki, Challenger, Cold Storage, Courts, Giant IKEA, Natureland, Shell, and Sheng Siong.

MCC 5311 MCC 5399 Amazon processes transactions over a range of MCCs, so use a card that awards bonuses for general online spend

Amazon

Courts

Challenger

Best Denki

Dairy Farm

Eu Yan Sang

IKEA

Klook

NTUC FairPrice

TADA

MCC 5999

Amazon

Best Denki

Cold Storage

Courts

Dairy Farm Group

eCapitaVoucher*

Eu Yan Sang

Giant

Grab

Guardian

IKEA

Lazada

NTUC FairPrice

Sheng Siong

TANGS

ZALORA

*Admin fee of up to 5% applies to purchases

MCC 5311

Amazon

Best Denki

Courts

Deliveroo

Foodpanda

Giant

Grab

IKEA

Klook

Lazada

Natureland

NTUC FairPrice

Oddle Eats

Pelago

Ryde

Shein

Shell

Sheng Siong

TADA

TANGS

ZALORA

MCC 5812 MCC 5814 MCC 5311 ShopBack processes transactions over a range of MCCs, so use a card that awards bonuses for general online spend

Amazon

Foodpanda

Gojek

Grab

IKEA

Lazada

NTUC FairPrice

Ryde

Shell

Shopee

TADA

Uniqlo

MCC 5947

Amazon

Best Denki

Caltex

Challenger

Cold Storage

Courts

Giant

GrabGifts

Guardian

IKEA

iStudio

Klook

Lazada

Muji

NTUC FairPrice

Shell

Shopee

TADA

TANGS

Trip.com

Watsons

I found this particularly useful when buying my TV from Courts, in a month when I’d already maxed out the 4 mpd caps with the UOB Visa Signature and UOB Preferred Platinum Visa.

I was still able to earn 4 mpd by purchasing Courts gift cards via HeyMax using my Citi Rewards Card and HSBC Revolution, then redeeming them in-store (yes, the OCBC Rewards Card would have offered 6 mpd, but I’d also maxed that out for the month).

Get S$5 (in the form of 750 KrisPay miles) when you sign-up with code W644363 and make your first transaction

Kris+ transactions code as online spend, whether you’re buying deals via the app or making in-store payments. The original MCC is usually maintained, though there are some very limited exceptions (mostly for travel agencies).

For a recommended list of cards to use with Kris+, refer to the post below.

ShopBack Pay transactions code as online, even if in-store

Payments made via Shopback Pay or FavePay will code as online spend, even when payment is made in-store.

These transactions usually (but not always) retain the MCC of the underlying merchant. However, do note that DBS cards explicitly exclude FavePay, so don’t use the DBS Woman’s World Card here.

Frasers Experience

FRx gift cards can be used at any participating store inside of Fraser malls

FRx Experience gift cards can be used to make payment at most merchants inside Frasers malls. This includes clinics, tuition/enrichment centres, and other places that might not otherwise be eligible for bonuses.

Causeway Point

Century Square

Eastpoint

Hougang Mall

Northpoint City

Tampines1

The CentrePoint

Tiong Bahru Plaza

Valley Point

Waterway Point

White Sands

Gift card purchases will code as MCC 5965, and while this isn’t whitelisted by any particular card, it’s still eligible for 4 mpd with the Citi Rewards and DBS Woman’s World Card.

Do Apple Pay and Google Pay count as online transactions?

Google Pay is online if it’s online, and offline if it’s offline!

I might as well address this too, given how often it comes up.

Asking “do Apple Pay and Google Pay count as online transactions” is a very strange question. It’s a bit like asking “do credit card payments count as online transactions”. They do, if you make payment online!

When you use Apple Pay and Google Pay to make in-store payments, it’s conceptually similar to tapping your physical card to pay, and considered an offline transaction.

When you use Apple Pay and Google Pay to make an in-app or website-based payment, it’s conceptually similar to entering your card details in the app or website, and considered an online transaction.

Conclusion

While some cards will only award bonuses for online spending, that doesn’t necessarily mean that physical stores are off-limits. By buying gift cards, paying with certain apps, or using Amaze, you can convert that transaction into an online expenditure.

I’m guessing there are probably other ways that I’ve missed out, so feel free to share other options in the comments too!

What other ways do you know of turning offline spend into online spend?

Here’s The MileLion’s review of the KrisFlyer UOB Credit Card, aimed at those who want a co-branded Singapore Airlines card with broader acceptance than American Express.

While I’m not a fan of its debit card sibling, the credit card offers two compelling features: uncapped bonuses on Singapore Airlines and Scoot tickets, KrisShop, Kris+, and Pelago, as well as dining, food delivery, online shopping, travel and transport (known as “Accelerated Miles”).

Unfortunately, the Accelerated Miles feature was recently nerfed. Previously, it offered an uncapped earn rate of 3 mpd, but this was reduced to 2.4 mpd from 1 June 2025. In addition, the minimum annual spend on Singapore Airlines Group transactions required to unlock this rate was increased from S$800 to S$1,000.

Despite these changes, the card remains a solid option for high spenders who regularly exceed bonus caps on other cards, or for those who prefer the convenience of using a single card for most of their spending.

The KrisFlyer UOB Credit Card may not offer the highest earn rates in every category, but its uncapped bonuses make it a great choice for big spenders, or those who prefer to stick to a single card.

👍 The good

👎 The bad

Uncapped 3 mpd on SIA and Scoot tickets, KrisShop, Kris+, and Pelago

Accelerated Miles feature offers uncapped 2.4 mpd on dining, food delivery, online shopping & travel, and transport

No conversion fees

2x S$15 Grab vouchers for airport rides each year

Accelerated Miles rate cut to 2.4 mpd, with min. spend hiked

Accelerated Miles are only credited after the end of the membership year

Be careful not to confuse the KrisFlyer UOB Credit Card with the KrisFlyer UOB Debit Card. The two sport similar designs and names, but the value proposition is altogether different.

Credit Card

Debit Card

Min Income Req.

S$30,000

N/A

Annual Fee

$196.20

S$54.50

Base Earn Rate

1.2 mpd

0.4 mpd

Requires KrisFlyer UOB Savings Account?

No

Yes

Simply put: if you earn enough to qualify for a credit card, there’s very little reason to consider the debit card option.

In fact, the only thing that debit card does that the credit card can’t is to earn miles on insurance premiums– and even then, just 0.4 mpd.

How much must I earn to qualify for a KrisFlyer UOB Credit Card?

The KrisFlyer UOB Credit Card has a minimum income requirement of S$30,000 per year, the MAS-mandated minimum.

If you do not meet the minimum income requirement, it may be possible to place a S$10,000 fixed deposit with UOB to get a secured version. Contact your nearest UOB branch for more details.

New-to-UOB customers who apply and are approved for a KrisFlyer UOB Credit Card will enjoy up to 25,000 bonus miles when they spend at least S$2,000 in the first 60 days of approval.

This offer is currently scheduled to end on 28 February 2025, but has been renewed every month for more than a year now.

❓ New-to-UOB definition

New-to-UOB is defined as customers as those who:

do not currently hold a principal UOB credit card, and

have not cancelled a principal UOB credit card in the past six months